KD - IBM: Don't Be Fooled By Recent Share Price Performance

2023-04-14 12:01:58 ET

Summary

- IBM has delivered a positive return of nearly 20% over the past two years, but that has little to do with actual business performance.

- In addition to sluggish growth, IBM's declining profitability remains a problem.

- Issues related to the company's high debt load, low dividend coverage and an addiction to acquisitions have not gone away.

Being an IBM ( IBM ) shareholder hasn't been easy over the years as the market continues to make new highs, while IBM still trades at levels from 2010.

Since I warned that IBM is a value trap in early 2021, the company has returned nearly 20% which in combination with the large spin-off of Kyndryl ( KD ) gave investors hope that the worst is already behind us.

During this same period, however, Hewlett Packard Enterprise ( HPE ) and Oracle ( ORCL ) performed significantly better than IBM, returning 46% and 55%, respectively.

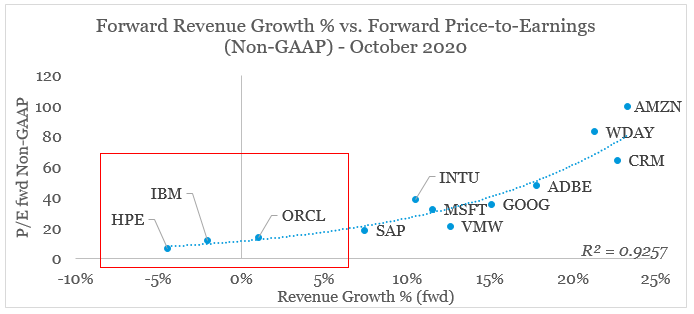

At this point, you might be wondering, why I'm comparing IBM to Oracle and HP Enterprise when these two companies are not the perfect comparables to IBM's business.

The reason is that within the broader cloud sector, these three businesses were at the very bottom in terms of expected revenue growth and earnings multiples back in 2020.

{kind=link}

Since then, interest rates have normalized and the slope of the trend line above has flattened, thus benefiting HPE, IBM and ORCL and penalizing the high flyers at the top right-hand corner of the graph (you can read my whole sector analysis here ).

Back then, IBM's forward revenue growth was around negative 2% and those of ORCL and HPE were +1% and -4% respectively. Fast forward two and a half years and IBM's forward revenue growth has now barely improved to 4.2%.

Seeking Alpha

Before making any conclusions though, you should take into account that the spin-off of the declining business of Kyndryl had a profound impact on IBM's figures.

Seeking Alpha

HPE, on the other hand, has remained a low growth company with forward revenue growth of roughly 3% and Oracle's growth has accelerated to almost 10%. And yet, as we saw above, IBM underperformed these two companies by a very wide margin over the past two years.

Profitability Issues Are Still With Us

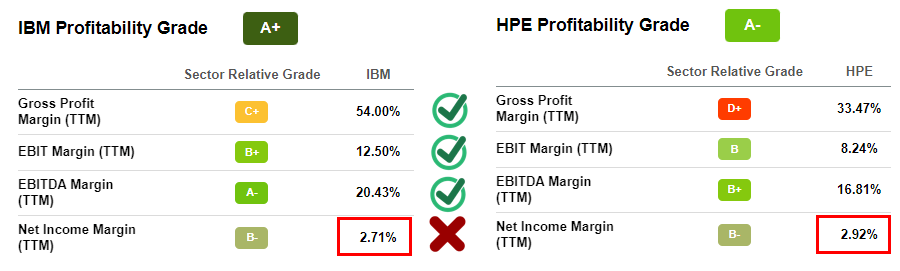

When compared to one of the worst performers within sector, IBM also has far better profitability metrics. From significantly higher gross profitability to operating and EBITDA margins.

{kind=link}

However, as we see above, it's IBM's net income margin that falls short of expectations.

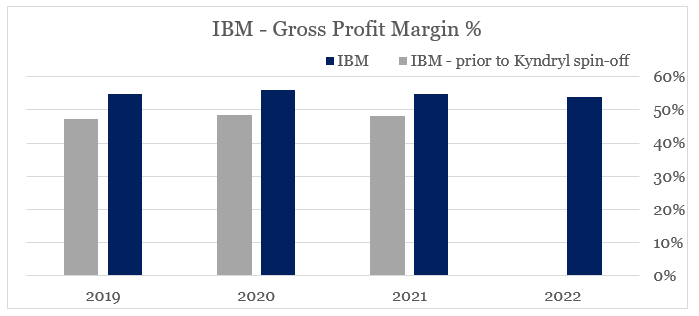

Once again, this was an area of the business that benefited massively from the recent spin-off. Although it might not seem much on the graph below, IBM's gross margins improved from an average of around 48% prior to the transaction to around 55%.

