AZN - Incyte: Making Hay While The Sun Shines

Summary

- It is useful to understand the financial implications for Incyte with its major product, JAKAFI, facing loss of exclusivity ("LOE") in 2028.

- 2028 is still five years away and JAKAFI continues to provide a powerful and growing stream of earnings and cash.

- The underlying earnings for JAKAFI are camouflaged by large R&D expenditures, providing an extensive portfolio of opportunities to offset the JAKAFI LOE by 2028.

- I find it useful to attempt some quantification of the financial outlook for Incyte from now through 2029, following JAKAFI LOE.

Incyte: Investment Thesis

Incyte (INCY) should experience strong cash inflows from both JAKAFI and OPZELURA over the next 6 years before JAKAFI LOE during 2028. JAKAFI LOE in 2028 will likely see underlying earnings retreat to below FY-2022 levels, unless additional new drugs are successfully developed and brought to market in the meantime. While R&D spend does not ensure success it is certainly a necessary part of achieving successful drug development and marketing approval. Fortunately, Incyte appears to be capable of generating cash flows over the next 6 years more than double cash flows over the last 6 years. Together with existing cash, future cash flows could likely allow Incyte to more than double average yearly expenditures from $1.3 billion yearly average over the last 6 years to close to $3.5 billion per year over the next six years. This cash availability could also position Incyte well for advantageous acquisition of promising drug candidates in an atmosphere where funding might become more difficult for smaller players.

Incyte remains a Buy at current share price, and even more so should the share price fall back from current levels.

