INCY - Incyte: The Jakafi Company Branching Out - Baby Steps

2023-04-17 09:02:31 ET

Summary

- With billions in revenues and modest growth, Incyte has an elephantine problem.

- Incyte is building a three pronged stool of therapies to generate revenues outside Jakafi.

- Its financial position is fully supportive of its efforts to bolster Jakafi revenues with new therapies.

Incyte ( INCY ) is an interesting company that has prospered mightily during its relatively short existence on the back of a particularly successful therapy. In this article I review its prospects as its cash cow loses exclusivity in future years.

Making up a disproportionate share of Incyte's revenues, Jakafi's future is a big deal.

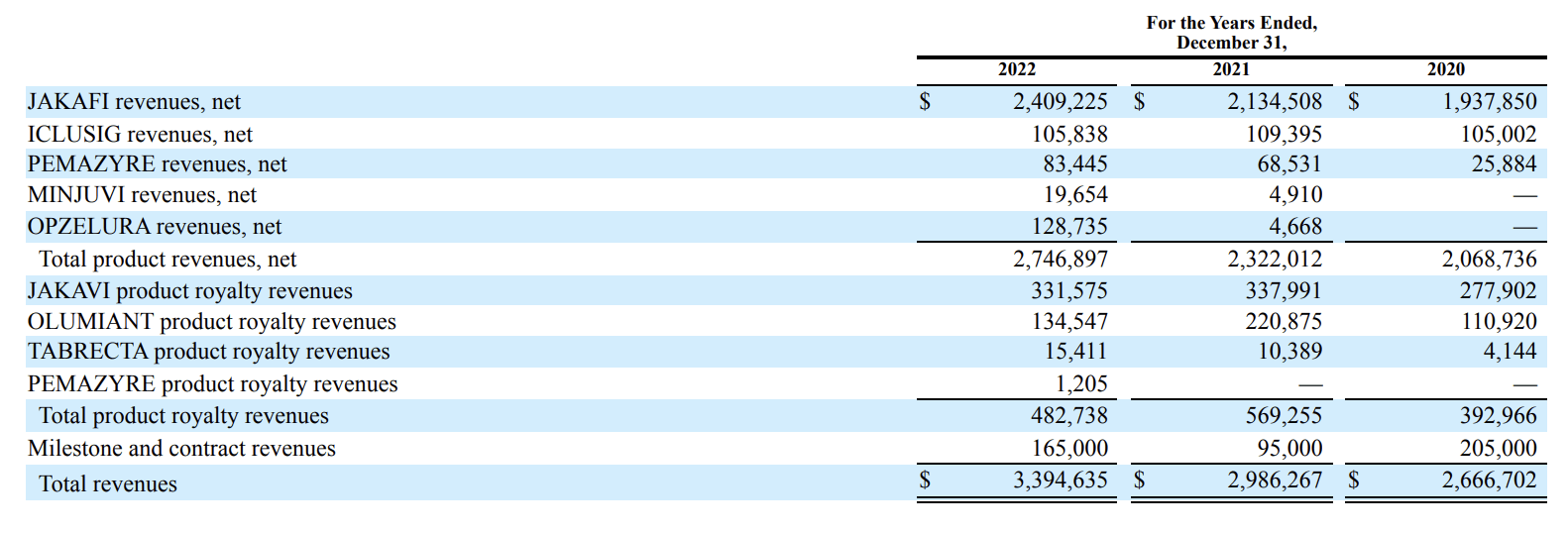

This is my first take on Incyte. With ~$3.4 billion in 2022 revenues from diverse sources its position seems solid. Take a quick peak at its disaggregated revenues for years 2020-2022 as shown by its 2022 10-K (the 10-K):

{kind=link}

Gulp...there is an elephant in the room. Incyte has a diversity of revenue sources. Five different products bringing in product revenues; four more bringing in product royalty revenues. With new ones developing nicely.

