PACB - Illumina Pacific Biosciences And Oxford Nanopore Market Position Comparison

Summary

- The gene sequencing market is ripe for disruption.

- ILMN suffers from multiple strategic setbacks that will likely impact margins for years.

- Oxford Nanopore and Pacific Biosciences will likely grow at a faster pace than ILMN.

- The industry trades at high price multiples.

Investment Thesis

Gene sequencing revolutionized our understanding of the human genome and its function. Today, we can accurately identify thousands of genetic variations that contribute to human health and disease, opening up the possibility of personalized medicine - creating medicine that is customized to the individual. The decrease in the cost of sequencing expanded its use in every area of life science research, from investigating cancer to improving agriculture yields, and with that comes an attractive market opportunity.

In 2021 sales of gene sequencing devices and consumables exceeded $5.8 billion globally and are expected to reach $9.6 billion in the next five years. At the market's helm are Illumina ( ILMN ), a manufacturer and provider of high-throughput, automated DNA and RNA sequencing instruments, including the widely-used NovaSequ 6000 series. However, despite their technical prowess and their success at building profitable sequencing businesses, ILMN is still to fully recover from multiple strategic setbacks that plagued the company in recent years. In this article, we overview two rising stars in the industry, pioneering what we believe is an exciting new landscape of a sequencing technology-based business; Oxford Nanopore ( ONTTF ) and Pacific Biosciences ( PACB ).

Illumina

- Device Installed Base: 23,000

- Consumable Sales per Device (2021): ~$140,000

With a market share of over 70%, ILMN maintains its position as the industry leader in the gene sequencing market. It is one of the few companies with an established profitability record, rendering it the least speculative in the gene-sequencing device manufacturing space. Its competitive edge lies in production-grade sequencing devices with high throughput requirements, making them ideal for clinical labs, research, and pharmaceutical companies.

A series of setbacks in the past twelve to eighteen months have drained the company's cash reserves, created a regulatory compliance headache , put pressure on margins, and, by some accounts, culminated in the departure of key executives.

In a way, ILMN has been a victim of its success. Shares traded at high valuations, incorporating a high growth premium that reflects shareholders' confidence in its ability to deliver. Management felt the pressure and understood (before shareholders) that the company's organic growth wasn't enough to justify its valuation, especially as the competition started to increase.

After a botched acquisition attempt of Pacific Biosciences (shut down by regulators in 2020), ILMN shot itself in the foot, closing the Grail acquisition before gaining regulatory approval. In September 2022, the European Commission made its final decision to prohibit the deal. In December 2022, it issued a directive order for ILMN to divest its $8 billion acquisition. Here is what makes things worse. Grail was purchased when the market was sizzling hot, and if ILMN is to sell Grail today, it will most likely realize a significant loss, which explains the Q3 impairment charge announced last November.

ILMN now finds itself stuck with a company it will most likely spin out (awaiting a possible EU supreme court hearing), but in its current shape, Grail can't survive in the current market conditions. Bringing up a molecular diagnostic company to scale requires a significant amount of cash spanning many years, and investors today aren't keen on these types of ventures.

The European Commission and Illumina agree on one thing: make sure that Grail survives. The reasons are different, with the EU interested in establishing precedent, given that Grail/Illumina prohibition is the first case under the regulator's newly-amended Article 22 of the EU Merger Regulation (EUMR), which aims at targeting what the legislation calls "Killer Acquisitions," and although ILMN was never intended to "kill" Grail, the latter's failure would be an embarrassment for EU regulators.

Last December, the EU provided ILMN with what it expects from the California-based gene sequencing manufacturer.

First, the dissolution of the transaction must restore GRAIL's independence from Illumina , to the same level that GRAIL had prior to the completion of the transaction.

Second, GRAIL must be as viable and competitive after the divestment as it was before Illumina's acquisition, to ensure that the innovation race between GRAIL and its rivals can continue as before.

