INDT - INDUS Realty: $65 Offer Is Too Low

Summary

- On November 28, INDUS Realty received a non-binding acquisition proposal from Centerbridge and GIC for $65 per share in cash.

- At $65 per share, the proposal works out to an implied cap rate of 5.6% on expected 2023 NOI.

- While higher interest rates and minimal near-term lease expiries likely put a lid on the price a buyer can pay, I think $65 is too low.

- A bid of $70-75 would equate to a 5-5.3% cap rate which appears reasonable in the current market environment.

On November 28, INDUS Realty ( INDT ) received a non-binding acquisition proposal from Centerbridge (which owns just under 15% of INDT shares outstanding) and GIC for $65 per share in cash. While this offer is 13% above where INDUS traded the day before the proposal, it is 21% below INDUS stock's 52 week high. Like most industrial REITs, INDT has seen its share price decline in 2022 as higher interest rates and softening demand (albeit from record levels) have reduced public and private valuations throughout the sector.

While an increasing cost of capital, softening demand and a relatively high overhead expense burden (discussed below) argue for a transaction, $65 is too low a price in my opinion. I think a $70-75/share price would represent a win-win transaction.

Overview

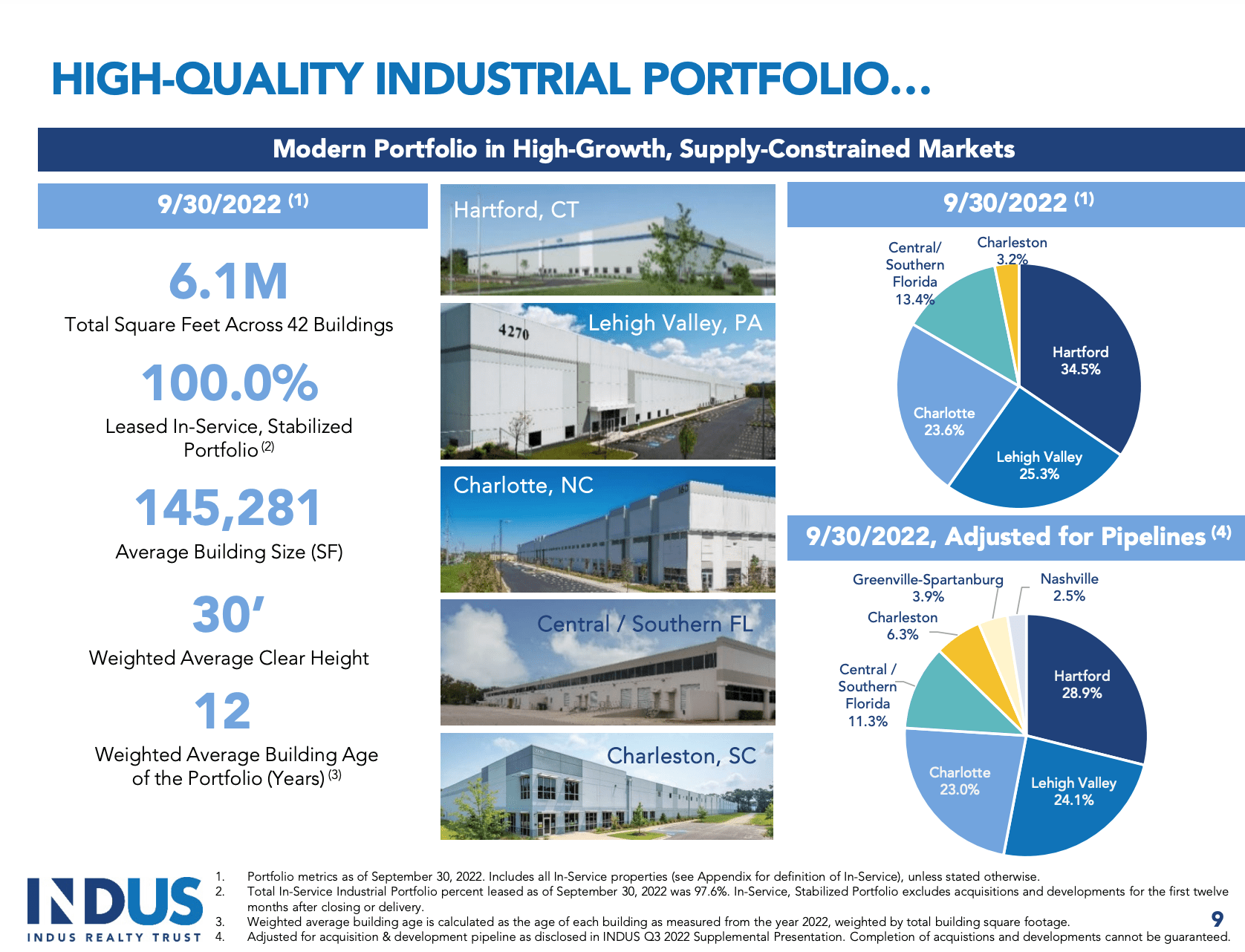

INDUS (formerly Griffin Industrial Real Estate) is an industrial REIT which owns a relatively young portfolio (12 year average age) of 42 industrial/logistics buildings aggregating approximately 6.1 million square feet in the Eastern United States. Over the past five years the company has divested excess land holdings and deployed the proceeds into the acquisition and development of industrial real estate.

Overview (Investor Presentation)

