REIT - Industrial REITs: Shortages Become Gluts

Summary

- Pressured by global recession concerns, Industrial REITs dipped by 30% in 2022 - the sector's worst year on record- snapping a seven-year streak of outperformance over the broader REIT Index.

- The frenzied investment in logistics space clashed with already-tight supply, fueling an incredible surge in rent growth across logistics and warehouse properties. Market rents have soared 50% since early 2021.

- Global supply chains have rapidly normalized following historic pandemic-era disruptions. Consistent with its "boom-bust" history, global shipping rates have plunged 80% from recent inflation-fueling peaks to below ten-year averages.

- Industrial REITs aren't entirely immune from post-pandemic demand normalization, but supply remained inherently capped by land constraints. Rent growth will naturally moderate toward "trend" levels, but fundamentals are forecast to remain healthy absent a demand shock.

- We doubled-down on the sector amid the extreme weakness last year, but discounts have narrowed following a rally from stellar earnings results and retreating interest rates, so selectivity has become critical.

REIT Rankings: Industrial

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on January 17th.

{kind=link}

Hoya Capital

A perennial performance leader in recent years, Industrial REITs were slammed in 2022 - snapping a seven-year streak of outperformance over the broader REIT index - despite delivering a record year of operating performance as demand for well-located logistics space substantially outstripped supply. Despite economic challenges, the industrial property market is expected to remain strong in the near term, as e-commerce and logistics companies continue to drive demand for well-located warehouse and distribution space. Within the Hoya Capital Industrial REIT Index , we track the eleven industrial REITs which total roughly $155 billion in market value.

{kind=link}

Hoya Capital

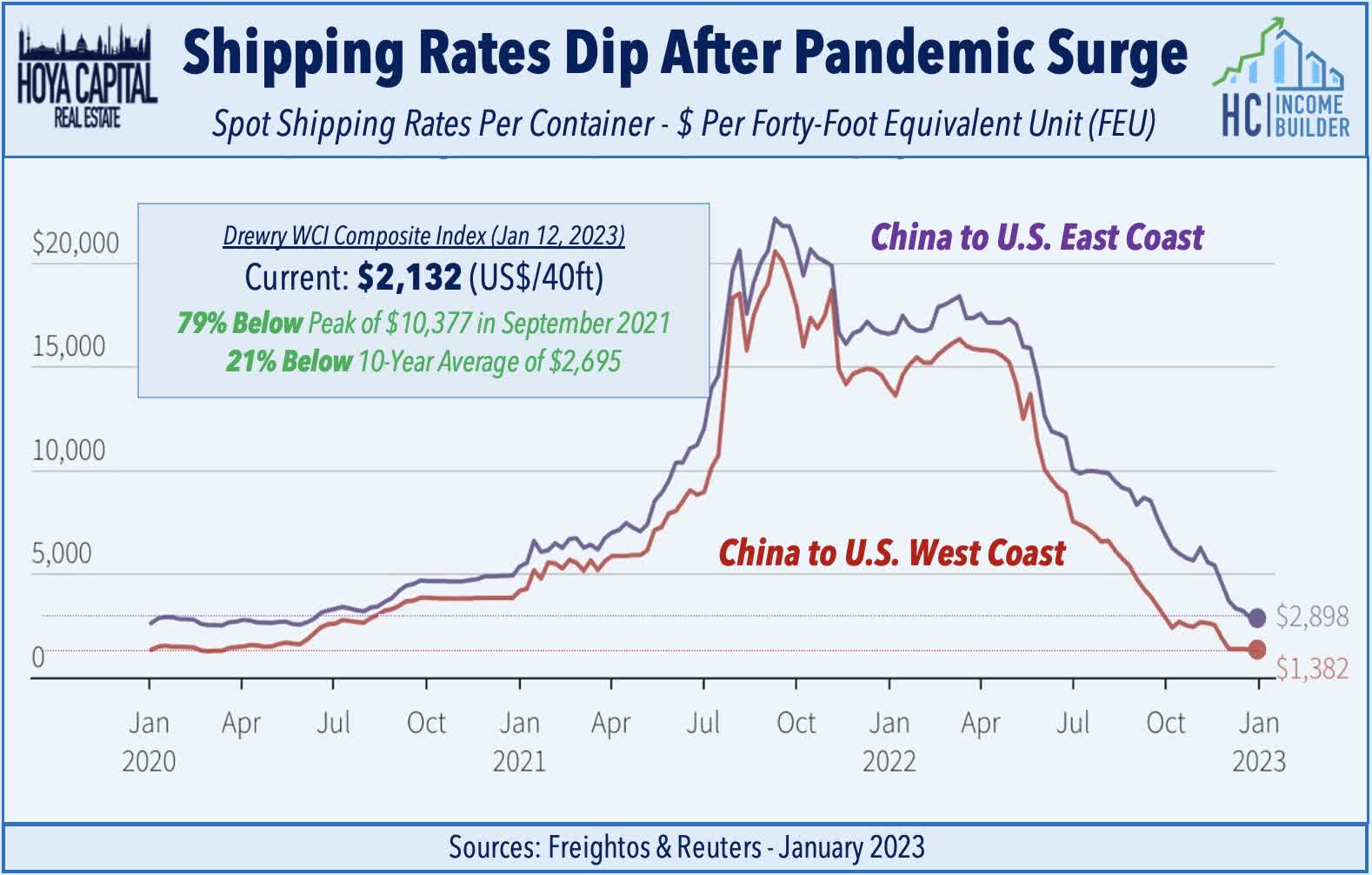

Storm clouds have gathered over the global economy in recent months as historic levels of inflation, synchronous central bank tightening, and moderating fiscal spending have combined to rapidly normalize aggregate demand following a COVID-era surge. Industrial REIT valuations have been pressured by concerns that the "boom-bust" dynamics currently on display across other supply-chain-oriented segments will bleed into the logistics property sector. Global Shipping Rates - as measured by the Drewry WCI Composite Index - have now plunged 80% from recent inflation-fueling peaks of over $10,000 per forty-foot equivalent unit ("FEU") in September 2021 to around $2,000 per FEU in January 2023 - below its 10-year average. The Cass Freight Index - which measures shipping volumes - was down 3.9% in December from the prior year, a second-straight month of declines.

{kind=link}

Hoya Capital

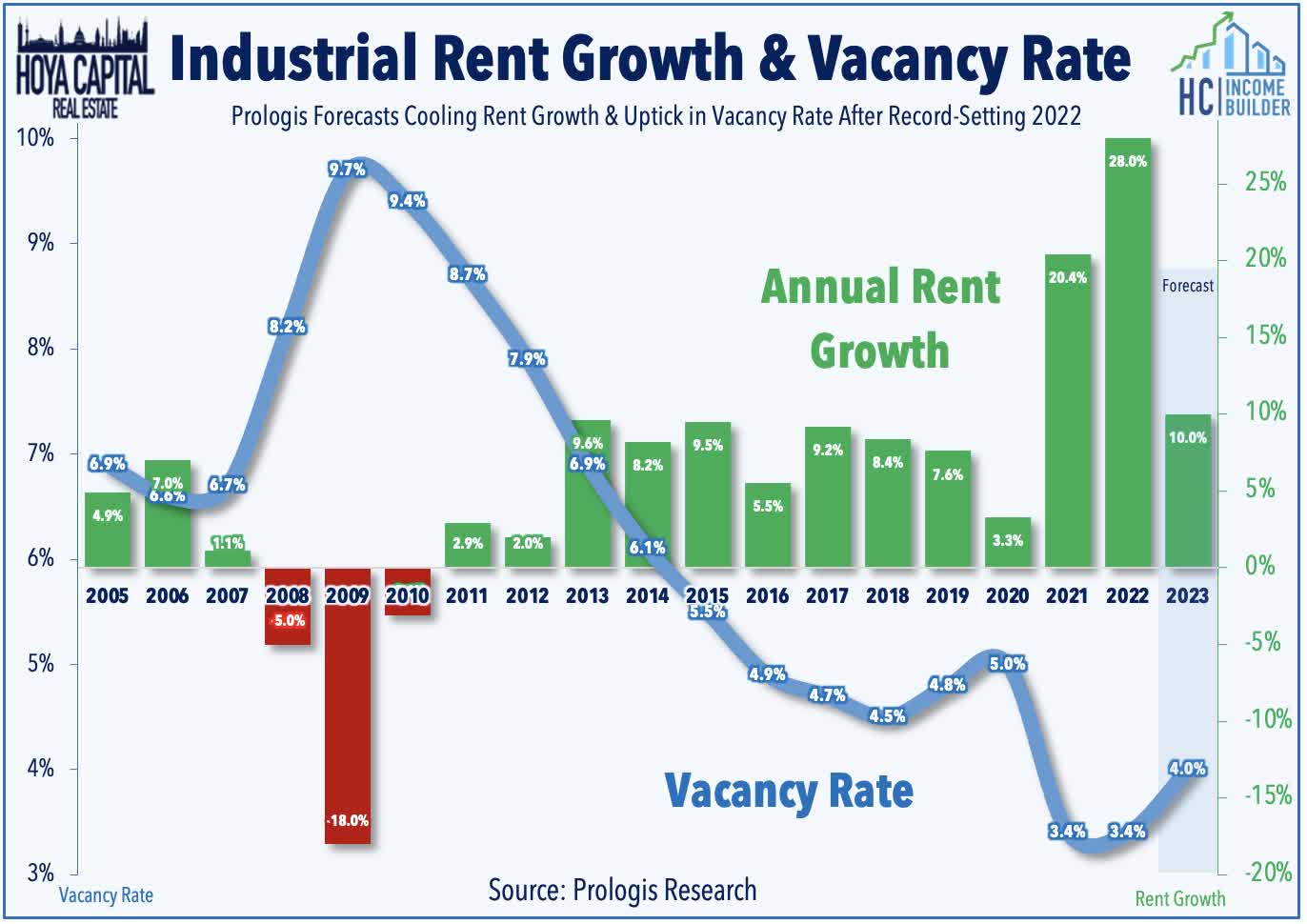

Industrial REITs aren't entirely immune from these boom-bust supply chain dynamics, but due to the inherent supply constraints from limited land availability, property-level fundamentals are nevertheless forecast to remain healthy absent a more pronounced demand shock. Brokerage firms CBRE ( CBRE ) and JLL ( JLL ) each reported last month that industrial vacancy rates remained near record-lows at around 3% in late 2022 even as the early effects of the global economic cooldown become more visible. CBRE noted that "companies continued to expand their warehouse footprint given strong e-commerce sales, supply chain diversification, inventory control, and population shifts" and forecasts that "continued strong demand from large occupiers is expected to keep supply and demand in balance." Separately, JLL noted that "despite a loss of momentum in the macroeconomic environment, industrial market fundamentals remained sound" with year-over-year rent growth exceeding 25% in 2022, consistent with recent reports from Prologis.

