ILPT - Industrial Logistics Properties Trust: Maturities Are Looming Over Its Fate

2023-07-24 11:24:13 ET

Summary

- Industrial Logistics Properties Trust, a REIT focusing on industrial properties, is facing financial difficulties due to high debt load and interest burden from its acquisition of Monmouth Real Estate Investment Corporation.

- The company's interest rate caps, acquired through swaps agreement, are set to expire in March 2024, potentially leaving over $2.6 billion of debt at higher rates and impacting profitability.

- The future of ILPT is uncertain, with potential outcomes ranging from bankruptcy to a 40% increase in share value, depending on the pricing of new interest rate caps and other factors.

Introduction and thesis

Industrial Logistics Properties Trust ( ILPT ) is an externally managed REIT that focuses on industrial properties, with a particular focus on logistics. Thus, they acquire and manage facilities such as warehouses and other key infrastructure.

The company is highly leveraged, and they recently cut all their dividends and started a going concern process, under which they are trying to preserve as much cash as they can. This is because there are important maturities coming up in less than 9 months that we are going to discuss in this article, and the company needs to be prepared for every scenario. We believe that this company has a high-quality portfolio of industrial properties, however, the high debt load and interest burden make it an extremely risky investment. We would like to see how the upcoming maturities of swaps and debt are managed, and how the macro and rates environment will position itself in the medium run to eventually take a position. That said, the peculiarities of the RE assets that ILPT was able to acquire position it as one of the key players in the logistics and e-commerce-related markets, which could fuel long-term organic growth.

The rise and fall of ILPT

ILPT has been a successful REIT for many years, managing high-quality logistic assets that are the key to e-commerce expansion. Indeed, in the last years, they were able to grow revenues consistently thanks to demand coming from e-commerce.

But then everything changed with a single deal in 2022: the Monmouth Real Estate Investment Corporation acquisition. ILPT management decided to bet big into this growing segment that was fueled by big players such as Amazon (AMZN) and FedEx (FDX) to expand their facilities and RE footprint. Thus, they acquired MNR for $21 per share, in an all-cash deal valued at $4 billion. But as is often the case with REITs, the company did not have much cash to finance the acquisition (less than $100 million on hand) and had to fund it with debt - effectively an LBO.

At the time of the agreement, in November 2021, there wasn’t much of an issue in raising $4 billion of debt at sub-5% interest rate (the cap rate of the acquired portfolio). However, the deal effectively closed only in 2022 as the FED was starting its rates hiking process that eventually drove interest to today’s 5.25%, and ILPT immediately found itself in a dilemma. Eventually, they were able to find temporary financing under a bridge loan, which was repaid in October 2022. The definitive non-temporary financing didn’t come as easily though, and not cheaply too. Right now, the company has the current debt outstanding:

ILPT Debt Maturities (Latest 10-Q)

The two highlighted floating rate facilities were signed to finance the deal, and they bear interest above 6%, meaning they are financing the MNR portfolio with debt more expensive than the cap rate itself at the time of the closing of the deal. However, the two debt deals are actually bearing an interest of SOFR + 3.93% for the $1.2 billion loan, and SOFR + 2.77%. But the company bought caps through swaps that allow for the actual rate to be “only” around 6%. But these caps are coming very close to maturity, and this may create some serious issues. See below.

The interest rates caps and the debt maturities

As one can immediately notice in the debt table, the maturities are not that bad, with the closest one being in October 2024, but that allows for extension options for up to three years of additional life. This looks quite convenient as ILPT will be able to opt for an extension of these deals if they are not able to find cheaper alternatives, at the same terms.

The problem is the interest rate caps, which the company acquired through swaps agreement that they signed after incurring in this new debt.

Interest Rate Caps (Latest 10-K)

{kind=link}

This is a summary of such products. As noticed, they are fixing SOFR well below its current level of around 5.2%, to a more sustainable level between 2% and 3%. But these contracts expire in March 2024, and thus ILPT’s shield against 5% rates will disappear, leaving more than $2.6 billion of debt at rates around 2% higher.

This will translate into an additional interest expense of around $52 million per year, which represents almost 50% of their current cash and would tremendously impact profitability.