Finally, the divestment must be executable swiftly and with sufficient certainty , so that the pre-transaction situation can be restored promptly. European Commission Press Release . December 2022

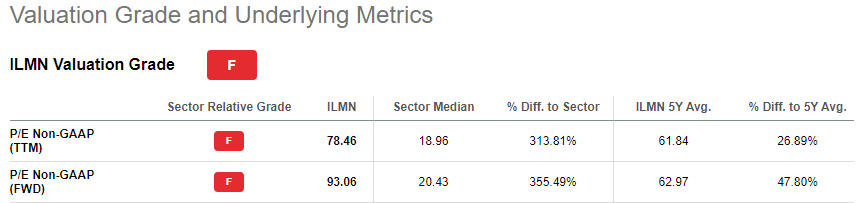

Balancing points two and three could be tricky. Bringing Grail to its feet is a long process, tainted with uncertainty. We'll have to see how long ILMN keeps Grail under its wing, but it could be years, putting pressure on margins. Last month, management guided non-GAAP earnings per share of $1.25 - $1.5 and a GAAP per share between $0.03 - 0.28$, with the difference stemming from the amortization of intangible assets, such as customer relations inherent from its acquisitions. Even when considering the Non-GAAP P/E, ILMN seems significantly overvalued.

{kind=link}

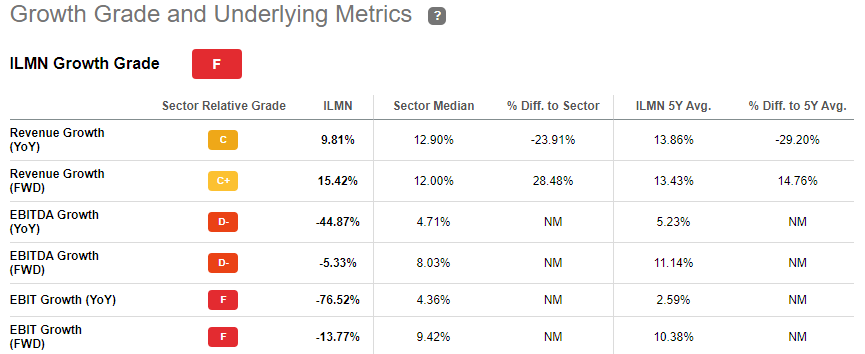

The acquisition of Grail also has created pressure on earnings growth, with no meaningful contribution to the top-line figure given its low revenue base.

{kind=link}

Pacific Biosciences

- Installed Base: 512

- Consumable Sales per Device: ~$139,521

The gene-sequencing industry is yet to design the perfect gene-sequencing instrument, and no single gadget is complete enough for all clinical and research uses. PACB found an opportunity to fill gaps lift by shortcomings in the ILMN portfolio by offering a different balance of the many trade-offs in device design, including price, speed, accuracy, and read length. For example, accuracy typically requires slower devices, while read size is negatively correlated with indel errors. For this reason, I believe that the market can accommodate multiple technologies. PACB can provide a significant asset given its high accuracy, exceptional read lengths, relatively affordable costs, fast throughput, and global footprint.

{kind=link}

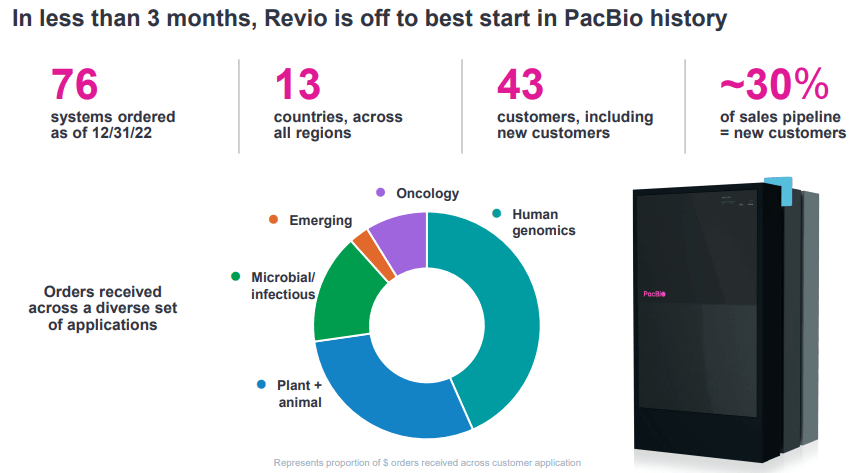

Stocks of PACB have gained ground in recent months after positive media coverage, thanks to a well-received new product roll-out. During the JP Morgan Health Conference, PACB CEO cited 76 new orders for its Revio Long-Read sequencers, a third of which are new customers, while the remaining are previous customers either upgrading their Sequel devices or expanding their capacity.

With the purchase of Omniome in the fourth quarter of 2021, PACB entered the short-read arena, competing more directly with ILMN's benchtop devices like the NextSeq and MiSeq series. The company will start shipping its new Onso short-read device later this year and is currently accepting pre-orders.