Unfortunately the diversity is populated by Lilliputians. Jakafi (ruxolitinib) is the Brobdingnagian in Incyte land. Aggregate product and product royalty revenues for 2022 were ~$3.228 billion, of which ~$2.740 billion or ~85% were Jakafi.

This is an improvement, albeit a slight one, over the 90% Jakafi constituted in 2020. This sets up a drama reminiscent, on a smaller scale, of Abbott's ( ABT ) epic 10+ year battle to control its disproportionate HUMIRA revenues.

The Abbott Humira drama, which is now being played out by Abbott spinoff AbbVie ( ABBV ) is all about patent expiration. Incyte's 03/2023 presentation (the " Presentation ") slide 10 lists Jakafi as having US expiry at end of 2028.

As I write in 04/2023 that gives Incyte >5.5 years to build up its revenues outside of Jakafi. Incyte's approved and near term candidate molecules appear to be up to the task. Another question intrudes. Up until 2029 when it loses exclusivity, can Jakafi itself maintain its nice product income growth trajectory?

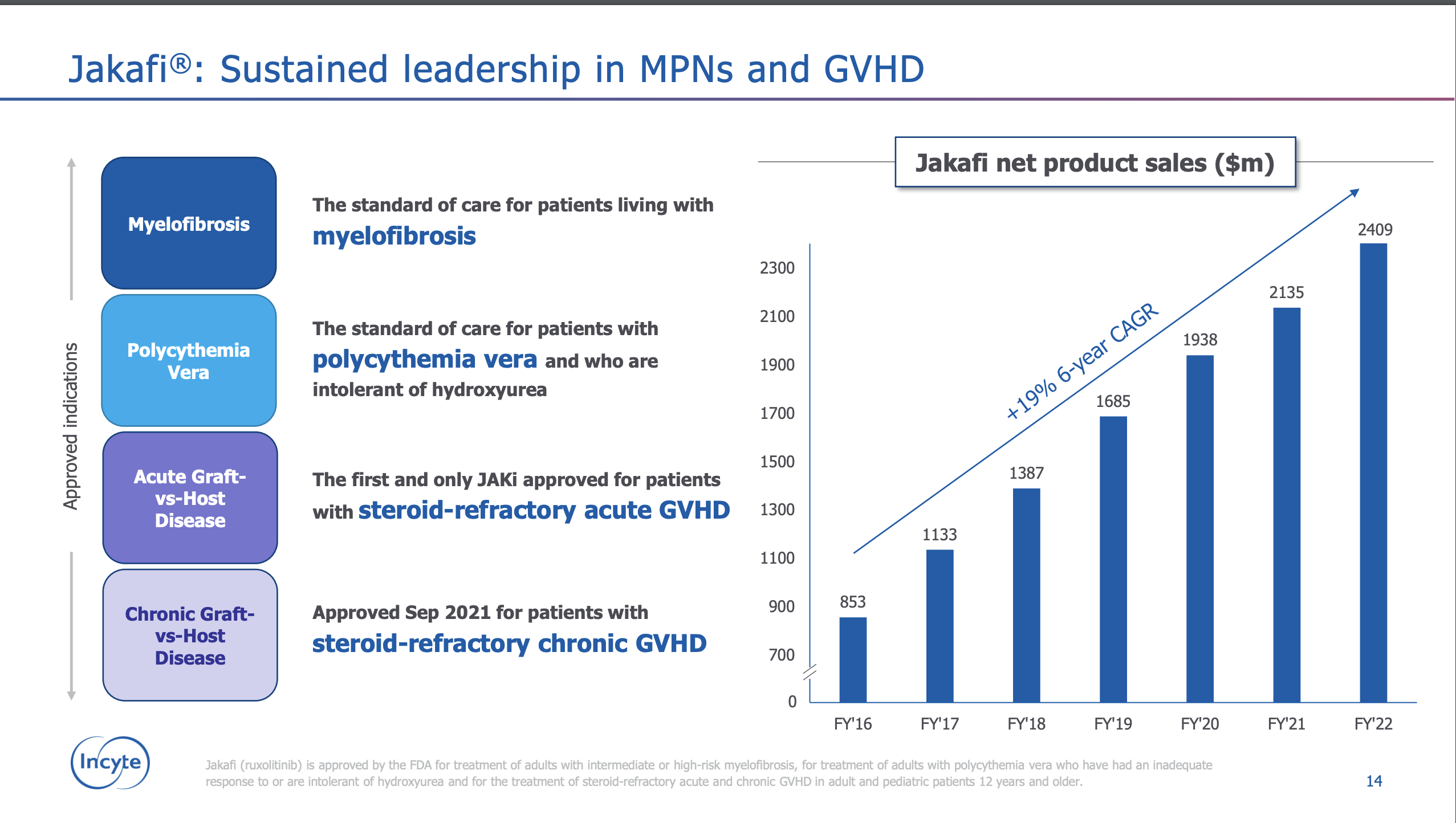

Presentation slide 14 below provides a helpful overview of Jakafi's steady progress over the years:

{kind=link}

It appears that Jakafi will soon have competition from big pharma player GlaxoSmithKline ( GSK ). Glaxo recently acquired Sierra Oncology for its myelofibrosis [MF] therapy momelotinib which has an upcoming 06/2023 PDUFA date.

Assuming as I do that Glaxo was correct in its expectation for momelotinib's approval, Jakafi may soon be facing some keen competition in MF.

Incyte is building a three pronged stool of therapies to grow its revenues outside Jakafi.

Overview

The Incyte story is an American success story. Started in 2002 in Wilmington Delaware by scientists formerly with DuPont ( DD ), it has grown mightily into a diversified pharma. As shown above it has sundry products generating product and product royalty revenues aggregating ~$3.4 billion.

