DDOG - IGV: Every Investor Needs Diversified Software Exposure (Rating Upgrade)

2023-08-28 06:28:08 ET

Summary

- iShares Expanded Tech-Software Sector ETF has outperformed the S&P 500 by 150%+ over the past decade.

- Strong catalysts supporting the software sector include the proliferation of mobile devices, the growth of enterprise software, migration to the cloud, and the emergence of AI.

- Top holdings in the IGV ETF are increasing margins as they continue to scale up their fast-growing SaaS-based business models.

I advise investors to build a well-diversified portfolio (built on a foundation of the S&P 500) and to hold it through the market's up-n-down cycles. In my opinion, such a portfolio should have strong exposure to software stocks. Today, I'll explain why that is the case, and why the iShares Expanded Tech-Software Sector ETF ( IGV ) is an excellent way to achieve that exposure. That's because if your goal is to beat the returns of the S&P 500, which is certainly my own personal goal, the IGV ETF has a long-term track record of doing exactly that. The graphic below compares the total returns of the IGV ETF to those of the Vanguard S&P 500 ETF ( VOO ):

As you can see in the graphic, the IGV ETF has outperformed the S&P 500 by 150%+ over the past decade.

Investment Thesis

But of course the investment thesis going forward cannot simply be built on past accomplishments. And going forward, the outlook for the coming decades is just as bullish - if not more so - than it was over the past decade. I say that because there are multiple strong catalysts supporting the software sector, some of which include:

- The proliferation of mobile devices.

- The proliferation of apps, be they mobile or on desktops.

- The growth of enterprise software.

- The need for creative productivity enhancements.

- The demand for clean-tech optimization, and for that matter - process optimization across practically all sectors.

- The need for all governments, companies, and consumers to have cybersecurity protection - it's no longer "optional".

- Last, but certainly not least, the emergence of AI is going to turbo-charge what was already a rapid migration to the cloud.

Next, most all leading software companies operate software-as-a-service (SaaS-based) platforms that are easily and efficiently scaled-up. That is, the investment in software development and platform operation/functionality has already largely been made for customer "A", so it is very little cost, time, and effort for the company to add customer "B".

In addition, most of these companies operate on a subscription basis, and these subscriptions generate "ARR", or annual recurring revenue. Growing ARR via subscriptions on a SaaS-based platform is the essence of success for most of these software companies because it increases margin while solidifying long-term revenue.

In December of last year, toward the end of the mauling the technology sector got in the bear market, I cautioned investors not to give up on the software stocks (see IGV: Software Is Dead, Long Live Software - an Seeking Alpha Editor's Pick). Since that buy-rated article, the IGV has nearly tripled the returns of the S&P 500. In April, I changed my rating to a HOLD because I thought that inflation would take a bite out of the software sector (see IGV: Did OPEC+ Just Kill The Tech Rally ), but the ETF just kept rising as calendar Q2 earnings reports continued to be robust (see examples below). Indeed, just last month, Credit Suisse gave 10-reasons why investors should stay over-weight software. One big reason is that AI is just accelerating what already was a fast migration to the cloud.

With that as background, let's take a look at how the IGV ETF's portfolio has positioned investors for success going forward.

Top-10 Holdings

The top-10 holdings in the IGV ETF are shown below and were taken directly from the iShares IGV webpage where investors can learn more details about the fund:

iShares

The top-10 holdings equate to ~59% of the entire 117 company portfolio and is what I consider to be a relatively and moderately concentrated allocation.

