DMTK - Immunocore: Potential To Unlock Capital With New Melanoma Treatment Paradigm

Summary

- Clinical trial momentum within the Melanoma diagnostics and treatment paradigm is gaining steam.

- Immunocore Holdings plc presents with unique exposure for investors to position at the treatment end of the spectrum.

- Recent advancements in its investigational compounds are well received, with robust clinical data in support of the same.

- We believe Immunocore Holdings has potential to unlock long-term risk capital in this domain.

- Net-net, we rate Immunocore a buy, price objective of $61.15 based on 8.4x FY 2023 consensus book value per share of $7.23.

Investment summary

There's been multiple developments in the Melanoma treatment paradigm in 2022, ranging from diagnostics to treatment. Recently, we covered DermTech, Inc. (DMTK), noting its strengths in advancing diagnostic methods for advanced stage Melanoma. In that report, we also performed a deep dive on the Melanoma diagnostics and treatment market, and noted there is a strong expectation of growth looking ahead. You can check out our DMTK publication here.

Following this, we also examined Immunocore Holdings plc (IMCR) given its unique positioning at the treatment end of the Melanoma spectrum. Hence, I'm here today to discuss our examination findings on the stock. Net-net, we rate IMCR a buy, with several inflection points on the horizon, and tremendous support from existing investors in its latest round of equity financing. With these points in mind, we rate IMCR a buy at a $61.15 price objective.

Exhibit 1. IMCR 12-month price evolution and downshifting covariance structure.

This suggests investors are rewarding the stock on idiosyncratic features, and not as a function of equity market beta.

Data: Updata

Catalysts to move the needle: KIMMTRAK clinical trial momentum

KIMMTRAK (from hereon in, simply Kimmtrak) is a protein that is highly specific to gp100, a lineage antigen that is often expressed in melanocytes and melanoma cells. This innovative, bispecific protein is composed of a soluble T-cell receptor, which is fused with an anti-CD3 immune effector function. Using Immunocore's ImmTAC technology, Kimmtrak is designed to redirect and activate T-cells, enabling them to recognize and destroy tumor cells with precision.

Kimmtrak has received regulatory approval for the treatment of HLA*A2:01-A-positive adults with inoperable or metastatic uveal melanoma in several jurisdictions including the U.S., EU, Canada, Australia, and the UK. The targeted therapy is the first of its kind to emerge from the ImmTAC platform, promising to revolutionize the treatment of melanoma and other forms of cancer if it were to successfully pass through to commercialization.

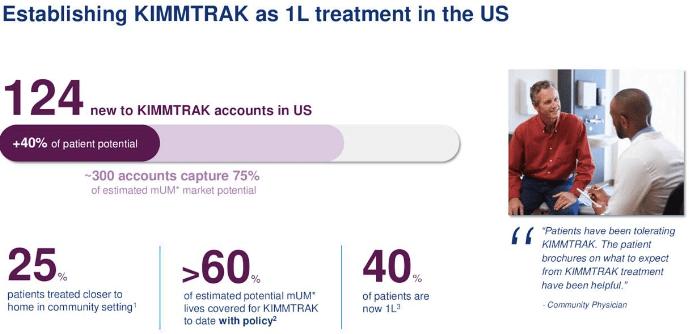

KIMMTRAK's momentum in the U.S. market so far

{kind=link}

Kimmtrak' safety and efficacy is being investigated versus a compound of investigator choice, for treatment of advanced uveal Melanoma. The study will assess the impact of Kimmtrak on overall survival in individuals with advanced melanoma, that has progressed despite treatment with anti-PD1 therapy and, if applicable, tyrosine kinase inhibitors.

It's worth noting the randomized clinical trial ("RCT") is a Phase 2/3 trial. Participants will be assigned to one of three groups, including treatment with Kimmtrak alone or in combination with an anti-PD1 agent, or a control group. Patients in the control arm will have the option to receive "real world" treatment, including participation in other clinical trials, while being followed for overall survival.

The Phase 2 portion will include 40 patients cohort per arm, and will measure both overall survival and a reduction in circulating tumor DNA as primary outcome measures. Whereas the Phase 3 portion is planned to enroll 170 patients per arm, with overall survival as the primary endpoint. Noteworthy, however, is the design of Phase 3 - including eligibility criteria, the potential discontinuation of an arm, and statistical considerations - may be modified based on the results of Phase 2.

