EMR - I Am Not Buying Emerson Electric

2023-12-05 06:17:34 ET

Summary

- Emerson Electric has been increasing dividends since 1991 and currently yields 2.33%.

- The company reported a revenue decline of -23.7% and an earnings reduction of -15.7%.

- I rate Emerson Electric as a growth company and give it a "HOLD" rating based on my analysis.

Introduction

I recently screened for equity income stocks to see if there was anything new on the shelf. Up pops Emerson Electric (EMR). Why not Emerson? It is a company that has been increasing dividends since 1991 and yields 2.33%. It is also financially healthy with clean balance sheets.

Unfortunately, I am not buying into this simple story. I contend that dividends are a function of earnings. However, those earnings are a function of sales. I will outline my quantitative thesis later.

According to Reuters , Emerson manufactures technology and engineering on a global scale. They operate in intelligent devices and software. These focus on valves, actuators, liquid analysis, gas analysis, and tank gauging systems. In total, they operate in six distinct businesses and have a diversified revenue model.

This is how others rate Emerson Electric:

- Morningstar—Buy

- Zacks—Strong Buy

- The Street—Buy

- KeyBanc Capital Markets—Overweight

- UBS —Hold

- Consensus—Strong Buy

In their fiscal earnings report , Emerson reported a revenue decline of -23.7% and an earnings reduction of -15.7%. Despite this gloomy news, the consensus has future earnings growth for EMR pegged at 9.6% and revenue growth at 7.5%.

Methodology Disclosure

I am a quantitative analyst. I put little stock in making future predictions about what a company will or will not do. My preference is to analyze the revenue of a company over the last five years and make determinations for earnings and free cash flow from there. I contend that most financial results for a company are the function of sales. The direction of sales dictates everything else for a corporation and one will that is the basis of all analysis I do.

Balance Sheet

I used a modified version of Harry Domash’s “Bulletproof” strategy to determine a grade for a company’s financial health. These are the numbers for EMR:

- Debt-to-Equity is 0.42

- Must be less than 0.4.

- Current Ratio is 2.75

- Must be greater than 1.5.

- Altman-Z Score is 4.04

- Must be greater than 3.00.

- Free Cash Flow is $15.1B

- Must be positive.

Most metrics pass, so I rate EMR’s financial health as SAFE simply based on its current ratio, Altman-Z score, and positive free cash flow.