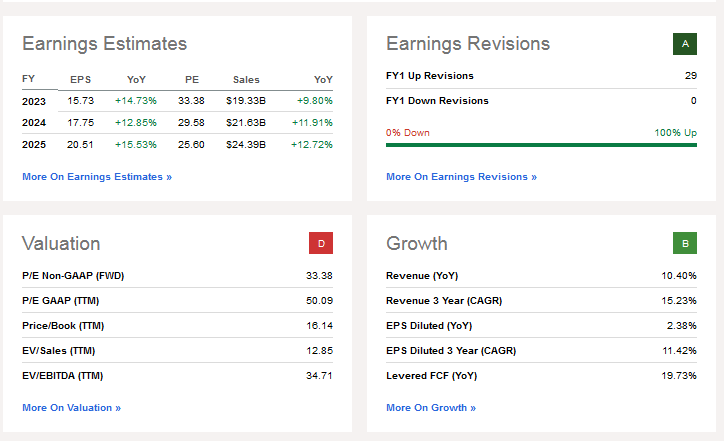

The #1 holding with a 9.6% weight is Adobe ( ADBE ). I covered Adobe, and it's Creative Cloud platform, back in August of 2020. I started the company with a HOLD due to what I considered to be a very high valuation (TTM P/E=57x, forward P/E=45x). That turned out to be a good call as the S&P 500 has outperformed ADBE by 13% since that article was published. However, with that Creative Cloud platform firmly established, Adobe is in a great position to leverage AI across its products, making them more creative and compelling than ever before.

Today, ADBE is still very richly valued (TTM P/E=48.8x , forward P/E=33.4x ), but note the forward P/E has dropped by 25%. The Seeking Alpha summary page pretty much shows the basic risk/reward opportunity for investors:

{kind=link}

As you can see, the go-forward earnings estimates indicate a yoy growth rate in earnings of ~15%, significantly higher than revenue growth (i.e. the power of scaling up a SaaS-based platform). As you know, and all things being equal (but acknowledging they seldom are ...), a stock growing at 15% should double every 5 years. The other side of the coin, of course, is that ADBE earns a low valuation grade ("D").

However, the current valuation level seems rational to me. I say that because in ADBE's Q2 report came in better than expected and the company raised the midpoint of FY23 adjusted earnings from $15.45/share to $15.70/share . ADBE ended the quarter with $14.14 billion in Digital Media ARR, +15% yoy on a constant currency basis. Note Adobe ended the quarter with only $3.63 billion in long-term debt, and $6.60 billion in cash, for a solid net-cash position.

Salesforce.com ( CRM ) is the #3 holding with an 8.0% weight. Last week, Seeking Alpha reported that Wells Fargo analyst Michael Turrin said he is "confident" CRM can sustain double-digit growth while expanding margins, while also commenting:

Our recent checks suggests the demand environment appears to have stabilized, but optimism is also growing that the remainder of the year will prove stronger, with activity having more meaningfully picked up in June/July.

Effective this month, Salesforce raised list prices an average of 9% pretty much across it entire platform: Sales Cloud, Service Cloud, Marketing Cloud, Industries and Tableau. The price increase applies to new clouds purchases from both existing and new customers. Turrin has an overweight rating on Salesforce and a $250 price target (the stock closed Friday at $209.47).

Cybersecurity expert Palo Alto Networks ( PANW ) is the #7 holding with a 3.3% weight. PANW delivered a strong Q4 report that significantly beat bottom-line consensus estimates:

- Revenue of $1.95 billion was +25.8% yoy.

- Non-GAAP EPS of $1.44 beat by $0.15.

- Q4 billings grew 18% yoy to $3.2 billion. FY23 billings grew 23% yoy to $9.2 billion.

- Remaining performance obligation grew 30% year over year to $10.6 billion.

- For Q1, ADBE expects Non-GAAP net income per share in the range of $1.15 to $1.17 vs. consensus of $1.11 , representing yoy growth of 39%-41%.

Free-cash-flow was $388 million , for a FCF-to-revenue margin of 20%. Going forward, on an adjusted basis ADBE expects FY24 FCF margin will be in the range of 37% to 38%. The stock popped 4% higher after the report.

The IGV ETF has, in aggregate, allocated 6.2% of the portfolio in the two companies that arguably operate a duopoly in the EDA (electric design automation) space that supports the semiconductor design engineering community: Synopsys ( SNPS ) and Cadence ( CDNS ). Synopsys is +21.7% over the past year while Cadence is 25.8%. Both companies will be (and already have been...) beneficiaries of the AI boom in high-performance computing ("HPC"). It is impossible to design leading-edge semiconductors without robust tool support (take it from me, I was an electronic design engineer for 25 years).