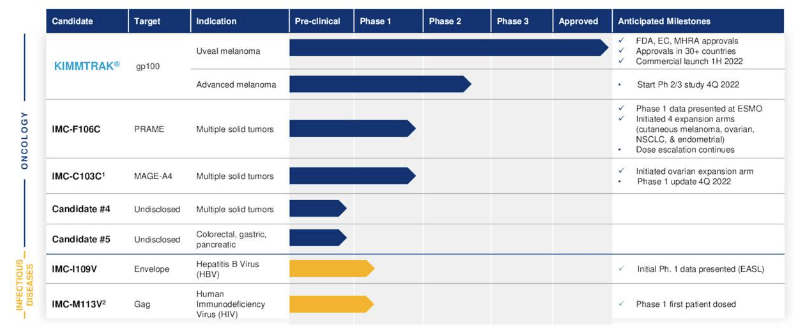

These are meaningful catalysts that have potential to add additional torque to IMCR's flywheel. We'd encourage investors to keep active on the stock as readouts emerge in 2023. You ca see IMCR's full pipeline in the image below.

Exhibit 2. IMCR Clinical pipeline

{kind=link}

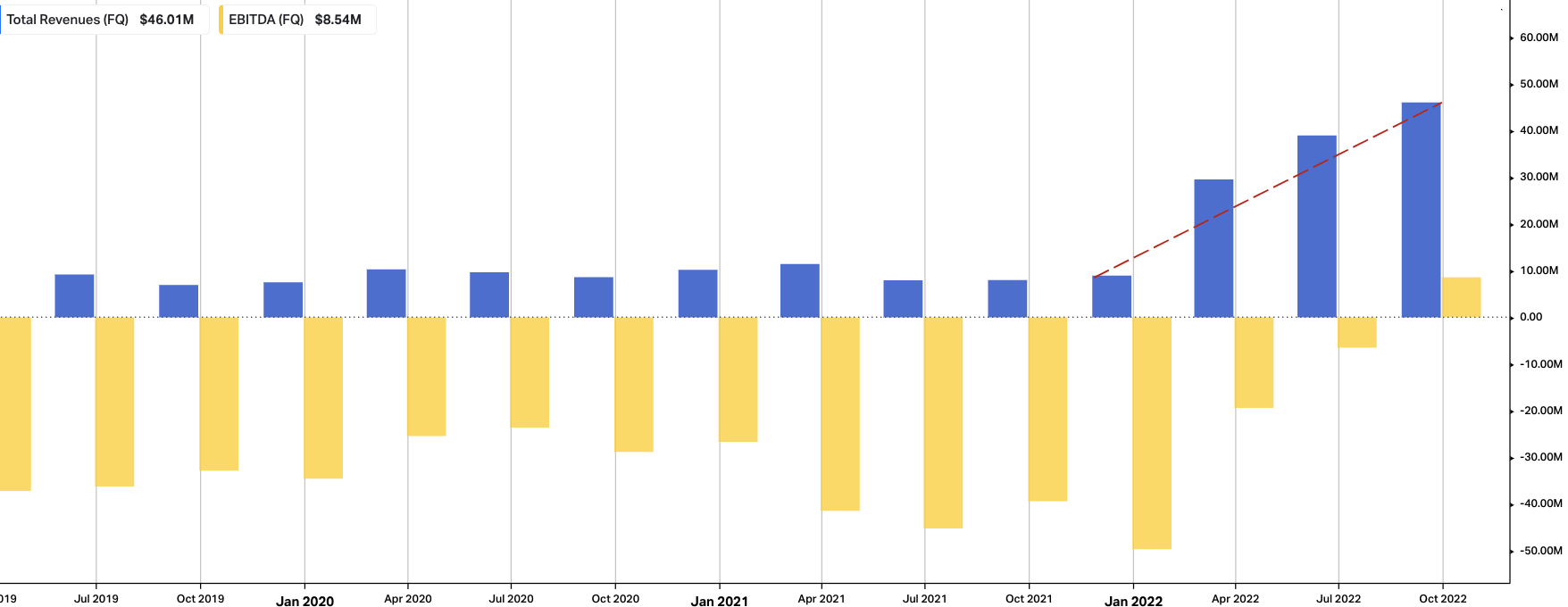

Q3 financials: a reasonable period of growth

Turning first to the numbers, we saw IMCR report net Kimmtrak [tebentafusp] revenues of $40.4mm, a 20% YoY increase. It brought this down to EPS of $0.14, well up from the loss per share last year. In July 2022, Immunocore also announced a private investment in public equity ("PIPE") financing with four existing investors, yielding net proceeds of $139.6mm.

This funding, alongside anticipated revenues from Kimmtrak and current cash reserves, is expected to provide sufficient cash runway through to 2025. In addition, the company has entered into a loan agreement with investment funds managed by Pharmakon Advisors, providing up to $100mm in committed funds.

