PLW - Inflation Rebound Doesn't Change The Big Picture

Summary

- Inflation bounced back in January, which will likely make the Fed more cautious and increases the probability of further rate hikes.

- The increase in inflation was fairly broad based and not just the result of a change in basket weights.

- The latest inflation figures also need to be viewed in light of the strong December labor market data.

The economy is still adjusting to strong demand and supply chain issues caused by the pandemic. As a result, inflation continues to be an issue in some areas and temporary deflationary forces appear to be waning. Despite this, extreme price increases now appear to be a thing of the past and there is no longer broad-based inflation across all categories. January's inflation data does not change the big picture, but it does increase the probability that the Fed will continue to raise interest rates.

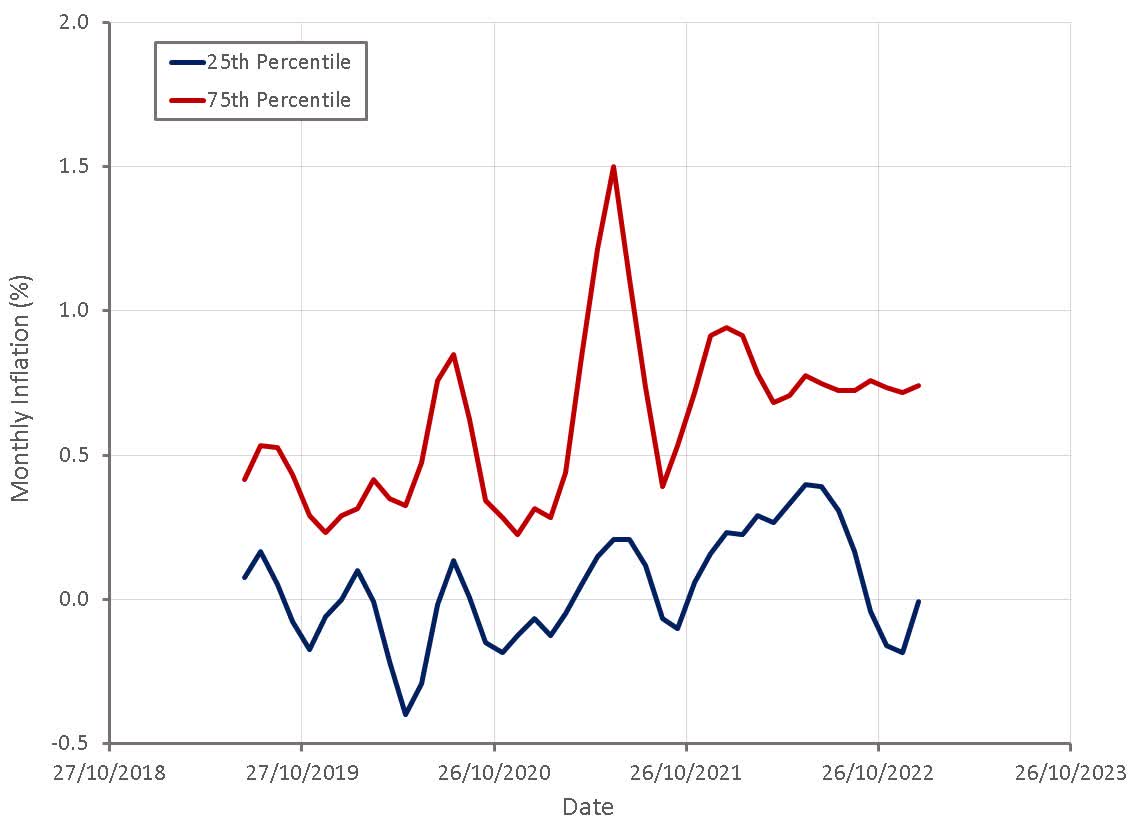

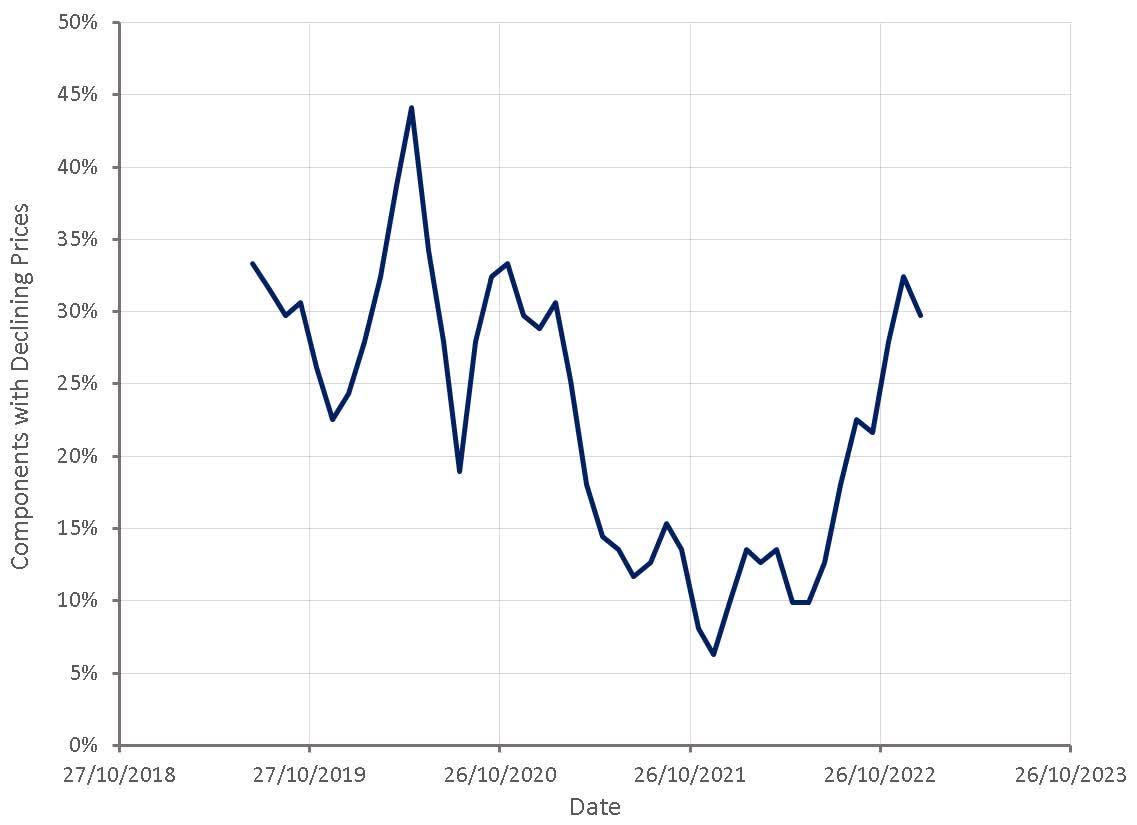

Figure 1: Monthly Inflation by Percentile Ranking 3-Mo. Moving Average (source: Created by author using data from BLS) Figure 2: Proportion of CPI Components with Declining Prices 3-Mo. Moving Average (source: Created by author using data from BLS)

