INFA - Informatica: Severely Undervalued Despite Winning The Cloud Transition Journey

2024-01-09 09:36:29 ET

Summary

- Informatica is undergoing a successful business transformation and has strong growth prospects, with the potential for at least a 30% upside in its stock.

- The company competes in the data management space and maintains platform relationships with large cloud enterprises, positioning it well in a hybrid cloud environment.

- Informatica commands a leadership position in the data management industry, as recognized by Gartner's Magic Quadrant report.

Investment Thesis

Informatica ( INFA ) is not the first name that comes to mind when someone asks me about hot tech stocks to invest in. The company debuted on the stock market in 2021 but is not new to being publicly traded. In another life, Informatica was a public company before being taken private in 2015 . It faced struggles with its business transformation, and investors at the time seemed to have lost patience with Informatica.

However, with Informatica being given a second life after its IPO in 2021, I believe Informatica's business transformation is well underway, and I see some strong prospects for buying Informatica's stock. The company's growth metrics are on track to grow higher in terms of its Annualized Recurring revenue ((ARR)). With expanding margins complementing the growth reversals in the stock, I see strong potential for at least a 30% upside in this stock.

About Informatica

Informatica is a software-based company that focuses on delivering data management and data integration tools for enterprises whose businesses are driven by data. The company is based out of Redwood City, CA, and was founded in February 1993 to initially distribute its data management tools via the on-premise, software-license model. Its popularity would rise over the next decade and a half as more business models went online and data harvesting became a necessity.

However, the advent of cloud computing severely dented its growth prospects, and Informatica completely missed the transition trend of software models from on-premise, license-based to subscription-based and was taken private in 2015, giving the executives time to turn the company around.

As per its most recent FY23-Q3 quarter , the company makes over 64% of its revenue from software subscriptions, while the remainder comes from a combination of maintenance service and perpetual license revenue.

By operating in the data management space, it competes directly with other vendors such as Confluent ( CFLT ) and Palantir ( PLTR ), while also facing threats from tools in the open-source software complex popular amongst today's cohort of data executives, such as Python and Airflow .

Further, while Informatica does not directly compete with other large enterprises such as Amazon ( AMZN ), Google ( GOOG ), Microsoft ( MSFT ), and Snowflake ( SNOW ), it does maintain platform relationships with these large enterprises, which I believe is a win for the company in a hybrid cloud environment. I will explain these relationships in further detail in the sections below.

Informatica Still Commands a Leadership Position in the Data Management Industry

According to the most recent Data Integration Magic Quadrant report by technology research giant Gartner, Informatica is still recognized as a leader in the data integration and data management tools market. I have attached Gartner's Magic Quadrant below, which breaks out all software tools into four quadrants based on the company's ability to execute vs. the completeness of its vision. The company was also previously named a leader in 2022 .