{kind=link}

Valuation

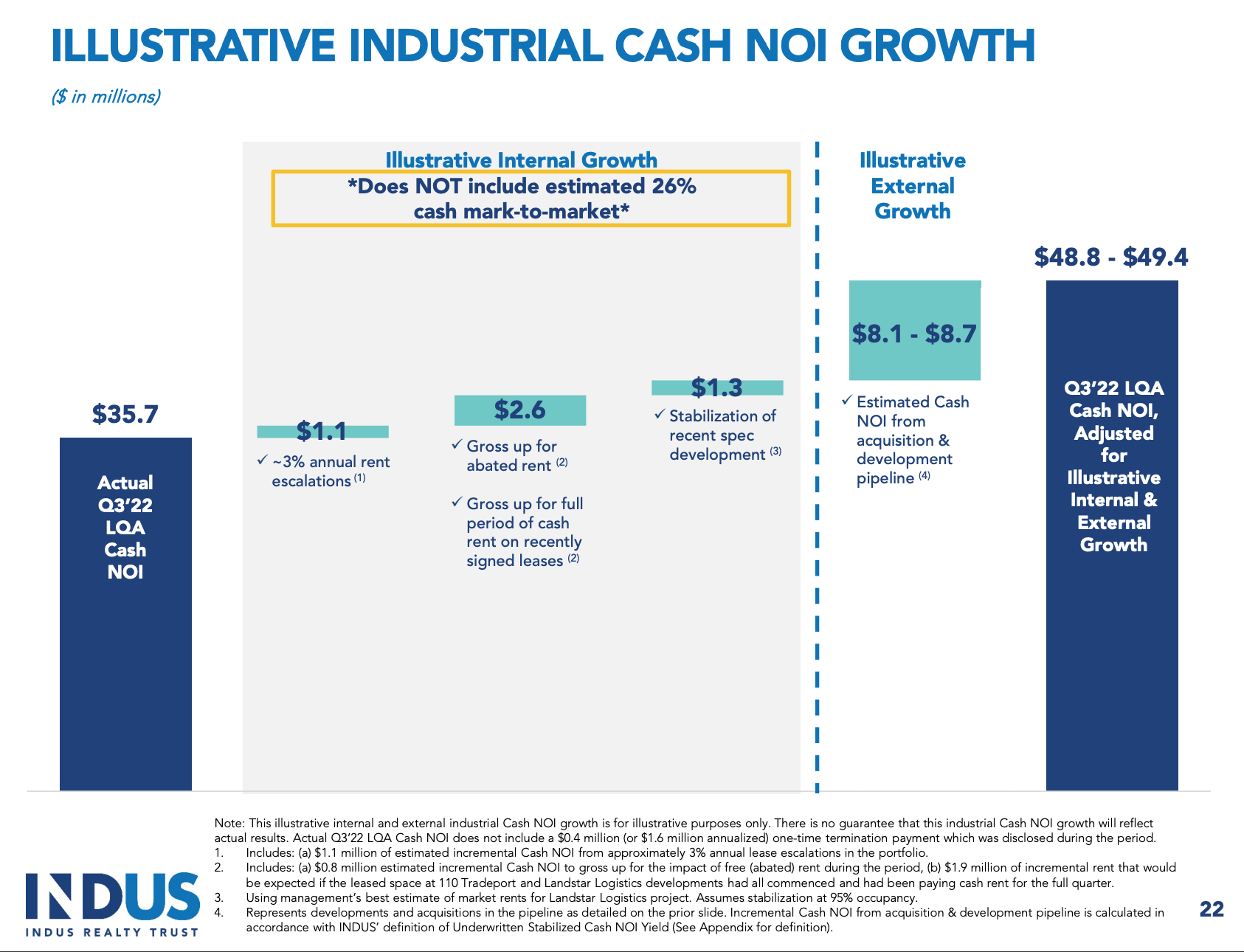

Cash NOI (Investor Presentation)

{kind=link}

As shown below, after adjusting for developments in progress, pending property acquisitions, and 2023 expected rent growth the $65 bid equates to an implied cap rate of 5.6%. On the one hand, the 2023 implied cap rate of 5.6% is above recent property purchases agreed to by INDUS (higher cap rate means valuation is lower than prices recently paid by INDUS). Similarly, earlier this year industrial real estate in INDUS's markets was changing hands in the 4-4.5% range (would imply a valuation close to $90 per share).