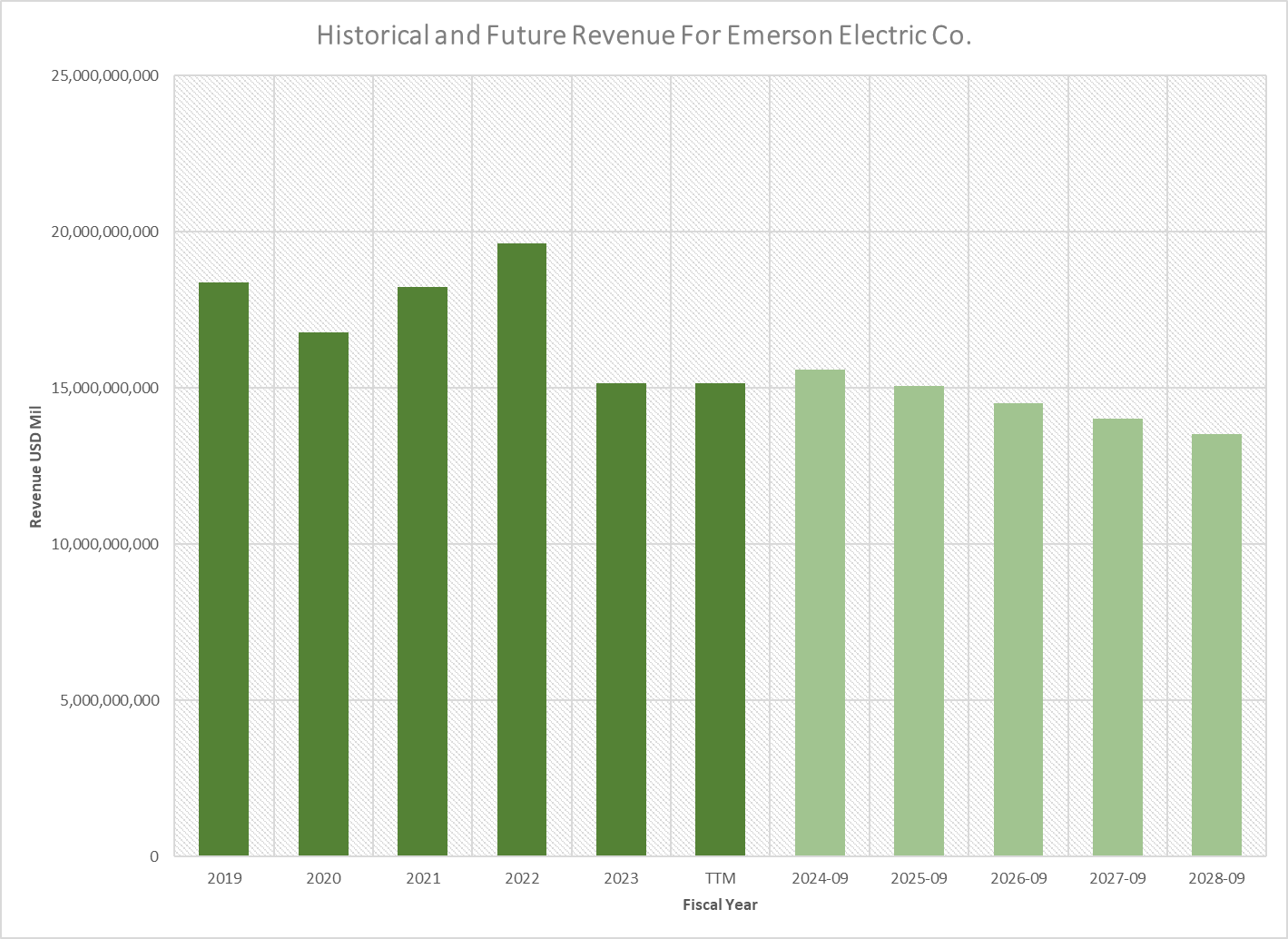

Revenue Analysis

As I wrote in my introduction, Emerson’s revenue collapsed by -23.7% for the most recent fiscal year. This, for me, is unacceptable and gives the company a regressed revenue decline of -1.27% per year. Unless we see added information soon, I cannot assume future growth based on recent results. I state this from a quantitative viewpoint.

{kind=link}

EMR has a historical beta of 0.96, which gives me a required rate of return of 9.8%. This historical Price-to-Sales ratio is a low of 2.52 and a high of 3.41. Using the metrics and the recent decline in revenue, this is how I calculate the present value of Emerson based on revenue:

