LLY - Hutchmed: Attractive Chinese R&D Giant

2023-08-11 17:59:00 ET

Summary

- Hutchmed (China) Limited, a Chinese biopharma company, has experienced fluctuations in its stock price but has potential for improvement.

- The company acts as a liaison between the healthcare systems of China and the U.S., working to get its products approved in both countries.

- Hutchmed (China) Limited has a vast pipeline of products, with several in clinical trials, and has major collaborations with companies like Takeda and AstraZeneca.

We covered Hutchmed (China) Limited ( HCM ), a Chinese biopharma major, in 2017. A lot has happened to the company in the last 6 years. Although the stock is actually down 36% from the 2017 prices, that is probably not the correct way to look at it, because at least twice in those years, the stock had nearly doubled, so there was a lot of scope to make good profits. The stock is now trading at $14, a low price which we also saw in 2017; HCM reached its lowest in Oct. 2022, at $8 - what I am trying to say is, there seems to be potential for improvement now. Let us dig in.

HCM is a Hong Kong-based company with a very extensive product and pipeline set, and collaborations with major biopharma companies. HCM's business model is this - HCM works as a liaison between the healthcare systems of China and the U.S., more or less. It has certain products and assets it ran through trials in China and received approvals there, and then it is endeavoring to get them approved in the U.S. It has certain other assets that were originally US approved by another company; HCM then partnered with that company to bring that product to China.

In the latter class fall Epizyme's tazemetostat, which was approved in the U.S. in 2020, and Epizyme was acquired by Ipsen; meanwhile, HCM got it approved in China last year. In the former class is fruquintinib, which was approved in China in 2018, and has a November PDUFA date in the US. They have two other approved products - surufatinib and savolitinib - both of which are approved in China. Savolitinib is under US development through a partnership with AZN, while surufatinib was rejected by the FDA last year.

In its rejection letter, the FDA told Hutchmed - which was developing surufatinib all by itself - that the FDA wants to see a "multiregional clinical trial with individuals more representative of the U.S. patient population and in accordance with U.S. medical practice." This is going to be a recurrent problem for Chinese companies working their way through the U.S. system. A few Chinese companies are bypassing the problem by losing their entire Chinese identity, showing their HQs in Boston or CA, and running trials in the U.S. This is fine, but then they lose the vast and (for them) easily accessible China market. A few others are doing what Hutchmed is doing - having both identities clearly visible - but they are facing the problem of an increasingly protective U.S. market.

The way out for Hutchmed is to run trials here in the U.S., but this is expensive. A good way is to partner out with more U.S.-settled companies; like AZN, a British behemoth which has no problem working in the U.S., and has a very large presence here. Critics can claim - rightly - that it is not fair for Hutchmed to call such US trials expensive, because the added expense is more than accounted for by the very large U.S. market. They also have an advantage: having run trials for that molecule in China, they know exactly what to expect, and while the FDA will balk at giving them any advantage of using past data, that data can certainly inform their U.S. trial choices, and make them more efficient.