A More In-Depth Discussion Of Incyte's Prospects

Incyte R&D -

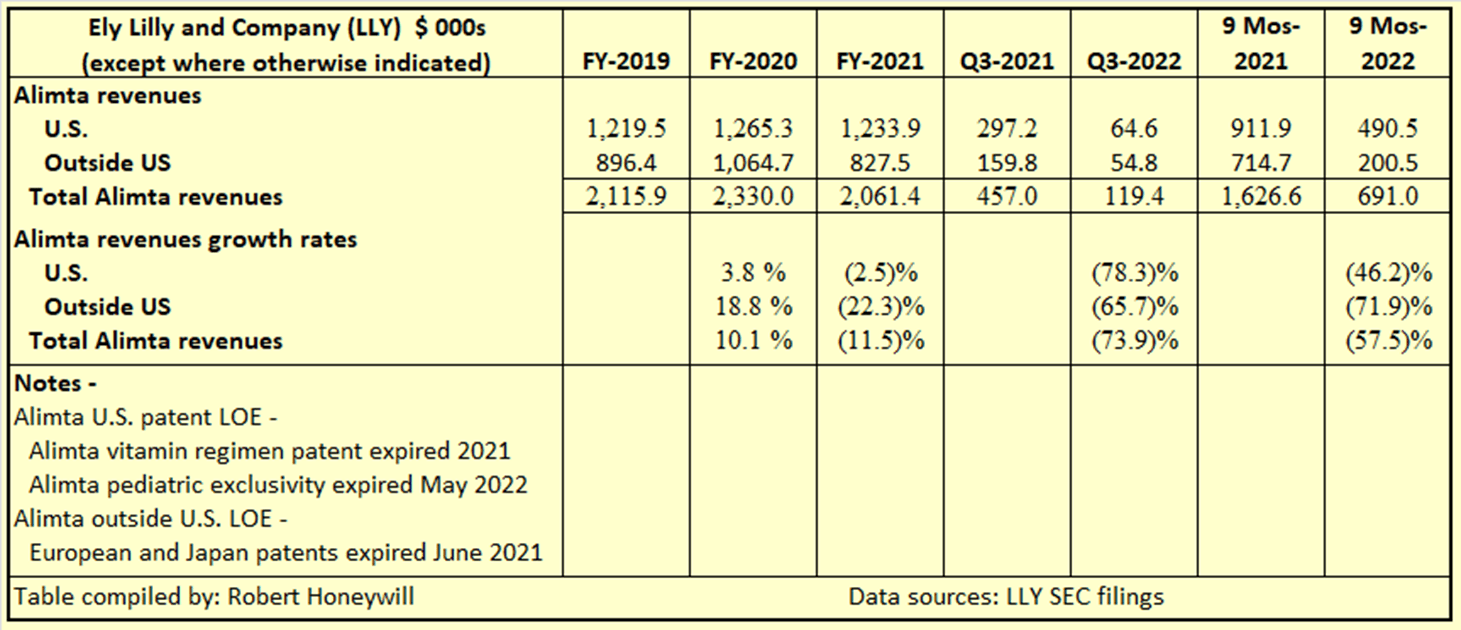

In previous articles on Incyte Corporation, I took a look at Incyte's results from a different angle to the company, and analysts as well. Incyte is investing a large proportion of its operating earnings in R&D. R&D is expensed against current earnings, so Incyte's results are materially impacted by R&D spending levels in any particular financial year. Separating out R&D allows a picture to emerge of growth in underlying operating earnings, including the contribution of newly developed formulations based on the company's immune modulating medication Ruxolitinib, marketed in the U.S. as JAKAFI and outside U.S. as JAKAVI. Incyte will suffer loss of exclusivity ("LOE") for Ruxolitinib in 2027/2028 as patent coverage expires. It is possible to extend patent lives by developing combination therapies involving two or more drugs, and novel delivery methods. Incyte R&D has been directed towards both combination therapies and developing new more friendly methods (e.g., topical vs injection) for drug delivery and for finding new indications to treat. As discussed further below, these new products have patents providing longer periods to LOE than the main product JAKAFI. This work is showing excellent results but there is a narrowing window for recovery of R&D investment and making outsize profits as LOE approaches from 2027/2028 onwards (hence the 'Making Hay While The Sun Shines' in the title). The revenue effect of loss of exclusivity for Eli Lilly's ( LLY ) oncology drug Alimta® in 2022, per Table 1 below, provides an indication of the potential impact on Incyte revenues of LOE for Incyte's main product, JAKAFI, in 2027/2028.

Table 1

{kind=link}

Table 1 presents a very sobering picture for anyone believing JAKAFI LOE will not be a hugely significant event for Incyte in 2027/2028. The Eli Lilly outcome is for just one product for one company. However, this 2019 study, " The effect of patent expiration on sales of branded competitor drugs in a therapeutic class ", indicated similar results from a broader study,

Composite quantity sales decreased by 49%, 65%, and 67% in the first three years, respectively, following patent expiration.

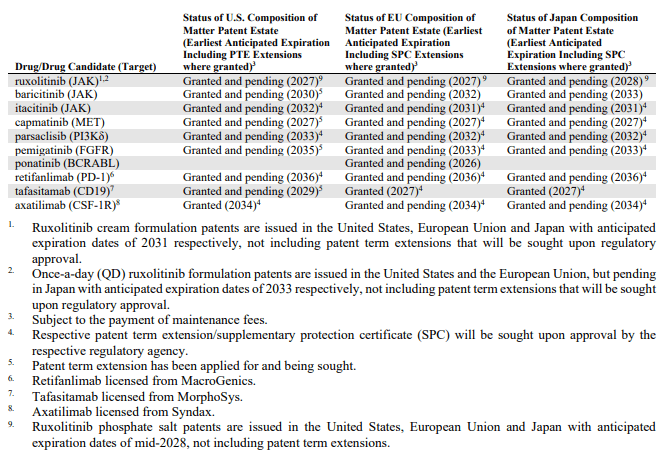

There might be some factors that make the impact less for Incyte than for Eli Lilly, such as loyalty of patients who have been using the one brand for several years for a chronic condition. Also, not all Incyte patents expire in 2027/2028 as per Figure 1 below from Incyte FY2021 Annual Report.

Figure 1

{kind=link}

Note 1 in Fig. 1 is of special significance as it indicates the LOE for Incyte's most promising new product, OPZELURA, a topical cream containing Ruxolitinib as the active ingredient, is not until 2031.