{kind=link}

{kind=link}

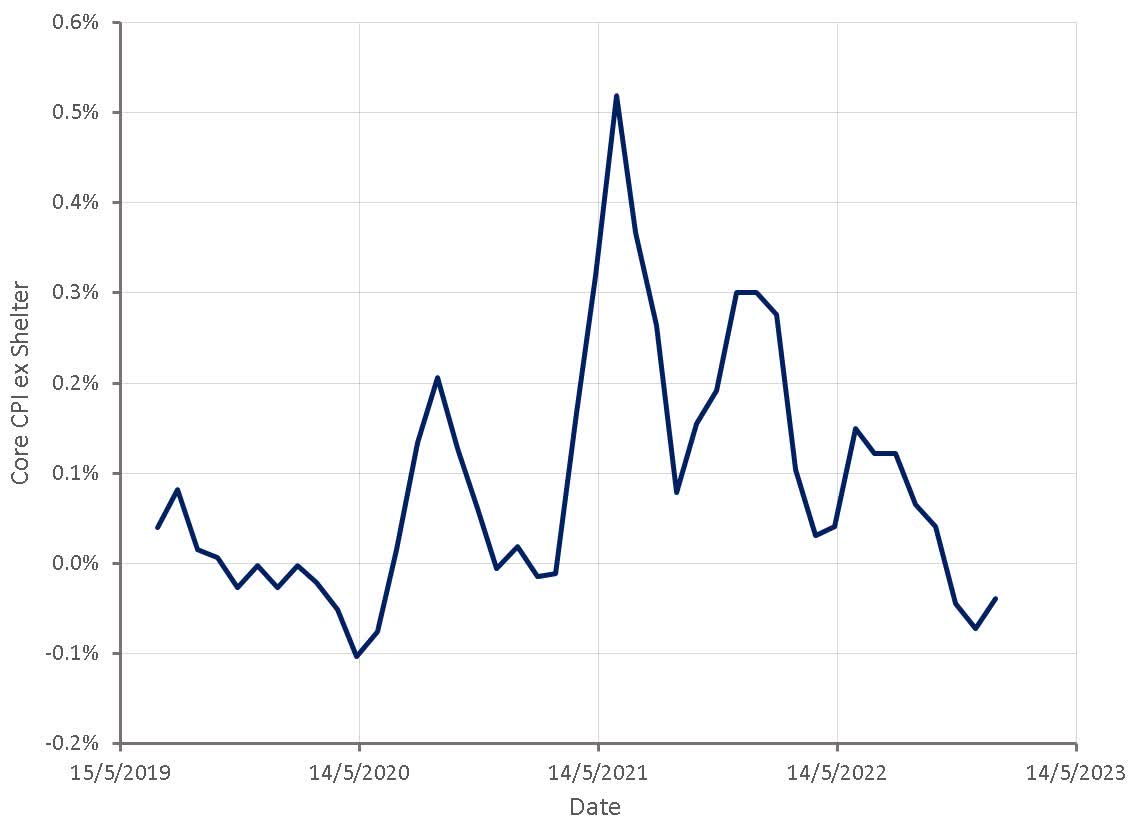

While inflation continues to be a problem in some parts of the economy, excluding the highly lagged shelter component, core CPI inflation continues to illustrate that high inflation is largely a thing of the past.

Figure 3: Core CPI ex-Shelter Monthly Inflation 3-Mo. Moving Average (source: Created by author using data from BLS)

{kind=link}

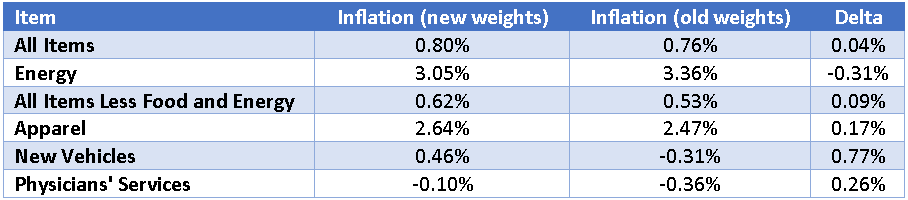

There was some concern that updated weights in the CPI basket would distort January's inflation figures, and while this did occur to some extent, it did not really change the overall picture. Inflation was much stronger in January than it has been in recent months, both headline and core.

Table 1: Monthly CPI Inflation (source: Created by author using data from BLS)

