ZTS - IDEXX Laboratories: Excellent Business But Extremely Overpriced

Summary

- IDEXX Laboratories, Inc. is a U.S. healthcare company, that currently leads the veterinary industry developing diagnostics tools to satisfy veterinarians’ everyday needs.

- IDEXX has delivered solid and consistent results that rival those of Google's, Metas', and Microsoft's out there.

- Despite IDEXX being expected to deliver solid returns in the future, the market is currently paying a huge market premium, making its stock highly overvalued.

Investment Thesis

With its margins of 26% and return on capital of 46%, IDEXX Laboratories, Inc. (IDXX) can overshadow companies the like of Google ([[GOOG]], GOOGL ), Meta Platforms ( META ), and Microsoft Corporation ( MSFT ). Founded in 1983, IDEXX is a U.S. healthcare company, that currently leads the veterinary industry developing diagnostics tools to satisfy veterinarians' everyday needs.

Over the years, IDEXX has delivered solid and consistent results combining revenue growth with incredible efficiency and profitability, and we can comfortably expect the company to keep succeeding in the future.

With this premise, IDEXX's stocks might seem an obvious buy, but unfortunately, the company is extremely overvalued at today's prices if compared to an intrinsic value of $259 per share.

In today's analysis we will assess why, despite having an incredible business model expected to deliver strong cash flows in the coming years, IDEXX Laboratories does not represent a good investment opportunity given the current market conditions.

Business Model

IDEXX Laboratories, Inc.'s business model is divided into three main segments: Companion Animal Group, Water quality products, and Livestock, Poultry and Dairy solutions.

The Companion Animal Group ((CAG)) offers a wide variety of diagnostic tools that help veterinarians and pet owners to detect pet diseases in time and possibly cure them. IDEXX's offer comprises both analyzer instruments, usually sold once to each customer, and consumable test kits, which are purchased on a recurring basis by customers.

In addition to the diagnostic tools, the CAG segment also comprises the development and sale of software products, to help veterinary clinics to improve their daily operations, and a network of owned laboratories to which veterinarians can submit their samples to be analyzed or ask for consulting services.

The Water segment comprises testing solutions able to detect the presence of bacteria in water and are usually sold to water utility companies and government laboratories.

Finally, the Livestock, Poultry and Dairy segment offers diagnostic tools that are used by farmers to test the health status of cows, pigs, and chickens, to prevent illnesses like African Swine fever, and to test dairy products to assure their quality.

Revenues are generated 91% by the Companion Animal Group, of which the sale of consumable products accounts for 87% of total segment revenues, while the Water and Livestock segments respectively account for 5% and 4% of total revenues.