Separating out R&D from underlying operating earnings -

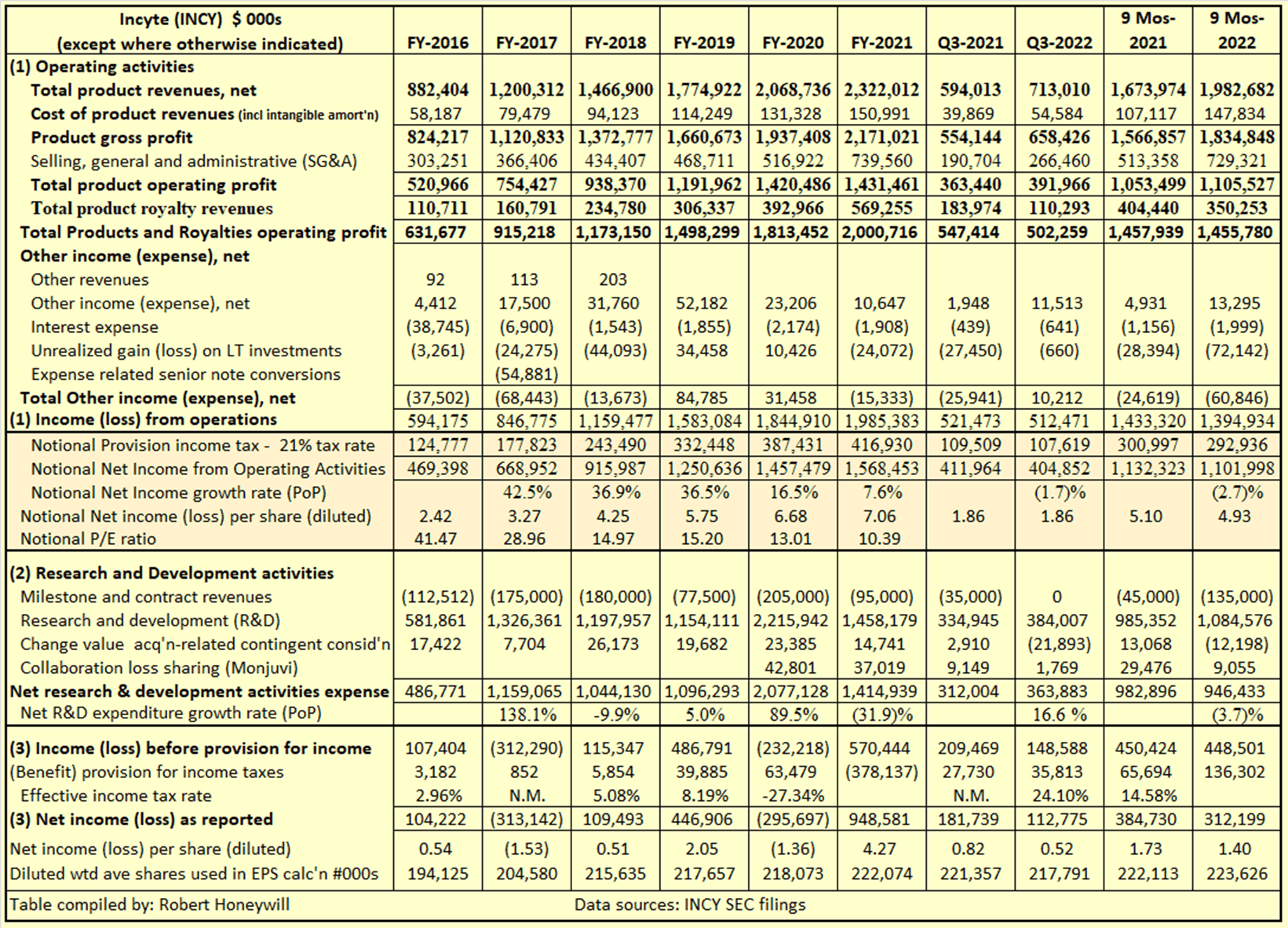

Table 2.1 below provides an alternative presentation of Incyte's income statement, separating out investment in R&D from underlying earnings from approved products generating income streams.