{kind=link}

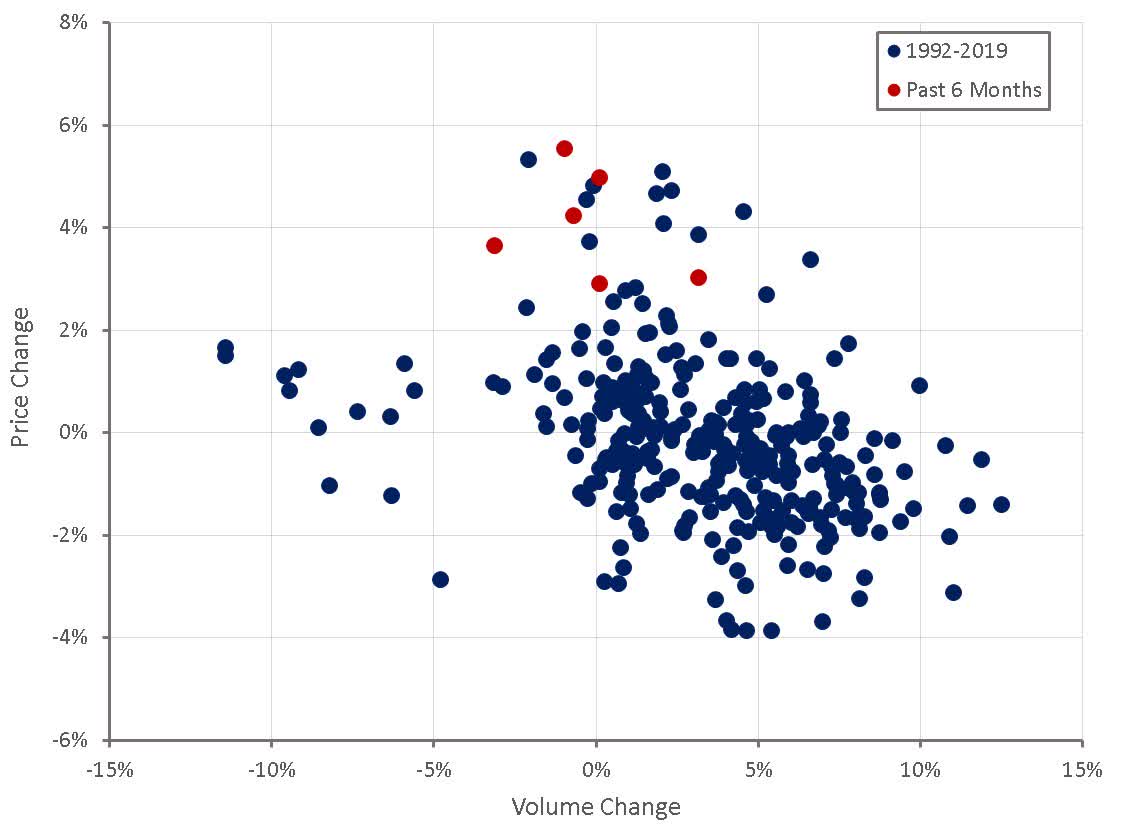

Apparel inflation is somewhat illustrative of the problem with extrapolating January's data and assuming it represents a reacceleration. Growth in real apparel sales has been fairly weak in recent months, but despite this apparel inflation has been quite strong, a situation that is unlikely to persist.

Figure 4: Apparel Sales (source: Created by author using data from The Federal Reserve)