{kind=link}

Hoya Capital

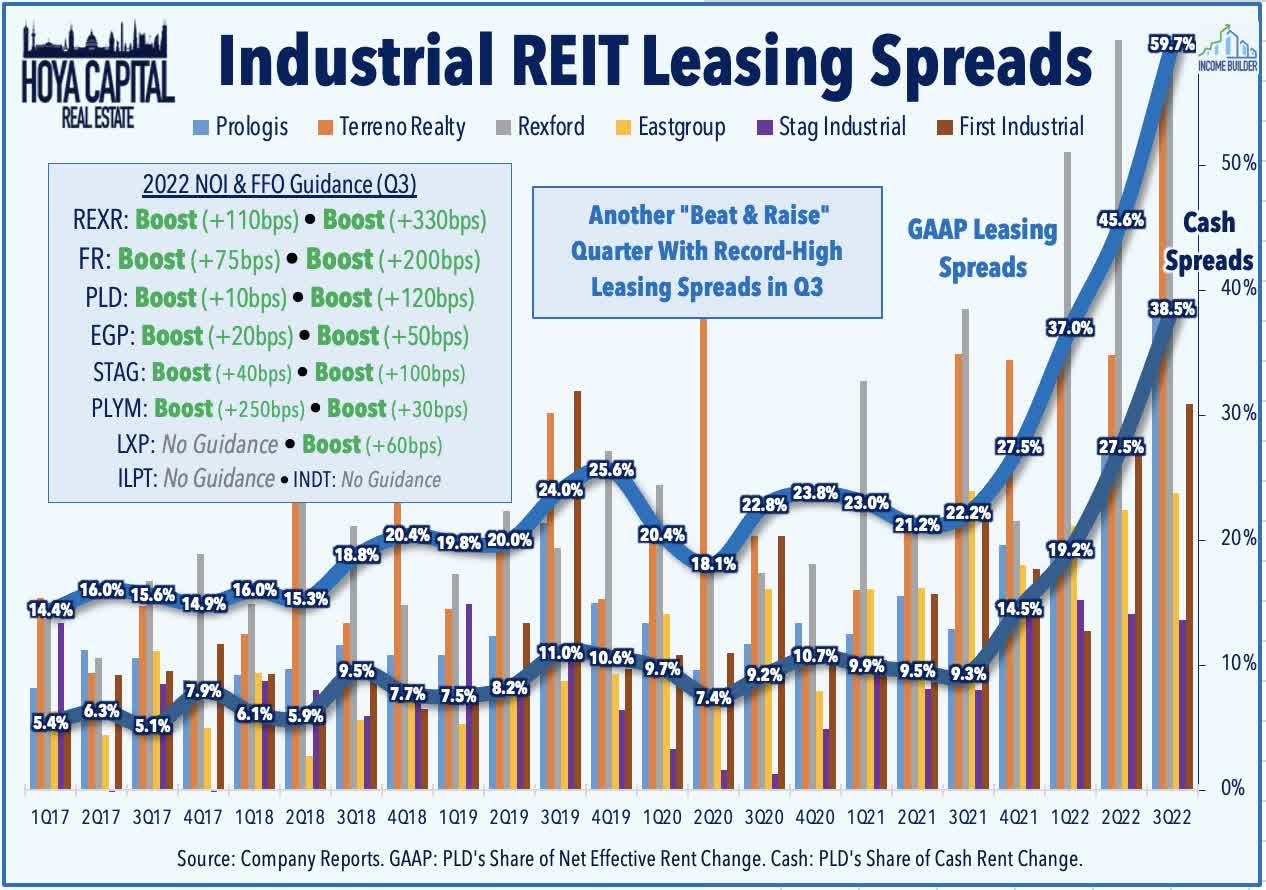

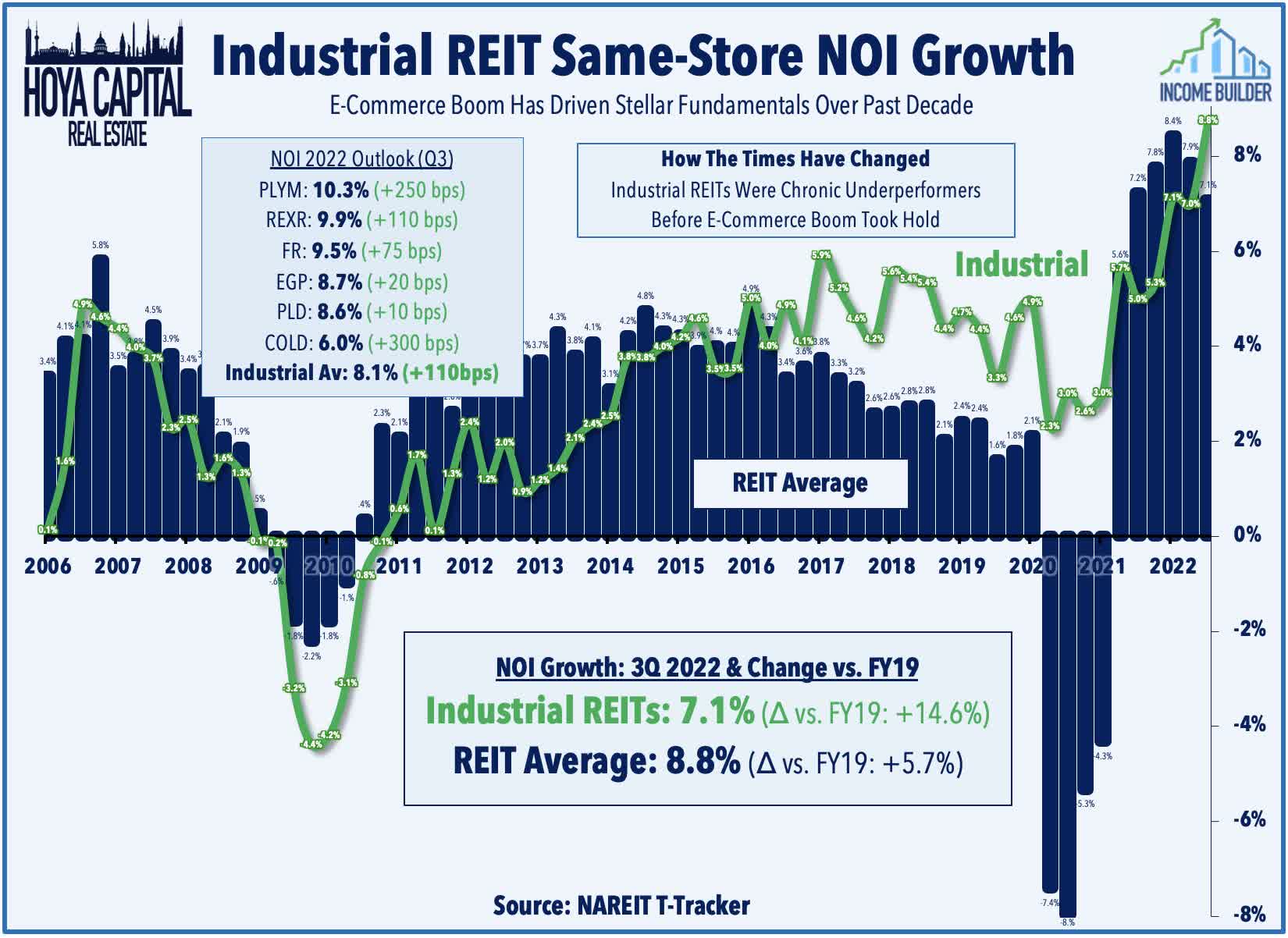

The still-favorable fundamental conditions were quite apparent throughout earnings season and recent interim updates as well. As analyzed in our REIT Earnings Recap , powered by another quarter of head-spinning cash rental rate spreads of over 30%, all seven of the industrial REITs that provide guidance raised their full-year FFO growth target in the third quarter. Industrial REITs are now expected to report full-year Funds From Operations ("FFO") growth of over 10% in 2022 - a second-straight year of double-digit earnings growth - and the momentum is expected to continue into 2023 given the significant embedded rent growth to be unlocked via the renewals of in-place leases which are currently estimated to be 20-40% below market rents.

