PI - Impinj: Valuation Is Frothy Despite Pullback And Future Opportunities

2023-10-18 01:41:27 ET

Summary

- Impinj has long-term opportunities to expand into more complex cases and other verticals, like the logistics market.

- The company faces risks such as timing on large deployments, inventory issues in the apparel industry, inflation, competition, and financial risks.

- PI stock's valuation is still high despite recent declines.

Impinj ( PI ) has some nice, long-term opportunities, but its recent issues and valuation keep me on the sidelines.

Company Profile

PI is an Internet of Things (IoT) company that provides a platform to connect and track items via RAIN technology, a version of radio-frequency identification, or RFID. The company provides endpoint integrate circuits (ICs) that have miniature radios-on-a-chip that can wirelessly connect to its platform. These endpoint ICs attach to an item and can have features such as data storage, security, authentication, and loss prevention. The ICs can be placed on a tag or directly embedded into an item. The company notes that the ICs cost pennies.

In addition to the endpoint ICs, PI's system includes readers and gateways that can bidirectionally communicate with the endpoint ICs. The company says it sells its IC readers to ODM partners that use them in mobile or handheld readers, fixed readers, gateways, RAIN-enabled appliances, and other intelligent edge devices.

Opportunities & Risks

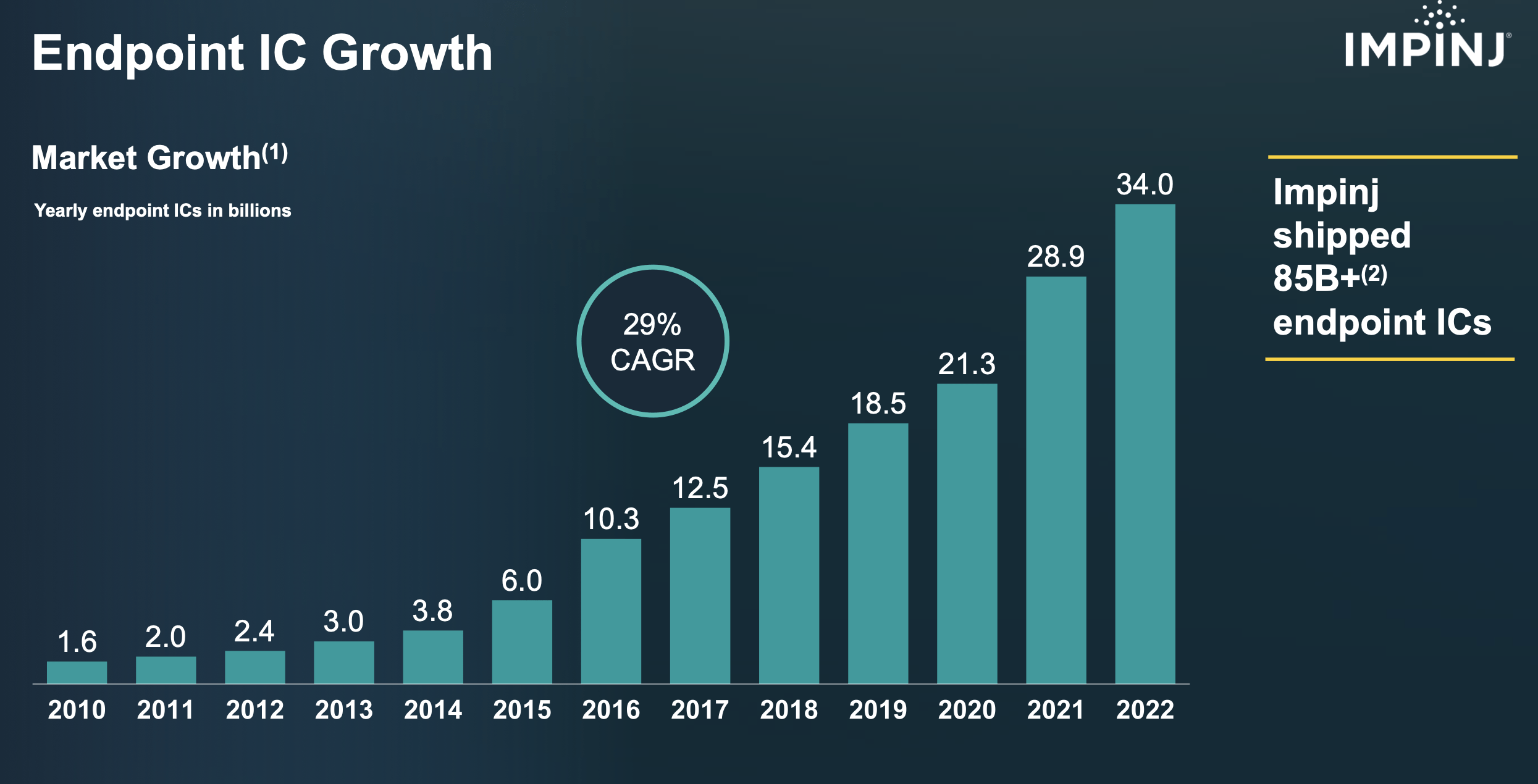

The biggest market for PI's products has been the apparel retail industry. The company has seen solid success in this vertical, with about 25-30% unit compounded growth rate ((CAGR)) over the years. The company is about 30% penetrated in this vertical, so it continues to have room to run.

{kind=link}

Within the retail apparel category, the company also can offer more beyond simple inventory cases into more valued complex cases. Discussing this at a Goldman Sach's conference last month , CFO Cary Baker said:

So think of retail inventory visibility. As I said it before, the base use case, it's counting the items in the store using a handheld reader. That's designed for a mix-and-match solution. When we move to loss prevention, that's a more complex solution because now you're putting a reader at the point-of-sale terminal to read all the items and enable that self-checkout environment. You're also putting an algorithm in the reader telling the tag to turn off so that when you walk out the door, it doesn't trigger the alarm. And then you're also enabling the returns desk to have a similar reader with the algorithm there to send that 8-bit pin back to the chip telling the tag to turn back on, so the item can be reshelved and sold to the next customer. That entire experience relies on our platform to deliver that solution I just described. So it's much more complex than the base case. So we talk about 2 platform or 2 lighthouse accounts right now. One is our visionary European retailer that's doing the loss prevention deployment and now moving into self-checkout as well."