Table 2.1

{kind=link}

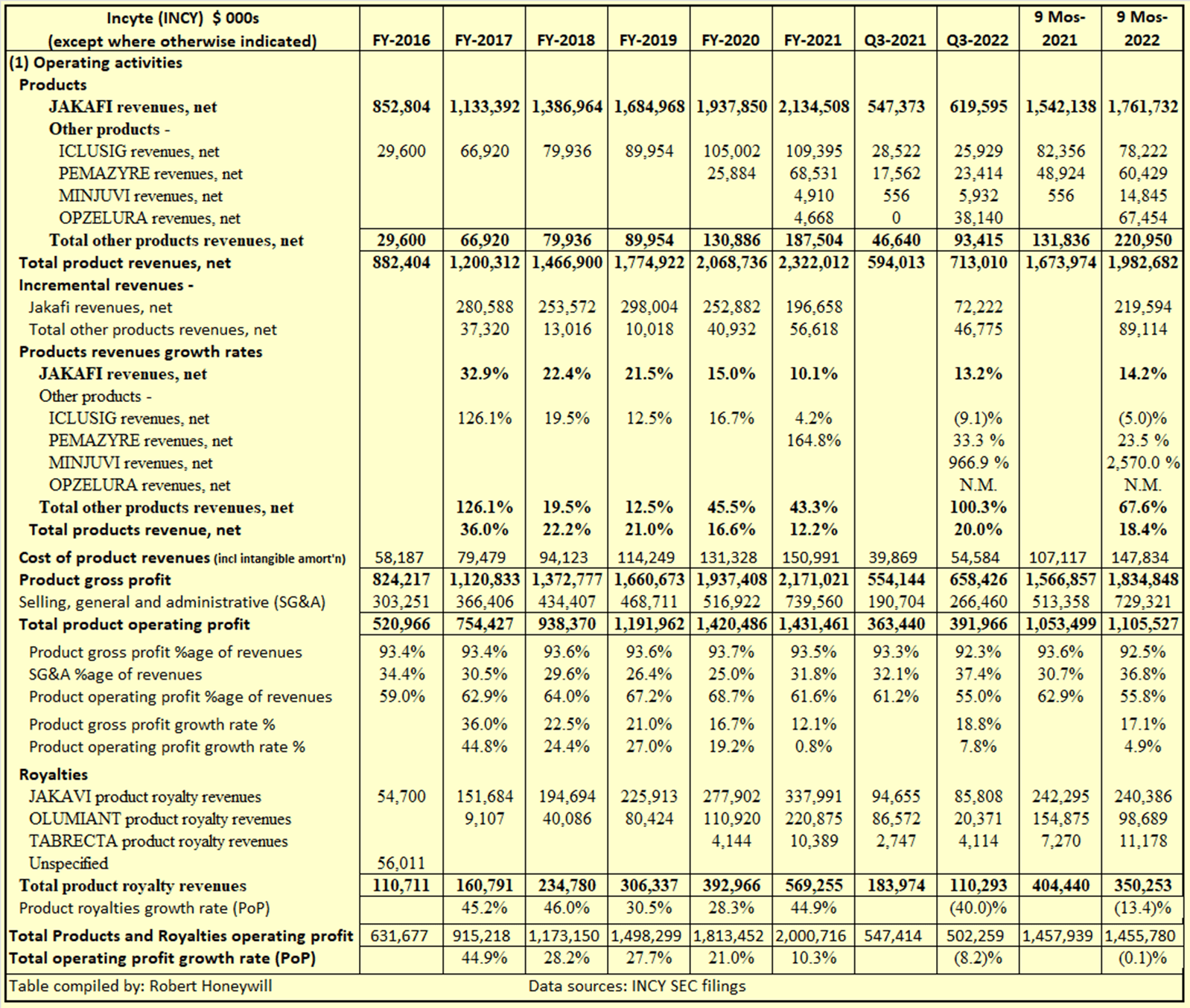

Table 2.1 shows Incyte spent $7.9 billion (before tax benefit) on R&D, an average of ~$1.3 billion per year for the 6 years FY2016 to FY2021. Table 2.1 also shows, over the same period, total notional income before tax from operations was $8.0 billion. This demonstrates Incyte has effectively funded all of its $7.9 billion in R&D over the last 6 years from operating earnings, requiring no borrowings. Notional net income has shown steady growth from $469 million in FY2016 (EPS $2.42) to $1,568 billion (EPS $7.06) in 2021, with notional P/E ratio decreasing from 41.47 at end of 2016 to 10.39 at end of 2021. But if shareholders are to benefit from the $7.9 billion invested in R&D then that amount and more must be recovered from future operating earnings, net of ongoing R&D expenditures. With patent expiry looming for the company's main revenue driver, that becomes a major issue. Table 2.2 below further analyses data in Table 2.1 to show details of product and royalty revenue growth rates and trends to date.

Table 2.2

{kind=link}

Despite introduction of new products, most of Incyte's revenues still come from JAKAFI sales in the US and JAKAVI (JAKAFI brand name outside U.S.) royalties. JAKAFI/JAKAVI revenues were 91.8% of total revenues in FY2019, 85.5% in FY2021 and 85.8% for nine months ended September 2022. Of non JAKAFI products, Olumiant showed promising growth in 2020 and 2021 due to use in COVID treatment but this has now ceased and revenues have fallen significantly in 2022. JAKAFI is still showing double digit percentage growth, resulting in incremental revenue growth far exceeding total incremental revenue growth for all other products. Outside JAKAFI, there is one product that promises to accelerate revenue growth markedly. This is the topical cream OPZELURA (ruxolitinib), approved by FDA in September 2021 as a second line treatment for moderate atopic dermatitis ("AD"). Since then, OPZELURA has also been approved for treatment of vitiligo. Initial quarterly revenues of $4.7 million in Q4 2021 have grown to $38.1 million for Q3 2022, with expectations of further acceleration in growth rates. Excerpted from the Incyte Q3 2022 earnings call ,

... Opzelura access continues to improve as NDC blocks are removed and payers continue to add Opzelura onto their formularies...Opzelura is now the number one prescribed agent for new AD patients amongst dermatologists with a new patient share of 17%. Opzelura is changing the treatment paradigm, helping to break the cycle of repeated failures on topical corticosteroids and calcineurin inhibitors. The number of dermatologists gaining experience with Opzelura continues to increase and 96% of prescribers are reporting satisfaction with Opzelura. Efficacy and rapid itch reduction continues to be a top driver for prescribing. And when it comes to selecting patients for therapy, dermatologists consider half of their AD patients as candidates for Opzelura. We expect the number of patient initiations per prescriber to continue to increase over time. Turning now to launch in vitiligo, where we are seeing positive early momentum, awareness levels are high with 9 out of 10 dermatologists aware of Opzelura as a treatment for vitiligo. Dermatologists view Opzelura, which is the first ever approved treatment for repigmentation as a transformative therapy for patients living with vitiligo. In a recent survey... dermatologist indicated their use of Opzelura in vitiligo, would more than triple in the next 6 months. Of their currently treated vitiligo patients, dermatologists considered nearly 70% could be candidates for treatment with Opzelura. For the 1.3 million diagnosed vitiligo patients who are currently not seeking treatment, we are launching several initiatives, including direct-to-consumer campaigns, patient advocacy group engagements, and branded patient meetings to raise awareness and encourage those patients to seek treatment now that there is a new approved therapy. Both AD and vitiligo are substantial opportunities and we expect Opzelura to become a meaningful growth driver over the next several years...