{kind=link}

Hoya Capital

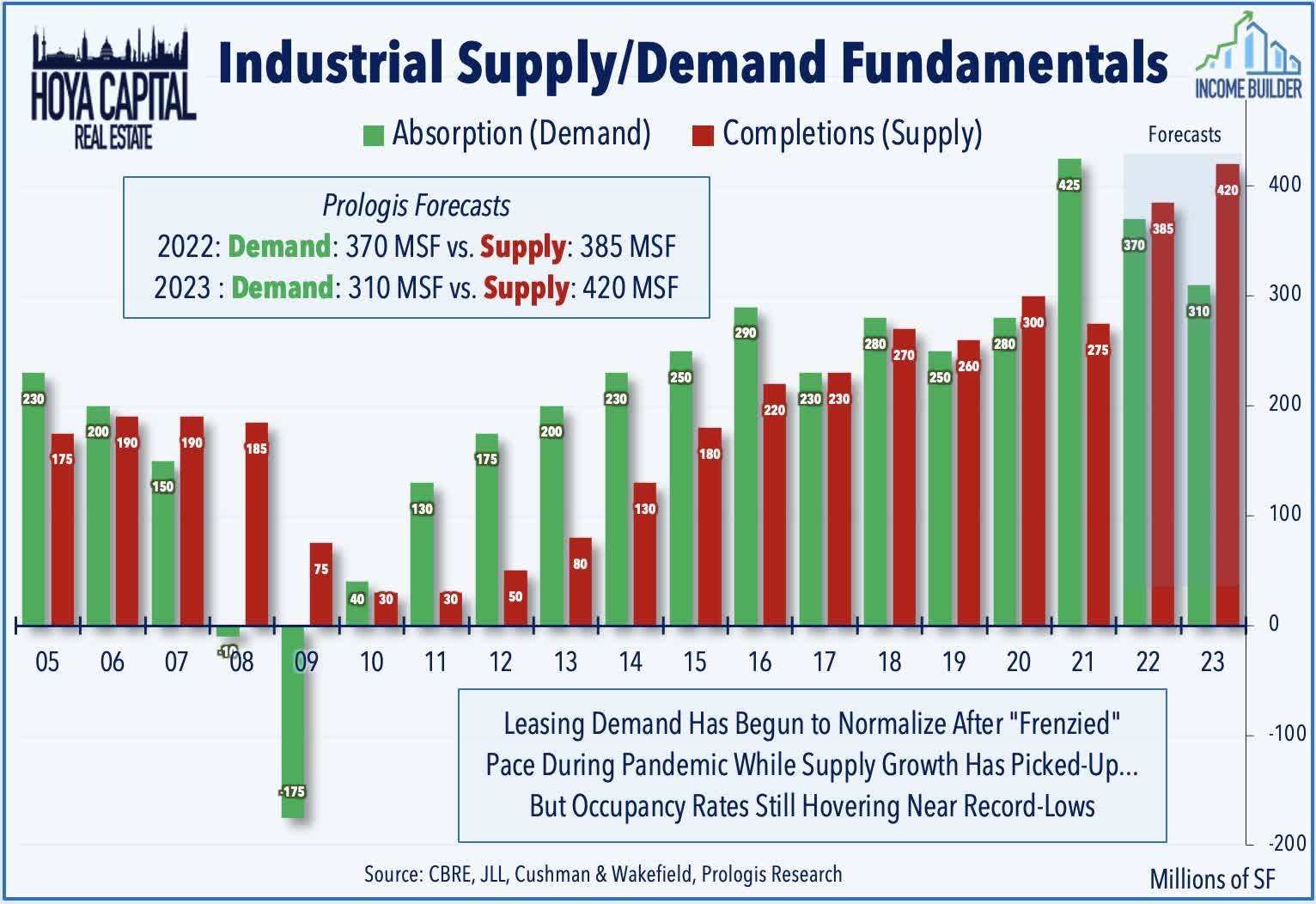

Pushing back on concerns of a sharp slowdown, Prologis Research actually increased its market rent growth forecast last month to nearly 30% in 2022 on the heels of 20% market rent growth in 2021, which had been the prior record high. Incremental demand is expected to moderate from the frenzied pace of activity during the pandemic, however, with Prologis' forecast now calling for 370 million square feet ("MSF") of net absorption in 2022, outpaced slightly by deliveries at 385 MSF. For 2023, Prologis expects 310 MSF of demand compared to 420 MSF of completions as "supply that was stuck in the pipeline is finally delivering" which is expected to push the vacancy rate to 4.0% this year - still historically low, but above that of 2021 and 2022. Driven by a rapid rise in the cost of capital, however, incremental development starts have declined significantly in recent months - down 60% by Prologis' estimates - implying an easing of these supply pressures in 2024.

{kind=link}

Hoya Capital

Deeper Dive: Industrial REIT Fundamentals

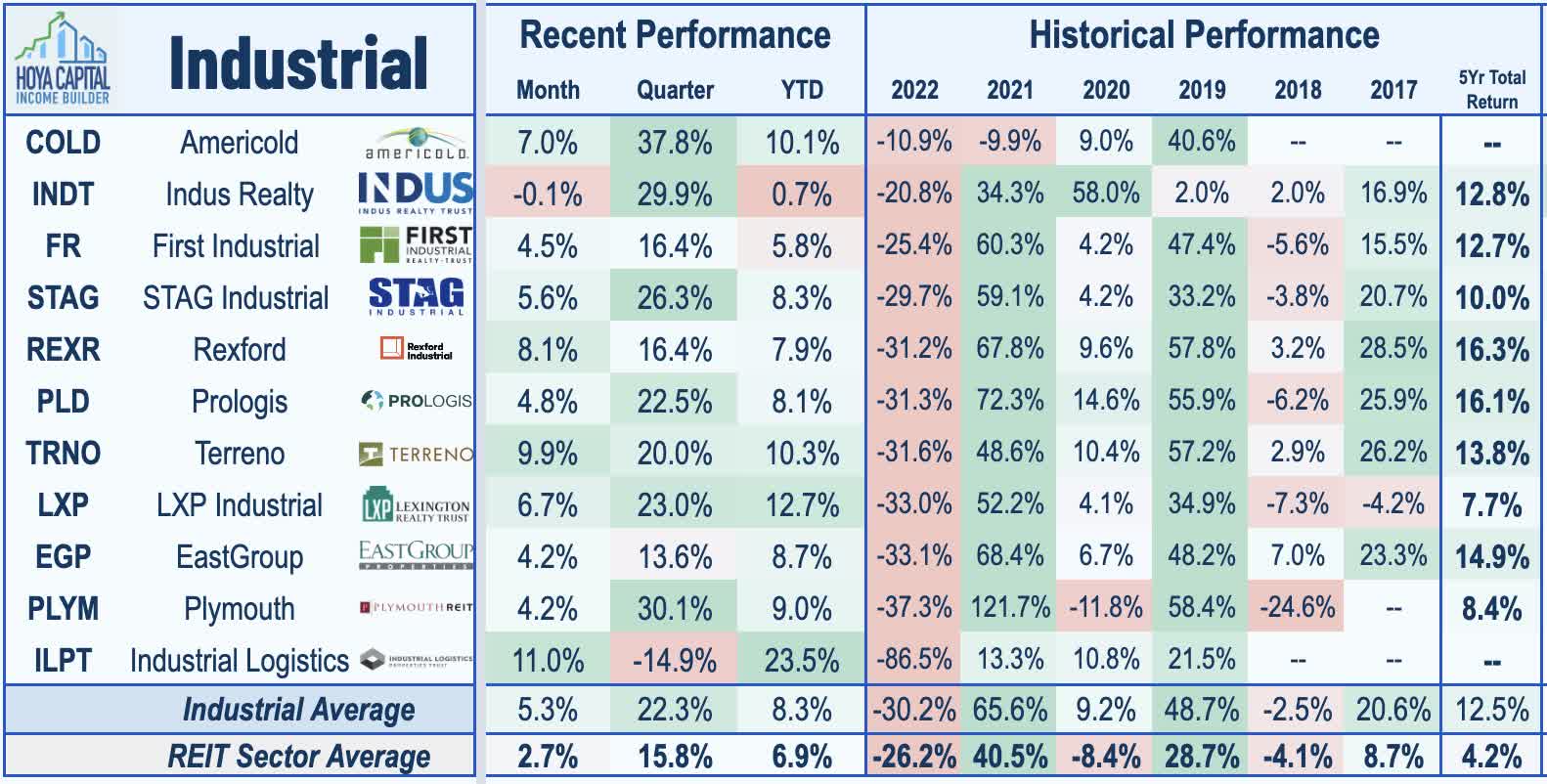

Diving deeper into company-level performance, sector stalwart Prologis ( PLD ) - which kicks off fourth-quarter earnings season this week - reported a record-high effective leasing spread of 59.7% in the third-quarter alongside record-high cash same-store NOI growth at 9.3%. First Industrial ( FR ) also reported record-high cash leasing spreads of 30.9%, driving a boost to its NOI outlook by 75 basis points to 9.5% and its FFO growth outlook by 200 basis points to 13.2 while Rexford ( REXR ) reported incredible cash rental rate spreads of 62.9% in Q3. STAG Industrial ( STAG ) also delivered impressive results with rent growth on new leases of nearly 20%. Plymouth ( PLYM ), meanwhile, hiked its full-year NOI growth target by 250 basis points to 10.3%, and now expects the strongest NOI growth in the sector.

