INFA - Informatica: 3Q23 Results Will Determine If One Should Size Up

2023-08-13 12:24:54 ET

Summary

- INFA's 2Q23 results demonstrated strong cloud performance, with Cloud ARR growth of 37%, exceeding management guidance by 200bps.

- Cloud ARR growth has slowed but still exceeds management guidance, with a smooth shift from self-managed to cloud subscriptions.

- I recommend to maintain a small investment position in INFA while awaiting the 3Q23 results to assess the strength of the cloud transition and to observe more positive market sentiment.

Overview

My recommendation for Informatica ( INFA ) is to continue holding a small stake as I await INFA’s 3Q23 results to ascertain the strength in cloud and also for the headline to turn more positive. Note that I previously recommended holding a small stake in INFA as I was positive about the long-term aspect of the business but worried about the fact that migration remained weak in 1Q23.

Recent results & updates

INFA reported good 2Q23 results that beat consensus estimates and, along with the profit outlook, led to a share jump of more than 10%. In this aspect, I believe the choice of holding a small stake has worked out well.

As I've already mentioned, I was worried about cloud performance, but INFA hasn't let me down so far this quarter. Although the growth rate of Cloud ARR has slowed from 41% in 1Q23 to 37% in 2Q23, I still consider this to be an excellent achievement, as it exceeds management guidance by 200bps. In addition, INFA's net-new cloud ARR was stable at $29 million compared to the $30 million it was in 2Q22. Most importantly, the shift from self-managed to cloud subscription sales is progressing smoothly, with cloud accounting for 49% of subscription ARR, up from 42% a year ago. IPUs now account for 43% of Cloud Subscription ARR, an increase of 200 bps sequentially, as reported by management, further demonstrating the growing traction of the consumption-based model.

“In my opinion, pricing, and in particular the elasticity of consumption pricing based on IPU licensing, will become just as important as the functional value proposition.” Creative Capital

Overall, INFA's total ARR grew by 8% y/y, slowing slightly from 10% growth in the previous quarter as slower self-managed ARR growth and a decline in maintenance ARR offset faster cloud growth. I believe the focus shouldn’t be on the deceleration vs. 1Q23; in fact, I believe the takeaway should be that the migration is going well. More users are adopting the cloud (hence the decline in self-managed ARR), which has a much better CLTV.

Moving forward, I support management's choice to maintain their guided revenue level even though the macro situation is stable so far in July. This approach has effectively curtailed a certain degree of risk for the latter half of 2023, concerning performance expectations. While the forecasted revenue figure remains unaltered, management has, however, adjusted the anticipated operating margin upwards. This adjustment stems from their ongoing positive assessment of the impact resulting from the earlier implemented RIF, alongside the incorporation of specific additional measures aimed at enhancing cost efficiency. The way I see it, it appears that management has managed expectations in a way that if macro turns for the better, they have a good chance of beating guidance and consensus estimates.

Investors appear to be becoming more optimistic about INFA's cloud performance and the "meetable" guidance for 2H23, judging by the stock price reaction following the release of the results. Personally, I am also positive about INFA hitting its Cloud ARR target in FY23, and the decision to de-emphasize its self-managed consumption model in favor of its cloud-based consumption model should continue to drive faster growth potential within its installed base and improved operational efficiency. Nonetheless, I'd rather keep my investment position modest until 3Q23 results are released, after which I'll have a better idea of whether or not the shift to the Cloud is improving. I would also prefer to wait for headline deceleration figures to flip into "stable" or "acceleration" before sizing up, as that would drive more momentum at the stock level.

Valuation and risk

Author's valuation model

According to my model, INFA is valued at $27.59 in FY24, representing a 37% increase. This target price is based on my growth forecast of high single digits over the next two years and FY23, following management guidance. INFA should have no issues meeting FY23 guidance given the strong performance so far and management comments of a stable July. My growth assumption of 8% is driven by my expectation that cloud growth will become more apparent as the migration completes.

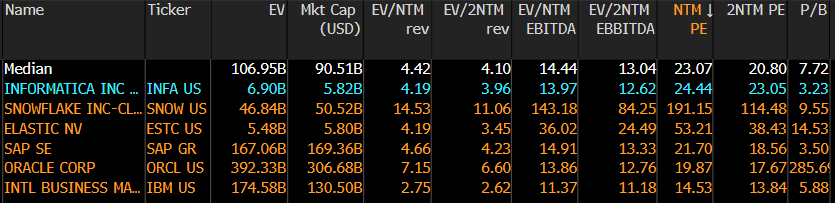

INFA is now trading at 24x forward PE, which I believe will be sustainable over the next two years as the market gradually recognizes INFA's cloud growth potential. Given the lack of a large comp set, I compared INFA to peers that have a competing product. INFA has historically traded at a 10% premium to peers, and that premium took a dive to a discount when the market punished INFA's 1Q23 results (due to the cloud migration weakness). As 2Q23 shows that migration remains healthy and is going in the right direction, INFA has resumed trading at a premium.

{kind=link}

Summary

My recommendation for INFA is to continue holding a small stake while awaiting the 3Q23 results to gauge cloud strength and observe a more positive market sentiment. Despite a slight slowdown in Cloud ARR growth, the progress from self-managed to cloud subscriptions, and the traction of the consumption-based model are noteworthy.

For further details see:

Informatica: 3Q23 Results Will Determine If One Should Size Up