PLW - Inflation Remains High Enough To Keep The Fed On Guard

2023-06-14 06:40:00 ET

Summary

- The pandemic may be over, but the aftershocks it created are still with us and have caused persistence in inflation.

- We believe the factors driving recent higher inflation reports are now receding, and we expect disinflation to resume this summer.

- We expect the Federal Reserve (Fed) to keep rates on hold for the rest of the year until there are clear signs of progress toward its inflation target.

By Turgut Kisinbay, Chief US Economist, Invesco Fixed Income

Earlier this year, we at Invesco Fixed Income expected US inflation to rise temporarily in the first half of the year. This was partly due to a resilient US economy that has been able to maintain steady spending power. But we expected most of the impetus to come from remaining economic imbalances, originally triggered by the pandemic. The pandemic may be over, but the aftershocks it created are still with us, and have caused persistence in inflation.

We believe the factors driving recent higher inflation reports are now receding and we expect disinflation to resume this summer. We believe there is a path to around 3% inflation, but going below that may prove difficult for some time. For the Federal Reserve (Fed) — which will be closely watched at its next meeting June 13-14 — that likely means staying on course and keeping rates elevated until there are clear signs of progress toward the target. We expect the Fed to keep rates on hold for the rest of this year.

Why has inflation been higher in the first half of the year?

After a few months of promising inflation numbers late last year, monthly core inflation picked up momentum in the winter. A number of factors explain much of the uptick in inflation, namely, the pent-up demand for cars and travel, and the persistence in shelter inflation in official measures.

Car prices likely stabilizing

US car prices, new and used, rose substantially in the last two years because of supply shortages. Now we believe we are nearing the end of this imbalance and expect car prices to stabilize and fall in the coming months.

New car prices increased by as much as 14% at their peak in 2022, and used car prices rose by just over 40%. 1 Given the auto sector’s large share in the Consumer Price Index ((CPI)), it has been a major contributor to overall inflation. Despite improvements in global supply chains and auto production, the supply-demand imbalance in the sector hasn’t yet been fully resolved, leading to ongoing price increases until recently. Before the pandemic, US new car sales averaged around 17 million cars per year. 2 Auto sales declined to just over 13 million units last summer and have remained below 15 million units in the last six months on an annualized basis. 3

Going forward, we expect car prices to stabilize and decline. Pent-up demand should gradually be met with improving supply. Meanwhile high interest rates and slowing nominal income growth are becoming headwinds to demand. Finally, we have supportive evidence on disinflation from used car auctions that typically lead the retail market by two to three months. Used car prices consistently rose in auctions earlier this year, but they have come down by more than 5% in the last two months. 4

Travel prices are leveling off

Travel is another sector where we have seen pent-up demand because of the pandemic. After two years of restricted and risky travel, the world started to open up last year after the Omicron wave. It was a “boomy” travel season, and airfare inflation shot up to over 40%, with hotels prices rising sharply too, by about 29% as of last September. 5

Travel inflation has declined significantly since then, but we are currently experiencing another strong travel season, although perhaps not as buoyant as last year. Not surprisingly, both airline and hotel prices have risen sharply since the winter when many bookings and purchases are made for summer travel. We expect this demand to fizzle and turn to disinflation in the coming months, as travel patterns normalize and excess savings decline.

Housing inflation may have peaked

Finally, shelter inflation likely peaked recently, and should begin to converge toward historical norms. It is well understood that official CPI data follow private sector rent data with a substantial lag of roughly a year. Private rent inflation for new leases declined to historical norms last fall and, by some measures, it has been tracking below historical norms.

Our inflation models that rely on macro variables and private sector rents suggest that the peak in year-over-year shelter inflation occurred in April at around 8.1%. Our models suggest it should slow to below 6% by the end of the year. It is important to note that shelter inflation’s weight in core inflation is around one-third, so a decline would likely make a major impact on the overall inflation outlook.

