META - IGA: Strong 2022 Results Still A Buy At Current Levels

Summary

- IGA held up much better in 2022 than the overall market on a total NAV return basis.

- This was thanks to the portfolio's options strategy, currency hedging and overall value-tilt in their portfolio.

- The results were less attractive on a total share price basis, but that merely opened up the fund's discount to more attractive levels.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on January 23rd, 2023.

Voya funds often get ignored because they were historically some of the weakest performers. They've had to cut their distributions several times, while it seems like some other funds haven't had to do the same. Voya Global Advantage and Premium Opportunity Fund ( IGA ) has been put into this bucket.

The primary reason for all of this can be summed up quite easily, the fund's global positioning and the value-oriented portfolio have translated into weaker results. A closed-end fund is merely a wrapper for other assets; it isn't an asset itself. Voya has told you exactly how they'll invest IGA as a fund, and they did exactly as they said.

That was not a great strategy for most of the last decade. All Voya funds seem to have international exposure to some degree, which means most of their funds have underperformed. Thus, why they generally don't get a lot of attention, or if they do, it's generally negative.

Now, that's contributed significantly to the results we saw last year, where value stocks outperformed handily. Some luck with their foreign currency hedges and writing options also contributed to much better results than we saw elsewhere. Primarily, if we put IGA up against the SPDR S&P 500 ETF ( SPY ), a large-cap U.S.-focused measurement that's often considered the "broader market." IGA outperformed SPY significantly in 2022.

Since our last update, SPY has been able to keep up with IGA's total returns. I also went from "Hold" to a more bullish view at a "Buy" rating.

IGA Performance Since Previous Update (Seeking Alpha)

Since then, the discount hasn't moved, so it's still worth considering. Although after a strong rally in the broader market, it might not be as tempting as it was previously.

The Basics

- 1-Year Z-score: -0.04

- Discount: 11.47%

- Distribution Yield: 8.87%

- Expense Ratio: 0.99%

- Leverage: N/A

- Managed Assets: $160 million

- Structure: Perpetual

IGA's investment objective is "a high level of income; capital appreciation is secondary." They intend to write " call options on indexes or ETFs, on an amount of equal to approximately 50-100% of the value of the Fund's common stock holdings." Typically, this is an important metric to look at. This can help gauge how bullish or bearish the fund may be leaning.

The more overwritten the portfolio, then the more that would indicate they are bearish. They would not want to be overwritten significantly if they felt the indexes could reverse and head higher. With the latest 3Q 2022 strategy brief , the fund showed that 37.53% of the fund was overwritten.

This was reduced quite a bit from 50% earlier in the year. They also called out the options writing in the quarter as a detractor. This does happen when the market rallies because the written calls can end up losing money as they write against indexes, which are cash settled.

Having exposure to call writing funds isn't always bad, though, as we know, in 2022 as a whole, it contributed to performance. During flat years it can be a way to generate returns, too, if nothing else is really moving.

The fund operates with no leverage, so there is no added volatility coming from that side of the equation, as we see in most other CEFs. On the other hand, the relatively smaller size of the fund means that liquidity can be quite low. That can make it less appropriate for larger retail investors trying to buy and sell frequently.

Performance - Attractive Results And Attractive Valuations

On a total NAV return basis, IGA smoked SPY. The NAV is what the actual underlying performance has done. The total share price had still outperformed but not to the same degree. The share price is merely market sentiment speaking. This actually results in CEFs becoming more attractively priced, in general, as discounts can open up.

Ycharts

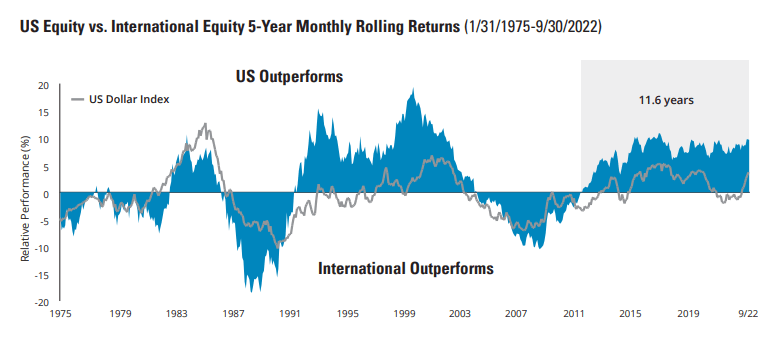

Will the fund outperform again in 2023? Who knows, but I think this helps highlight why there is a need for diversification. There are also some signs that global equities could perform better. Admittedly, global securities have been cheaper for several years, which has never gained traction. Russia invading Ukraine certainly hasn't helped stability in that region of the world.

