IFNNY - Infineon Technologies: Upside Attractive If It Rerates Back To Peers' Level

2023-08-06 23:27:50 ET

Summary

- I recommend a Buy rating as I expect growth normalization and valuation reversion to peers' levels.

- Demand for green energy transition and electromobility are driving performance.

- China's expansion of electromobility incentives should boost Infineon's automotive semiconductor sales in FY24.

Investment action

Based on my current outlook and analysis of Infineon Technologies ( OTCQX:IFNNY ), I recommend a buy rating. I expect the business to see its growth normalize as it continues to clear its backlog. Infineon should also see its valuation rerate back to 10x forward EBITDA, similar to peers’ levels, where it has historically traded in line.

Basic info

Infineon designs, manufactures, and markets semiconductors. The Company offers products including power semiconductors, microcontrollers, security controllers, radio frequency products, and sensors. Infineon markets its products to the automotive, industrial, communications, and consumer and security electronics sectors.

Review

Infineon reported a 3Q23 revenue of €4.089 billion (~1% sequential drop), with a sequential drop of 14% in Connected Secure Systems. Although demand for consumer applications like smartphones and PCs remains weak, I believe this is a problem shared by all industry participants. Management has noticed that, despite some seasonal fluctuations in smartphone-related areas, general demand remains subdued with customers continuing to clean out inventory levels. More importantly, the green energy transition and electromobility continue to support strong demand in IFNNY's primary end-markets, which include automotive and industrial applications. Also, 2Q23 backlog still stands at €32 billion which is still 2x FY23 guided revenue, as such I think there is little risk to near-term performance.

Remember too that roughly half of Automotive segment sales come from the high voltage power semis and microcontroller portfolio. Even though supply and demand for the company's more established automotive products are beginning to normalize, management noted that demand for the company's high voltage power semis and microcontroller portfolio remains tight, which is helping to maintain resilient pricing on a more systemic level. In fact, management believes there is room for price increases in the future in categories like differentiated power semis.

“So first of all, pricing in automotive is very firm and I think this is what you referred to, and also pricing in many parts of the industrial business is as it is in allocation, very firm. We even see some opportunities for silicon carbide to -- for example, on silicon carbide to increase prices.” 3Q23 earnings call

Management has also singled out China as a country with an especially severe demand/supply mismatch. Notably, the recent expansion of electromobility incentives is helping China become one of Infineon's robust growth markets. For Infineon, I see this as a boost to their automotive semiconductor sales in FY24, and I expect the growth of automotive semiconductor market will be a major contributor to the company's overall revenue and margin growth.

As the demand for EV and microcontrollers has persisted, the market for these products has fostered healthy price dynamics, keeping the absolute margin on ATVs relatively high. I believe the current margin will remain stable, and I have faith in Infineon's ability to structurally improve pricing due to the company's rising profile in these important markets.

Valuation

Author's work

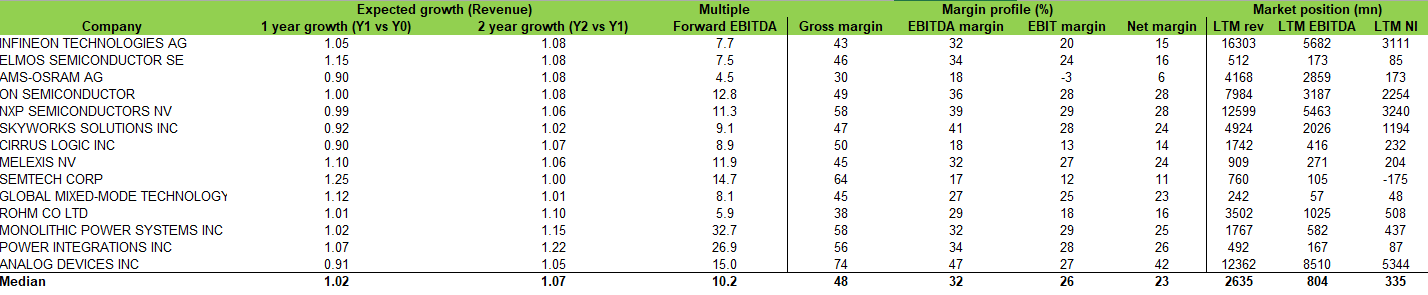

I believe Infineon's Growth in FY23 is pretty much in the bag given the huge backlog to clear, and it should see its growth normalized back to historical (pre-Covid) levels once its backlog normalizes. I assumed margin to remain strong at the current level, with potential for margin to improve (that I did not model in, just to be conservative). The key assumption in my model is that I expect multiple to re-rate back to 10x forward EBITDA, similar to peers’ levels, which it has historically traded in line with. I think the de-rating so far is because investors are worried about growth normalizing, and I point out that peers are also growing in the mid- to high-single digits. While Infineon's margins are lower than peers’ medians (justifying some discount), its market position (ranked by revenue) deserves some premium. As business and industry return to normalcy, valuation should too. At 10x forward EBITDA, I see 47% upside to the stock.

{kind=link}

Author's work

Risk and final thoughts

While Infineon is exposed to multiple secular tailwinds, like automotive electrification, the actual timing of adoption could be delayed or much slower than expected. This could potentially lead to a mismatch between investors’ expectations and actual results.

Overall, I recommend a buy rating based on the anticipation of growth normalization as backlog clears and valuation reverts to peers' levels. Demand for green energy transition and electromobility continues to drive performance in key markets. China's expansion of electromobility incentives should bolster Infineon automotive semiconductor sales in FY24, contributing to overall revenue and margin growth.

For further details see:

Infineon Technologies: Upside Attractive If It Rerates Back To Peers' Level