{kind=link}

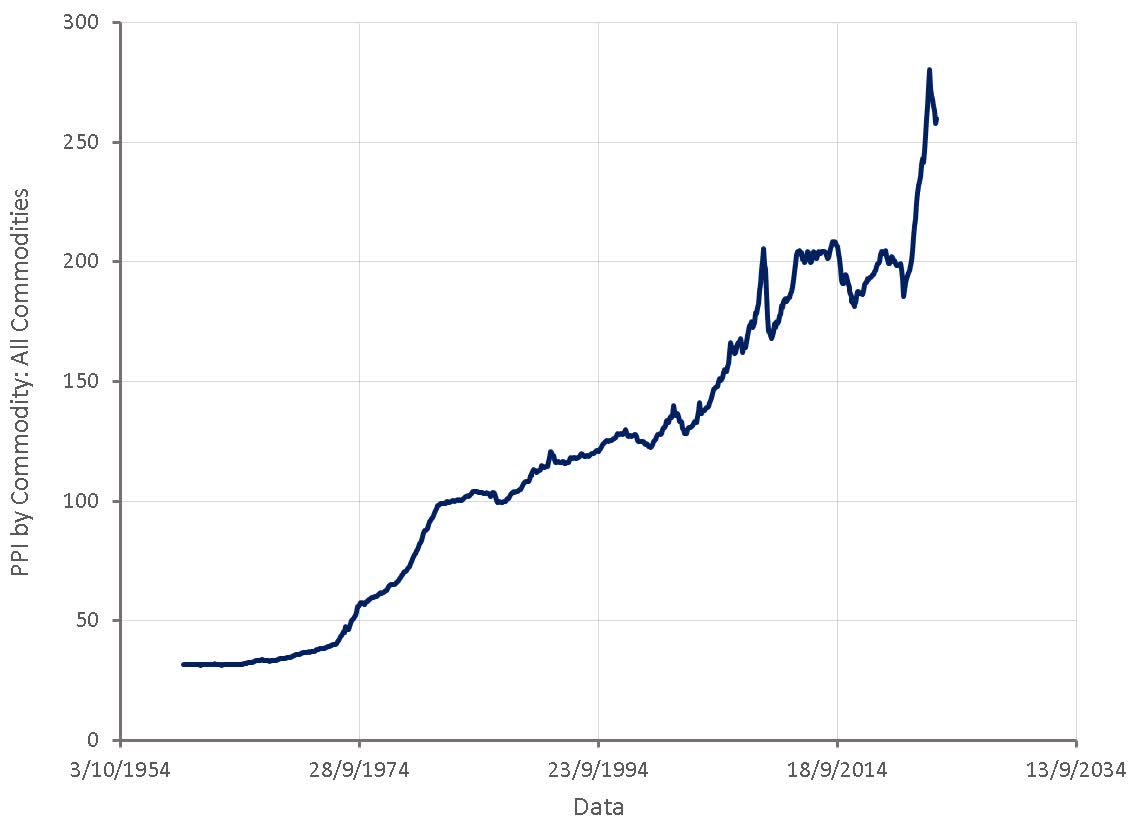

Monthly inflation data can be noisy and absent several consecutive months of strong inflation, there is no reason to think that there has been a change in trend. Data that is likely to lead consumer price inflation continues to show that supply chains are normalizing and inflationary pressures are easing. Shipping rates have returned to close to pre-COVID levels and continue to decline, the same with fertilizer prices. Commodity prices have generally been fairly weak in recent months, and China's reopening does not appear to be having a significant impact.

Figure 5: PPI by Commodity: All Commodities (source: Created by author using data from The Federal Reserve)