Still, this will matter at some point, and it is very likely that global equities will outperform more handily. That is, at least, if history is any gauge, as international securities have outperformed the U.S. in some periods .

Hartford US Equity vs. International Equity (Hartford Funds)

{kind=link}

In fact, we are in one of the longest runs for U.S. outperformance that has pushed up valuations. That could help to see the catalyst to push global positions higher and what could propel IGA to be a better performer once again going forward.

RBC Wealth Management Forward P/E Ratios Global Markets (RBC Wealth Management)

Either way, the current valuation for IGA looks fairly tempting if an investor is looking for international exposure.

The fund is trading below the historical average discount seen in the last decade. That's what makes it a more compelling investment today, even beyond just being attractive with global exposure.

Ycharts

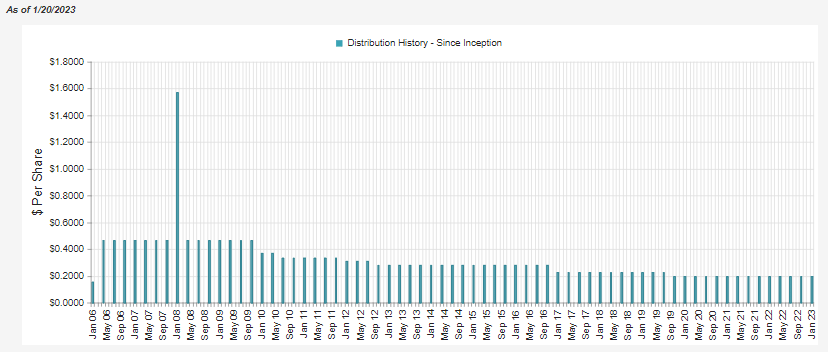

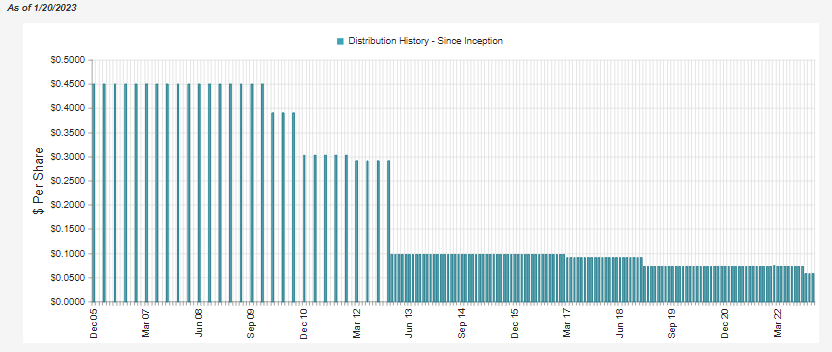

Distribution - 9% Distribution Yield

The fund's latest distribution works out to an 8.87% yield on the share price and a 7.86% distribution rate on the NAV. Thanks to the large discount, the fund has to earn much less than what investors receive.

{kind=link}

Over time the fund has had to cut the distribution several times, but the current level seems fairly reasonable and competitive with peers. Despite what might seem like a bad trend, this isn't really any different than other equity option writing funds we see.

Eaton Vance is a fund sponsor that generally gets fairly high praise. Although not recently, as they just went through with their own round of distribution cuts. However, relatively speaking, their international funds over this same period haven't done much better.

Even though they were holding the mega-cap tech names and writing index options, a fund like Eaton Vance Tax-Managed Global Buy-Write Opportunities Fund ( ETW ) gets the same criticism of having to reduce their distribution, too.

Again, this highlights that it's more about what these CEFs are holding in their underlying portfolio. It isn't necessarily the fund sponsor.

{kind=link}

Today my main focus is on IGA - despite ETW being a relatively attractive name too.