{kind=link}

The reason why this is so important is that even small changes to gross profitability could make a big difference once we reach to the bottom of the income statement.

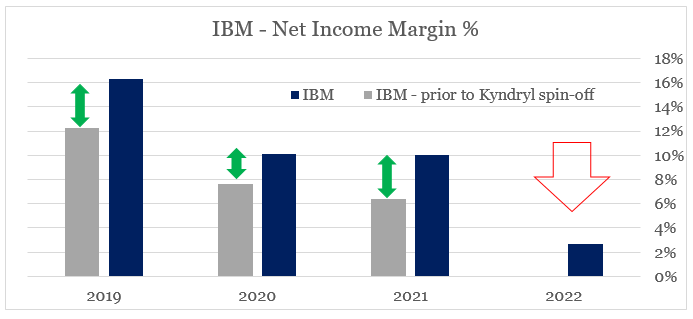

This is clearly illustrated in the graph below where we see large differences in IBM's net income margin prior and post the spin-off of Kyndryl.

{kind=link}

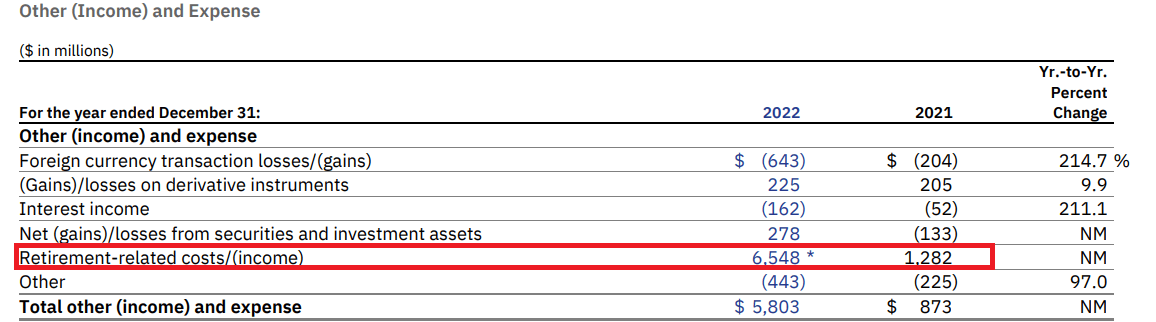

We also can't miss the massive drop in profitability during 2022 which is largely due to a $ 5.9bn pension settlement charge that according to the management is supposed to be a one-off item.

{kind=link}

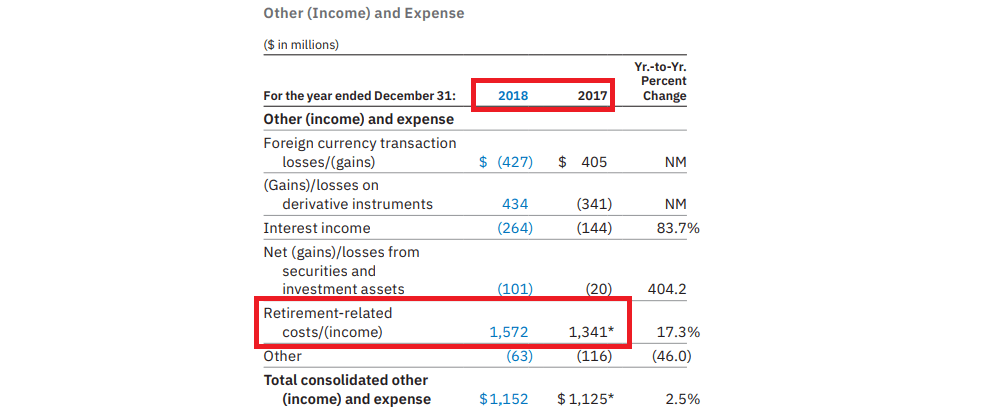

In reality, however, IBM experienced a $1.3bn retirement related costs in 2021 and similar expenses in 2018 and 2017.

{kind=link}

Therefore, although the nearly $6bn charge could indeed be a non-recurring item, IBM consistently experiences significant retirement-related costs over the years. I already highlighted this issue of relying on adjusted profitability a couple of years ago and it appears that non-recurring charges are still the norm at IBM.

Other Issues Have Not Gone Away

With an interest coverage of only 6.2 for the past 12-month period, IBM could be forced to continue selling assets in order to reduce its debt load. That's why I wasn't surprised that just as I was writing this it became clear that IBM is looking to sell yet another of its non-core businesses.