And on the same earning call, EVP and General Manager North America, Barry Flannelly in answer to questions on OPZELURA,

... there is about 150,000 to 200,000 patients that are actively being treated for vitiligo now. There may be 1.3 million or more patients that have vitiligo that may choose to come back to their dermatologists now that they have an active therapy that can help them there.... And as far as the guidance goes, we are confident that with the almost 30 million patients in the United States that have atopic dermatitis and the 5.5 million that are actively being treated now, that $1.5 billion guidance is certainly within our range – our possibilities.

Projecting The Financial Impact Of The Approaching Patent Cliff

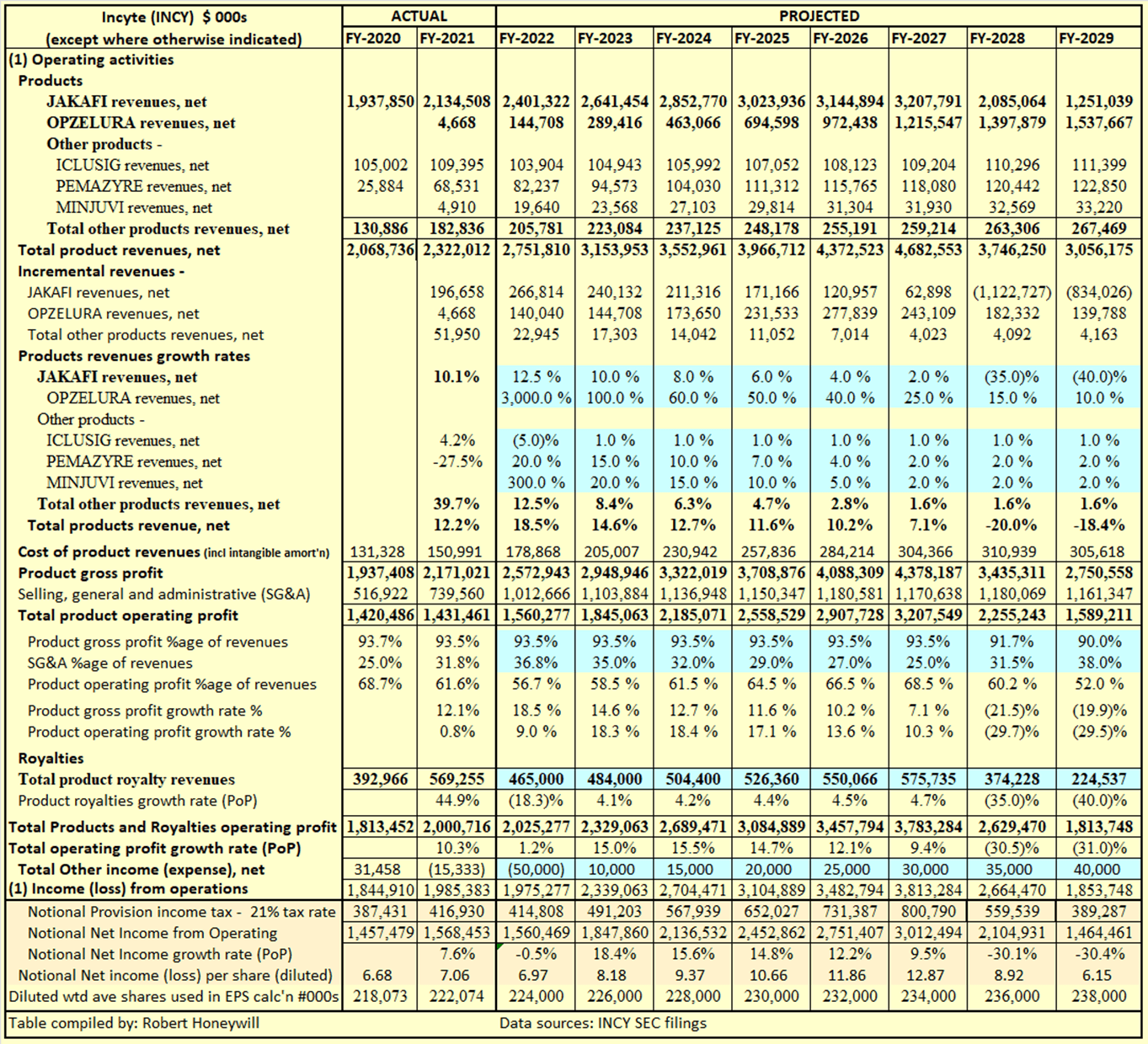

Table 3 below is not a forecast, it is merely a projection to quantify outcomes for revenues and earnings if the nominated assumed growth rates are achieved.

Table 3

{kind=link}

The drivers of the model in Table 3 are the data inputs/assumptions highlighted in blue. Comments follow -

- JAKAFI revenues are assumed to continue to grow, but at declining growth rates through end of 2027, before LOE in 2028 causes revenues to decline significantly.