{kind=link}

Hoya Capital

Even the lagging Americold ( COLD ) snapped a streak of icy-cold performance with a solid upward boost to its outlook. While property-level metrics remain stellar, some industrial REITs are still figuring out how to get out of their own way. LXP Industrial ( LXP ) still expects a decline in full-year FFO growth of nearly 15% as it seeks to sell its last remaining office assets as part of its transition to become a pure-play industrial REIT. LXP also announced earlier this year it is no longer pursuing a sale of the company, citing "the significant changes to macroeconomic, geopolitical, and financing conditions since it commended the process in early February." Another smaller industrial REIT, Industrial Logistics ( ILPT ) reported disappointingly slow progress in its plan to reduce its debt by selling assets from its recently-acquired Monmouth portfolio and an FFO drag from its bridge loan being used to finance the deal.

{kind=link}

Hoya Capital

While some smaller industrial REITs are facing challenges with portfolio repositioning, several other small- and mid-cap REITs are benefiting from the still-active M&A environment. In November, INDUS Realty ( INDT ) received a takeover proposal from Centerbridge Partners and GIC Real Estate for $65 per share, a 13% premium to INDUS' prior closing price. INDUS - previously known as Griffin Industrial Realty before its REIT conversion back in 2021 - is a small-cap REIT that owns 42 industrial/logistics buildings aggregating 6.1 million square feet in Connecticut, Pennsylvania, North Carolina, South Carolina, and Florida. INDUS' board said it will review the proposal "to determine the best path forward" that "maximized value for all of the company's shareholders." Centerbridge currently owns 15% of the Company’s common stock. For GIC, the deal would be its second major acquisition of the past year following its $14B takeover of net lease REIT Store Capital last September which is expected to close in the first quarter of 2023.

{kind=link}

Hoya Capital

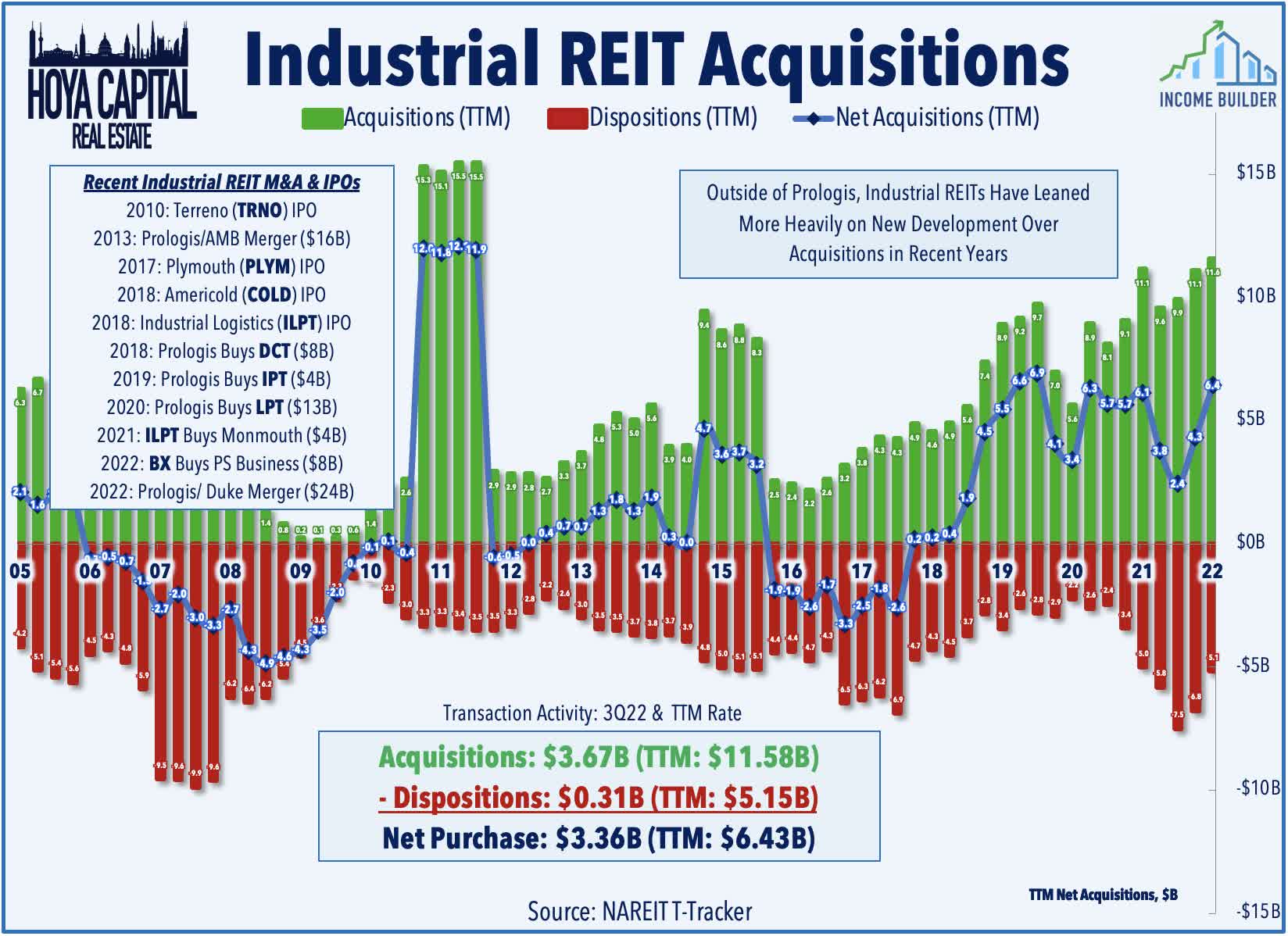

If Indus does indeed get acquired, it would be the fifth industrial REIT to be acquired since the start of 2022. In early 2021, Blackstone ( BX ) - scooped up PS Business Parks ( PSB ) - one of five public REIT acquisitions that fueled its growing non-traded REIT platform BREIT. Last June, Duke Realty ( DRE ) agreed to be acquired by logistics giant Prologis in a $26B all-stock deal that closed in the fourth quarter. Following months of pursuit and several rejected offers, the deal adds another 160 million square feet of space to Prologis' portfolio of over a billion square feet of logistics and industrial space. Prologis has been far and away the most active acquirer over the past half-decade with major acquisitions of DCT Industrial in 2018 for roughly $8B, Industrial Property Trust in 2019 of $4B, and Liberty Property Trust in 2020 for $13B.

{kind=link}

Hoya Capital

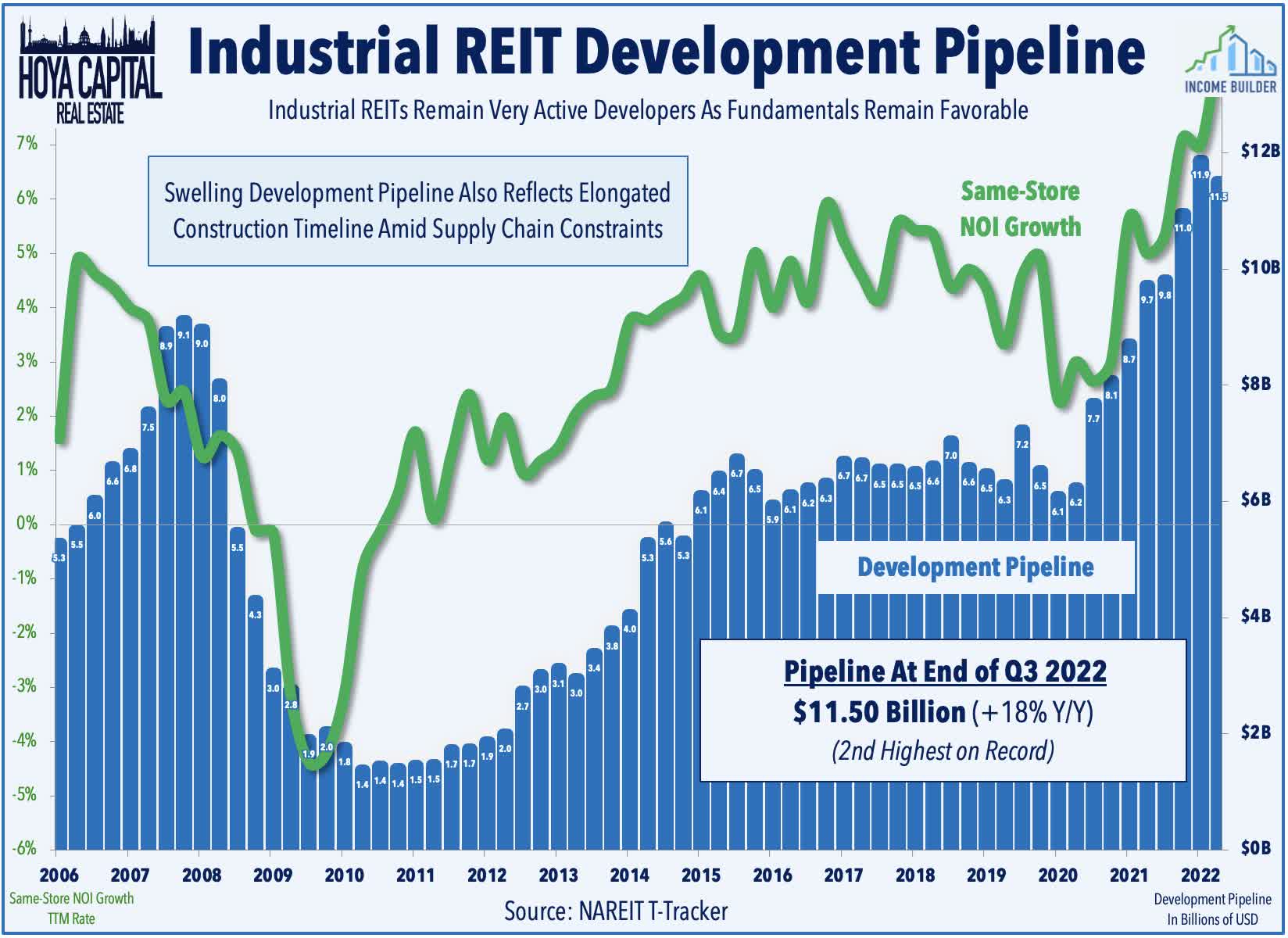

Industrial REITs have leaned heavily into ground-up development in recent years with accretive development yields averaging 6-8% compared to cap rates between 4%-6%. Industrial REITs have built up a sizable land bank over the last decade and are now responsible for a significant percentage of total industrial real estate development. While industrial supply growth is averaging roughly 2-3% per year, trends over the past three years lead us to believe that there are mounting barriers to entry and supply constraints that have limited the type of speculative building activity that resulted in sharp contractions in rent growth and Net Operating Income during the GFC period.