Moving into general merchandise and logistics are two big opportunities for the company. Both are larger opportunities than retail apparel, as apparel retail is an 80 billion unit opportunity, while general merchandise is 325 billion units per year and logistics is 400 billion per year. PI is currently less than 1% penetrated in these two areas.

The company does have a major North American Logistics company that is using one of its more advanced solutions. This appears to United Parcel Service (UPS), which has been touting its Smart Package Smart Facility RFID solution. UPS is looking to have the solution in 900 buildings across the U.S. by the end of this month and has been seeing fewer missloads and higher productivity as a result. Given that such a prominent player has been touting its success with PI, this could certainly expand to other logistic companies and be a nice growth driver for PI.

The company also has other areas of opportunity, such as using its solution for other applications such as authenticity. The company started an authentication service earlier this year and has been piloting a number of programs. This is a more SaaS-type business, and it's seen interest from high-end fashion, as well as specialty foods, duty-free stores, and pharmaceuticals.

Now PI comes with plenty of risks also, as illustrated by the huge declines the stock has seen this year, including a -39.4% nosedive after it reported Q1 earnings back in April. The big drop was the result of the company calling for endpoint IC revenue to be flat sequentially given its "inability to predict the precise timing and pace of large deployments."

In Q2, meanwhile, the company's stock also took a hit when it forecasted a -25% sequential decline in revenue due to retail apparel destocking. PI noted that retailers had built IC safety stock as they expected a stronger apparel recovery which did not happen.

These two misses demonstrate two risks that PI faces. One is the timing of large deployments, while the other is its ties to the apparel industry and how it's impacted by inventory issues at its customers.

Inflation is another risk for the company While its IC endpoints at volume only cost between 3.5 to 4 cents, that isn't necessarily cheap for a retailer when considering how much unit inventory they carry. Prices have gone up which it has passed along, but the goal was always for prices to come down as wafer costs came down, drawing in more customers.

Competition is also a risk. While the company doesn't have a lot of competitors today, there is risk from emerging Chinese competition eventually showing up and competing on price.

In addition, PI has about net debt of $172 million, with operating cash outflows of -$49 million over the first six months of the year. Having net debt while burning cash carries risk.

Valuation

PI stock currently trades at 107x 2023 EBITDA estimates of $15.1 million. Based on the 2024 consensus projecting EBITDA of $25.5 million, it trades at 63x multiple.