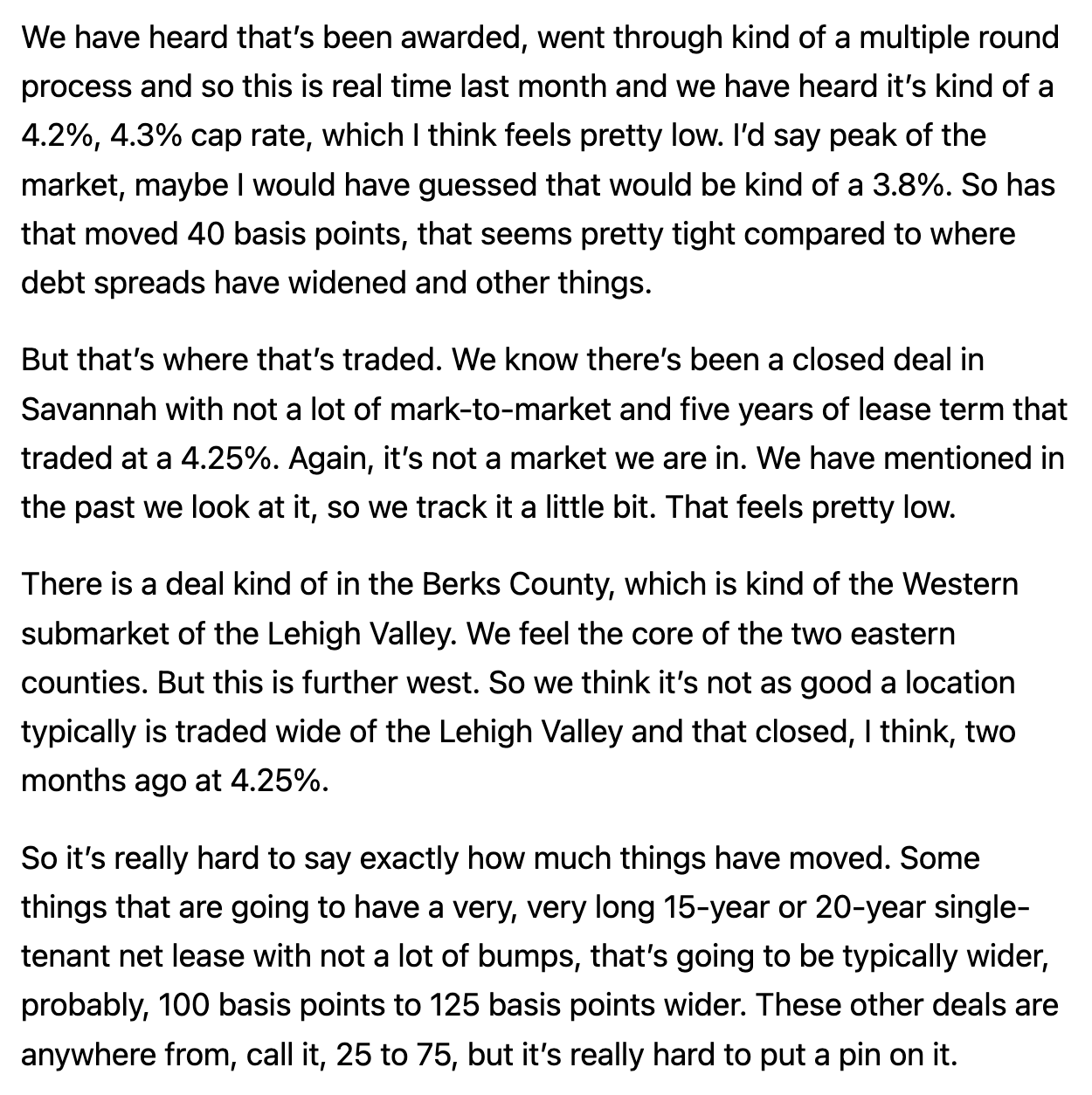

On the other hand, the transaction market for industrial real estate has slowed throughout 2022 and valuations have likely decreased. Here is recent management commentary on cap rates:

Cap Rate commentary (INDUS 3Q22 conf call transcript from Seeking Alpha) INDUS valuation at $65 per share (Company Filings; Author Estimates)

{kind=link}

{kind=link}

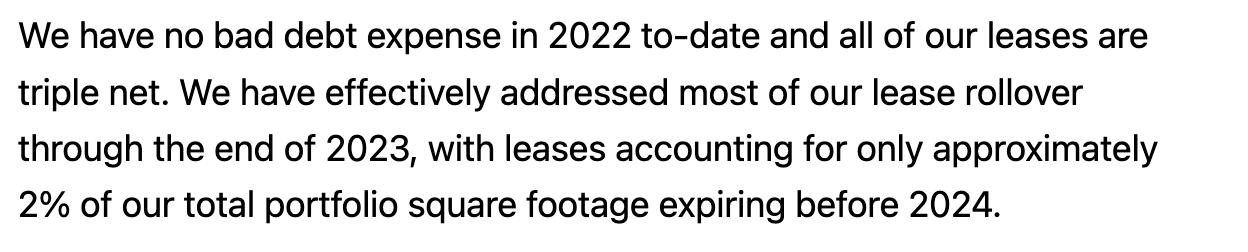

While INDUS believes that rents in its portfolio are ~26% below current market rent (shown in the 'Cash NOI' slide above), near term expiries are limited:

Near-term Lease Expiry commentary (INDUS 3Q22 conference call transcript from Seeking Alpha)

{kind=link}

Limited near-term expiries mean that it will take several years for this rental growth to materialize. Further, as industrial real estate market conditions are subject to change, it is possible that rent growth could soften and NOI growth will not come to fruition. That said, even if leasing market conditions soften, INDUS's portfolio should see mark to market rent increases over the next five years.

$65 seems too low. I think a bump (or a competing bid) would be necessary to get a deal done. A bid of $70-75 would work out to a 5-5.3% cap rate which I think is more reasonable. This basically assumes that cap rates have widened ~100 basis points from what where we saw deals trading earlier this year.

Why INDUS shareholders may be amenable to a deal