{kind=link}

Hoya Capital

Industrial REITs also operate with some of the most well-capitalized balance sheets across the real estate sector which is especially important for REITs with large development pipelines which can be a source of "shadow leverage." Industrial REITs operate with an average Debt-to-EV Ratio of just 14%, well below the REIT sector average of 25%. Four industrial REITs command investment-grade credit ratings including Prologis which owns the coveted "A-rated" long-term bond rating. The better-capitalized logistics-focused REITs including Prologis, Duke, Rexford, and Terreno have delivered some of the strongest performances of all REIT sover the past three years.

{kind=link}

Hoya Capital

Industrial REIT Stock Price Performance

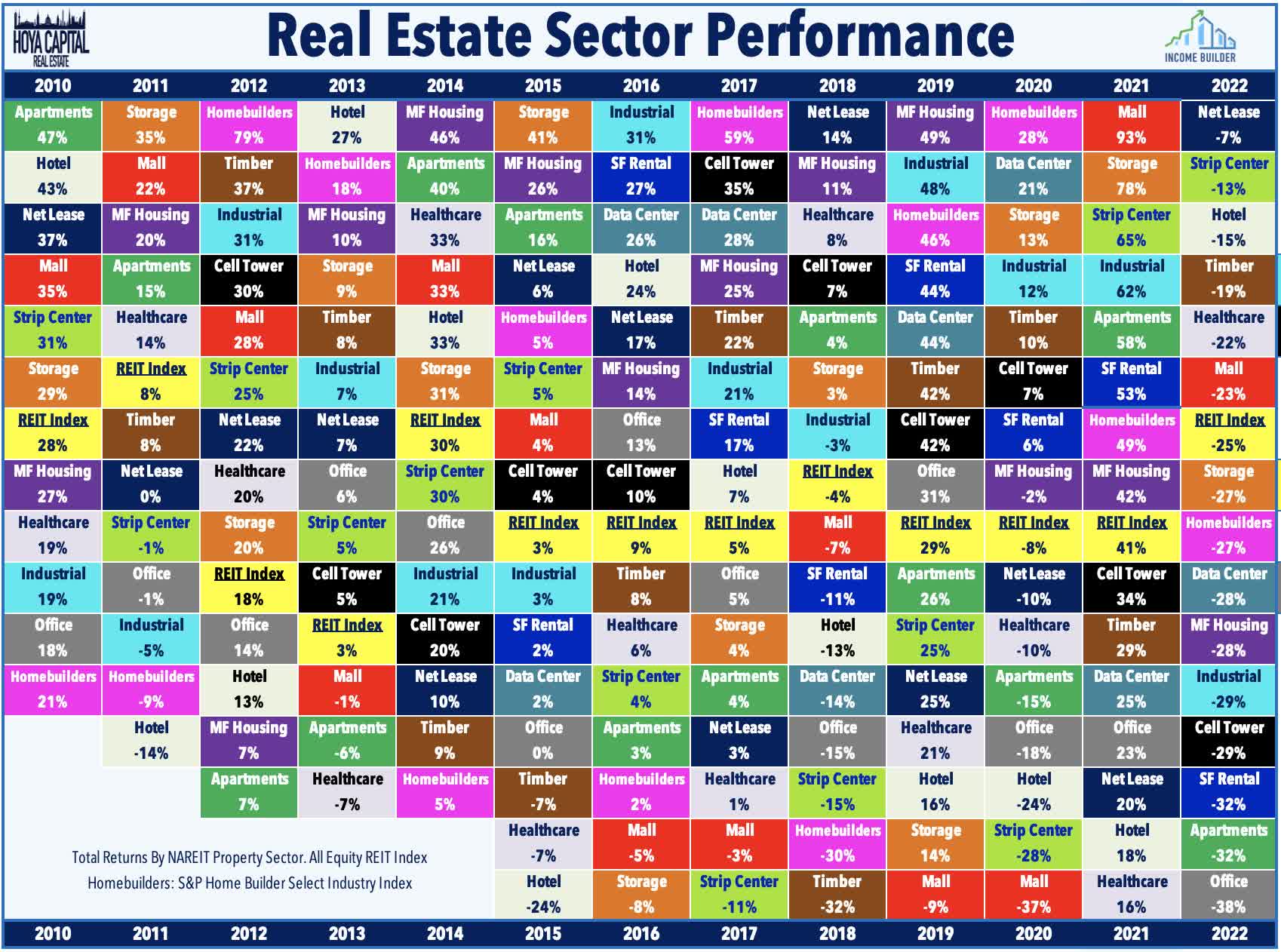

As noted above, Industrial REITs uncharacteristically lagged in 2022, dipping by nearly 30% for the year - the sector's worst year on record which snapped a seven-year streak of outperformance over the broader REIT Index. Despite the rough year, however, industrial REITs still remain the best-performing property sector since the start of 2015, producing average annual total returns of 16.7% which is more than triple the 5.6% average annual total returns produced by the Equity REIT Index during that period.

{kind=link}

Hoya Capital

Buoyed by the retreat in interest rates and cooling inflationary pressures, Industrial REITs are off to a stronger start in 2023 with the Hoya Capital Industrial REIT Index higher by 8.3% through the first two weeks of the year, outpacing the 6.9% returns from the broad-based Vanguard Real Estate ETF ( VNQ ) and the 4.2% gain from the S&P 500 ETF ( SPY ).

{kind=link}

Hoya Capital

The carnage last year was widespread across the sector with every industrial REIT lower by more than 10% on the year. Americold was the performance leader in 2022 after a disappointing 2021 for the cold storage operator. Indus Realty was also among the better performers following its takeover offer in November. Small-cap REITs were slammed particularly hard with Industrial Logistics dipping roughly 85% in 2022 after slashing its dividend while Plymouth pulled back by nearly 40%. The brutal year followed one of the strongest with nearly 65% returns in 2022.