{kind=link}

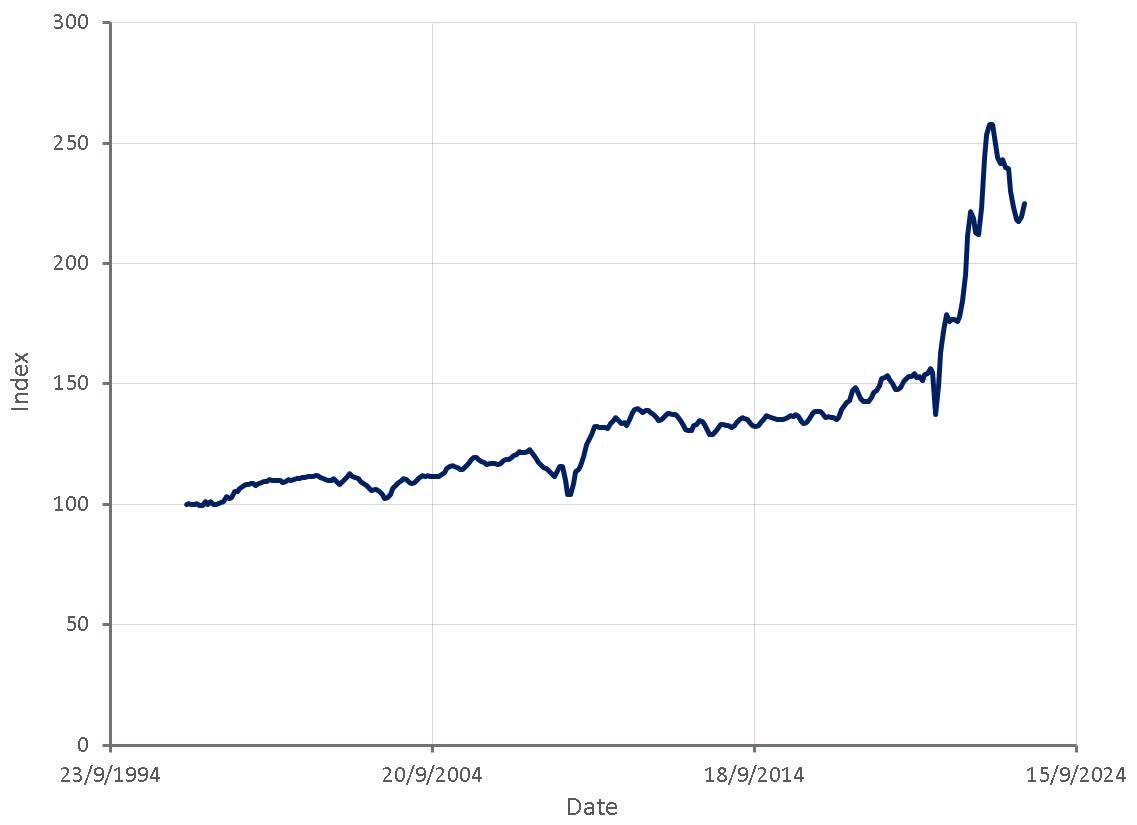

Not all data is positive though, used car prices remain high and have started to increase again.

Figure 6: Manheim Used Vehicle Value Index (source: Created by author using data from Manheim)

