INFA - Informatica Is Cautious On 2023 As Uncertain Macro Conditions Continue

2023-05-09 12:39:21 ET

Summary

- Informatica went public in October 2021, raising around $841 million in gross IPO proceeds.

- The company provides data integration and management software to organizations worldwide.

- INFA has produced uneven net results and is seeing lengthening sales cycles.

- I believe we are in the midst of a macroeconomic slowdown further worsened by reduced lending from U.S. banks in the wake of recent high profile bank failures.

- I'm therefore Neutral [Hold] on INFA for the near term.

A Quick Take On Informatica

Informatica ( INFA ) went public in October 2021, raising approximately $841 million in gross proceeds from an IPO that was priced at $29.00 per share.

The firm provides software for data integration and management functions in organizations worldwide.

The macroeconomic slowdown that I believe we are experiencing, as well as reduced lending activity, doesn’t bode well for customer buying decision-making.

As such, I’m Neutral [Hold] on INFA for the near term.

Informatica Overview

Redwood City, California-based Informatica was founded first to provide on-premises data integration and management solutions and has since completed a transformation into a cloud-based SaaS company.

Management is headed by Chief Executive Officer Amit Walia, who has been with the firm since October 2013 and was previously an executive at Symantec and at McKinsey & Company.

The company’s primary offerings include:

-

Data integration

-

API & Application integration

-

Data quality

-

Master data management

-

Customer & Business 360

-

Data catalog

-

Governance and privacy

The company markets its offerings via a direct sales team and through strategic partners, which include cloud hyperscalers, global system integrators, resellers and cloud data platforms.

Informatica’s Market & Competition

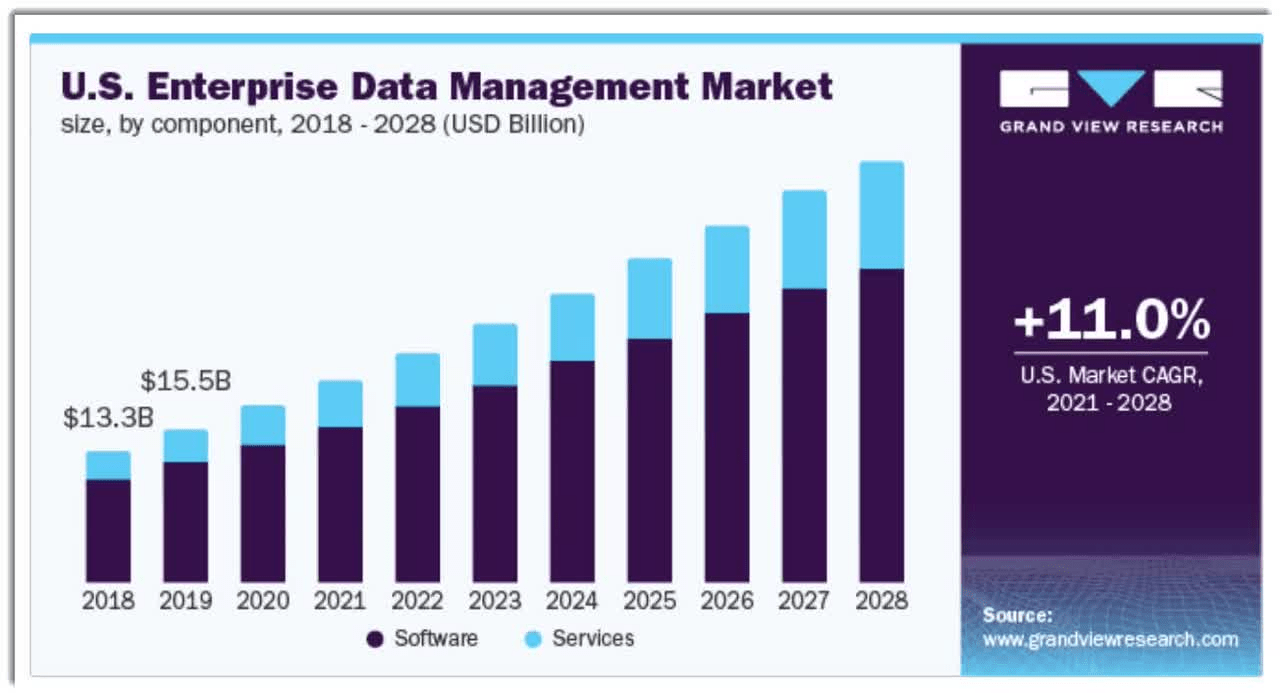

According to a 2021 market research report by Grand View Research, the global market for enterprise data management was an estimated $72.8 billion in 2020 and is forecast to reach $204 billion by 2028.

This represents a forecast CAGR (Compound Annual Growth Rate) of 13.8% from 2021 to 2028.