Operating Performance

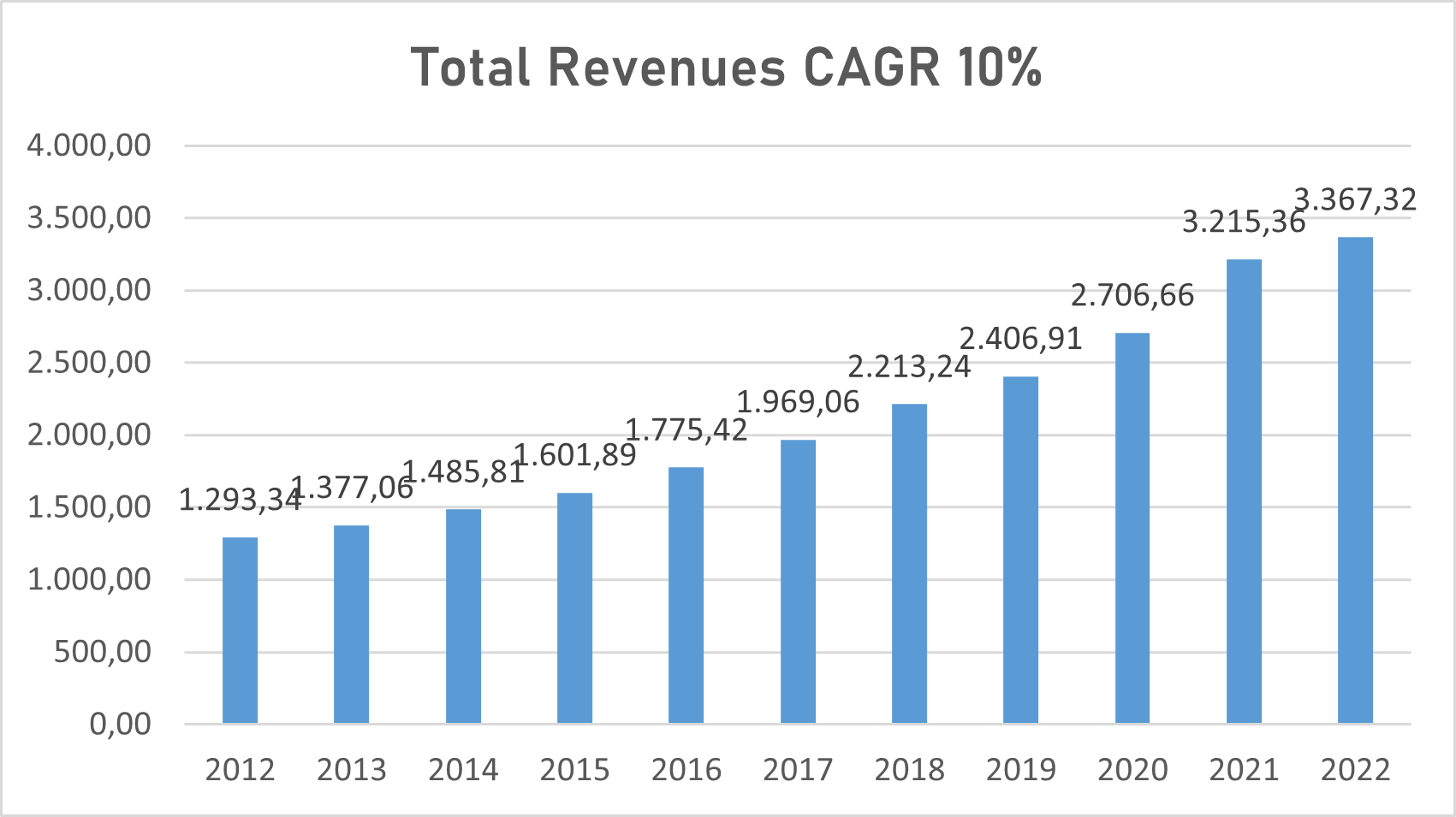

Looking at IDEXX's past operating performance , revenues went from $1.3 billion in 2012 to $3.3 billion in 2022 growing at a compound annual growth rate ((CAGR)) of 10%.

IDEXX Laboratories revenues (TIKR Terminal )