{kind=link}

Hoya Capital

Deeper Dive Into The Industrial Sector

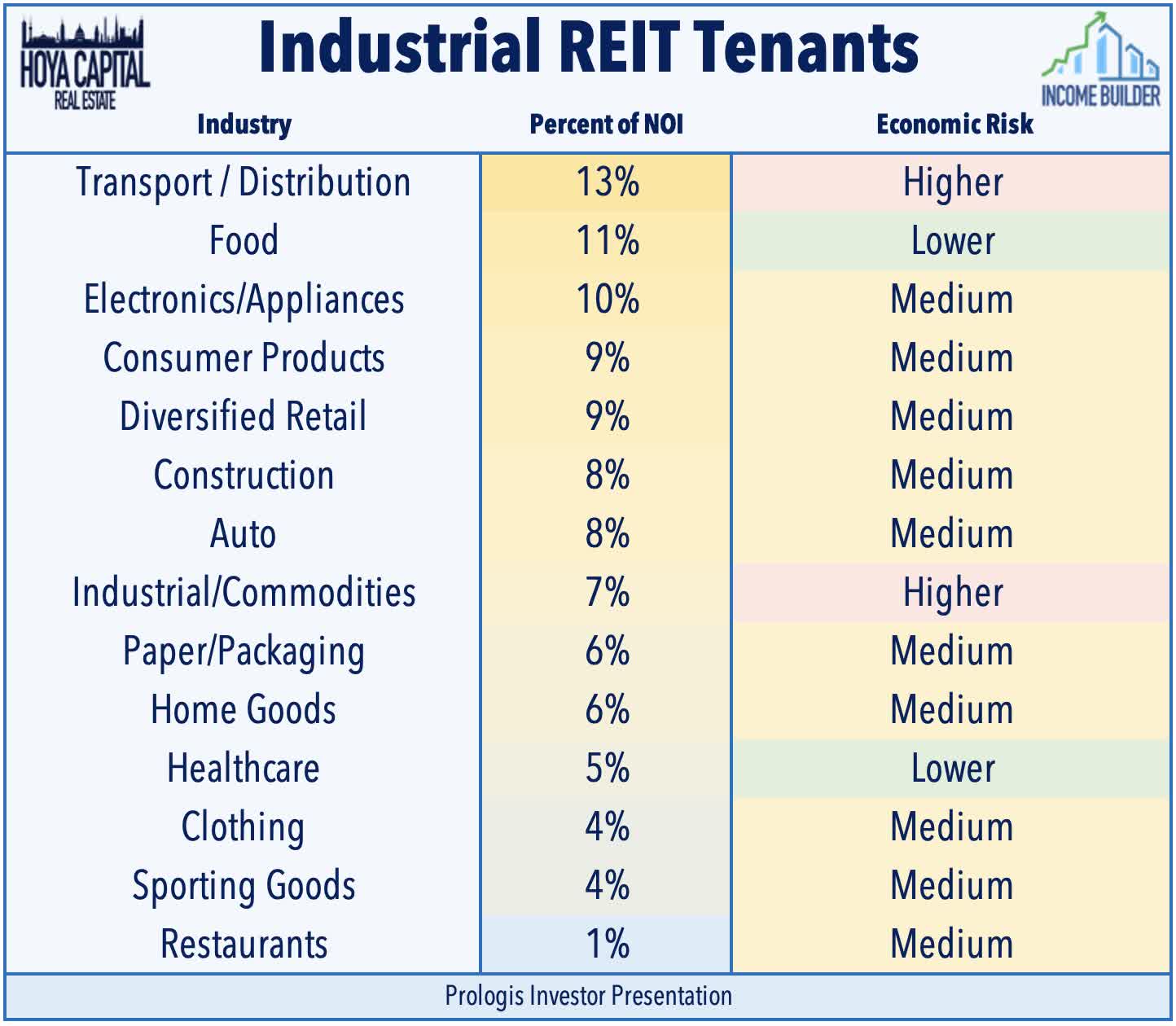

Industrial REITs own roughly 5-10% of total industrial real estate assets in the United States but own a higher relative percentage of higher-value distribution-focused assets with building sizes averaging around 200,000 square feet, which have seen significant rent growth and more favorable supply/demand conditions due to tangible constraints on land availability. Robust demand for space over the past decade has been driven by a relentless " need for speed " arms race as retailers and logistics providers have invested heavily in supply chain densification and physical distribution networks.

{kind=link}

Hoya Capital

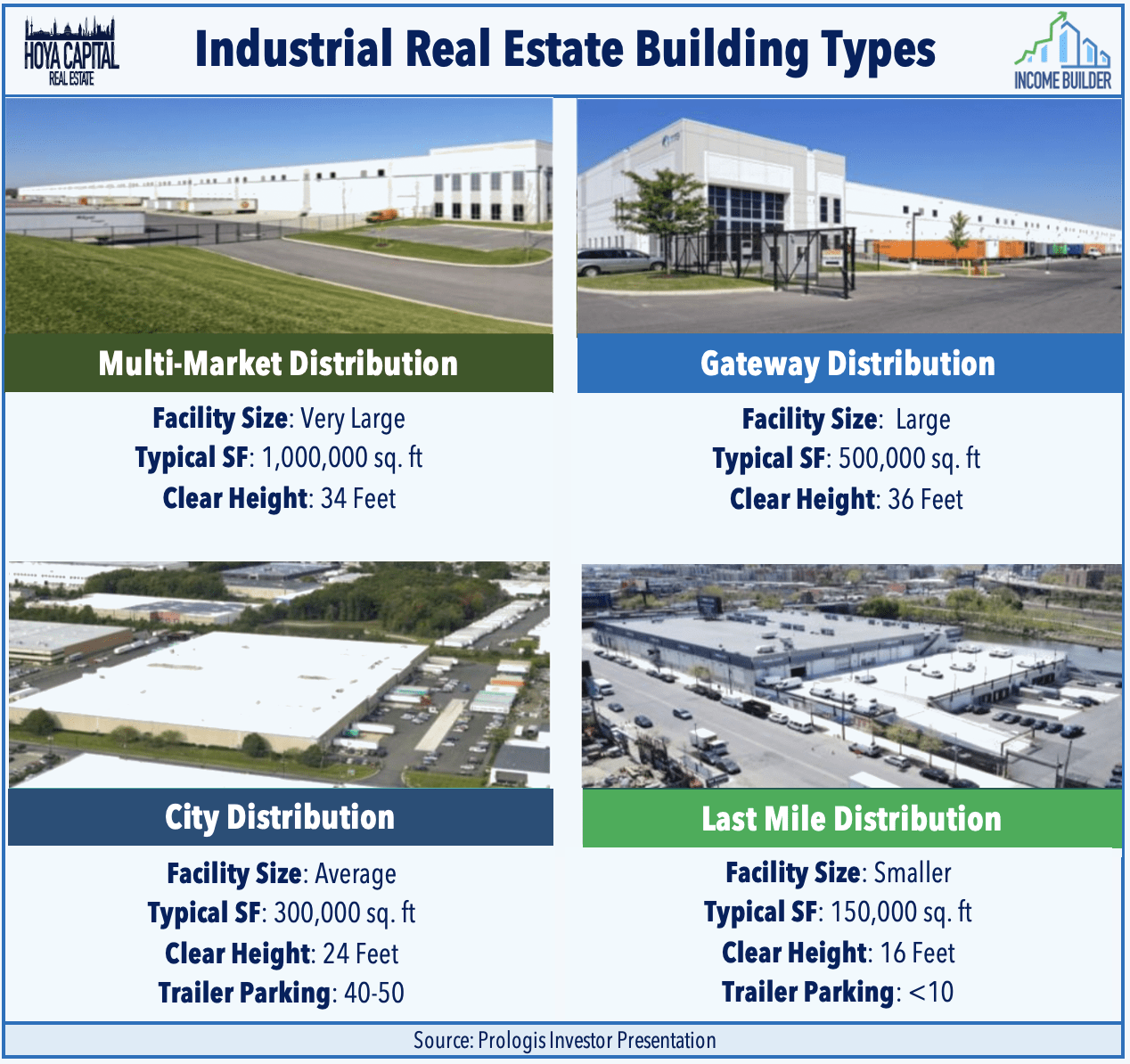

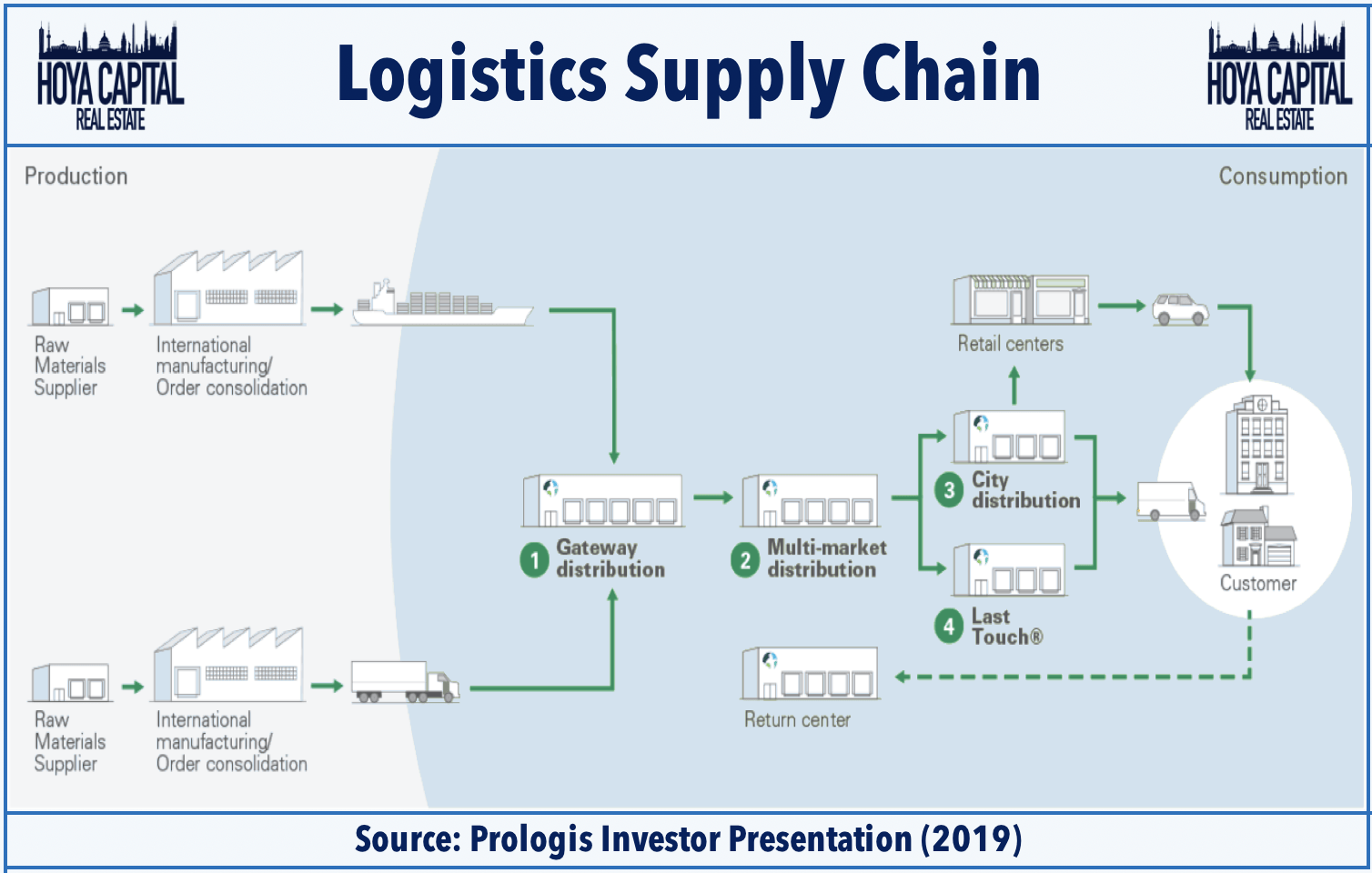

Prologis segments industrial real estate assets into four major segments: Multi-Market Distribution , Gateway Distribution , City Distribution , and Last-Touch Centers . Along that continuum towards the end-consumer, the relative value of these properties (on a per square foot basis) increases, as do the underlying barriers to entry due to the scarcity of permittable land. Rent growth has been most robust over the last half-decade in the segments closer to the end-consumer - typically occupied by distributors like UPS ( UPS ), and FedEx ( FDX ) - a trend that has been further accelerated by the pandemic.

