SURG - Ignore The Market SurgePays Is Doing Great

2023-08-28 07:30:00 ET

Summary

- SurgePays had a strong Q2 performance, with record revenue, EBITDA, and net income, and is on track to meet its full-year guidance.

- The company is expanding its distribution methods and is on track to be in 13,000 stores this year and 25,000 stores next year.

- Valuation multiples are depressed and even a conservative DCF doubles the share price, signaling an undervalued stock.

I am revisiting my Q1 thesis on SurgePays (SURG) in light of Q2 earnings.

Looking back on my Q1 analysis, I rated SurgePays a Buy and felt the business was on the verge of rapid scaling. Three key factors played into my recommendation. First and foremost, SurgePays turned profitable in Q1, and management guided it to even more growth in the back half of the year. Specifically, management guidance put the EBITDA margin in the double digits after being unprofitable for years. Second, the neighborhood store distribution model drove a low acquisition cost with significant room to grow. Finally, valuations were depressed relative to the industry and reflected an unprofitable business.

My downside concerns were around overreliance on government subsidies, competition, and the ability to deliver on the scale promised by management.

Since my last analysis, SurgePays shares have dropped more than 30%. Most of the decline occurred in July following negative reports on SurgePays regulatory compliance, which the company has strongly disputed.

The negative report aside, SurgePays had a great Q2, and I was pleased with the earnings . Profitability improved to record levels, and the company is still on track for its Q1 guidance . The Affordable Connectivity Program is going strong, and the company is expanding its distribution method while staying on track for its neighborhood store acquisition target. Valuation multiples are even more depressed than in my previous analysis signaling an undervalued stock.

With SurgePays meeting every point in my Q1 thesis and delivering performance in line with management guidance, I continue to believe there is an upside to the stock, especially at a lower price, and maintain my buy rating.

Expansion Is On Track

SurgePays primary method of expansion is partnering with convenience stores to install tablets that allow customers to sign up for subsidized cell service. The company announced in Q1 their goal to be in 13,000 stores and confirmed in the Q2 earnings discussion that they are on track for this goal.

In addition, SurgePays added two new distribution methods this quarter. They are partnering with SurgePays Announces Partnership with ParichuteConnect to increase awareness of subsidized cell service through public schools and community service organizations. They have also partnered with SurgePays Announces "Direct to Consumer" Partnership with LeadEx Solutions to prompt customers during ATM transactions. Both avenues represent an additional source of customers with a low cost of acquisition.

Since SurgePays relies heavily on the Affordable Connectivity Program , there have been valid concerns about the program's sustainability. Currently, funding is expected to be depleted by mid-2024; however, broad bipartisan support for the program is highly likely to be renewed in some form or fashion.

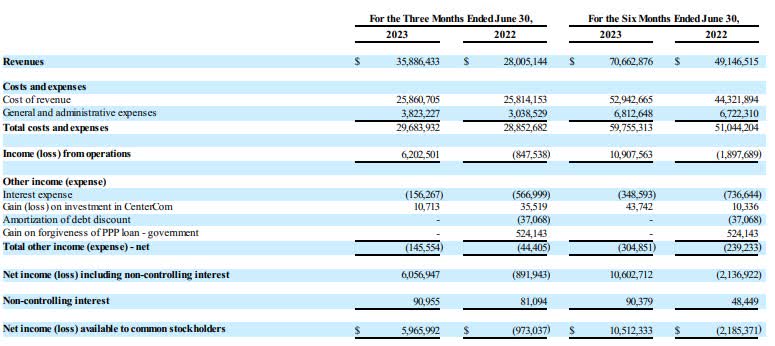

Record-Setting Q2 Performance

In the Q1 2023 earnings release, management set the following guidance:

2023 Earnings Guidance (SURG Investor Relations)

Critical to note from the earnings discussion that the scale-up is heavily backloaded, primarily late Q3 onward, due to supply chain delays in 2022 that have now been resolved. So far, SurgePays is right on track.

{kind=link}

In Q2, SurgePays posted record revenue, EBITDA, and net income. The business is 37% on its way to full-year revenue guidance, consistent with scaling expectations. While SurgePays doesn't provide profitability guidance, they are 40-45% of the way to my EBITDA estimate from Q1 of $26 to 30 million, ahead of expectations.