- OPZELURA revenues are assumed to grow to achieve management's guidance of $1.5 billion revenue, and it is assumed this will not occur until FY-2029.

- Other products will continue to grow at modest rates off a low base, so do not contribute significantly to incremental revenue growth.

- Royalty revenues will continue to grow at mid-single digit rates with a significant decline commencing in FY-2028 due JAKAVI LOE.

- Total projected operating income before tax for 6 years FY-2023 to FY-2028 is $18.1 billion. This is over double the $8.0 billion for the 6 years FY-2016 to FY-2021 mentioned further above.

- If R&D spend continues at the ~$1.3 billion yearly average for 2016 to 2021, and continues to be funded out of operating income, a surplus of ~$10 billion would be available for additional R&D or for acquisitions. Share repurchases and dividends would also be possible, but there does not appear to be any intent of management to go down these paths.

- Notional EPS (excluding R&D expense) is likely to fall below FY-2022 levels in FY 2029.

The Major Missing Element In The Projections

The major missing element/assumption in the above projections is the degree of success, or otherwise, management might achieve from their present and future R&D expenditures and acquisitions. Excerpted from this 2020 article ,

The mean cost of developing a new drug has been the subject of debate, with recent estimates ranging from $314 million to $2.8 billion... the median capitalized research and development investment to bring a new drug to market was estimated at $985.3 million (95% CI, $683.6 million-$1228.9 million), and the mean investment was estimated at $1335.9 million (95% CI, $1042.5 million-$1637.5 million) in the base case analysis.

This 2021 article had even higher costs,

Estimates of total average capitalized pre-launch R&D costs varied widely, ranging from $161 million to $4.54 billion (2019 US$). Therapeutic area-specific estimates were highest for anticancer drugs (between $944 million and $4.54 billion).

And from this 2021 accenture article ,

Depending on the therapeutic area, treatment modality and disease complexity, the cost of bringing a new treatment to market is between $2.6B and $6.7B (including the cost of capital and cost of failure). The growing price pressures on the healthcare ecosystem mean that this cost must come down from billions to millions.

What these articles do not reveal is how much is recovered on average by way of net revenues from drugs that do receive approval and make it market. The studies that are available tend to focus on the very successful drugs. One only has to look at the various products Incyte has successfully brought to market to understand a number of them will never recover the average spend to bring to market based on the abovementioned studies. If Incyte could bring a further drug to market in the next six years with the revenue potential of JAKAFI or OPZELURA, that would completely change the above projections and the financial outlook for the company. The projected level of cash available for R&D spend is certainly sufficient to expect further successful drug approvals, based on average spend required to develop a successful drug. But no matter how much is spent, success is not guaranteed.