{kind=link}

In 2022 IBM's interest expense stood at around $1.2bn, which should not be ignored given the company's roughly $7.5bn worth of adjusted operating income prior to exceptional items, such as intellectual property and custom development income and other/income and expense mentioned above.

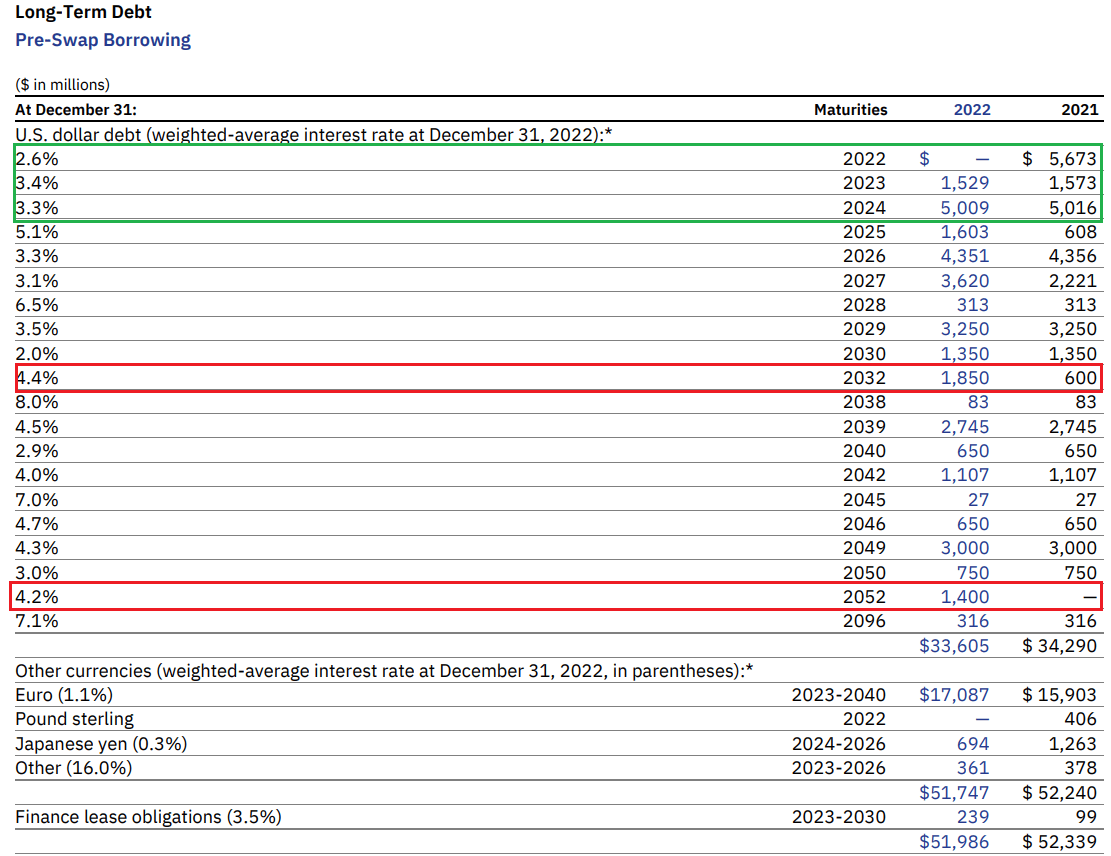

To make matters worse, IBM also will have to refinance its debt maturing in the coming years at higher much interest rates. This is visible from the newly issued debt maturing in 2032 and 2052 at rates above 4%.

{kind=link}

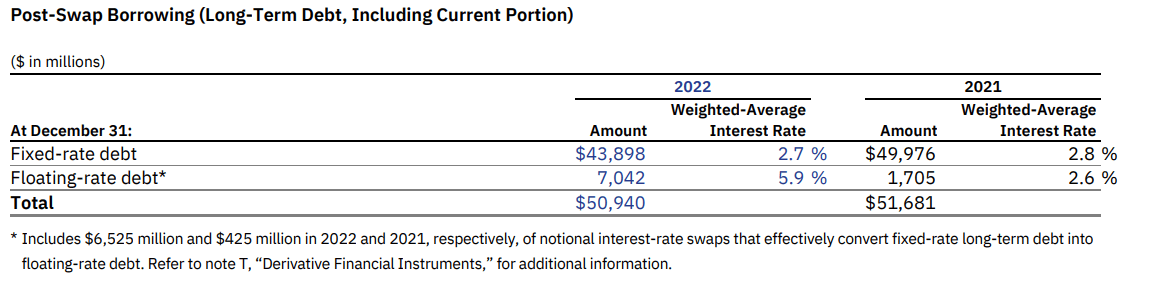

IBM's management also has made the decision to swap a sizable amount of its fixed-rate debt for floating (see below). In hindsight, this does not appear as a sound decision in an environment of rapidly raising interest rates.