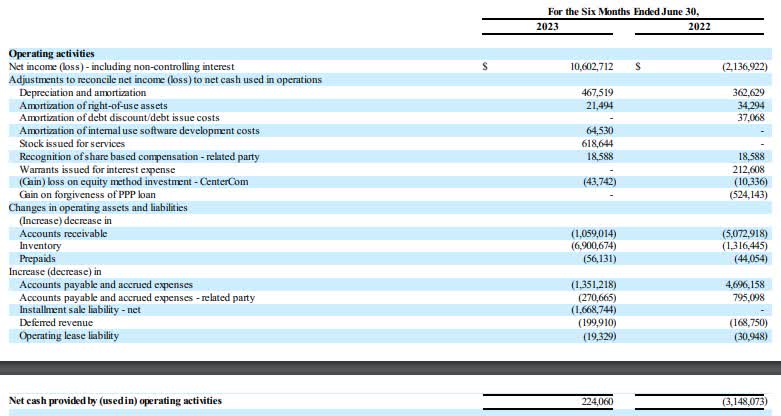

Cash flow improved despite significant investments in inventory, and SurgePays has already turned operating cash flow positive, well ahead of schedule. Inventory versus net income should improve as more stores come online annually.

{kind=link}

Lastly, let me comment on stores and subscribers. SurgePays doesn't report stores, but management confirmed in the earnings call they are on track for 13,000 stores this year and 25,000 next year. They do report subscribers in the 10-Q and are at 275,000, up from 130,000 in the prior year and 55% of the way to the annual target.

Buy Signals Across The Board

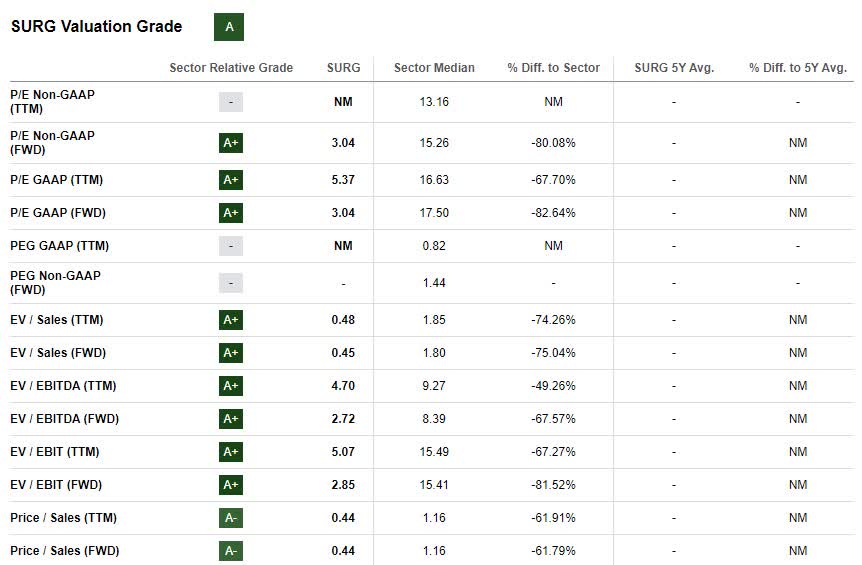

SurgePays is flashing buy signals across the board. First, valuation multiples are extremely depressed relative to the industry. This looks to me like the ratios for an unprofitable company, not one with a double-digit net income percent.

{kind=link}

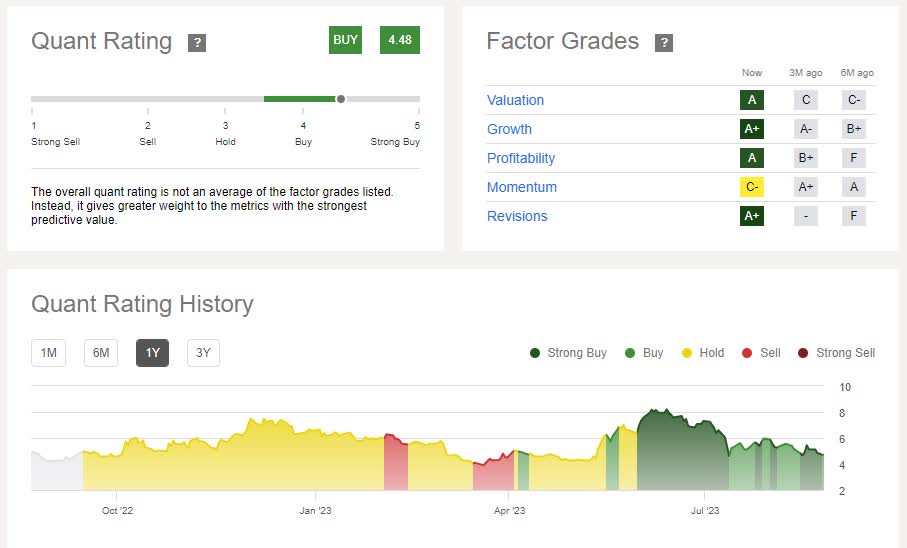

Next, the quant rating signals a strong buy across every measure except Momentum. Momentum of course is weighed down by the regulatory compliance allegations discussed above. Even with those allegations, quant is still a buy.