2023 Gartner® Magic Quadrant™ for Data Integration Tools

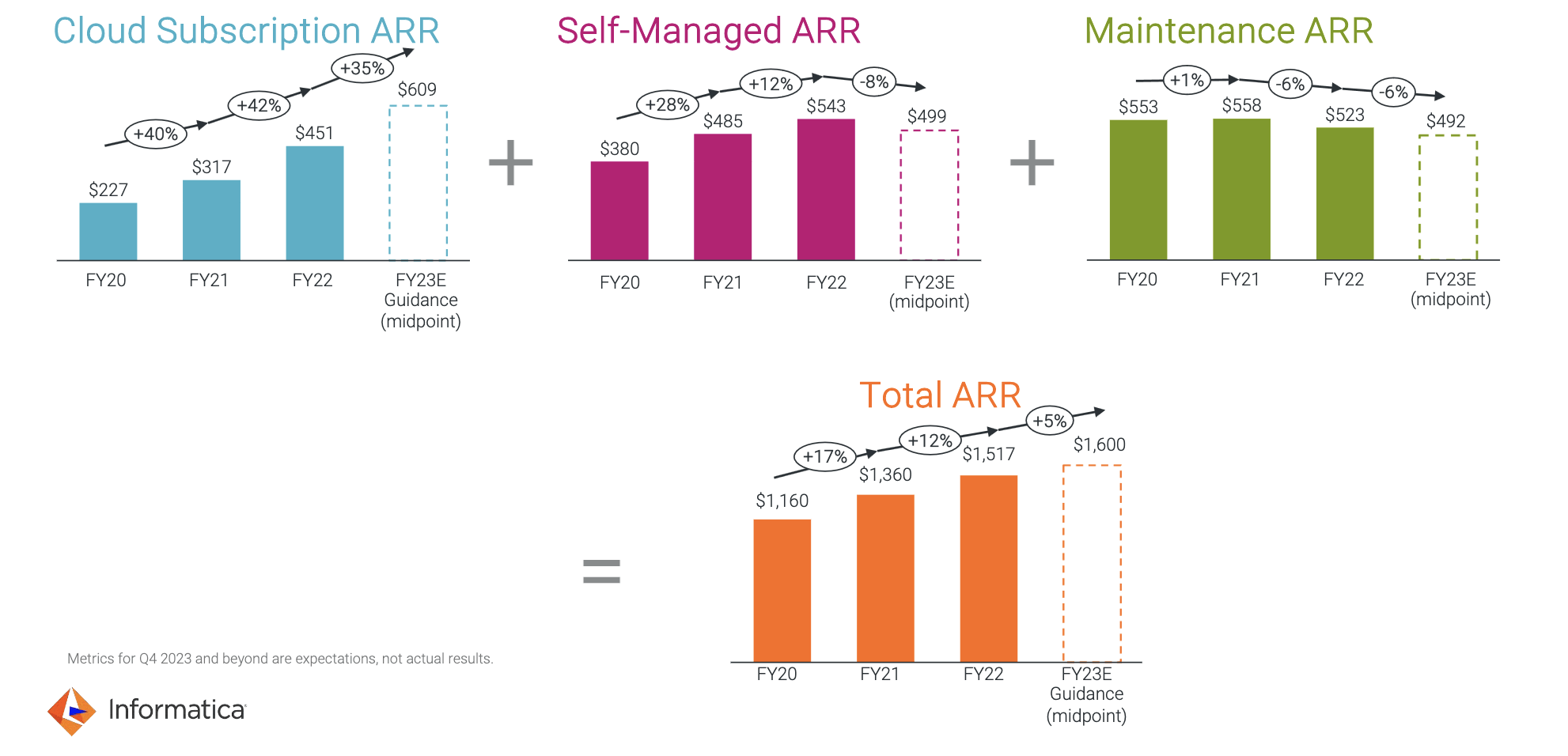

In the previous section, I pointed out how Informatica has strategically built partnerships with large hyperscalers such as Microsoft and Google to help their clients integrate and manage data in the cloud. My firm belief is that by leveraging relationships with cloud computing giants, Informatica has created an ecosystem that will keep feeding into its top line since most cloud computing contracts are generally multi-year. In 2022, Informatica expanded its partnership with data management leader Snowflake to help Snowflake's clients integrate data into their data clouds on Snowflake's servers. In my opinion, such partnerships with cloud enterprises are cleverly designed by Informatica to complete its transition to a cloud-based subscription-driven company. I have attached a slide from their most recent Investor Day last month that shows the cloud ARR continues to grow and lift the entire ARR despite its legacy revenue streams slowing down.

Informatica, 2023 Investor Day

{kind=link}

In addition, Informatica swiftly released their own ClaireGPT and AI tools last year that are designed to increase productivity for data engineers, a core user base for Informatica. Per Informatica's FY23-Q3 prepared remarks , management announced that their AI tools are already embedded into all of Informatica's solutions. This is very important for further solidifying Informatica's market share, according to me, especially given that Gartner projects data integration companies to lose 50% market share by 2025 if data vendors fail to add AI capabilities to their data integration solutions. I see Informatica's rapid expansion of AI and ML capabilities into its data tools as a huge step in solidifying its market share and expanding TAM.