The main drivers for this expected growth are the outbreak of the global pandemic, increasing demand from off-premises locations and increasing need for real-time information from across the enterprise.

Also, below is a chart showing the historical and projected future market trajectory for the U.S. enterprise data management market:

{kind=link}

Major competitive or other industry participants include:

-

Talend

-

Collibra

-

AWS (AMZN)

-

Microsoft (MSFT)

-

Google (GOOG)

-

IBM (IBM)

-

Oracle (ORCL)

-

Cloudera

-

SAP (SAP)

-

Broadcom (AVGO)

-

Teradata (TDC)

-

Micro Focus (MCFUF)

-

Mindtree

-

Others

INFA’s Recent Financial Trends

-

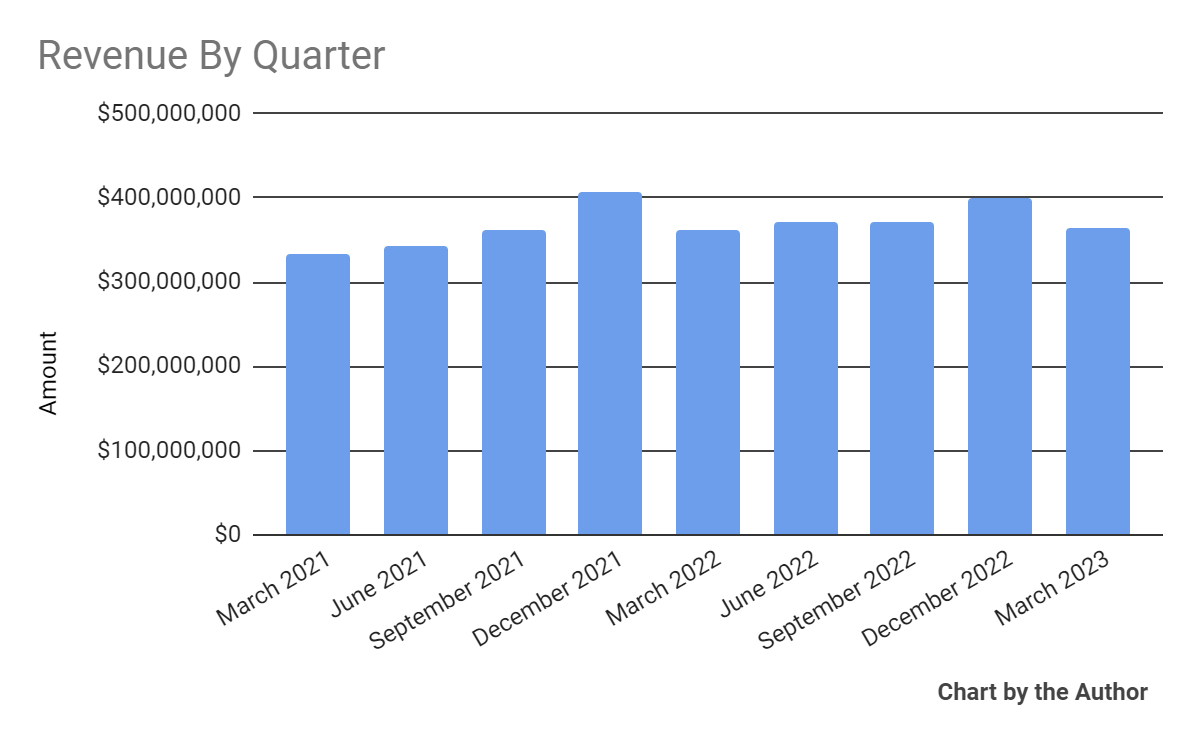

Total revenue by quarter has plateaued in recent quarters:

{kind=link}

-

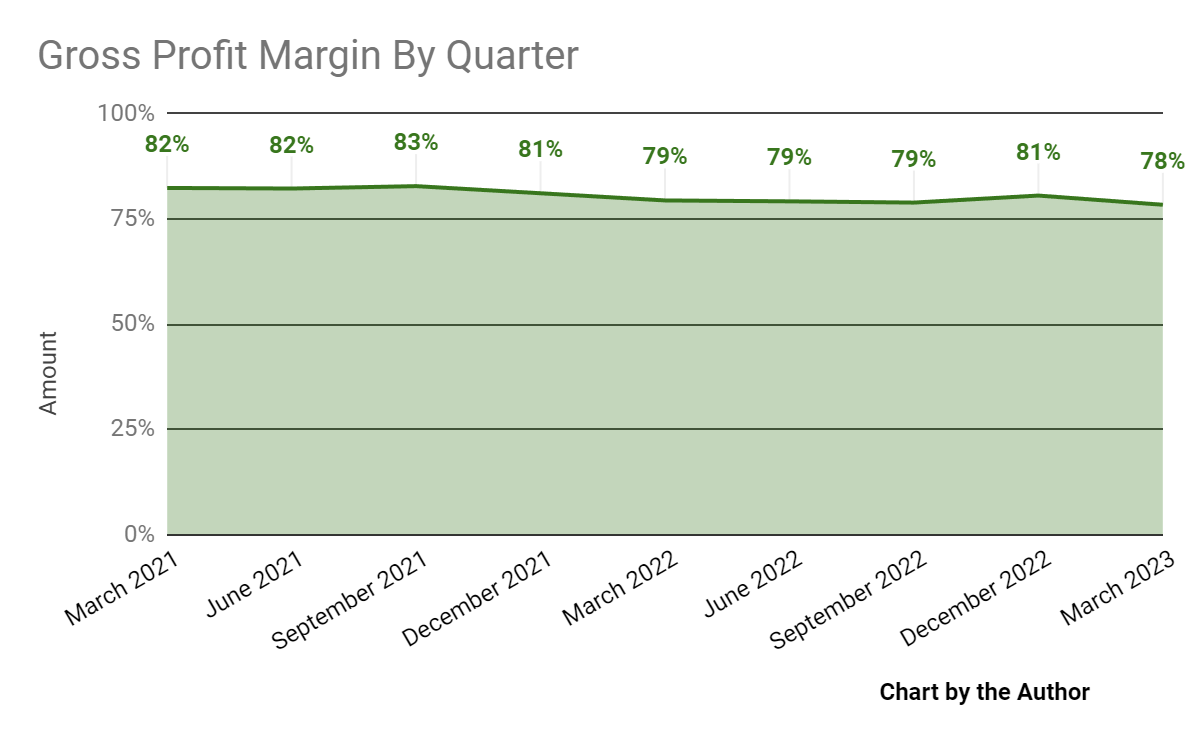

Gross profit margin by quarter has trended lower recently:

{kind=link}

-

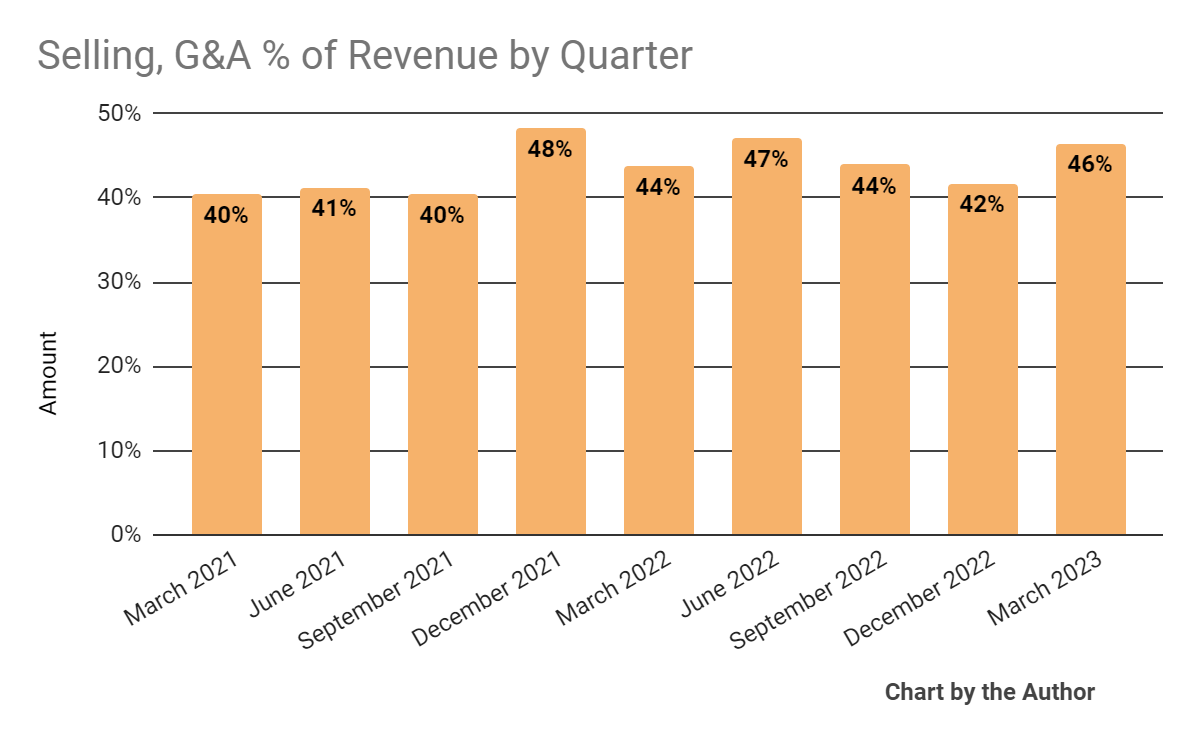

Selling, G&A expenses as a percentage of total revenue by quarter have fluctuated within a range:

{kind=link}

-

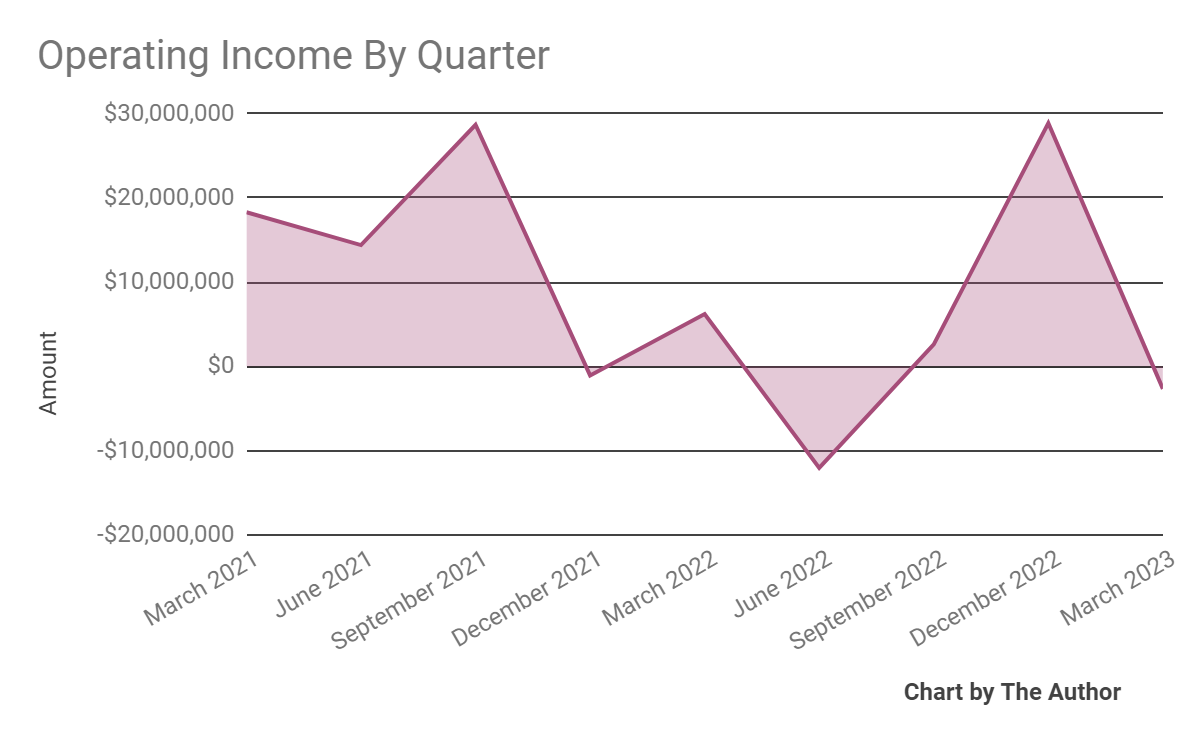

Operating income by quarter has varied materially in recent quarters:

{kind=link}

-

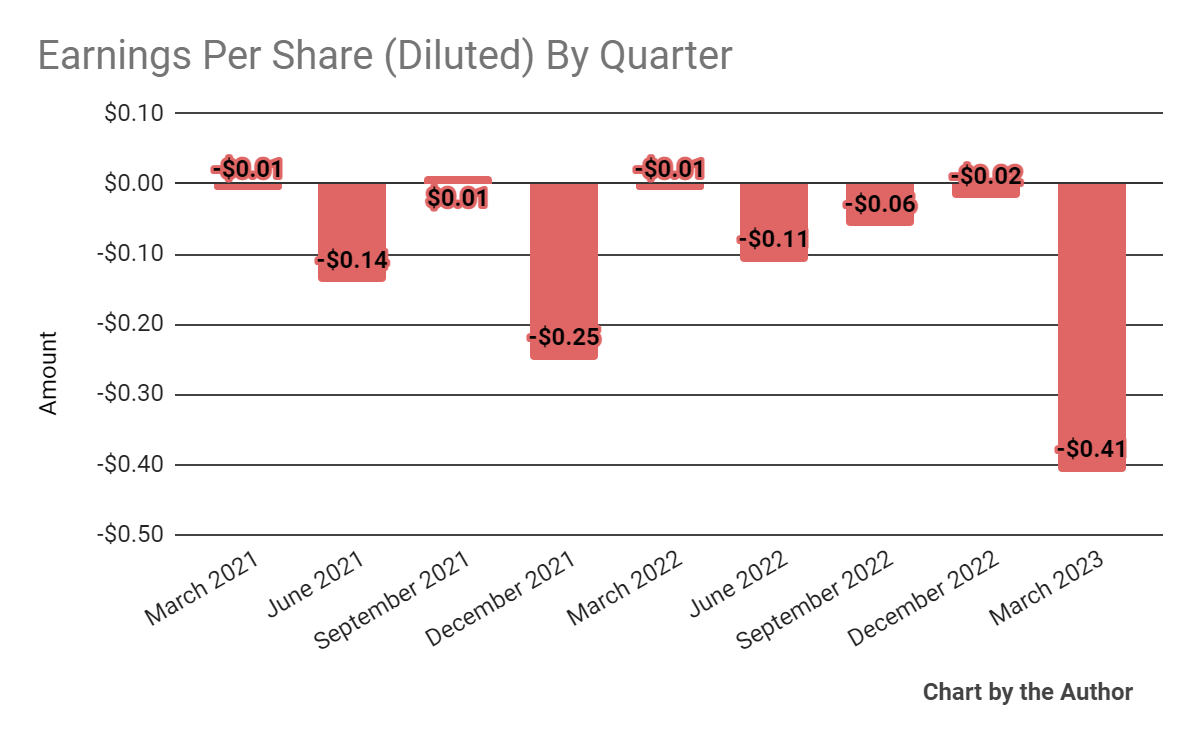

Earnings per share (Diluted) have dropped sharply into negative territory recently:

{kind=link}

(All data in the above charts is GAAP)

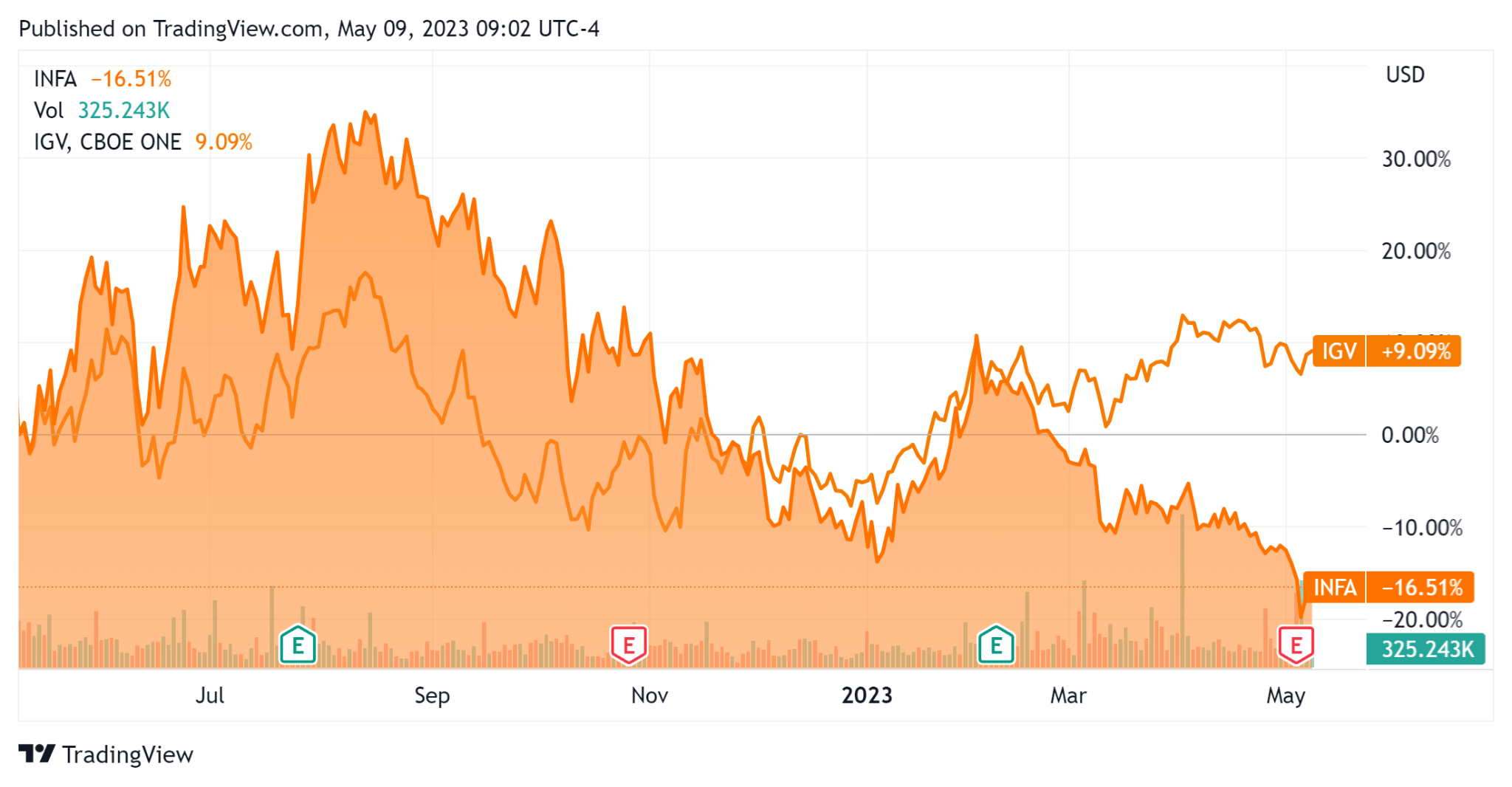

In the past 12 months, INFA’s stock price has fallen 16.51% vs. that of the iShares Expanded Tech-Software Sector ETF’s ( IGV ) rise of 9.09%, as the chart indicates below:

{kind=link}

For the balance sheet, the firm ended the quarter with $798 million in cash, equivalents and short-term investments and $1.84 billion in total debt, of which $18.8 million was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash flow was an impressive $193.8 million, of which capital expenditures accounted for only $6.0 million. The company paid a whopping $156.9 million in stock-based compensation in the last four quarters, the highest in the last eleven-quarter period.

Valuation And Other Metrics For Informatica

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 3.5 |

| Enterprise Value / EBITDA |

| 28.4 |

| Price / Sales |

| 2.7 |

| Revenue Growth Rate |

| 2.4% |

| Net Income Margin |

| -11.1% |

| EBITDA % |

| 12.3% |

| Market Capitalization |

| $4,150,000,000 |

| Enterprise Value |

| $5,260,000,000 |

| Operating Cash Flow |

| $199,780,000 |

| Earnings Per Share (Fully Diluted) |

| -$0.60 |

(Source - Seeking Alpha)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

INFA’s most recent Rule of 40 calculation was 14.7% as of Q1 2023’s results, so the firm is in need of substantial improvement in this regard and has produced worsening results in recent periods, per the table below:

| Rule of 40 Performance |

| Calculation |

| Recent Rev. Growth % |

| 2.4% |

| EBITDA % |

| 12.3% |

| Total |

| 14.7% |

(Source - Seeking Alpha)

Commentary On Informatica

In its last earnings call (Source - Seeking Alpha), covering Q1 2023’s results, management highlighted subscription ARR (Annual Recurring Revenue) growth of 20% year-over-year and cloud subscription ARR growing 41%.

Notably, 90% of new cloud bookings were the result of ‘new workloads’, rather than just transferring existing on-premises workloads.

Management expects to use its strong free cash flow to reduce its net debt leverage ratio to 2x by the end of 2023, or possibly six to twelve months ahead of its pre-IPO estimate.

However, the company continues to see longer sales cycles as customers exert greater scrutiny over spending and management thinks this will continue throughout 2023.

The company’s overall subscription net retention rate was 110% and its cloud retention rate was 118%, indicating pretty good product/market fit and sales & marketing efficiency.

Total revenue for Q1 rose only 0.9% year-over-year and gross profit margin fell one percentage point to 78%.

SG&A as a percentage of revenue increased two percentage points, a negative signal indicating higher costs for each additional dollar of revenue and operating income turned negative.

Looking ahead, management reiterated its previous guidance of 2023 full-year revenue growth of 5% at the midpoint of the range and non-GAAP operating income of $410 million at the midpoint.

Notably, cash paid for interest for full-year 2023 is expected to be $145 million.

The company's financial position is moderate, with a significant debt load that management is trying to reduce with its strong cash flow.

Regarding valuation, the market is valuing INFA at an EV/Sales multiple of around 3.5x.