{kind=link}

The company is capitalizing on the share hype, manifested in its shares' momentum, pricing a $175 million equity offering at $10 per share, up from a previous plan of $150 million underwritings. Shares are currently trading near 12 months high.

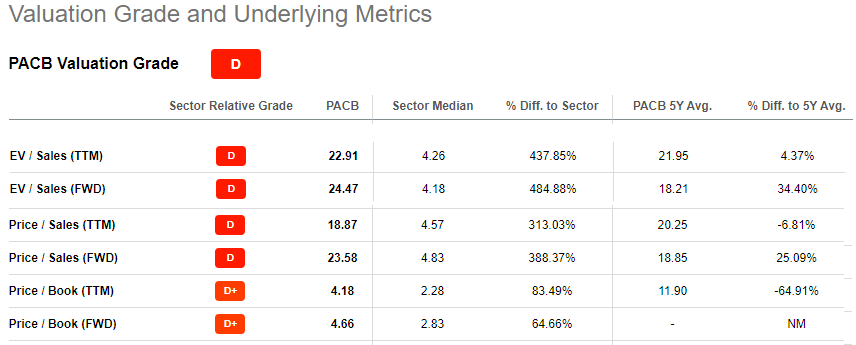

At current prices, the company seems overvalued, with a Price to Sales of 18x. Latest data show a cash balance of $850 million, weighed against $200 million of cash burn, making it one of the most well-funded third-generation gene sequencing companies on the market today. The company records $900 million in convertible notes maturing 2028. The company will likely convert this balance into equity, especially since the conversion ratio is out of the money at $43 per share. If converted, the number of shares outstanding will increase by 20,689,655, or 10% above the current share count.

{kind=link}

Oxford Nanopore

- Installed Base : 7300

- Consumable Sales per Device: ~$40,000

A formidable threat to US dominance in the gene sequencing market is arising across the Atlantic from the United Kingdom. Oxford Nanopore introduced new devices at attractive price points to cater to an expanded customer base characterized by fewer capacity needs and more simplicity. Its most prominent use was during the COVID pandemic, where its handheld sequencing devices allowed rapid deployment across the globe.

Oxford Nanopore

The market for DNA sequencing has historically been dominated by a few companies and research institutions that control the majority of the information and resources in the field. In 2014, the company introduced MinION, an affordable handheld sequencing device with a list price of $1000. Its affordable price democratized access and helped researchers with smaller budgets to publish their research, and in the process, created the academic research base necessary to validate the Oxford Nanopore platform. Thanks to the MinION device, Oxford Nanopore has a higher user base than PACB, with nearly 8000 users, 30% of ILMN.

ONTTF is less expensive than PACB but still trades at valuations above that a prudent investor would be comfortable with. Price/ TTM Sales stand at 10x, double that of the industry median.

ILMN offers guidance on what to expect from a mature gene-sequencing equipment manufacturer. ONTTF is still in its growth phase and will require many years until it realizes its potential. Last year, revenue grew by 50%, driven by expanded marketing sales operations and better-than-expected COVID testing in 2022. If ONTTF is to mimic the growth trajectory of PACB, we are looking at 20% - 25% revenue growth in the next five years. Based on these assumptions, and using ILMN's net profit margins, ONTTF's 2028 revenue and net profit should stand at $650 million and $100 million, respectively, barely justifying its current valuation of $2.6 billion.

Summary

The competitive landscape for the sequencing industry is ripe for disruption. In this article, we gave an overview of two rising stars pioneering what I believe is Third-Generation Sequencing. Growth for ONTTF and PACB will likely exceed the industry average of 7.5% in the medium term, fuelled by new product offerings filling the gaps left by ILMN's equipment shortcomings. For this reason, I believe that we should see further deterioration in ILMN's market share, especially beyond clinical diagnostic applications, where ILMN's high-throughput production-scale equipment enjoys a clear competitive advantage.

However, all three companies are overvalued to different degrees, with ILMN being the most expensive, while ONTTF appears to be the cheapest by some margin. But again, that is up to the reader to weigh those values against a variety of other factors that have not been discussed in this article, including opportunities arising from stock volatility, investors' sentiment, and perhaps more importantly, their desire to be part of the new genome revolution.

For further details see:

Illumina, Pacific Biosciences, And Oxford Nanopore Market Position Comparison