{kind=link}

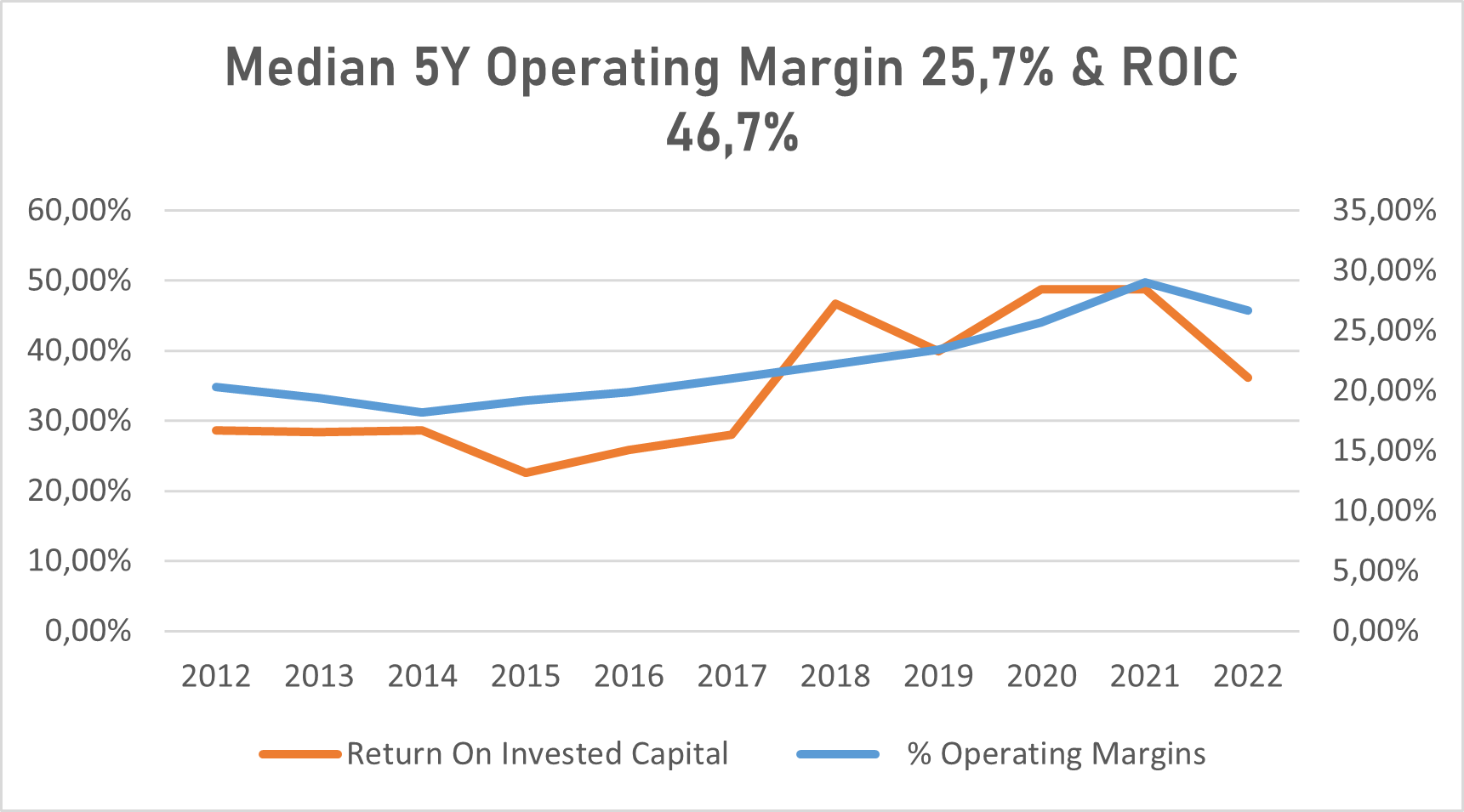

Both the median operating margin and the median return on invested capital ((ROIC)) of the last 5 years are excellent, respectively at 25.7% and 46.7%, showing how great IDEXX's business model is and the power they have on the veterinary industry, permitting them to maintain high prices without losing market shares.

IDEXX Laboratories' median 5Y operating margin & ROIC (TIKR Terminal )

