HYB - HYB: Revisiting This High Yield CEF After The Dividend Cut

2023-05-30 13:43:49 ET

Summary

- The New America High Income Fund is a U.S. high-yield closed-end fund that has been around for almost 40 years and has gone through various market cycles.

- The fund cut its dividend in 2023, leading to a widening of the discount to NAV, which is now close to -17%.

- The article suggests that the market has responded erroneously to the dividend cut, but that the discount may not be corrected until the next cyclical bull market.

- HYB remains a Hold for its conservative positioning, as reflected in its ratings parsing and yield coverage.

Thesis

The New America High Income Fund ( HYB ) is a U.S. high-yield closed-end fund. We have covered this name before here , where we thought it would be a good time to buy into the name on the back of one of the panic selling moments in last year's market. We did not expect the Fed to raise rates for so long, and this mid-recessionary cycle to be so long. Nonetheless, the CEF is flat on a total return basis since our rating:

Prior Rating (Seeking Alpha)

An investor needs to keep in mind this CEF has been around for almost 40 years now, and gone through various market cycles. What is nice about this fund is the fact that it does not come from a large fund family, and does not exhibit the pressure to do 'stupid' things in order to attract capital/attention.

To that end, the fund cut its dividend in 2023:

Dividend (Fund Website)

The market responded promptly by widening the discount to NAV for the structure, discount which now is close to -17%. We think that is not only unwarranted by also erroneous. We like when CEFs cut their dividends if they are not supported. Especially in today's environment. We are of the belief that HY CEFs should be playing defense this year until we have that cathartic sell-off that will set the lows for this cycle.

We have seen defensive positioning from other good HY CEFs, which have cut down their leverage a lot:

{kind=link}

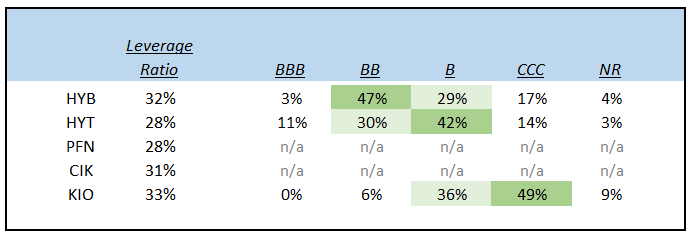

HYB has not altered its leverage ratio, but it is positioned more defensively via a better quality collateral composition. The fund is overweight 'BB' names versus other funds, which are mostly invested in 'B' names. When there is a credit crisis, lower-rated names tend to widen much more due to concerns around survival. Managers can position a portfolio more conservatively by either reducing leverage or improving the quality of the collateral (or a combination of both).

As we fully discuss in the 'Performance' section below, the widening of the discount to NAV has been the sole factor that has driven HYB to underperform its cohort. Absent that widening, the fund has pretty much the same total return on a 1-year look back as the other names in the above list. We think this is an erroneous response to the dividend cut, and we expect that discount to reverse when a cyclical bull market will start again.

We like HYB, we own HYB, and we actually think it is defensive to cut the dividend if not fully supported in today's environment. The market has responded erroneously (in our opinion), but this widening of the discount might not get corrected until the next cyclical bull market. We are Holding this name and clipping the coupons.

Premium/Discount to NAV + Performance

We can see that the discount to NAV for the CEF widened significantly since the dividend change:

In effect, the discount moved from -10% to close to -17% now. An HY PIMCO CEF, namely PFN, has seen its premium pretty much return to the same spot as a year ago, despite the turmoil. This is the exact factor which has hamstrung HYB when compared to its peers in the space:

If we take out the widening of the discount to net asset value, we can see the CEF has the exact performance as most of the cohort which we analyzed.

Conclusion

HYB is a closed-end fund focused on U.S. high-yield credit. The vehicle has a very long history and is conservatively run, having in December 2021 a NAV value close to the one exhibited on its IPO in the 80s. The fund cut its dividend at the beginning of 2023 due to the floating rate structure of its leverage, which ended up eating some of the fund's excess spread. The market 'rewarded' the fund by increasing the discount to NAV by -7%. We like what the fund did, and we think NAV stability is paramount for a long-term vehicle in this space. If we look at HYB's performance in the past year, we can see that absent the widening of the discount, the CEF has performed in line with its peers. We are of the opinion that HY CEFs should play defense this year, since it will end up being a tough one. We own this name and continue to Hold clipping the coupons and liking its conservative positioning.

For further details see:

HYB: Revisiting This High Yield CEF After The Dividend Cut