On a P/E basis, the stock trades at an under 110x forward P/E ratio. The current consensus is that the company will generate EPS of 48 cents in 2023. For 2024, it is projected to produce EPS of $1.08, which would be good for a P/E of 49x based on 2024 estimates.

The company is projected to grow its revenue by 17.5% in 2023. For 2024, sales growth is forecast to 13.3%, with growth in later years of over 20%.

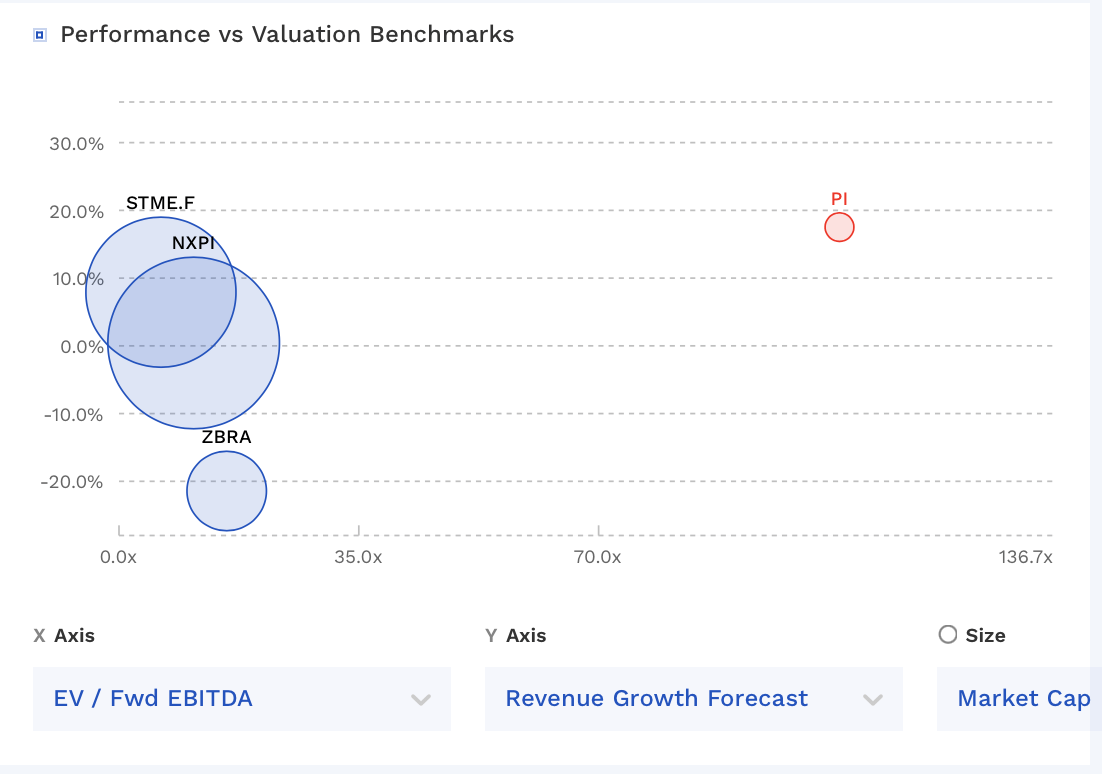

While PI doesn't have any great peers, it does trade at a significant premium to other somewhat similar companies.

PI Valuation Vs Peers (FinBox)

{kind=link}

Conclusion

PI has a lot of nice potential opportunities as it looks to expand into more complex cases and beyond apparel retail. Its early success helping UPS is a really nice opportunity to get further into the logistics market, which should bode well for the company over the long run.

In the near term, the company is dealing with issues in the retail space given its customers' destocking issues. This is something that has been common in the apparel industry over the past year or so due to over-ordering when there were earlier pandemic-related supply constraints. The fact that it is impacting PI should not come as a total shock, nor does it necessarily point to larger, long-term issues.

While there does look to be the potential for a nice PI turnaround next year, the stock's valuation is still quite high despite the large pullback in the name. Over 5x sales for a company with 50% gross margins, growing revenue sub-20%, and burning cash with net debt is too high of a valuation in my book. Putting a fair value on the company is difficult given its metrics, but I'd prefer to be a buyer at a much lower price, around $25-30. As such, I'm going to put a "Sell" rating on the stock at this time.

For further details see:

Impinj: Valuation Is Frothy Despite Pullback And Future Opportunities