{kind=link}

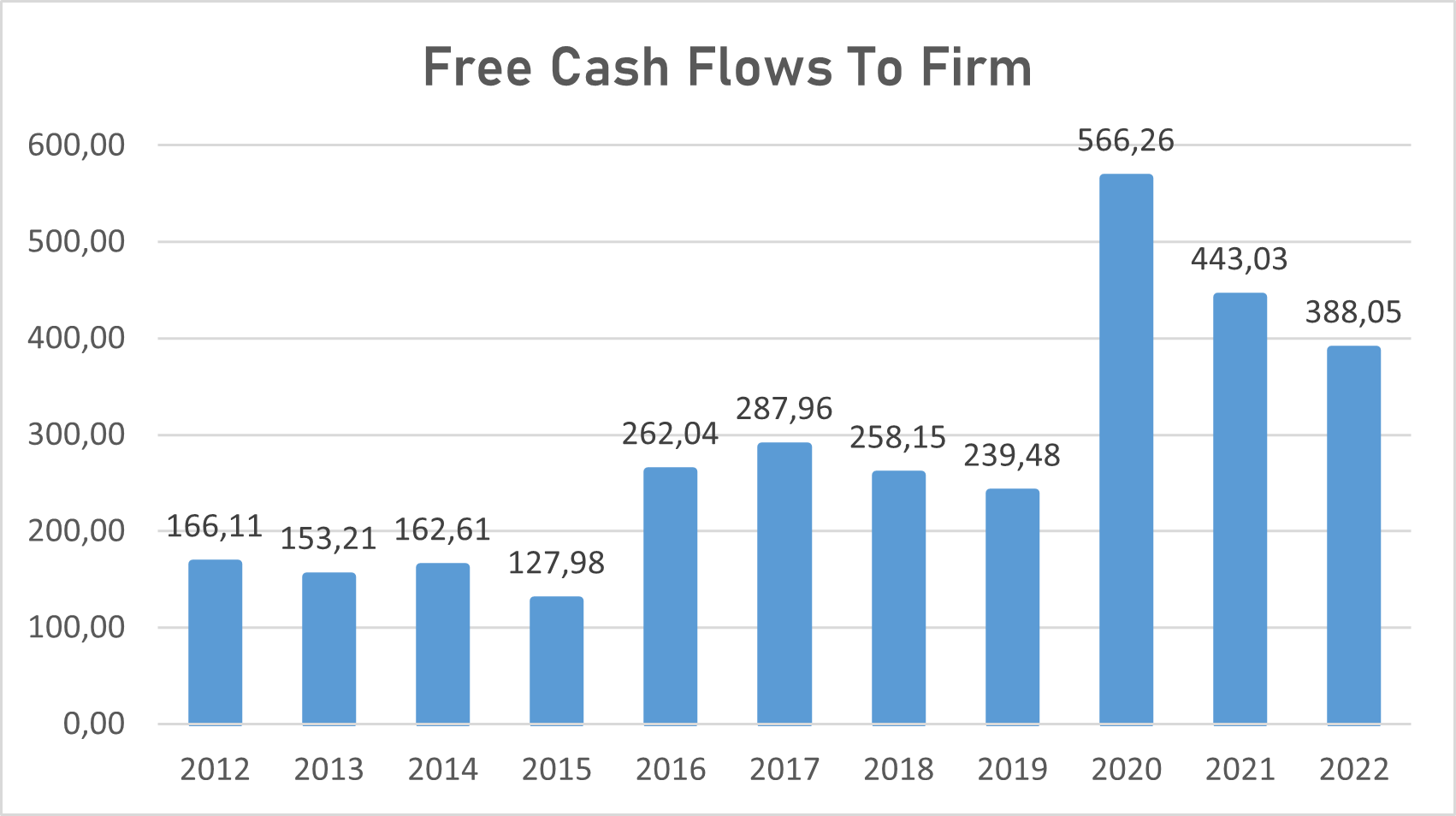

Combining revenue growth and high profitability, the company managed to deliver solid free cash flows to the firm ((FCFF)) for the entire period, equal to $388 million in 2022.

IDEXX Laboratories FCFF (Personal Data)