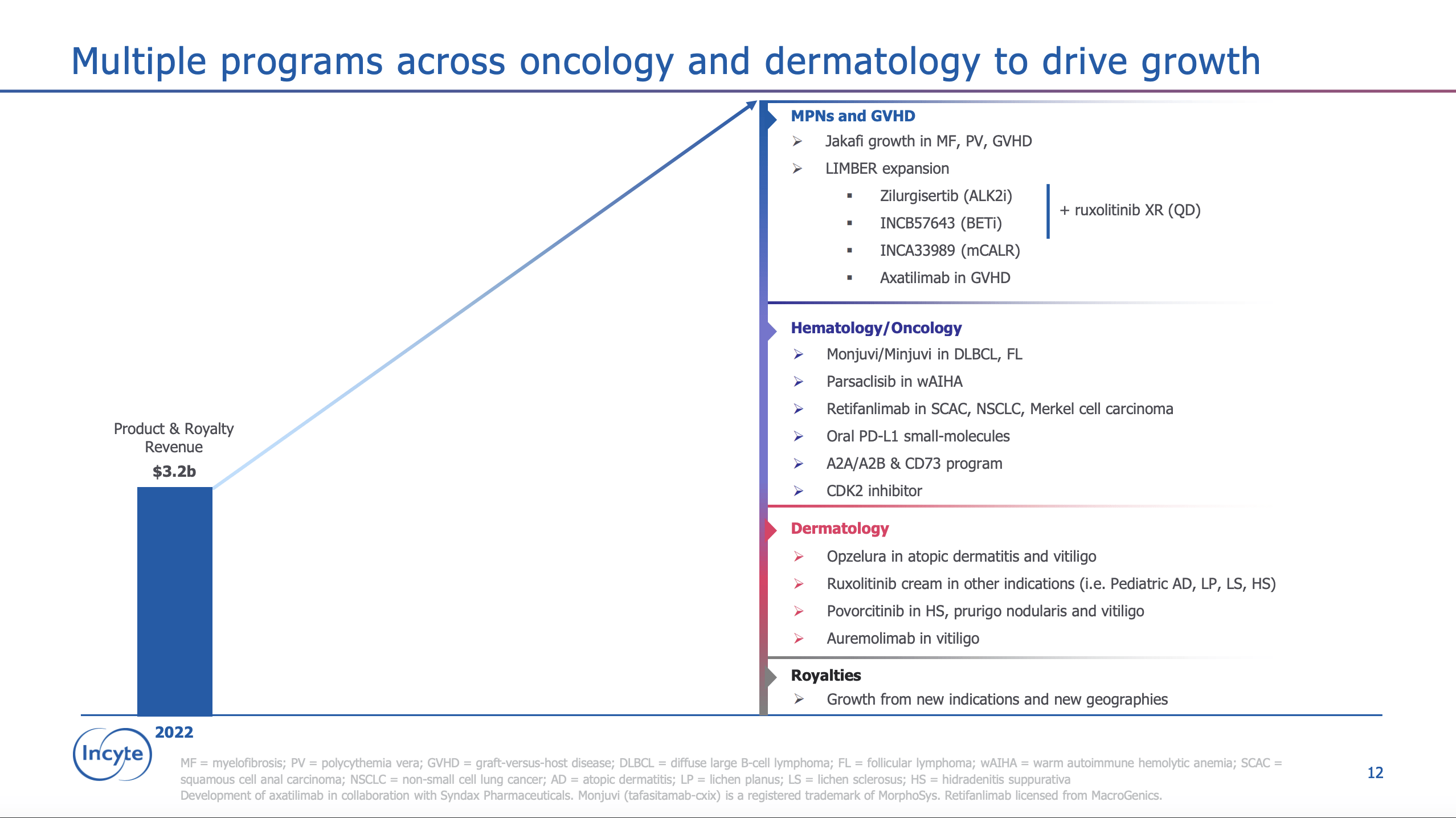

Despite its successes its over-reliance on Jakafi has held it back. Management is working to remedy this situation. Its Presentation slide 12 shows focus areas it is priming to do the job:

{kind=link}

Incyte acronyms

Following Incyte involves a heavy dose of acronyms. Refer to the list below for interpreting acronyms referred to in this article and its graphics:

AD = atopic dermatitis

DLBCL = diffuse large B-cell lymphoma

FL = follicular lymphoma

GVHD = graft-versus-host disease

HS = hidradenitis suppurativa

LIMBER = Leading in MPNs Beyond Ruxolitinib

LP = lichen planus

LS = lichen sclerosus

MF = myelofibrosis

MPN = myeloproliferative neoplasms

NSCLC = non-small cell lung cancer

PV = polycythemia vera

QD = daily dosing

SCAC = squamous cell anal carcinoma

wAIHA =warm autoimmune hemolytic anemia

XR = extended release

MPNs/GVHD

Incyte has a nice pipeline of therapies attacking these afflictions. Its nifty LIMBER acronym shows its recognition of the need to expand beyond Jakafi. Presentation slide 17 "LIMBER: Multiple opportunities to expand leadership in MPNs & GVHD" lists its broad LIMBER pipeline.

Of all the molecules shown only two are late stage. The FDA slapped down its QD ruxolitinib 03/2023 PDUFA with a CRL on 03/24/2023. That leaves only the combination therapy parsaclisib + ruxolitinib in a pair of phase 3 studies below as its sole remaining late stage LIMBER prospect:

-

LIMBER-304 trial ( NCT04551053 ) of 212 participants with MF who are suboptimal responders to ruxolitinib; data expected in H2,2023, but estimated study completion is 06/2025;

-

LIMBER-313 trial ( NCT04551066 ) study as a first-line MF therapy in 440 participants with estimated primary completion date in 11/2023 but estimated study completion date not until 05/2026.

Although late stage these are going to take a while to develop.

Hematology/Oncology

On Presentation slide 23 Incyte lists seven pivotal trials ongoing. In 03/2023 it hit pay-dirt with FDA approval of Zynyz (retifanlimab-dlwr), in treatment of adults with metastatic or recurrent locally advanced Merkel cell carcinoma (MCC).