Recent US inflation readings have been promising

The April inflation report was promising and in line with our baseline expectations. Monthly core CPI inflation was high at 0.41%, as expected, but about one-third of that increase was due to used car prices, which we expect to decline in a few months. Regarding shelter, monthly inflation has averaged 0.5% over the past few months, a decline from 0.7% over the prior six months and in line with our models. Finally, travel related inflation was below our expectations, partly due to seasonal adjustments, and we continue to expect inflation to persist in this sector for a bit longer.

Overall, the latest inflation report was broadly in line, if not slightly better, than our baseline forecast, giving us confidence in our forecast of resumed disinflation going forward, with declines in core annual inflation to around 2.8% in a year from now.

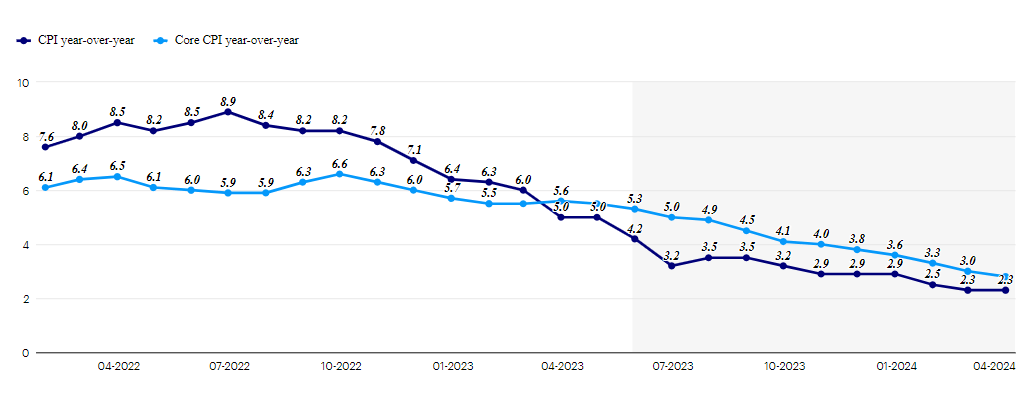

US CPI inflation projections

Source: Bureau of Labor Statistics, Invesco. Data from Jan. 31, 2022 to April 30, 2023. Invesco forecasts thereafter. There is no guarantee that forecasts will come to pass.

{kind=link}

Risks and the Fed

The remaining piece of the puzzle is non-shelter core services inflation that the Fed highlights in its communications. Those sectors are wage sensitive and the tight labor market poses risks to disinflation. Wages were on a declining trend last year but gained momentum in the first quarter of this year. There were one-off adjustments early in the year, such as cost-of-of living adjustments because of high inflation last year. Those are unlikely to be repeated in the coming months, and we expect wage inflation should decline.

On the other hand, health care inflation in CPI is backward-looking and is expected to rise in the fall, limiting the scope for disinflation. As stated earlier, we believe there is a path to around 3% inflation, and we expect the Fed to keep rates on hold for the rest of this year, until clear signs of progress toward that target emerge.

Footnotes

1 Source: Bureau of Labor Statistics. Data as of May 10, 2023.

2 Source: Ward’s Automotive Group. Data as of May 2, 2023.

3 Source: Ward's Automotive Group. Data as of May 2, 2023.

4 Source: Manheim Auctions. May preliminary data. Data as of May 17, 2023.

5 Source: Bureau of Labor Statistics. Data as of May 10, 2023.

Important information

NA2943544

Past performance is not a guarantee of future results.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial professional before making any investment decisions.

All investing involves risk, including the risk of loss.

An investment cannot be made directly in an index.

The Consumer Price Index ((CPI)) measures change in consumer prices as determined by the US Bureau of Labor Statistics. Core CPI excludes food and energy prices while headline CPI includes them.

The opinions referenced above are those of the author as of June 7, 2023 . These comments should not be construed as recommendations, but as an illustration of broader themes. Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions; there can be no assurance that actual results will not differ materially from expectations.

©2023 Invesco Ltd. All rights reserved

Inflation remains high enough to keep the Fed on guard by Invesco US.

For further details see:

Inflation Remains High Enough To Keep The Fed On Guard