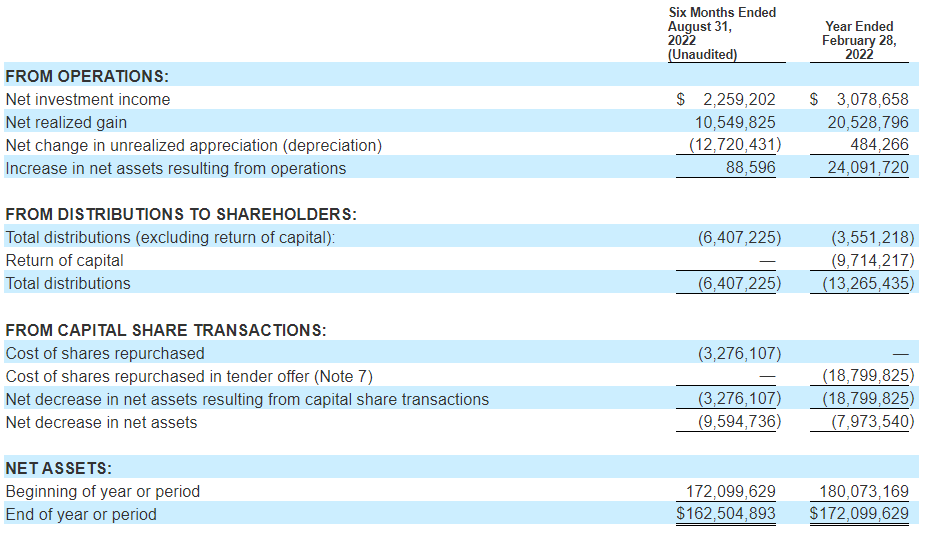

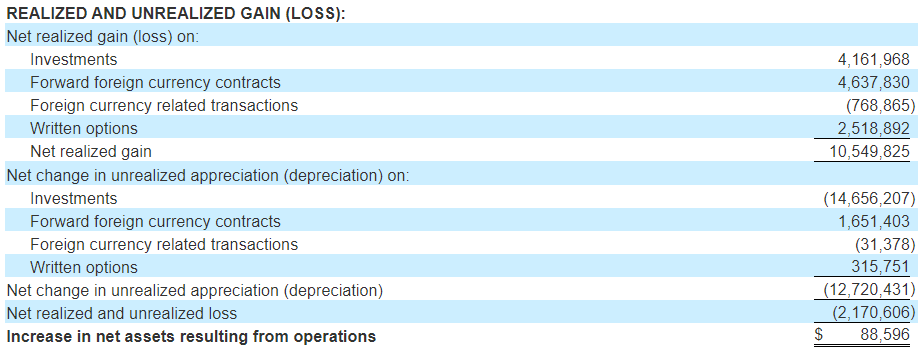

In looking at the distribution coverage from their last semi-annual report , coverage is looking great. Net investment income comes in quite light, but that's not anything unusual for equity-based CEFs. Instead, the realized gains they had produced took coverage well over the distributions paid to shareholders.

{kind=link}

Let's look at the breakdown of these realized gains further. We see that two sources contributed significantly outside of the usual realizing gains in underlying positions. That comes in the form of written options but even more so from the forward foreign currency contracts. Two sources that can produce gains, no matter the market conditions. The caveat is as long as they are on the right side of the trade.

In fact, currency contracts were the largest contributor to the overall realized gains in the portfolio. As we know, the U.S. dollar strengthening was a big story of 2022.

{kind=link}

IGA's Portfolio

Besides the gains from the underlying derivatives employed in the portfolio, the sector weightings combined with that to produce much better overall results for the fund. Overweight positioning in financials, healthcare, industrials and consumer staples were important driving factors. Following that were smaller weightings in energy and utilities, in which energy was the only positive sector and utilities were positive if you counted dividends.

Perhaps more important than being positioned heavier in better-performing sectors is the importance of not being invested too heavily in tech, communication services, consumer discretionary and real estate. Each of these was at the bottom or near the bottom half of performance for sectors in the last year.

IGA Sector Weighting (Voya)

At the end of the day, though, they are still a relatively diversified fund. By including IGA in one's portfolio, you aren't going to disrupt an already diversified portfolio. This is reflected by the fund's 244 total holdings, with the top ten amounting to a fairly small allocation. In this case, IGA's top ten represent 13.38% of the fund's total assets.

IGA Top Ten Holdings (Voya)

The only tech name we see here is Cisco Systems ( CSCO ). However, it's a fairly established tech name too. While it hasn't had the best performance in terms of share price in the last year, along with the rest of tech, it has provided a strong dividend. Those dividends get passed through into the total investment income of the fund, then to net investment income and make their way to investors' bank accounts through the distributions paid out from IGA.

We also see that Verizon Communications ( VZ ) is a position here. Again, this was in an unfavorable sector for the last year (communication services). Although some of the biggest declines in that sector were from the likes of Meta Platforms ( META ), VZ certainly didn't help.

VZ is in the fourth largest position in the Communication Services Select Sector SPDR ( XLC ), behind META in the top spot and then Alphabet's ( GOOG ) and ( GOOGL ).

Ycharts

Conclusion

IGA's global positioning and value-oriented portfolio hindered the fund through most of the last decade. However, the value-oriented tilt of the portfolio meant that results were much more attractive in the last year relative to the "broader market." With the fund's global exposure, the fund could experience more luck going forward. At the same time, the fund's attractive discount and seemingly sustainable distribution make it a fairly tempting offering.

For further details see:

IGA: Strong 2022 Results, Still A Buy At Current Levels