{kind=link}

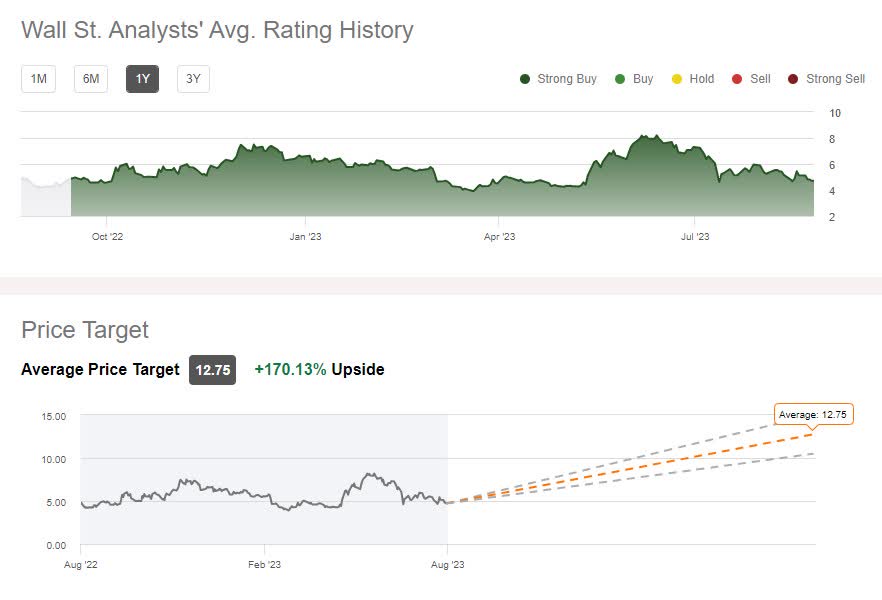

Wall Street Analysts consistently provide a strong buy with an average price target of $12.75.

{kind=link}

Under a very conservative DCF, I get a price target of $9.92, nearly double the current price. This DCF assumes management delivers on 2023 guidance, the Q4 performance annualizes to 2024 performance, and the business grows at 3% with improvements to investment in inventory.

{kind=link}

Downside Risk

Downside risks are similar to my previous analysis. However, I believe they are starting to mitigate. The largest risk to SurgePays business is a sudden disruption to the Affordable Connectivity Program. As discussed above, this is unlikely to happen given the broad bipartisan support for the program, especially in an election year. As the customer base grows larger, SurgePays will also have an easier time keeping a solid customer set, even if the program changes.

Another risk is competitive pressure from other players in the space. Certainly, other Affordable Connectivity Program Providers are offering ACP services, but no other provider has yet to approach consumers like SurgePays. Even if another company moves to this distribution model, SurgePays is several years ahead and has existing relationships with convenience store partners that will protect their revenue.

Lastly, there is a risk of SurgePays not delivering on scale. Specifically, not being able to get into 13,000 stores this year and 25,000 by next year. So far, SurgePays is on track for this goal and has diversified into other distribution channels. While they have to continue delivering in Q3 and Q4, so far so good.

Verdict

SurgePays has showcased resilience and controlled growth despite facing regulatory compliance allegations. The company's Q2 performance was impressive, with record-breaking revenue and EBITDA figures keeping the business on track for its full-year guidance.

I feel the expansion and diversification of their distribution model have positioned SurgePays favorably in the market and will help stave off competition. With valuation multiples significantly depressed and conservative DCF well above the current market cap, there's a strong signal for an undervalued stock.

I believe the downside risks, including competition and reliance on government subsidies, are being well managed and do not overshadow the potential upside. With that in mind, I maintain my Buy rating for SurgePays. The company's recent performance and promising strategies lead me to believe there is significant upside potential, particularly at the current share price.

For further details see:

Ignore The Market, SurgePays Is Doing Great