{kind=link}

Hoya Capital

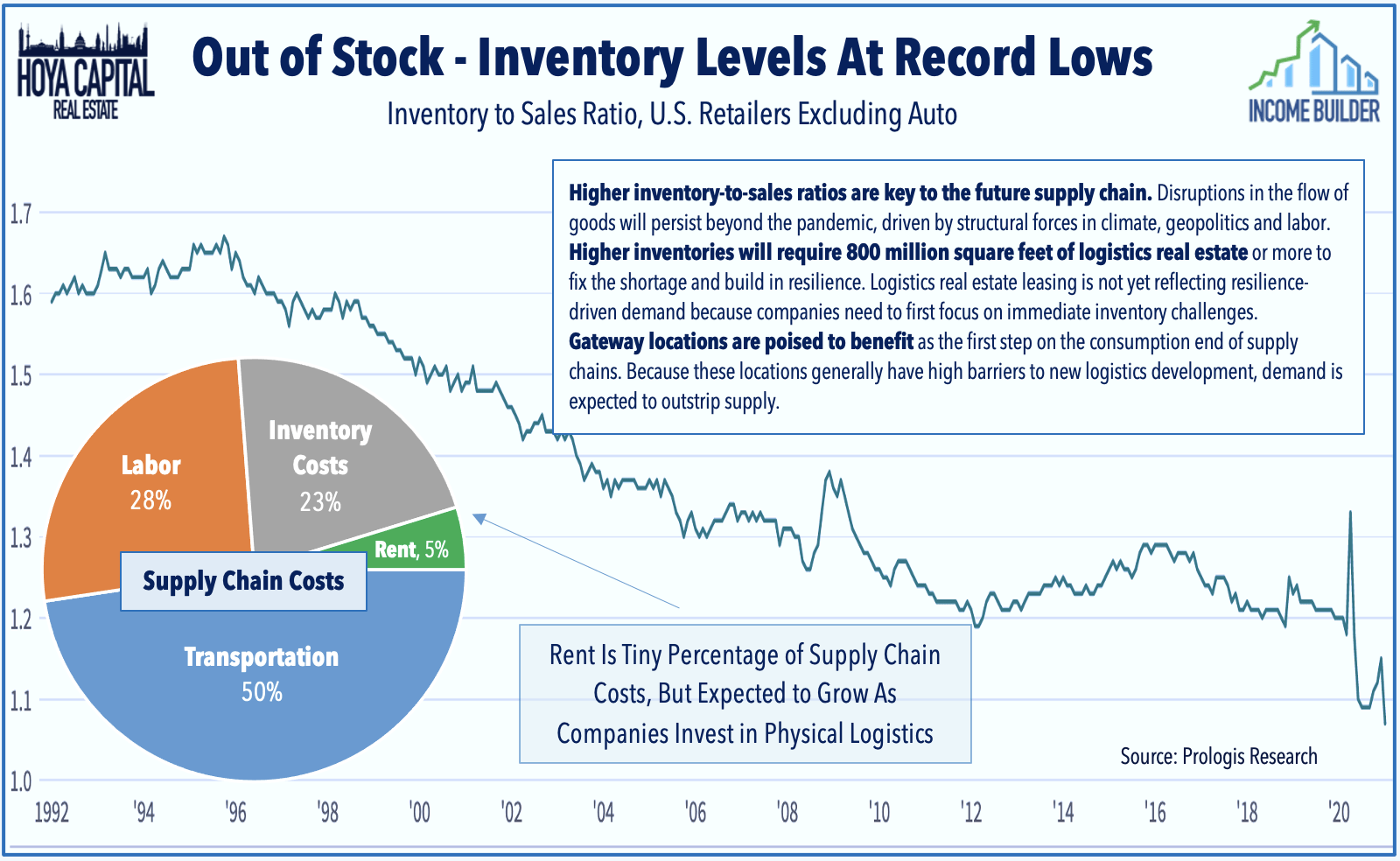

Supply chain disruptions came as inventory levels were already historically lean amid a shift towards "just-in-time" inventory management. Resilient supply chains will require substantial investments in logistics space with Prologis pegging the number at 800 million extra square feet just to reach equilibrium. These "just-in-case" trends are additive to the pre-existing "need for speed" trends which continue to be driven most prominently by e-commerce giant Amazon ( AMZN ) and increasingly by Walmart ( WMT ), Target ( TGT ), Home Depot ( HD ), and Lowe's ( LOW ). The pandemic significantly accelerated the penetration rate of e-commerce, which requires up to three times more logistics space than sales through traditional brick and mortar sales. A potential double-edged sword for industrial REITs, the shortage of industrial space itself has driven investments into logistics technologies that could eventually lead to higher levels of space efficiency.

{kind=link}

Hoya Capital

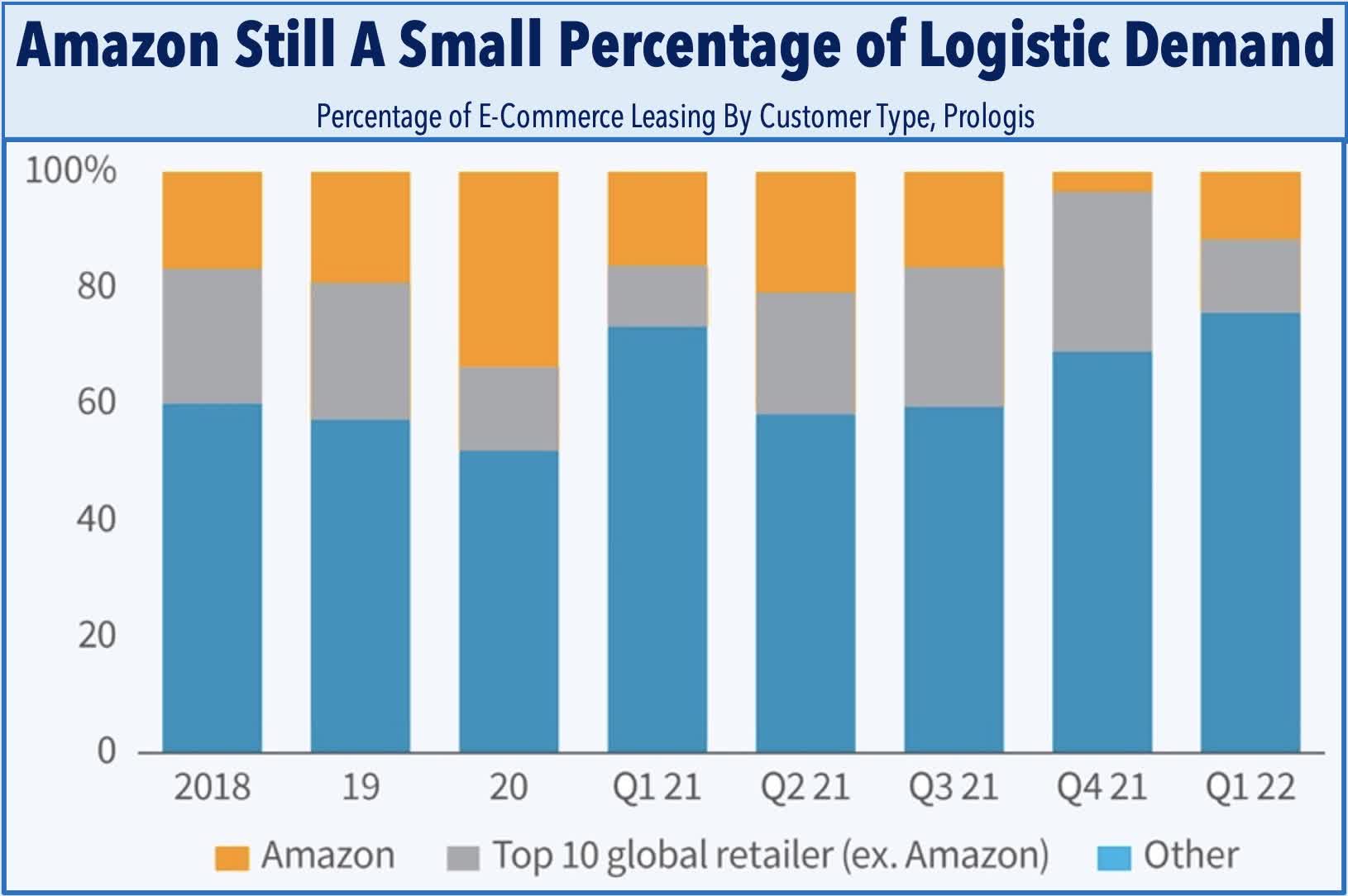

While major distribution and e-commerce giants like Amazon and FedEx are indeed among the largest industrial REIT tenants - and are decent bellwethers for the overall direction of incremental demand trends - these two companies combined still comprise roughly 5% of total occupied space. For industry insiders, Amazon's plans to scale back its expansion were not unexpected. Supply chain consulting firm MWPVL estimates that Amazon increased its square footage by nearly 400% between 2016-2021. The recent announcement from FedEx - which announced that it's "going fully into cost-management mode" - was a bit more surprising given its relatively slower pace of expansion in recent years, but unlike with Amazon, its industrial real estate portfolio isn't in the crosshairs of this cost cutting. FedEx noted that it is "reducing flights, temporarily parking aircraft, trimming hours for its staff, delaying hiring plans, and closing 90 FedEx Office locations."