Despite its success with Zynyz and its heavy load of pivotal trials, Hematology/Oncology is Incyte's Red-headed stepchild. It gets no respect. Despite its then imminent FDA approval, Zynyz got no mentions in the Call. Indeed there was precious little discussion during the Call of any upcoming prospects in this area.

Dermatology

Incyte's dermatology portfolio is very much a high potential situation. Strangely Incyte's old standby ruxolitinib plays another key role here. Ruxolitinib reformulated as a 1.5%cream and renamed Opzelura is now approved by the FDA in treatment of vitiligo and adults with AD.

Later in 2023 it will report data on its pivotal trial for treatment of ages >2 and <12. Recently Opzelura has generated positive vitiligo news flow including from CHMP and positive phase 3 vitiligo maintenance data.

Approved for adults with AD in 09/2021, 2022 — Opzelura's first full year on the market netted ~$128.7 million in revenues. With additional revenues from its 07/2022 approval in treatment of vitiligo, Opzelura tallied Q4, 2022 net revenues of $61 million.

It is still too early to see how Opzelura will fare in its first full year with combined revenues from AD and vitiligo. Its patent protection gives it ample room for development not expiring until 2040 as reflected by Presentation slide 28.

Incyte's expenses are growing on par with its revenues as it works to build Jakafi support.