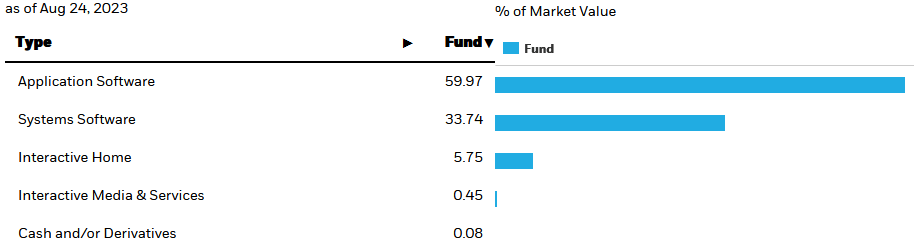

From a sub-sector allocation perspective, the IGV ETF is most highly exposed to the Application Software (60%) and Systems Software (34%) markets, which makes total sense to me.

{kind=link}

I say that because, although I disagree with much of what Cathie Wood says (specifically with her disruption/growth at any price "strategy"), she made a comment in a recent Barron's interview that rang true to me:

By our estimates, for every dollar of hardware sold around AI, we think the software pull-through will be somewhere between $8 and $21 . So we think the market and investors broadly are overlooking some massive AI opportunities in other stocks, more software oriented.

And most of that spend will be in application & systems. The ARK team does great research, they generally just seem to have trouble translating that research into sound investment strategies. Regardless, on this issue, I suspect that Wood's estimate will be toward the upper-end of that range. I say that because the hardware is typically purchased once (per technology node...), whereas the AI algorithms and LLM (large language models) is all software and will be running day-n-night through all semiconductor technology nodes. Not only that, many of these algorithms and LLM's - depending on the market - will need to constantly be updated and optimized.

I was slightly disappointed to see that one of my favorite software companies, Datadog ( DDOG ), only made the #22 position with a 1.1% allocation. DDOG is a free-cash-flow giant in the making.

Performance

I already touched on it, but the IGV ETF has a strong long-term performance track record, with a 10-year average annual return of a sparkling 18%:

iShares

That compares to a 10-year average annual return of 14% .

So, just in case there are investors that get confused on this issue (and believe it or not, there are...), the investment thesis here is capital gains, not income and not dividend growth. That being the case, IGV should be considered as a core technology and long-term holding in an IRA, Roth, or 401k retirement account.

The following chart compares the 5-year total returns of the IGV ETF with competitors: the Invesco Dynamic Software ETF ( PSJ ) and the SPDR S&P Software & Services ETF ( XSW ):

As they say, a picture is worth 1,000 words. However, if you look closer you'll see that the IGV ETF is still down ~22% from its all-time high from late 2021.

Risks

The primary risks of owning the IGV ETF are two-fold: first, it has a relatively high expense ratio of 0.41%. That is a full 38 basis points higher than the VOO S&P 500 ETF. But with this one: you get what you pay as it has significantly outperformed the S&P 500 and deserves the premium fee. And, if we neglect Microsoft's ( MSFT ) 8% allocation in IGV - because most all investors have adequate exposure to by directly holding the shares or through broad market ETF holdings - an investor would, in my opinion, need to hold at least 6-8 of the leading software companies to get adequately diversified exposure to the sector.

The second risk is larger: valuation. The following chart compares valuation metrics of the IGV ETF with the S&P 500:

As you can see, the IGV ETF trades at a whopping 2x premium to the S&P 500 (which, of course, includes most of the big software companies in the ETF). And, despite the ARR argument I made earlier in terms of stable go-forward cash flow, a slowing economy could certainly reduce the growth rates of these companies and, as a result, lower the valuation level. So too, could rising interest rates and a stronger U.S. Dollar. For more on that topic, consider reading my recent Seeking Alpha article: Energy In / Technology Out (another Editor's Pick).

With $6.5 billion in assets under management, there are no liquidity concerns with the IGV ETF. That's over 20x the size of the average ETF. And the average daily trading volume of 280 million is more than 200x that of the average ETF.

Summary & Conclusion

The iShares Expanded Tech Software ETF is more expensive than the ETFs I typically recommend for investors. However, one cannot argue with the fund's stellar long-term performance track record. That being the case, my opinion is that IGV is worth its relatively stiff expense fee (0.41%). And for that fee, investors get strong diversification in what already is, and will continue to be, a critically important sector within the overall market. I believe the Software Sector will continue to outperform the S&P 500 for many years to come.

IGV is a BUY. That said, given the current macro-economic environment, and market action, I suggest investors looking to establish a full-position not to do it all at once. Scale into the fund over time - which should be at least a matter of months, if not a year or more.

For further details see:

IGV: Every Investor Needs Diversified Software Exposure (Rating Upgrade)