HYB - HYB: Buy The Wide 14% Discount

2023-12-29 06:18:27 ET

Summary

- The New America High Income Fund is a fixed income closed-end fund focused on U.S. high yield.

- HYB follows a conservative strategy in managing leverage and collateral quality. It's willing to cut dividends to maintain sustainability, avoiding return of capital utilization.

- HYB has a long performance history since its inception in 1988. It aims to preserve NAV over the long term and has shown resilience through various credit cycles.

- The fund faced challenges due to the mismatch between its fixed-rate collateral and the floating-rate leverage obtained through a bank facility. This led to reduced net interest income amid rising rates but is expected to reverse when rates decrease.

- Despite its conservative approach and solid underlying performance, the market has undervalued HYB, leading to a substantial discount to NAV, currently at -14%.

Thesis

The New America High Income Fund (HYB) is a fixed income closed-end fund that we own and have covered before on the Seeking Alpha platform. The fund has a very long performance history, being in the market since 1988. The fund is conservatively run when it comes to leverage and quality of the collateral, and it does not hesitate to cut its dividend when distributions start requiring return of capital utilization. We like this approach, and retail investors should too, since it flags sustainability on a long term basis:

On a longer time-frame, retail investors should look for CEFs that always see their NAV return to their original start-points after recessions pass. On a 5-year time-frame HYB's NAV is down only -7%, and be assured that as rates decrease further in the next 18 months the fund will see its NAV go back to a 0% net move.

That is what you want to see as an investor because it tells you the CEF is employing leverage only to increase its distribution, but it is not taking cash out of the principal portion in order to pay unsupported high dividend yields.

The CEF has been dragged down in the past two years by its assets/liabilities mismatch, with most of its collateral being fixed rate, while its leverage is obtained via a floating rate bank facility. Higher rates have thus translated into a compressed net interest income for the fund. That is set to reverse once rates start moving lower.

The market is unjustly punishing the fund's conservative stance

Despite the significant sell-off in rates recently and the fund's solid underlying performance the discount to NAV is very high:

We can see from the above graph courtesy of YCharts that the CEF usually sees its discount in the -10% to -12% range in a normalized rates environment, with fluctuations as rates move up or down. In the 2020/2021 zero rates environment the fund traded even at a premium to NAV (it was overpriced at that level). Currently we find it to be underpriced from a discount to NAV perspective.

We feel in today's environment where the chorus for a soft landing grows louder but the certainty is not there, a fund like HYB which chooses to keep ROC utilization at a minimum and approach NAV preservation from a conservative viewpoint is punished unjustly. The fund currently has a 7% distribution yield which by all means is not attractive when compared to 10% plus figures observed for other fixed income CEFs. However the fund has shown time and time again that it is a long-term performer that has successfully navigated many credit cycles. Furthermore, the CEF has announced a special dividend of $.0475 per share payable in January:

Boston, Massachusetts, December 18, 2023 -- The New America High Income Fund (the "Fund") (NYSE: HYB) announced today that it will pay a special dividend of $.0475 per share on the company's common stock on January 31, 2024 to common shareholders of record as of the close of business on December 29, 2023. The ex-dividend date will be December 28th.

Conservative portfolio

The fund does not take excessive credit risk via its portfolio composition:

Ratings (Semi-Annual Report)

The CEF has a balanced approach, where BBB and BB names represent roughly 35% of the collateral, while single-B names make up 47% of the holdings. The riskiest CCC names are just 14.25% here.

The fund does not take industry concentration risk, and its highest exposure is to the Energy sector:

Sectors (Semi-Annual Report)

We like energy here, and are actually bullish energy equities and energy futures. Being long energy bonds is a very conservative stance on a sector that has significant upside in our mind. Energy companies have learned their lesson after Covid, and balance sheet strength became a priority after Covid. Balance sheet strength translated into significant debt repayments, with many names having debt/Ebitda ratios of around 1x now versus 4x prior to the pandemic.