{kind=link}

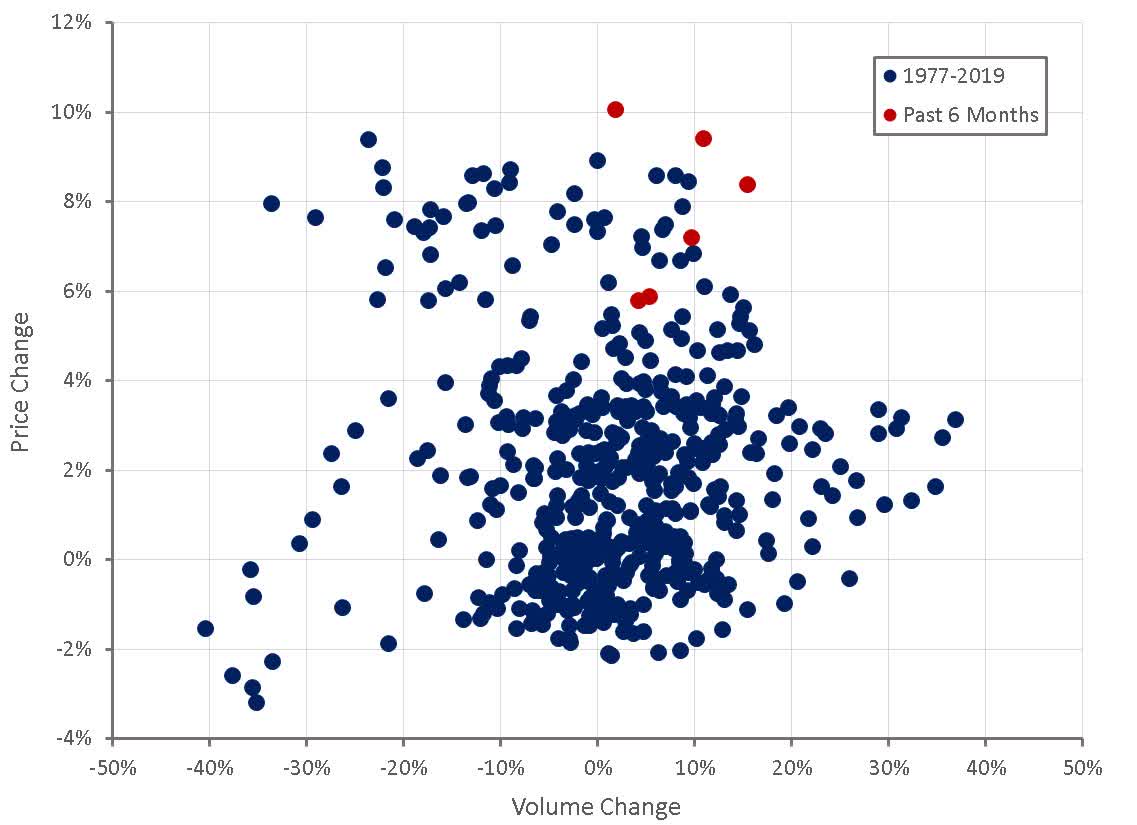

It has been suggested that automakers are taking advantage of current conditions to maintain high prices and profit margins. There is no reason to expect this situation to be ongoing though. Weaker growth in 2023 or 2024 is likely to result in lower prices and margins for auto makers.

Figure 7: New Vehicle Sales (source: Created by author using data from The Federal Reserve) Figure 8: Growth and Profitability of Large Auto Manufacturers (source: Created by author using data from The Federal Reserve)

{kind=link}

{kind=link}

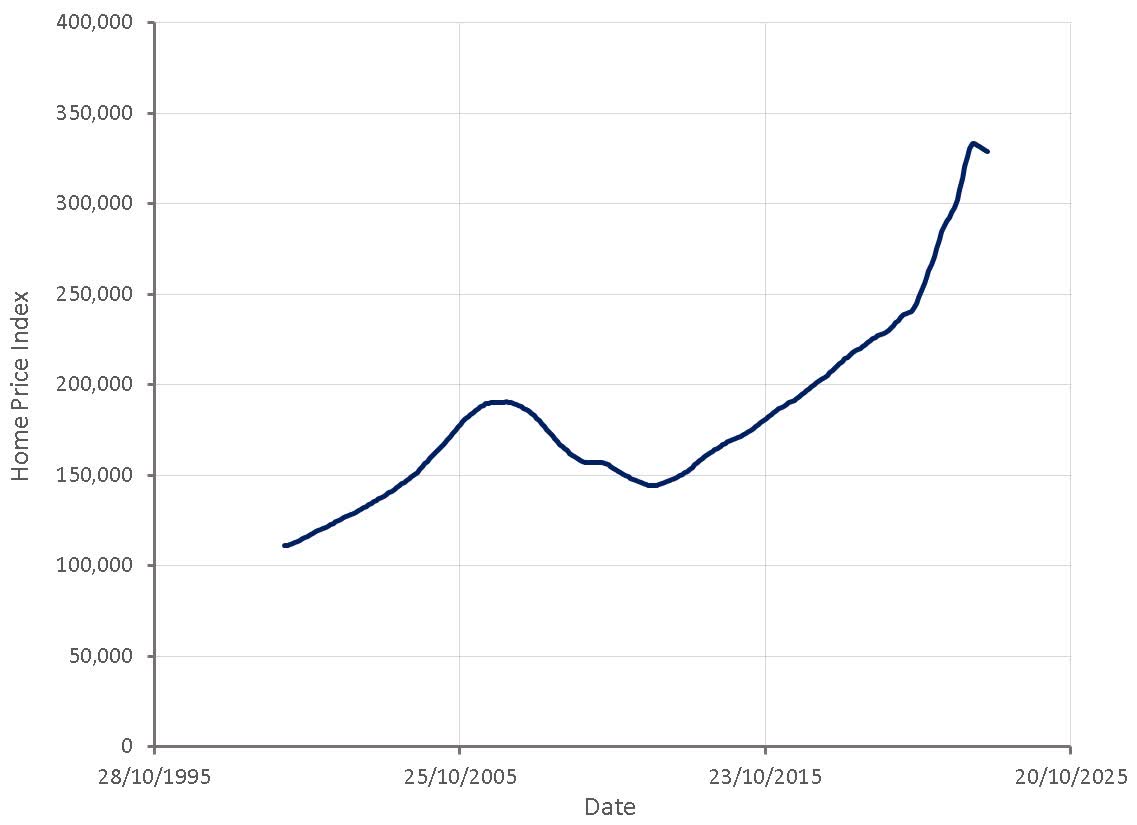

Home prices have been declining slowly but still remain elevated. Any easing of home prices or rents will not have an impact on inflation data in the short term though due to the way shelter inflation is calculated. There seems to be an expectation that the housing market will bounce back, supporting a strong economy, but this is unreasonable, as recent labor market and inflation data indicate that mortgage rates have little room to move downwards.