{kind=link}

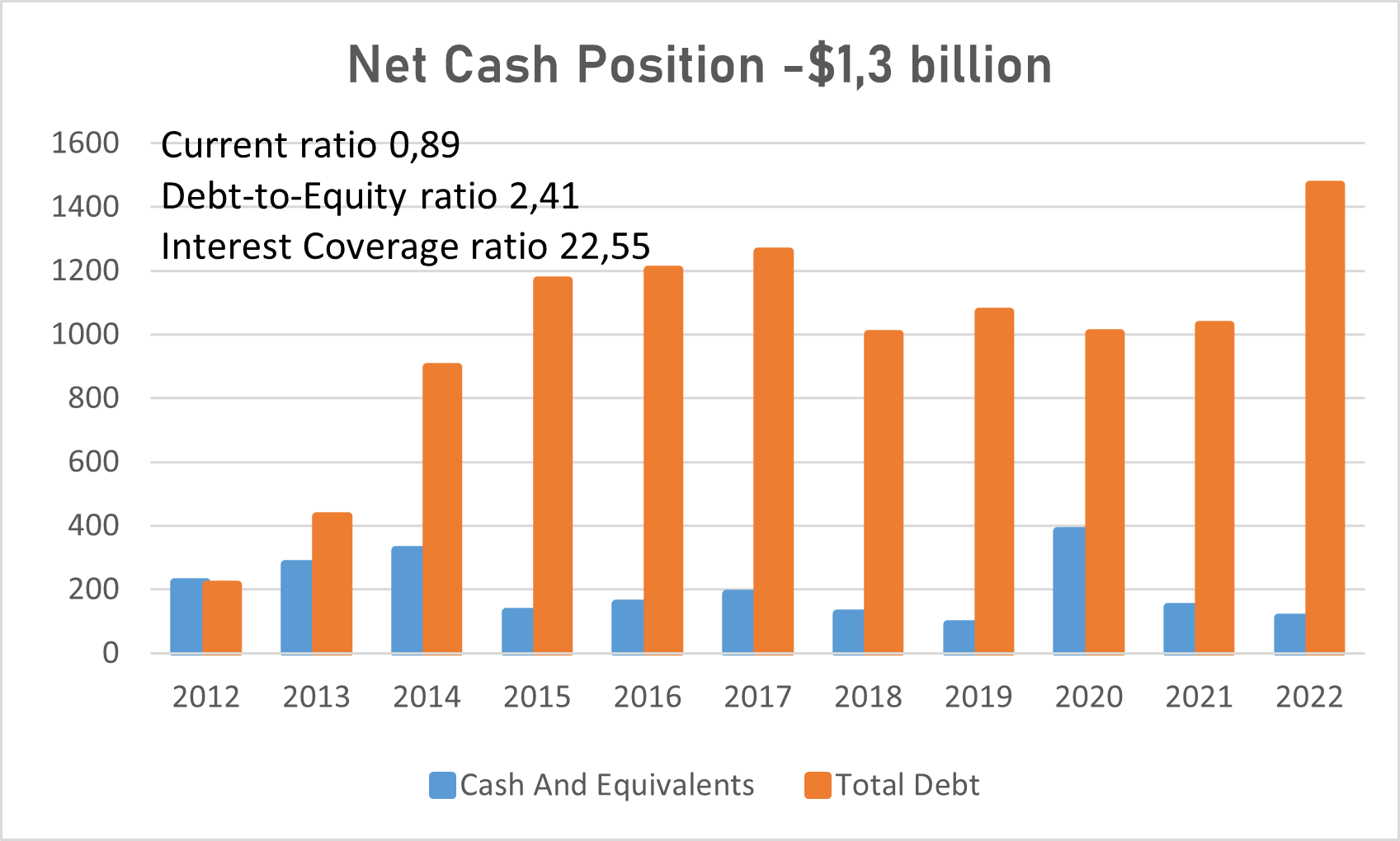

Financially, IDEXX has a negative cash position of -$1.3 billion, but despite having a considerable amount of debt outstanding the company results financially stable having an interest coverage ratio of 22.55, meaning that the operating income can more than cover the interest expenses being 22 times greater, therefore IDEXX is very unlikely to default.

IDEXX Laboratories financial position (TIKR Terminal )

{kind=link}

Growth Drivers

As typical for healthcare companies, IDEXX heavily relies on its investments in R&D expenses to fuel its growth. By developing new patients and improving its diagnostic tools, IDEXX will be able to maintain its leading position in the veterinary industry, which implies maintaining its astonishing margins and returns on investments.

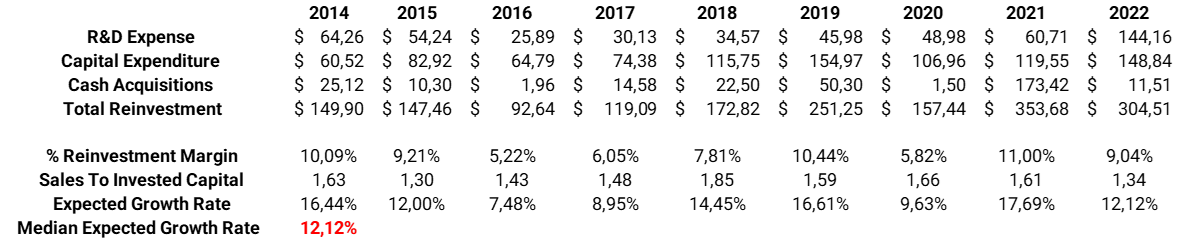

Future growth can be determined by looking at how much and how well a company has invested in its growth drivers. The Reinvestment Margin shows what percentage of revenues has been reinvested into the company, while the Sales to Invested Capital ratio, shows how much revenues have been generated for each dollar invested by the company. If we multiply these two values and take the median value over the years, we obtain the expected growth rate in revenues based on how much and how well a company has invested in its growth drivers.

In our case, IDEXX's expected growth rate is 12.12%.

IDEXX Laboratories expected growth rate (Personal Data)

{kind=link}

Market & Risks

Given the high margins that characterize the industry in which IDEXX operates, competition can be easily attracted to enter the market. Among IDEXX's main competitors, we have Zoetis ( ZTS ) and Mars Petcare, a subsidiary of Mars Incorporated, but despite these two strong players, IDEXX holds a 19.5% market share .

The biggest threat to IDEXX's future success is its ability to maintain and protect its patents and licenses in order to have the exclusivity of its high-quality products that will permit the company to justify higher prices and consequentially better margins.

IDEXX Laboratories patents expiring date (IDEXX Laboratories)

{kind=link}

DCF Model

I use the discounted cash flow ("DCF") analysis method to value companies. The aim of a DCF analysis is to determine the present value of expected cash flows generated by the company in the future. The first step is to project the growth rate at which revenues will grow in the future. Secondly, we will need to assume the degree of efficiency and profitability at which the company will turn revenues into cash flows.