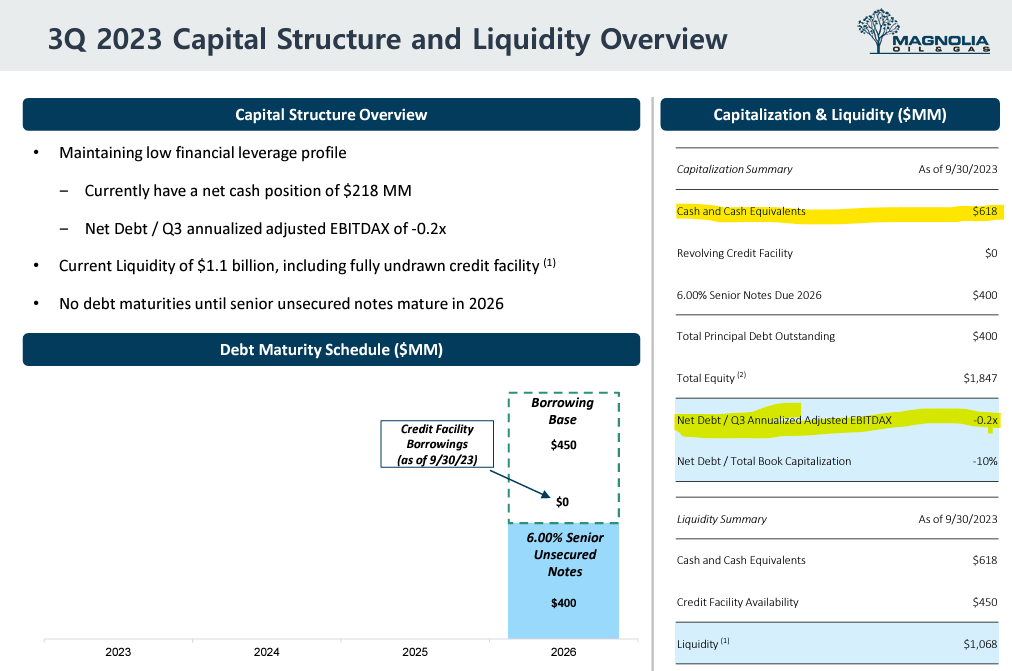

As an example, let us have a look at one of the line items from the fund's collateral line, namely the 'Magnolia Oil and Gas Operating LLC' notes:

{kind=link}

Magnolia ( MGY ) is an E&P company that has a very conservative balance sheet:

{kind=link}

Magnolia is a company that has $400 mm in notes outstanding with a 2026 maturity. The CEF contains a piece of that debt. What is interesting about MGY is that they have $618 mm in cash on their balance sheet, meaning their net debt is zero. Yes, you read that correctly. They could just pay down the entire debt portion tomorrow if they wanted to. They are not doing that because the coupon is very low (i.e. 6%) and the cash on the balance sheet gives them the flexibility of acquisitions, all while paying an interest rate close to what they have to pay on their debt (short term T-bills yield in excess of 5.2%). Is there any credit risk with owning MGY debt right now? Not really. Yet the company is rated BB (the 'Ba' equivalent by Moody's).

The one item that can be improved - leverage

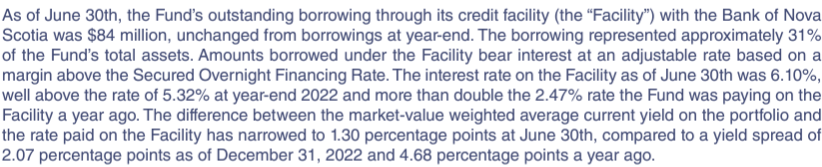

The fund employs leverage via an $84 million bank facility:

Assets & Liabilities (Semi-Annual Report)

The bank facility is set at roughly SOFR+100 bps, meaning it has exhibited an increasing cost as rates have moved higher:

{kind=link}

The fund suffered spread compression due to this assets/liabilities mis-match, and we would have liked to see the leverage move down to mitigate that. Unfortunately we did not see that happen. As an example (yet we are not the portfolio managers here) we would have sold the MGY piece of debt we discussed above and paid down some of the leverage. Why? Because the MGY note is trading at a very tight spread given its conservative balance sheet, which translates into an all-in yield close to what the CEF is paying on its own debt (the MGY note is trading close to par, meaning the all-in yield pretty much matches what the fund pays on the leverage).

As rates move lower, the fund will benefit from lower costs on its bank facility while the collateral is mostly fixed rate (outside a 8% sleeve for lev loans).

Performance

The fund is up over 16% this year from a total return perspective:

The fund's NAV and market price moved fairly similarly this year, with the rest of the total return coming from the dividend yield. Long term the fund compares favorably with other names in space

Conclusion

HYB is a fixed income CEF. The fund has been in the market since the late 80s and is run conservatively, aiming for stable NAV when utilizing long time frames. The vehicle's portfolio is 90% fixed rate, while its bank leverage facility is based on SOFR. This assets/liabilities mismatch has reduced net interest spread during the current high rate environment, and has caused the fund to cut its dividend this year in order to avoid ROC utilization. The market has unjustly punished the CEF, with the fund currently exhibiting a -14% discount to NAV. In a base case soft landing scenario we anticipate a +15% total return here, with 5% coming from the discount narrowing, 7% from its dividend yield and 3% from rates moving lower and the fund generating a higher net spread. We feel the current discount to NAV is too high for this long term performer, and the fund is a buy at the current levels.

For further details see:

HYB: Buy The Wide 14% Discount