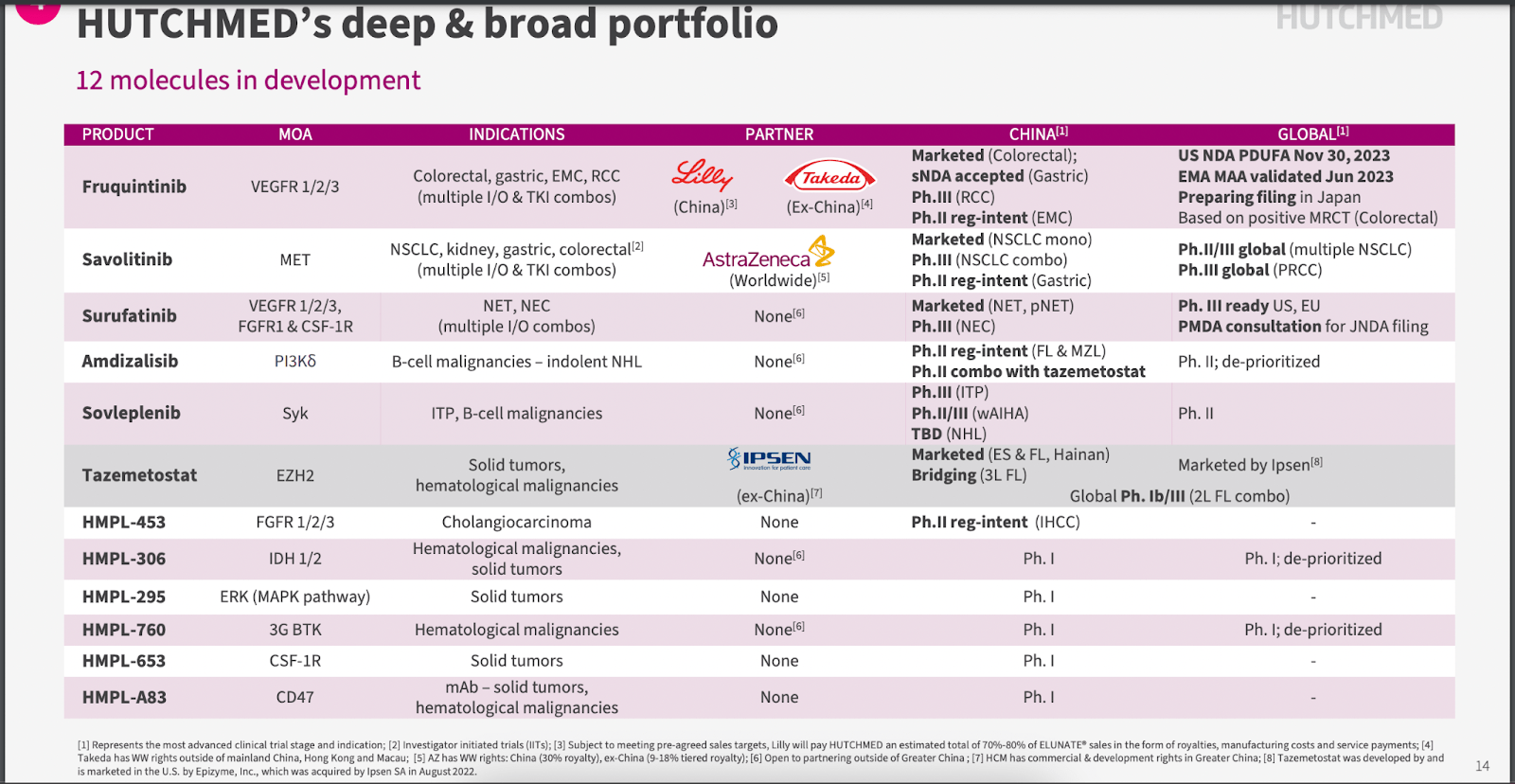

The company's pipeline is vast, with 12 clinical-stage products and 40 clinical trials. 3 of these trials have "registration-intent." 6 of these molecules have global trials ongoing - meaning they are being developed in the U.S. as well.

Here's a look at HCM's deep moated portfolio:

{kind=link}

They have 12 molecules in trials, all in hematology-oncology. Besides the marketed and PDUFA-ready products, the latest stage asset is savolitinib in a phase 3 trial in the US targeting NSCLC and Papillary renal cell carcinoma, or PRCC. Surufatinib is also phase 3 ready in the U.S. targeting neuroendocrine tumors and carcinomas.

The lead asset in the U.S. is fruquintinib, which is the 12th VEGF inhibitor to be launched in the U.S. Its differentiating factors are that, first, it is a small molecule, two, it is specific to just VEGF receptors 1, 2 and 3, unlike other "dirty" VEGFis which inhibit just about everything; and three, it targets colorectal cancer, a relatively uncrowded space for VEGFis. Data supporting the NDA comes from the FRESCO-2 trial, which showed a clear benefit in safety and efficacy for fruquintinib over standard of care, which here was regorafenib. Takeda has rights to fruquintinib in the U.S. Some analysts peg ex-China revenue from this molecule at around $300mn at peak in the 3L CRC setting; thus, for Takeda to recover its costs, it has to work harder to get fruquintinib approved in earlier line settings.

Financials

HCM has a market cap of $2.46bn and a cash balance of $850mn. This year, Takeda paid them $400mn upfront for fruquintinib (as well as $730mn in potential milestones plus royalties). Their:

"consolidated revenue was up by 164% from around $200 million to over $530 million, mainly contributed by the recognitions of the upfront income from Takeda, around $260 million."

Net Expenses for the six months ended June 30, 2023, were $364.3 million. The company plans to become profitable by 2025.

HCM has major deals with Takeda (TAK), AstraZeneca (AZN), Ipsen (IPSEF), and Eli Lilly (LLY). Smart money holds 75% of the stock, while retail holds 25% - a distribution I have come to prefer.

Bottom Line

Hutchmed (China) Limited is trading midway between its 52-week highs and lows. For those who are fine with the risks associated with investing in what are essentially Chinese stocks, HCM is attractive because it is an emerging big pharma, a big pharma in the making. HCM's R&D abilities are outstanding, and it is the face of China's emergence as a biopharma R&D destination. The bottom line, for some investors, HCM at current prices makes an attractive investment option.

For further details see:

Hutchmed: Attractive Chinese R&D Giant