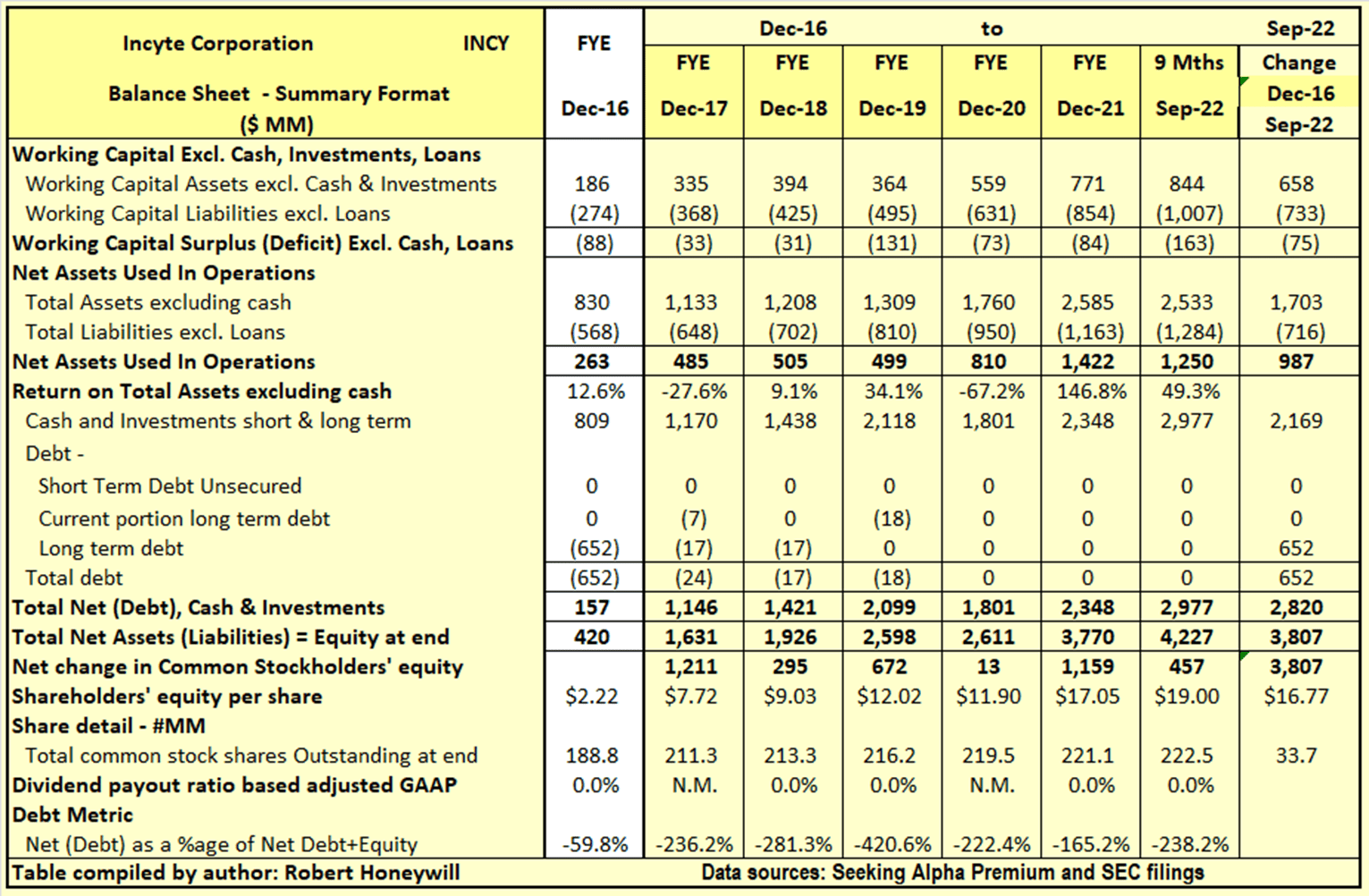

Checking Incyte's "Equity Bucket"

Table 4.1 Incyte Balance Sheet - Summary Format

{kind=link}

Table 4.1 shows, over the last 5.75 years, Incyte has increased net assets used in operations by $987 million and increased cash net of debt by $2,820 million. These increases were funded by $3,807 million in equity. Outstanding shares increased by 33.7 million from 188.8 million to 222.5 million, over the period. The $3,807 million increase in shareholders' equity over the last 5.75 years is analyzed in Table 4.2 below.