{kind=link}

Hoya Capital

Industrial REIT Dividend Yields

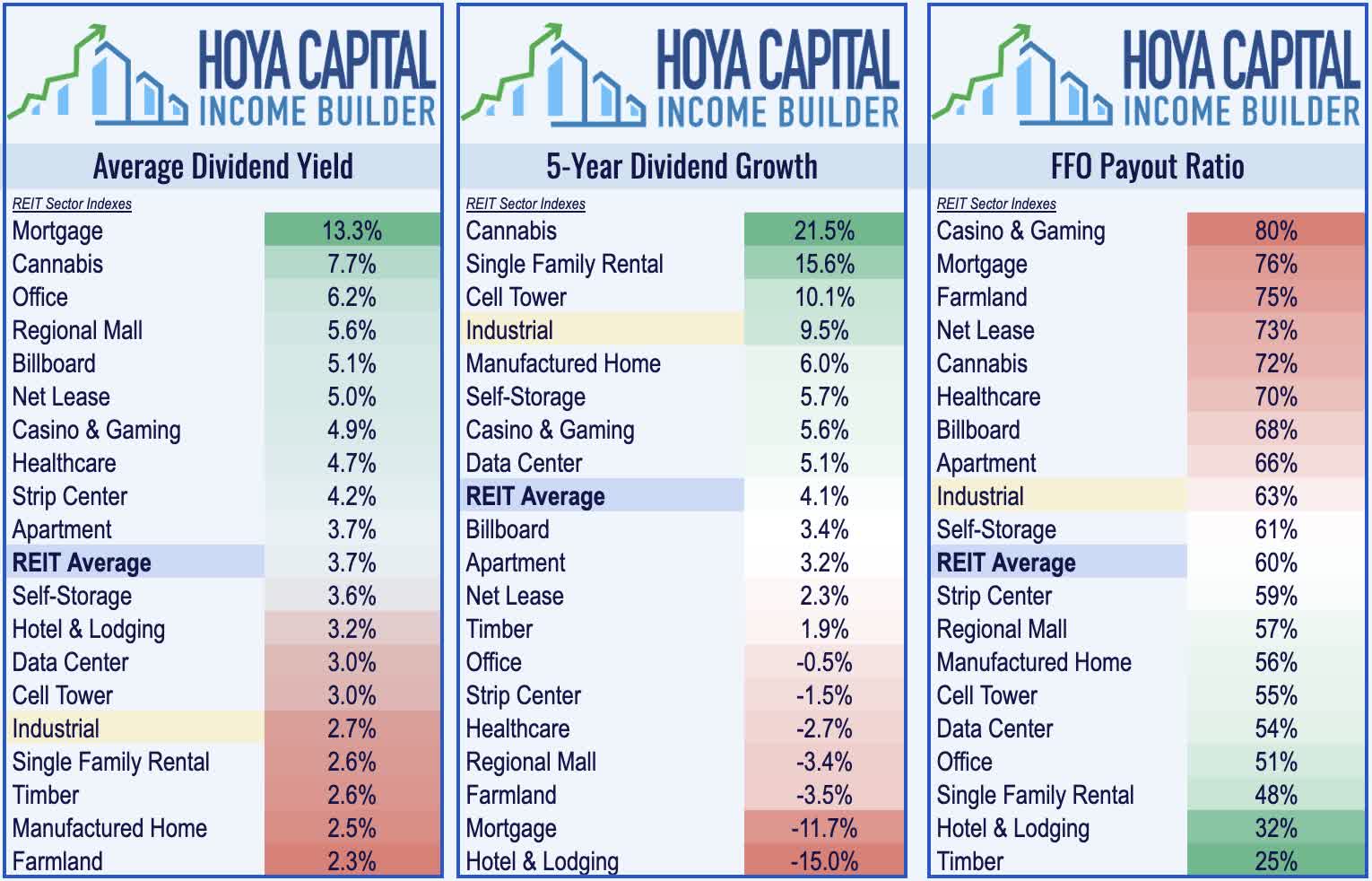

Appreciated more for their dividend growth than their current yields, industrial REITs pay an average dividend yield of 2.7%, which is below the REIT average of roughly 3.7%. However, it's important to note that Industrial REITs have grown both dividend distributions and FFO by nearly 10% per year since 2014, significantly higher than the REIT sector average of roughly 4%. Industrial REITs pay out roughly 60% of their available free cash flow, leaving an ample cushion for development-fueled growth and future dividend increases.

{kind=link}

Hoya Capital

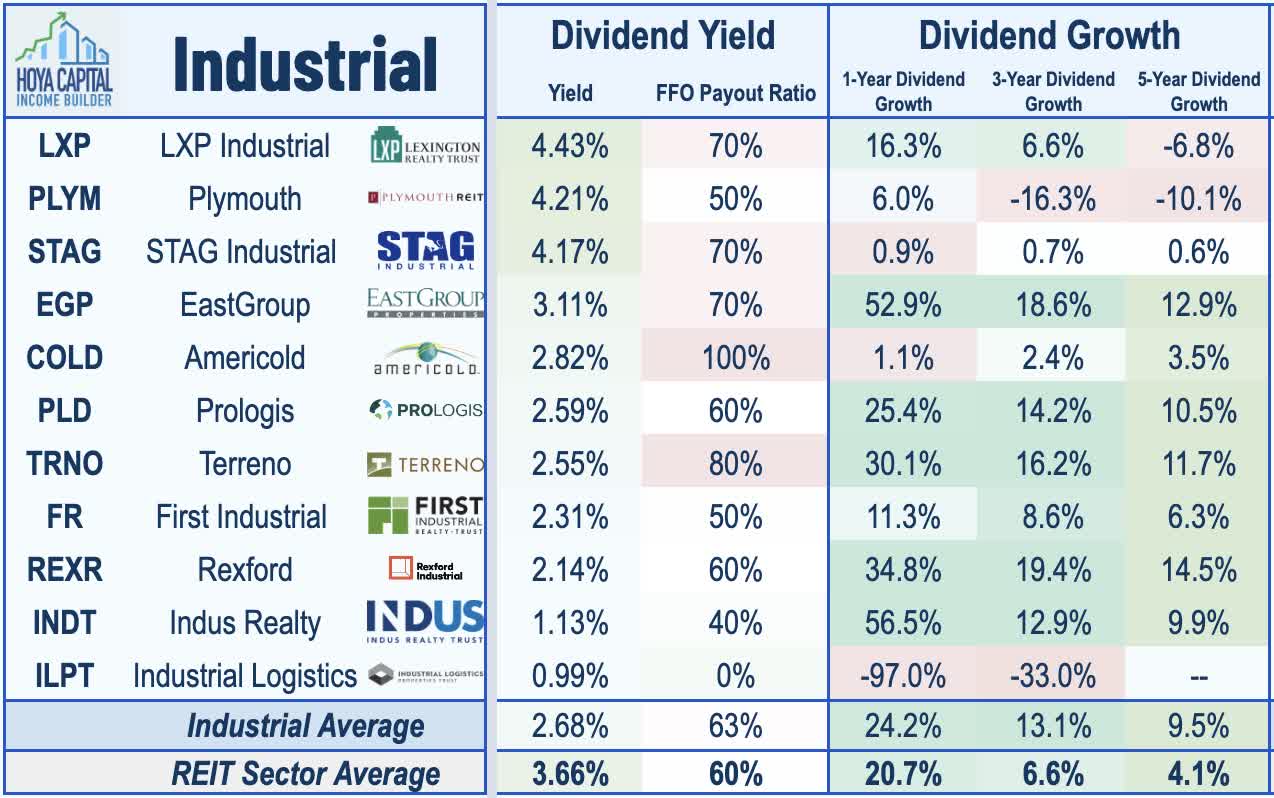

Within the sector, we note the varying strategies of the eleven industrial REITs where the "tradeoff" between high current yield and long-term dividend growth becomes quite apparent. The three "Yield REITs" at the top of the chart pay an average current yield between 4.0%-4.5% but have seen their dividends grow at slower rates. On the other hand, the eight "Growth REITs" pay an average dividend yield of around 2% but have seen their dividends grow by an average of 10% per year over the past five years.

{kind=link}

Hoya Capital

Takeaways: Logistics Tailwinds Still Intact

Global supply chains have rapidly normalized following historic pandemic-era disruptions, fueling concern that the "boom-bust" dynamics seen in the global shipping industry are headed for the industrial property sector which enjoyed historic rent growth of over 20% in 2021 and 2022. While industrial REITs aren't entirely immune from post-pandemic demand normalization, supply growth remained inherently capped by land constraints. While rent growth will naturally moderate toward "trend" levels, fundamentals are forecast to remain healthy absent a significant demand shock. We reiterate our view that dividend growth-oriented investors should be overweight in the industrial sector and be willing to "pay up" for the higher-quality names while looking for targeted value opportunities among the mid-cap and small-cap names.

{kind=link}

Hoya Capital

For an in-depth analysis of all real estate sectors, be sure to check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

Hoya Capital

For further details see:

Industrial REITs: Shortages Become Gluts