- Bearish Case: $48.62

- Bullish Case: $60.53

- Fair Value: $54.24

Earnings Analysis

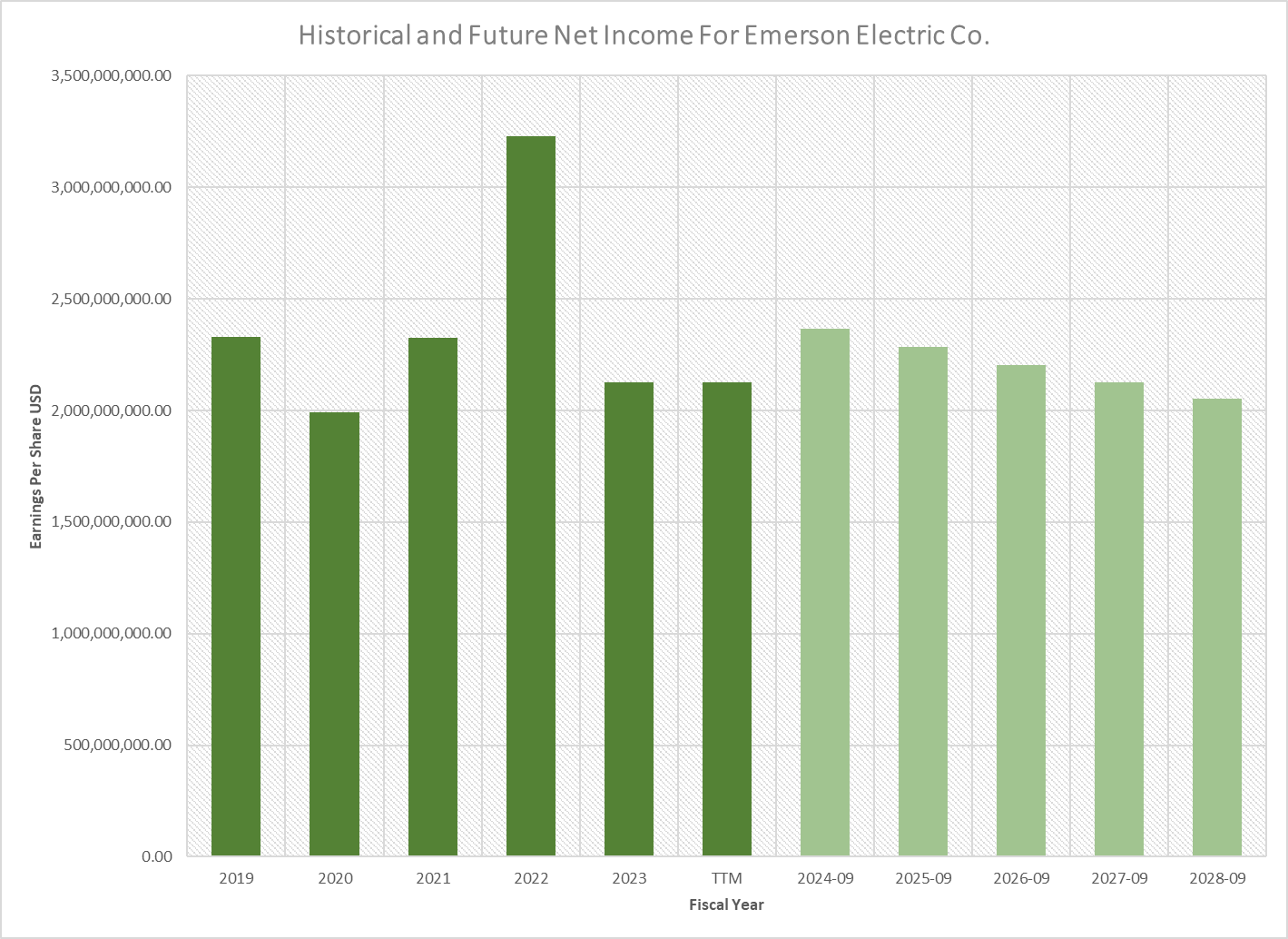

As mentioned in the introduction, earnings, like sales, also collapsed during the most recent fiscal year at -15.7%. Because of this, the regressed earnings growth is a decline of -2.23%. Again, there needs to be an immediate improvement to convince me that things will change.

{kind=link}

The historical Price-to-Earnings ratio for Emerson is a low of 13.61 to a high of 28.52. This is how I evaluate EMR based on its earnings:

- Bearish Case: $42.53

- Bullish Case: $ 72.80

- Fair Value: $54.89

Free Cash Flow Analysis

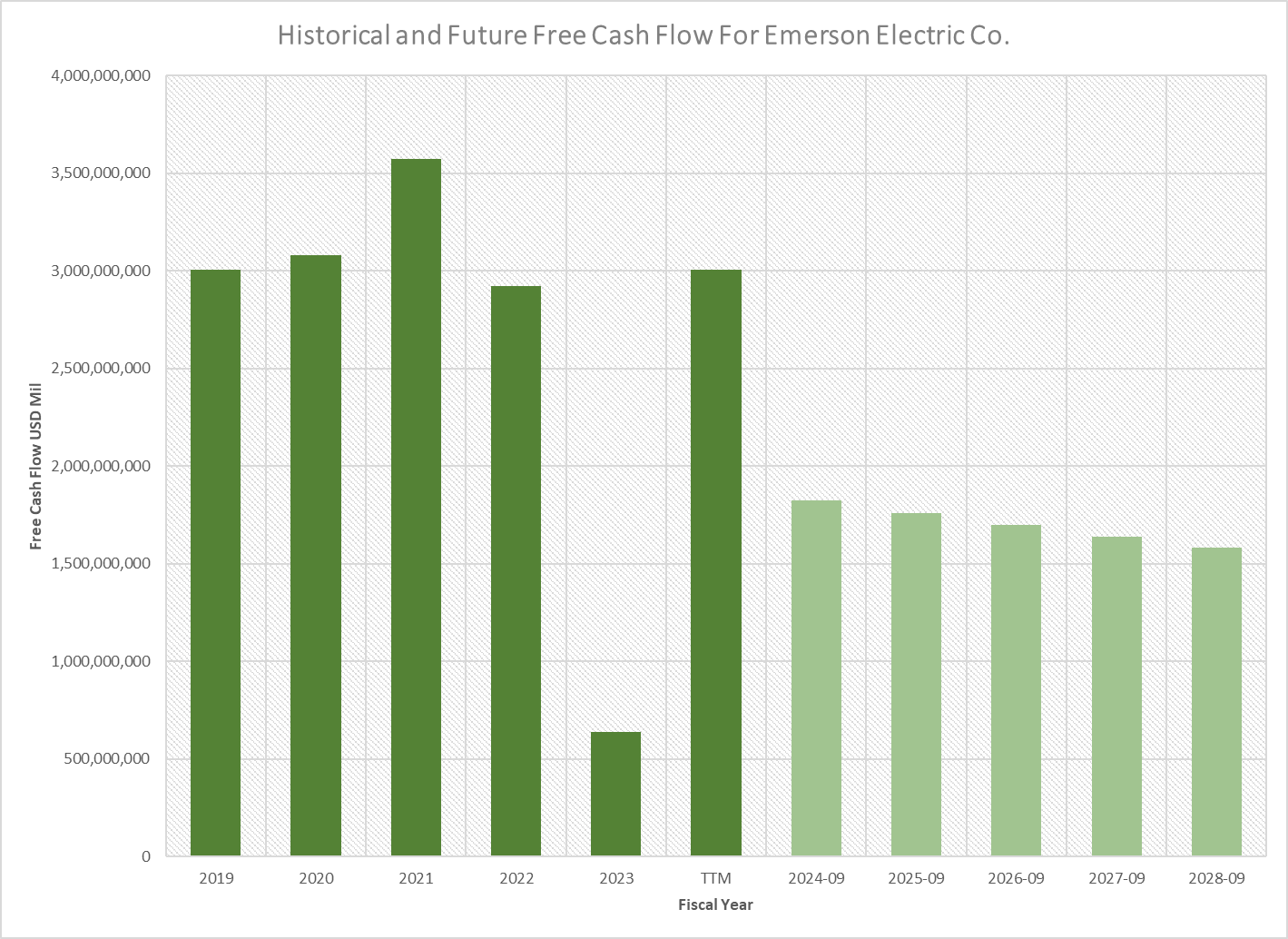

One of the more pleasing stories about Emerson is that they can maintain positive free cash flow from year to year. That does give one faith that EMR can turn it around and maintain its position as an income stock.

{kind=link}

EMR’s cost of debt is 6.2% and its cost of equity is 9.8%. I use sensitivity tests of 1% to 3%. This is how I see its present value based on free cash flow:

- Bearish Case: $26.24

- Bullish Case: $37.84

- Fair Value: $31.07

Growth Rating

This is how I rate Emerson Electric as a growth company:

- The minimum is one point.

- Financial Health is SAFE

- One point

- Revenue Analysis

- Present Value < Current Price

- Zero points

- Earnings Analysis

- Present Value < Current Price

- Zero points

- Free Cash Flow Analysis

- Present Value < Current Price

- Zero points

- Growth Rating: two points (SELL)

Dividend Analysis and Rating

I was originally looking for dividend ideas, and Emerson passed my initial screens.