Figure 9: US Home Price Index (source: Created by author using data from Zillow)

{kind=link}

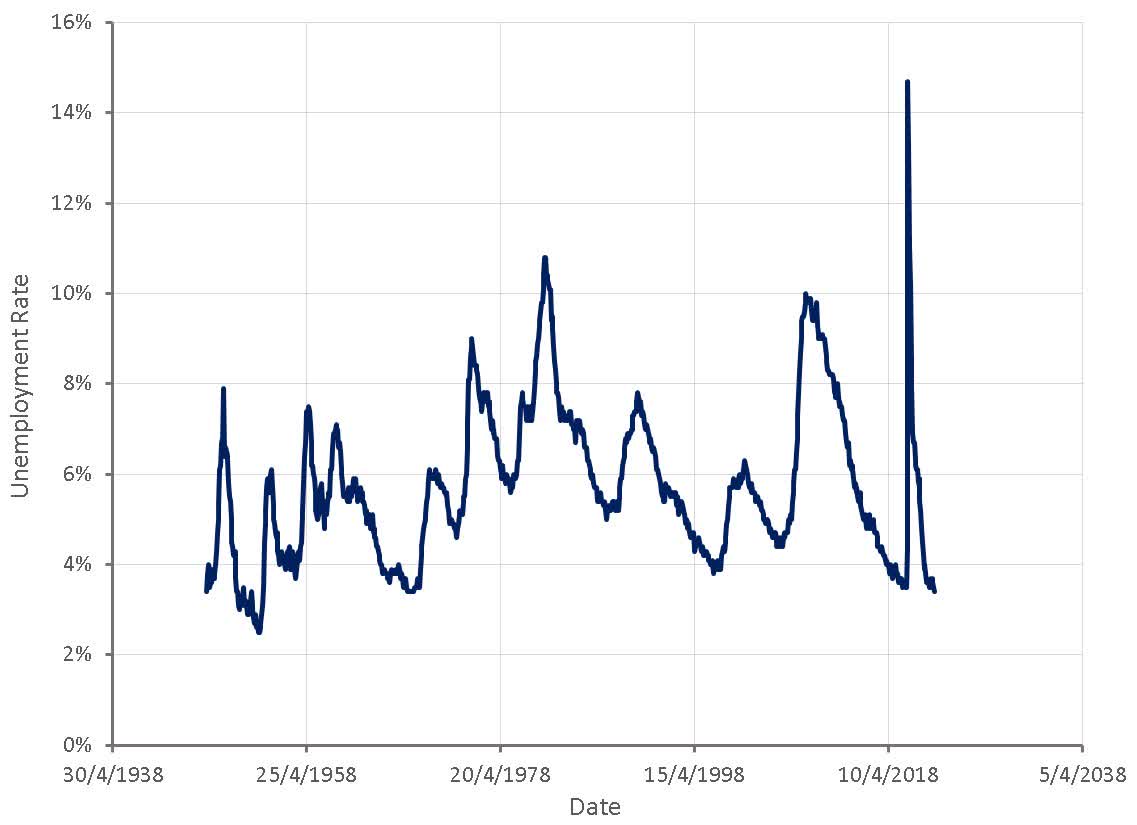

In addition to January's inflation data, strong labor market data from December will give the Fed the confidence to continue raising rates. Relatively strong economic data appears to be driving markets at the moment, rather than inflationary fears or the prospect of a weakening economy later in the year. It is hard to see the current move in equity markets being sustained though as incoming data is unlikely to support higher prices.

Figure 10: Unemployment Rate (source: Created by author using data from The Federal Reserve)

{kind=link}

For further details see:

Inflation Rebound Doesn't Change The Big Picture