Valuation Suggests Informatica is Positioned for 32% Upside

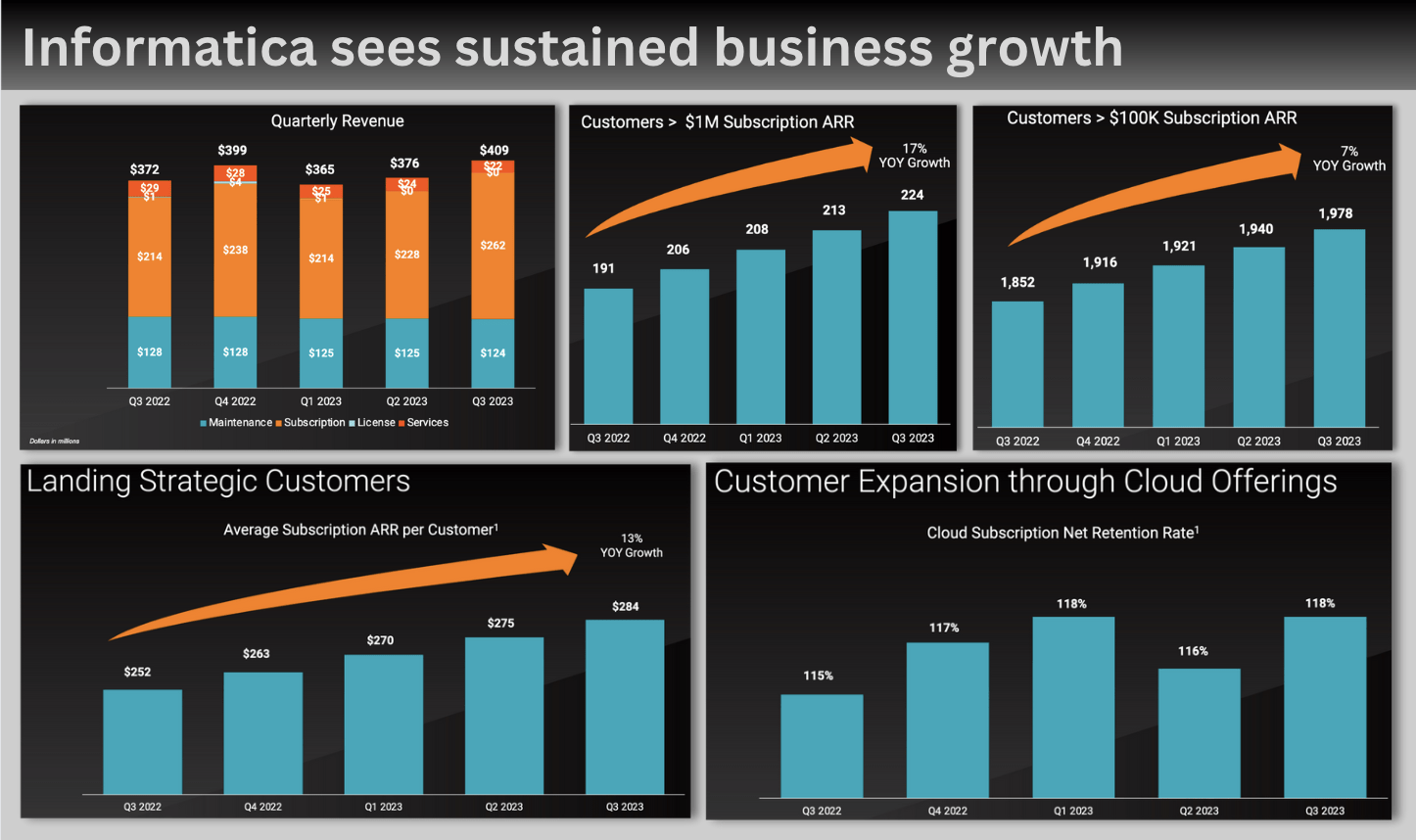

According to their FY23-Q3 earnings, Informatica is seeing some secular trends build into its business. I have added a dashboard below based on its latest Q3 earnings report of some metrics that are crucial in highlighting Informatica's progress.

Informatica, 2023 Q3 Earnings Report

{kind=link}

From the earnings, two metrics stood out to me when analyzing Informatica's business operations. First, despite slowdowns in its legacy business segments, such as on-premise software and maintenance software, its quarterly revenue growth is being driven by the strength of its subscriptions. The key driver in its subscription business is its cloud revenue, which, as I pointed out earlier, accounts for over 64% of the revenue. This is very important given that 10 years ago, at the time of being taken private, the company struggled to transition into a subscription-based business. More importantly, most of that growth is being driven by sustained spending by its large customers, with greater than $1 million growing 17% YoY. Even better, Informatica's cloud subscription NDR is 118%, which is impressive given that it is a late-stage, mature software company.

Turning to its financial metrics, I did see some potential issues in its books, namely its expense profile and its debt. While net debt was at $1.2 million, I expect management to work towards delevering to below two times by the end of the year. Informatica had a CFO transition early last year , and their new CFO has reaffirmed their commitment to reducing debt and expenses. Attaching some of the CFO's comments below from the FY23-Q2 calls:

We expect the business to naturally delever to below two times by the end of 2023, which is six to 12 months ahead of our commitment at the time of the IPO.

On expenses, I believe management is also committed to reducing their expense profile. On the latest earnings call, management guided towards reducing their headcount by 10%. Given that management expects to save approximately $84M by next year by incurring $45M in restructuring expenses, the company will reduce its operating expenses by approximately 4%. I expect them to announce more cost-effective initiatives over the course of the next few quarters to guide the company towards its FY26 Non-GAAP operating margin target of 35%.