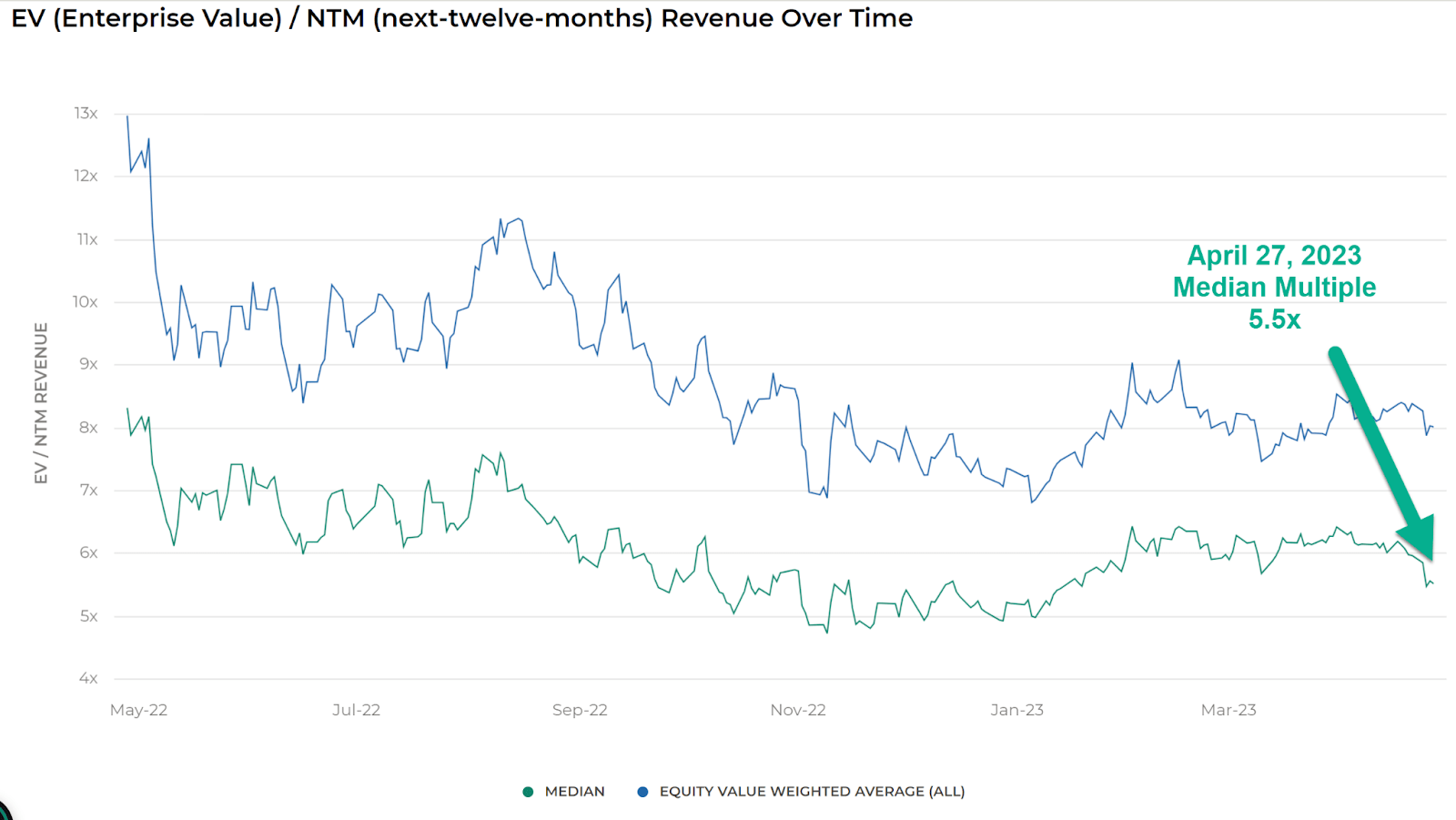

The Meritech Capital Index of publicly held SaaS software companies showed an average forward EV/Revenue multiple of around 5.5x on April 27, 2023, as the chart shows here:

{kind=link}

So, by comparison, INFA is currently valued by the market at a discount to the broader Meritech Capital SaaS Index, at least as of April 27, 2023.

The primary risk to the company’s outlook is a macroeconomic slowdown that appears to be already underway, tightening credit conditions which may delay customer spending plans and lengthening slower sales cycles which may reduce its revenue growth trajectory.