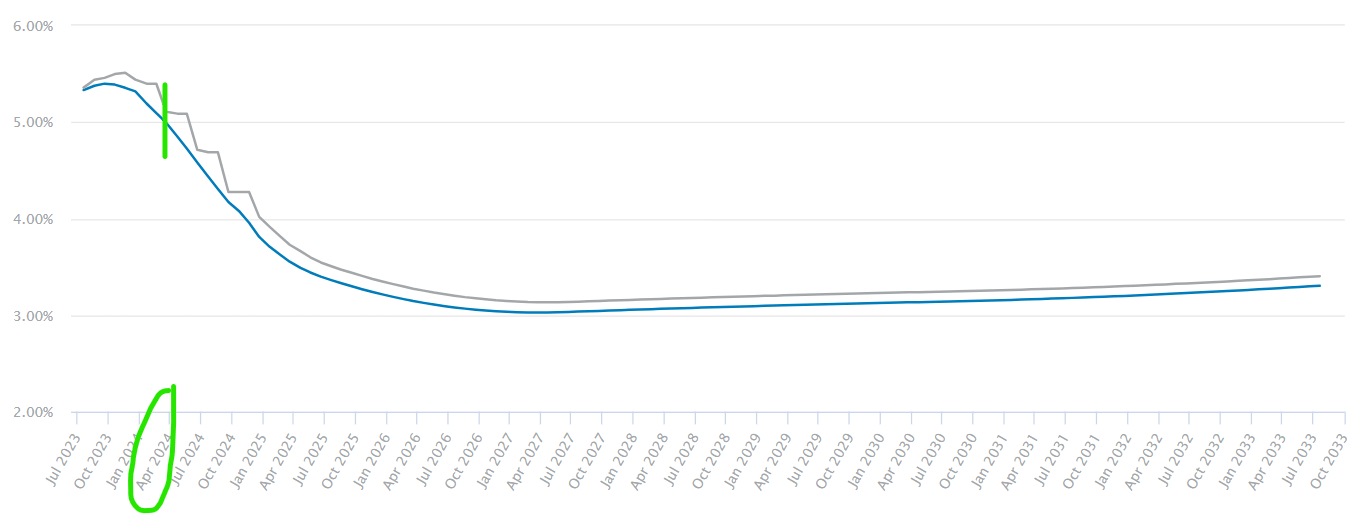

Forward Swap SOFR curve (Chatam Financial)

{kind=link}

And this is what the forward SOFR curve looks like for a 3 months swap. In March 2024 it is expected close to 5%. If ILPT was to go out today looking for pricing its caps, it would be forced to close any deal at very high rates.

Valuation

To properly present a valuation framework for ILPT equity is challenging, as there is very little earnings and cash flows visibility after March 2024 as we do not know the pricing of the new interest rate caps. This could result in materially higher cash interest expense that could wipe out the accumulated cash position as FCF will turn negative. We can try to assess the fair value using two different scenarios: one in which pricing for the caps is at the current FED rates, and one more optimistic view where the caps are priced at around the same level as of today's. This last scenario could represent the case where the FED starts cutting the rates in the 2H 2023, or ILPT is able to get very favorable pricing also based on developments of the swap curve.

1) Under the first scenario, the consequences on the equity would be likely catastrophic. In our own estimates, we see FCF going from $8 million to a loss of $44 million per year (assuming $52 million of additional interest), and with no visibility in future cash flows, we have to continue to estimate such a negative number throughout the maturities of the debt (3 years with the extensions). After discounting the values, we derive a fair value per share that is negative, meaning that ILPT would have to declare bankruptcy.

2) Under the more favorable scenario, the interest would be again between 2.5% and 3.5%, close to today's caps. This means also that FCF would be the same if not more positive, as rent roll-ups may improve the top-line. This means that the present value of such cash flows would be around $370 million equity value, or $5.70 per share, representing an upside of more than 40% from the current price.

It looks like the outcome for ILPT would be almost binary, either zero or X, under our own assumptions. This is probably reflected in today's market cap and more than a 90% drop from its average price of the last years of trading. The market, like us, is cautious about the valuation as these maturities loom on their balance sheet and cash generation capabilities.

Conclusion

Industrial Logistics Properties Trust has many high-quality assets in its portfolio, which are vital for e-commerce and many other activities. The quality of their tenants and their occupancy ratio confirm this. However, the company is facing an existential maturity of its interest caps in March 2024 which could make it or break it. We remain very cautious and monitor the situation of the SOFR curve to spot any buying opportunity.

For further details see:

Industrial Logistics Properties Trust: Maturities Are Looming Over Its Fate