{kind=link}

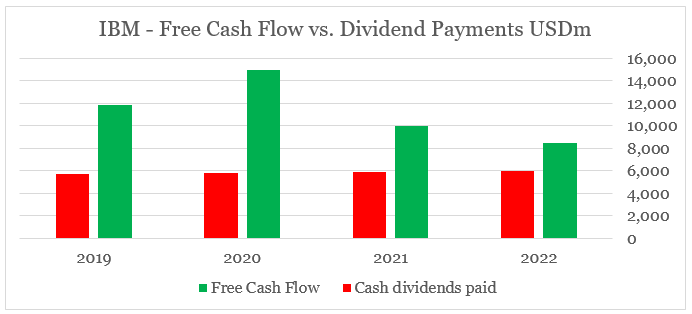

Overall, the debt continues to be a problem for IBM, while the company's attractive dividend with a yield of above 5% appears riskier with every year that passes. The gap between the annual dividend payments and IBM's free cash flow is now at very low levels.

{kind=link}

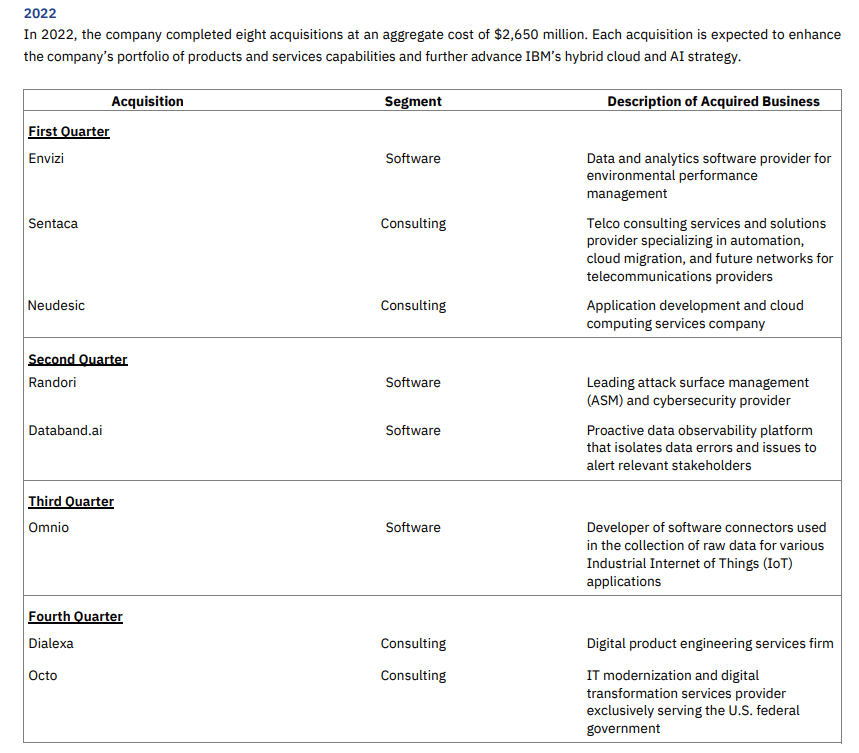

In the meantime, IBM continues to spend enormous amounts on acquisitions each year. After I flagged this issue in 2021, the management has spent an additional $2.3bn on acquisitions in 2022 alone.

We invested $2,348 million in acquisitions to accelerate our hybrid cloud and AI capabilities , generated $1,272 million from the divestiture of certain businesses, and returned $5,948 million to shareholders through dividends in 2022.

Source: IBM 2022 Annual Report

It seems that as IBM struggles to compete organically, the company requires a large number of deals across most of its business units in order to retain its competitive positioning.

{kind=link}

Conclusion

The positive return of IBM over the past two years is largely due to broader market movements and the normalization of the monetary policy, which benefited the value stocks more broadly.

At the same time, however, IBM continues to underperform other value names in the sector and most pressing issues have not gone away as a result of the large spin-off of Kyndryl. IBM's dividend remains at risk and the company's acquisition spree is not a good sign either.

For further details see:

IBM: Don't Be Fooled By Recent Share Price Performance