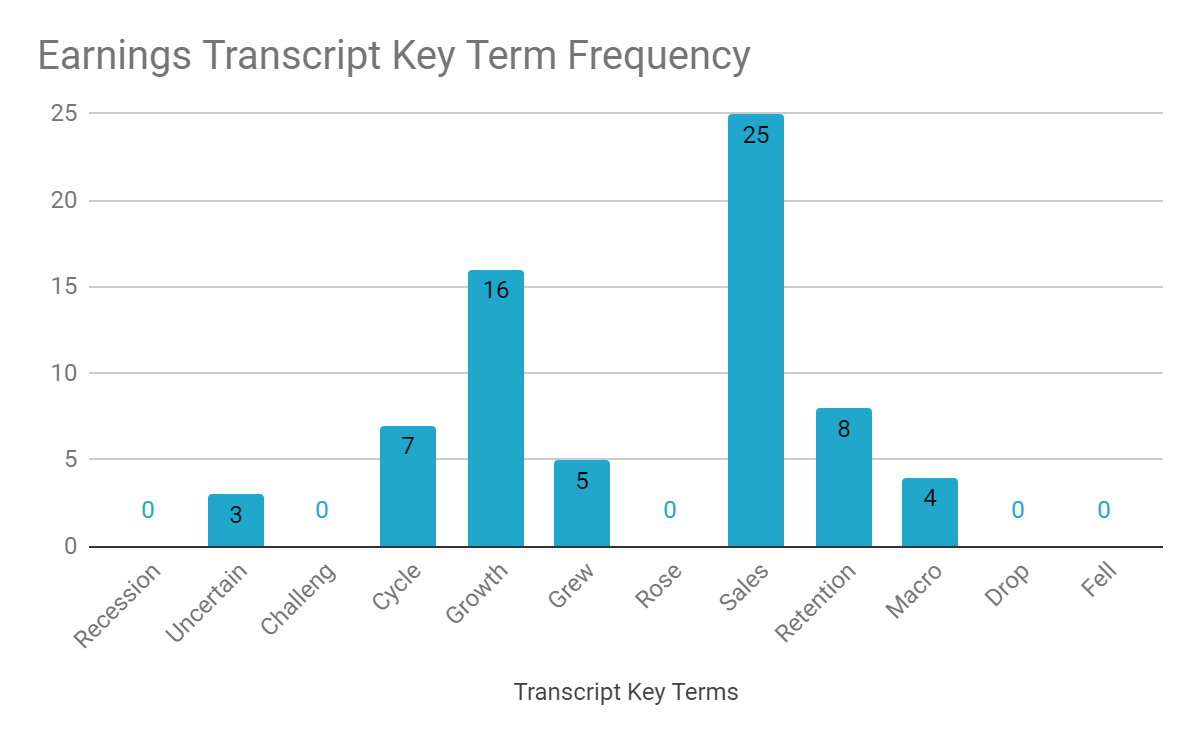

From management’s most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below:

{kind=link}

I’m most interested in the frequency of potentially negative terms, so management cited ‘Uncertain’ three times and ‘Macro’ four times in various contexts, indicating their hesitancy in forward guidance.

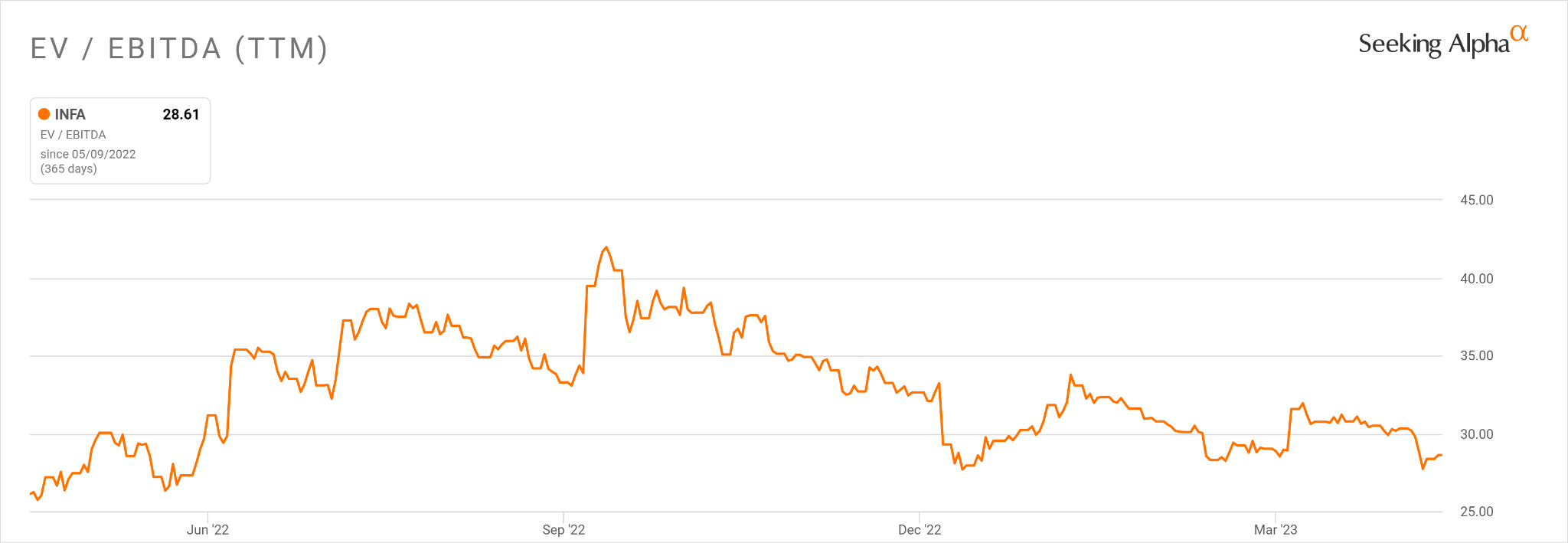

In the past twelve months, the firm's EV/EBITDA valuation multiple has risen about 10%, as the chart from Seeking Alpha shows below:

{kind=link}

A potential upside catalyst to the stock could include a pause in U.S. interest rate hikes, reducing downward pressure on its valuation multiples and foreign exchange headwinds if the US dollar dropped as a result.

However, the macroeconomic slowdown that I believe we are experiencing, as well as reduced lending activity, doesn’t bode well for customer buying decision-making.

As such, I’m Neutral [Hold] on INFA for the near term.

For further details see:

Informatica Is Cautious On 2023 As Uncertain Macro Conditions Continue