Efficiency is represented by the operating margin, and profitability by the ROIC. Having the revenue projections and future operating margins, we obtain the EBIT and, after subtracting taxes, we get the net operating profit after taxes. The ROIC is used to determine the reinvestments needed to support future growth, determining how much profit the company generates from every dollar reinvested into the company.

Future cash flows are calculated by subtracting the reinvestments from the net operating profit after taxes. The higher the growth rate, the higher the reinvestments needed to support it, hence the lower future cash flows will be.

The last step of a DCF analysis is to apply the discount rate to future cash flows, usually calculated using the weighted average cost of capital ('WACC').

Projections

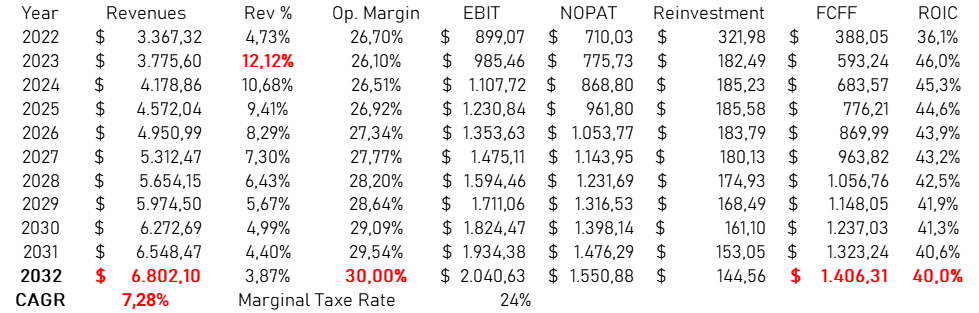

Now trying to project IDEXX's future performance, we will assume the company to maintain a modest and steady growth rate, establishing itself as one of the main player in the veterinary industry with high margins and returns on capital, that will lead to a solid cash flows generation over the years.

Starting with revenues, the first step is to apply the expected growth rate of 12.12%, based on how much and how well the company has reinvested in its growth drivers, and after that, we can let it slowly decline as the company enters its steady state. Revenues are expected to double in 10 years, at a CAGR of 7.28%, reaching $6.8 billion by 2032.

As regards future efficiency and profitability, we can expect IDEXX to maintain excellent values, as we assume the company will remain at the top of the industry. By 2032 the operating margin can be expected to improve to 30%, as the company might benefit from larger economies of scale growing its revenues, while the ROIC can be expected to remain in the 40% range.

With these assumptions FCFF are expected to be around $1.4 billion by 2031, growing at a CAGR of 13.74%.

IDEXX Laboratories performance projections (Personal Data)

{kind=link}

Valuation

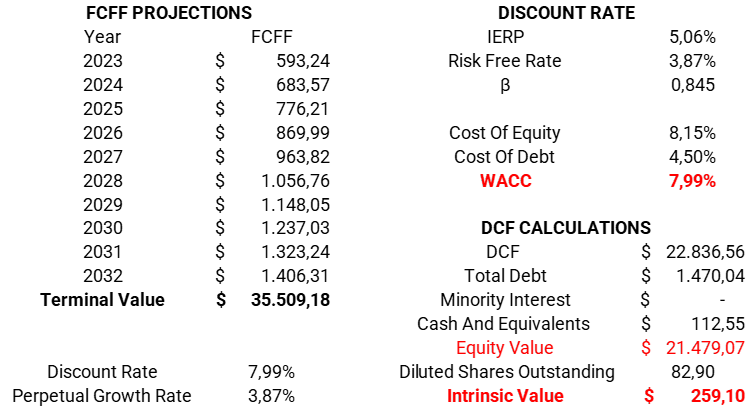

Applying a discount rate of 7.99%, calculated using the WACC, the present value of these cash flows is equal to an equity value of $21.4 billion or $259 per share.

IDEXX Laboratories intrinsic value (Personal data)

{kind=link}

Conclusion

Given my analysis and assumptions, IDEXX Laboratories, Inc. stock appears to be overvalued at today's prices.

IDEXX Laboratories, Inc. is such a great company, with an incredible business model that rivals the one of the Google's, Metas', and Microsoft's out there, that the market is currently paying a huge market premium to jump on board. Unfortunately, until we see a significant price correction, IDEXX Laboratories, Inc. does not represent a good investment opportunity.

For further details see:

IDEXX Laboratories: Excellent Business But Extremely Overpriced