The initial $50mm drawn from this credit facility will be used to refinance Immunocore's existing debt with Oxford Finance on improved terms, while the remaining $50mm [if utilized] will be directed towards advancing its pipeline for conversion. In our opinion, this evidences the positive steed in which the company's investors view its long-term outlook, and ability to unlock risk capital. To attract $100mm in equity investment this year when the cost of capital is at multi-year highs, in addition to a less supportive funding environment, is ample evidence of the same.

Moving down the P&L, we'd also note that IMCR booked a quarterly operating profit of $6.9mm, a significant upshift from the $31mm operating loss in the same quarter of 2021. Note, this profit was largely due to FX gains of $16.9mm from the GBP/USD pair. Importantly, R&D investment for the third quarter was $25.9mm, compared to $16.8mm for the same period in 2021. Conversely, IMCR lost some leverage at the SG&A line, with Q3 expenditures of $13.0mm compared to $20.0mm last year.

You can see IMCR's revenue ramp in the chart below [Exhibit 3] which has demonstrated a sequential uplift over the course of 2022. At the same time, core EBITDA is now in the black. This is a solid bedrock for the company looking ahead, as it is well capitalized to continue funding its pipeline.

Exhibit 3. IMCR quarterly operating performance, FY19-date [revenue, core EBITDA]

{kind=link}

Valuation and conclusion

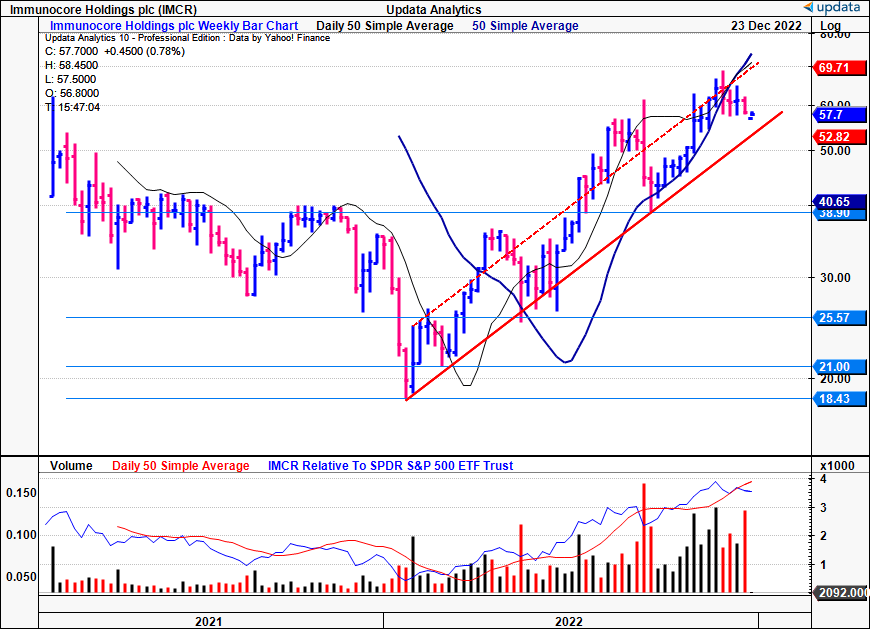

You'll see in the chart below that IMCR's price evolution across 2022 has been heavily skewed to the upside. It remains in a near 12-month long uptrend that's tested support 3-4x across the year, pulling away each time.

It now trades in sideways consolidation, although, as you'll see, the weekly volume trend continues to ascend, suggesting accumulation from larger accounts. Moreover, the presence of sideways price action with ascending volume is evidence of strong support in our opinion.

Exhibit 4. IMCR 24-month price evolution [weekly bars, log scale]

{kind=link}

It's worth noting the stock trades at 16x forward sales and is richly priced at 8.4x book value. However, we'd also advise that IMCR's increased its book value per share by ~34% YoY to $6.15, ahead of the S&P 500's total loss of 18.5% for the last 12 months. Looking ahead, at the 8.4x multiple, and noting IMCR's consensus estimates of $7.28 in FY23' book value per share, this derives a price target of $61.15.

In our opinion, this represents value creation and, therefore, justifies the premium. You'll also note the stock is attractively rated using Seeking Alpha's quantitative factor gradings, scoring in the green across most measures bar valuation. This must be heavily factored into the investment debate also. Rate buy, $61.5.

Exhibit 5. Seeking Alpha Quant ratings, IMCR

Data: Seeking Alpha, IMCR quote page

For further details see:

Immunocore: Potential To Unlock Capital With New Melanoma Treatment Paradigm