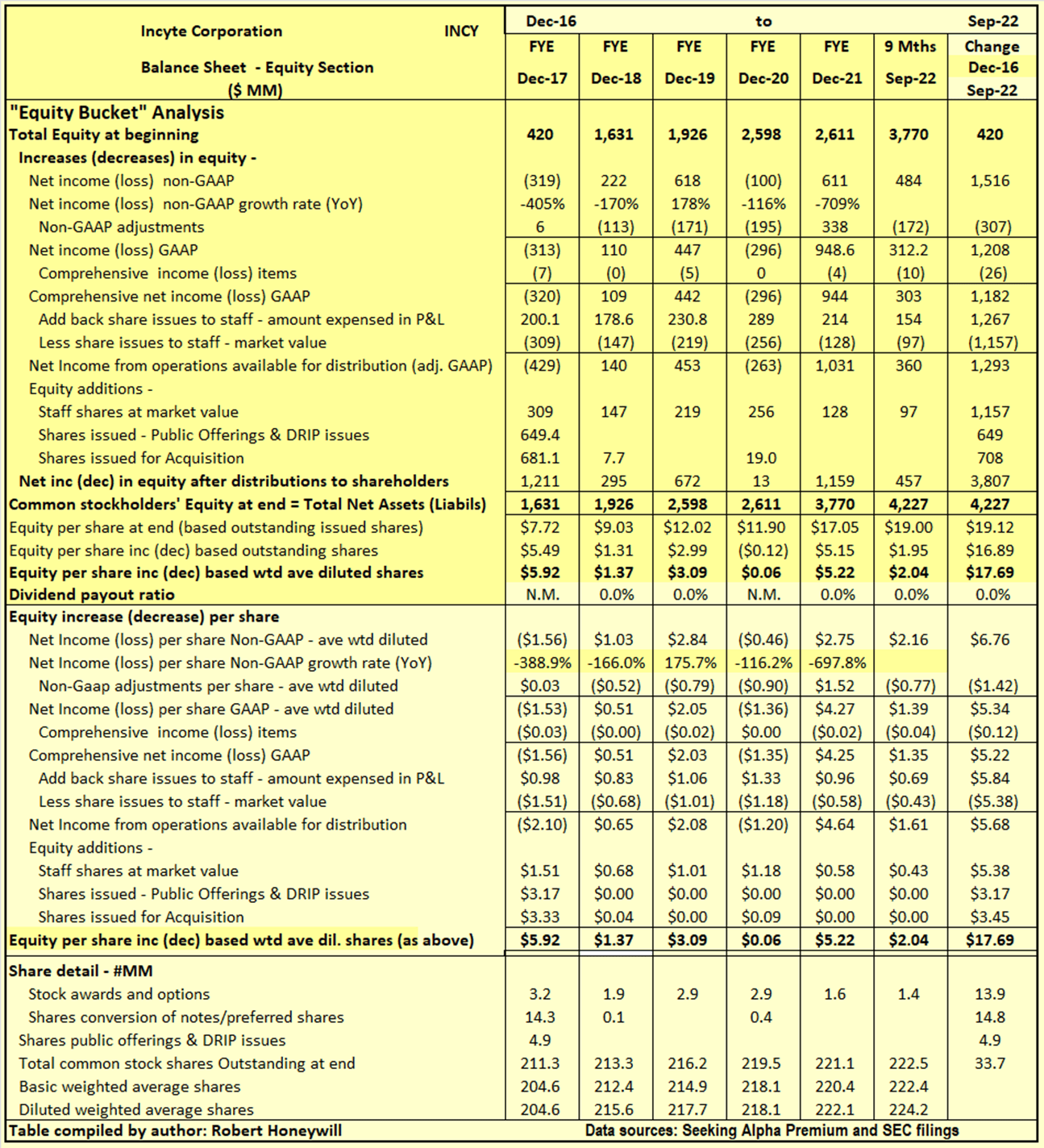

Table 4.2 Incyte Balance Sheet - Equity Section

{kind=link}

I often find with companies, while they produce earnings that increase shareholders' equity, significant amounts of distributions out of, or other reductions in equity, do not benefit shareholders. Hence, the term "leaky equity bucket." I find this is not of concern with Incyte, as explained below.

Explanatory comments on Table 4.2 for the period Jan. 1, 2017, to Sep. 30, 2022:

- Reported net income (non-GAAP) over the 5.75-year period totals to a profit of $1,516 million, equivalent to a diluted net income per share of $6.76.

- This non-GAAP net income is after substantial charges against income for research and development.

- The non-GAAP net income excludes $307 million of expense (EPS effect $1.42) regarded as unusual or of a non-recurring nature, in order to better show the underlying profitability.

- Other comprehensive income includes such things as foreign exchange translation adjustments in respect to buildings, plant, and other facilities located overseas and changes in valuation of assets in the pension fund - these are not passed through net income as they fluctuate without affecting operations and can easily reverse in a following period. Nevertheless, they do impact on the value of shareholders' equity at any point in time. For Incyte, these items were negative $(26) million and reduce EPS by $(0.12) over the 5.75-year period.

- The amounts recorded in the income statement and in shareholders' equity, for equity awards to staff, totaled $1,267 million ($5.84 EPS effect) over the 5.75-year period. The market value of these shares is estimated to be ~$110 million lower than the amount recorded for stock compensation expense purposes charged against net income over the 5.75-year period. This is not seen as a major negative, as very often the amounts charged by companies against net income is far below the actual cost, thus significantly overstating earnings. Compensating staff with shares conserves precious cash, and the $1,157 million value attributed to the shares issued is, in Incyte's case, a significant part of the $3,807 million increase in equity over the 5.75-year period.

- By the time we take the above-mentioned items into account, we find, over the 5.75-year period, the reported non-GAAP EPS of $6.76 ($1,516 million) has decreased to EPS of $5.68 ($1,293 million) from operations.

- There were no share repurchases by Incyte.

- There were 14.8 million shares issued for conversion of notes and another 4.9 million shares issued for other purposes in 2017. These issues, together with issues to staff, resulted in outstanding shares increasing by 33.7 million to 219.5 million shares, over the 5.75-year period, raising equity funds totaling $2,514 million. This $2,514 million plus the $1,293 million generated from operations gave rise to the $3,897 million increase in equity over the 5.75-year period.

- In the period under review, the company was in a net cash position throughout, with cash of $2,820 million and no debt at end of Sep. 2022.

Incyte: Summary and Conclusions

Incyte does not pay a dividend, so share price growth, and thus total return, is dependent on levels of earnings growth, which in turn is dependent in the longer term on success with R&D efforts. The projections included above indicate Incyte will generate operating earnings over the next six years greater than double earnings over the last six years. But, following JAKAFI LOE in 2028, underlying EPS will fall below FY-2022 level by 2029 unless further new drugs with significant revenue potential are successfully brought to market in the meantime. The prospects for that appear quite reasonable. Incyte has no debt and current cash balance of $2.8 billion. Based on projections above, a further ~$18.1 billion will be generated from operations before R&D spend over the next 6 years. These funds, together with existing cash, would allow R&D spending and acquisitions to increase to ~$3.5 billion per year over the next 6 years, compared to the $1.3 billion yearly expenditure over the last 6 years. While that does not guarantee success, based on industry success rate averages, several new drugs could be successfully developed and brought to market on the back of those levels of expenditure.

Incyte remains a Buy at current share price, and even more so should the share price fall back from current levels.

For further details see:

Incyte: Making Hay While The Sun Shines