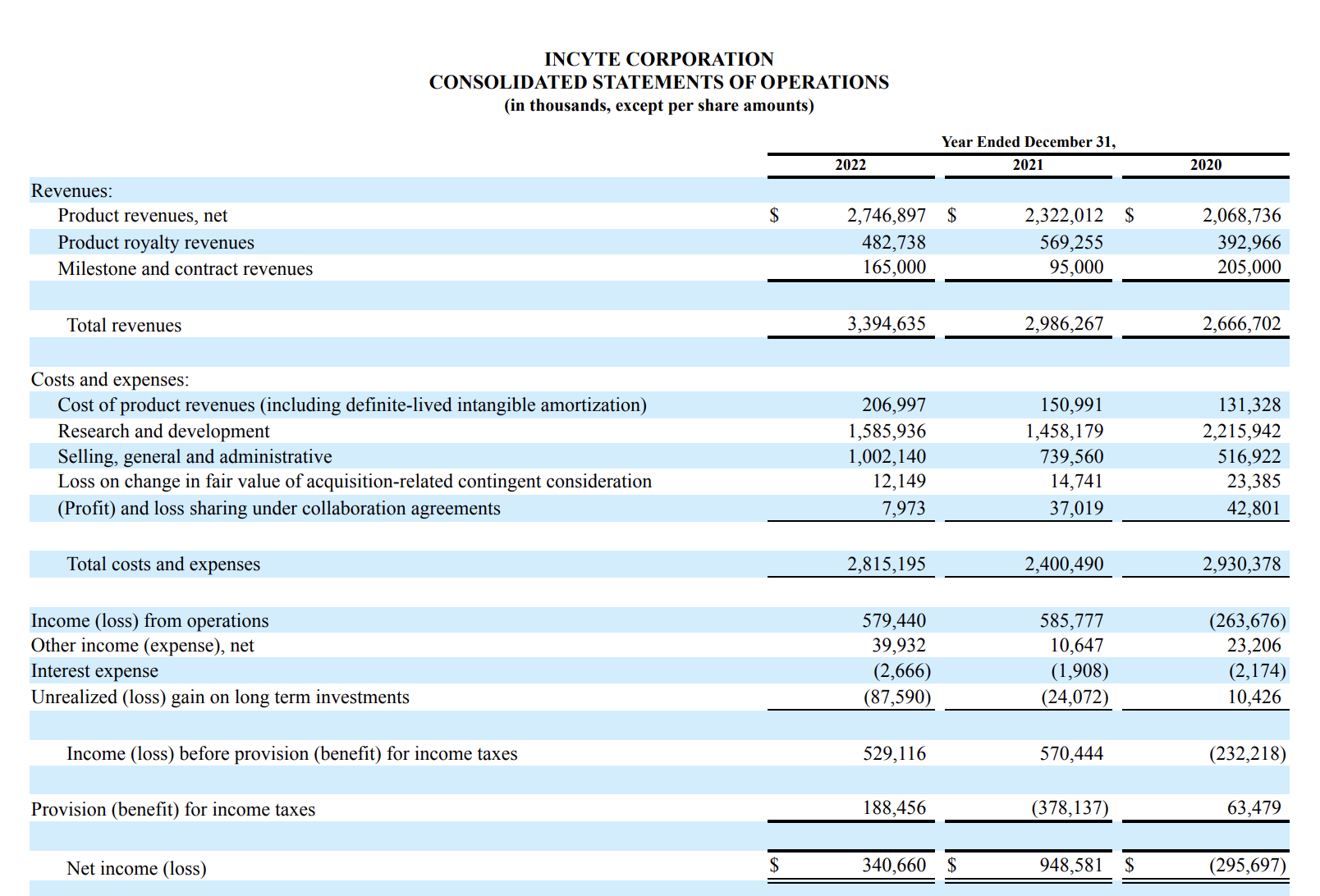

Incyte's Q4 2022 statement of operations points to a so-so dynamic of revenues rising in line with expenses:

{kind=link}

Incyte's 2022 revenues and expense rose over 2021's by ~400 million leaving its year/year income roughly at par. Income tax provisions explain the major difference in net income between the years.

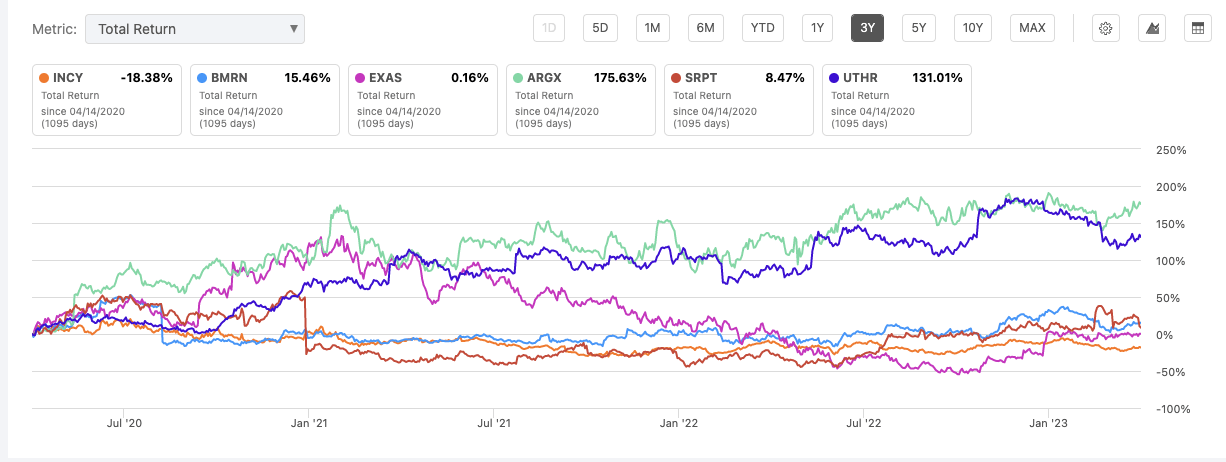

All very respectable but highly uninspiring. In terms of total return it is lagging right at the bottom of its Seeking Alpha peers:

{kind=link}

Incyte maintains comfortable liquidity of $3.238 billion at the close of 2022.

Conclusion

Incyte has its supporters, Seeking Alpha's summary ratings panel sets it as "Buy" across the board. I am passing on this one. I note that Wall Street Analysts have an average price target of $ 88.39 ( +18.64% Upside).

All told I consider Incyte an interesting stock, but not one I would consider buying at its current $16.61 billion market cap.

For further details see:

Incyte: The Jakafi Company Branching Out - Baby Steps