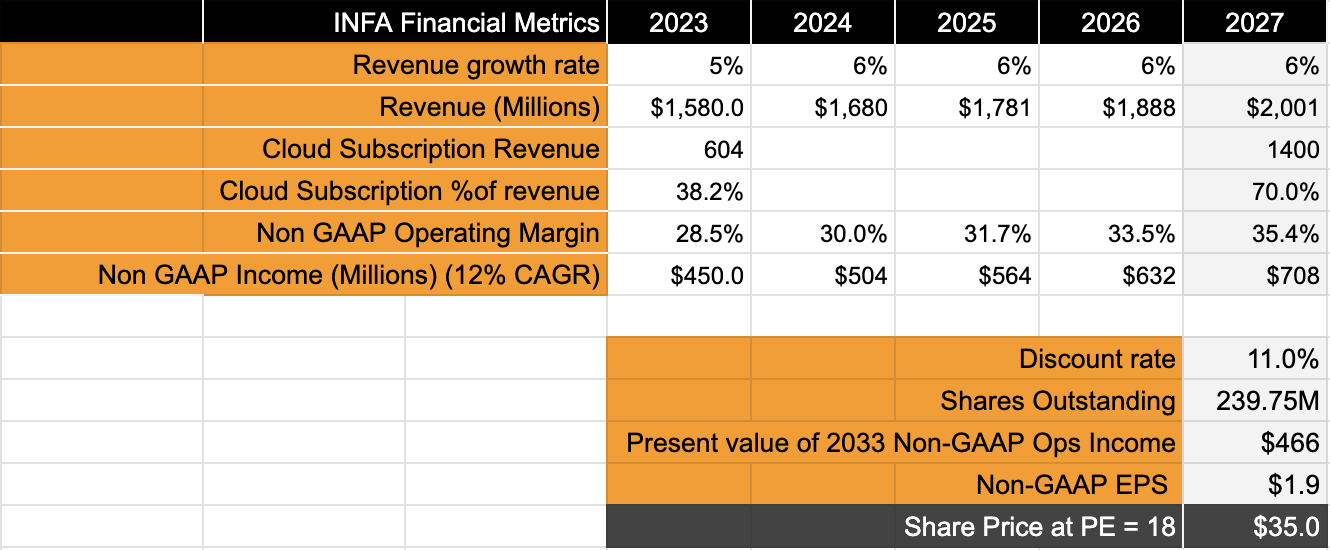

Finally, in terms of valuing the company, I have assumed a higher discount rate of 11%, given certain risks that I outlined earlier. According to the company's own projections, as stated in the Investor Day in Dec 2023, since management expects to grow total ARR to $2 million in 2026, I have assumed a 6% y/y average annual growth.

{kind=link}

Management expects non-GAAP operating income to grow at a 12% CAGR until 2026. Taking into consideration that S&P trades at a 10Yr average of 18, according to FactSet , I estimate Informatica's shares to be valued at $35, giving it a 32% potential upside.

Risks

Informatica's biggest risks come from its failure to innovate and maintain a steady roadmap of products and features that underserve their clients' expectations. So far, Informatica has proven to be operating and innovating at speed by releasing its ClaireGPT and AI tools, making it a consistent leader in Gartner's Magic Quadrant. However, should it fail to innovate, it can run severe risks of lower adoption and customers moving to competing platforms.

Competition from vendors in the same space is also another threat to Informatica, which will risk the 6% revenue growth rate that I earlier projected. So far, Confluent has focused on customers with more than $100k in ARR, while Informatica has a stronger hold on customers with more than $1M in ARR. Meanwhile, Palantir's focus has mostly been on sovereign entities as its clients, allowing Informatica to further strengthen its market share over large enterprise clients. For now, it appears that each competitor's differentiated product strategy appeals to different segments of the target market, but were any of Informatica's competitors to successfully go after large clients, it would impact Informatica's ARR.

Conclusion

Informatica is showing immense progress in its transition into a cloud-software, subscription-based company. So far, management is moving with urgency towards innovating its way into solidifying its market leadership position in the data management space. Moreover, the company's strengthening financial position and expanding margins are putting it in a pole position to sustainably grow towards its target. Informatica is definitely undervalued today, in my opinion, and is a Buy.

For further details see:

Informatica: Severely Undervalued Despite Winning The Cloud Transition Journey