While $65 seems to be a low-ball bid, there are several reasons INDUS should explore a going private transaction:

- Prior to the announcement of the bid, INDUS was trading in the mid/high 50s which is an implied cap rate over 6%. While the transaction market has stalled and valuations for industrial property have declined, it is unlikely that INDUS can acquire properties much above 6% making it difficult to grow NAV per share. Similarly the cost of debt financing has increased with interest rates.

- Other potential suitors like Blackstone ( BX ) which has been a voracious acquirer of industrial real estate over the past several years may be losing their appetite to undertake more acquisitions as fund flows turn negative .

- As mentioned above, INDUS has relatively few leases expiring over the next 12-18 months, limiting near-term rent growth.

- As a small REIT (sub $50 million in NOI) INDUS has high G&A expenses relative to NOI. G&A represents ~25% of NOI which is considerably higher than larger peers like Prologis ( PLD ) or Terreno ( TRNO ) which have G&A burdens below 15%. This means that as a standalone company, INDUS will generate less FFO/share per dollar of NOI.

Conclusion

$65 seems an opportunistic bid (opening offer) by Centerbridge/GIC given a difficult financing environment and slowdown in buyer activity. Ultimately I think the price will have to be raised to a minimum of $70 to get board/shareholder approval.

For further details see:

INDUS Realty: $65 Offer Is Too Low