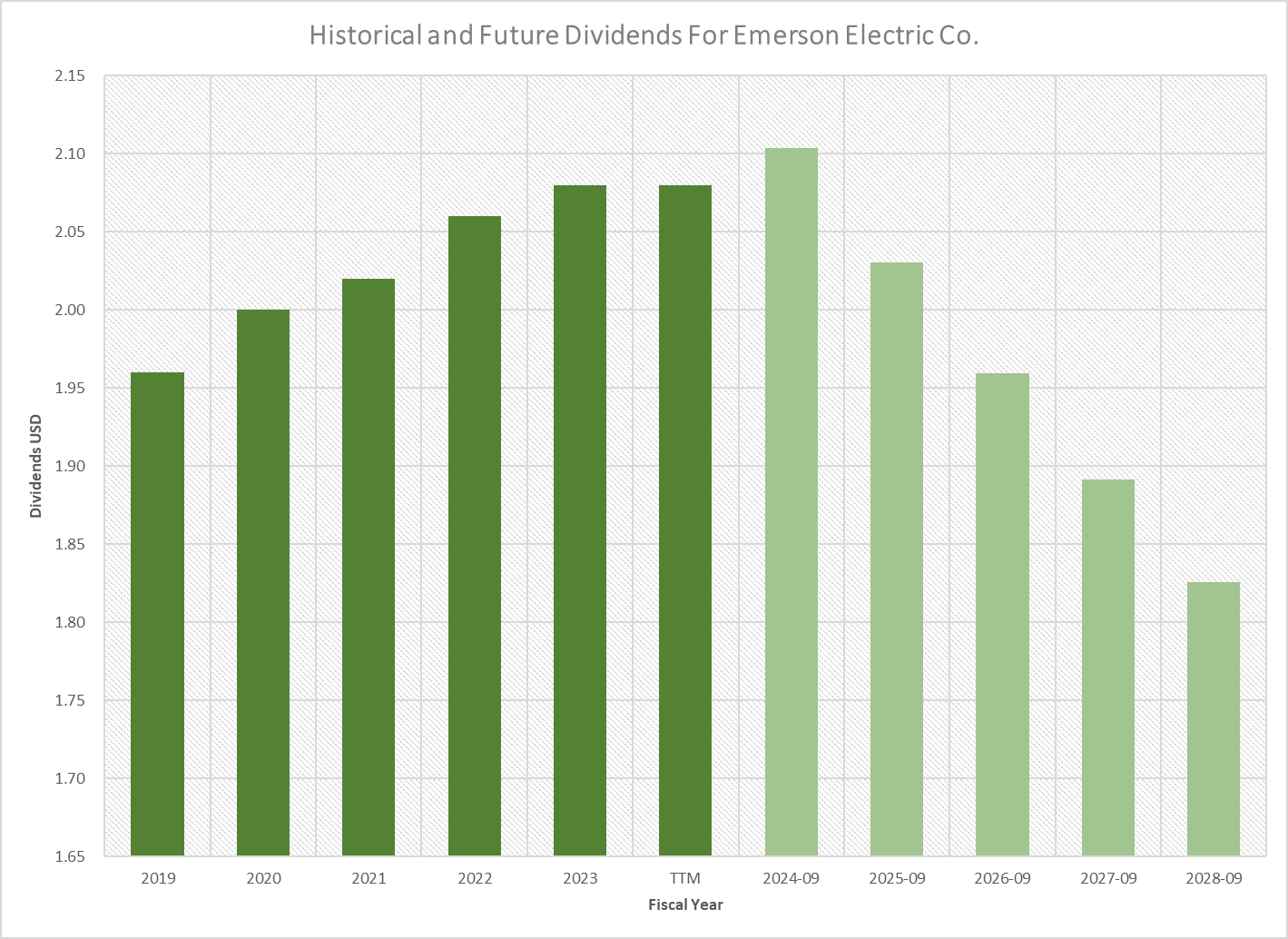

- The current yield is 2.33% and the historical yield is 2.39%

- Must be at least 2%

- The dividends have increased every calendar year since 1991. They have also increased a regressed annual average of 1.50%

- Must see increases for ten consecutive years.

{kind=link}

Since all my growth assumptions are based on future revenue growth, I view EMR’s dividends as potentially declining if the sales trajectory does not change. Based on a constant growth model, I see this as a $58.49/share stock, and a non-constant basis, it is a $60.76/share stock.

Here is my rating for EMR based on its dividend history:

- The minimum is one point.

- Financial Health is Safe

- One point

- Current Yield > 2%

- One point

- Free Cash Flow Analysis

- Present Value < Current Price

- Zero points

- Discount Dividend Analysis

- Present Value < Current Price

- Zero points

- Income Rating: 3 Points (Hold)

My Take

Emerson Electric is a fantastic company, and those who own it have seen a 9.3% annual total return over the last five years. Unfortunately for the long-term stockholders, they have not been able to participate in the overall market’s rise this past year and have seen their investment lose -3.98%. One of two things will have to happen before I can recommend the stock. The revenue line must improve immediately or there is a massive collapse in the price of the stock. For now, I will take a pass on this one.

For further details see:

I Am Not Buying Emerson Electric