NLCP - Innovative Industrial Properties: I'm Not Falling For This 10% Dividend Yield

2023-07-10 11:48:48 ET

Summary

- IIPR is the largest cannabis REIT in the US.

- The company faces legislation as well as collection risks.

- The valuation is not particularly depressed and dividend safety is questionable.

Innovative Industrial Properties ( IIPR ) is the largest cannabis REIT in the US. The REIT owns a diversified portfolio of properties that cater to cannabis producers. The vast majority (91%) of their assets are industrial warehouses where cannabis is grown and processed, followed by retail at less 10%.

IIPR

Investing in the cannabis sector comes with its risks, most notably legislation, but with risk comes also potential reward. The industry is still in its early stages and the growth potential is definitely there. In fact, the industry is expected to grow by a double-digit CAGR for the rest of the decade, which will most definitely benefit owners of key infrastructure within the sector.

IIPR

IIPR is better positioned than some of its smaller competitors, such as NewLake Capital Partners ( NLCP ) because it’s larger, which means that it can spread its overhead expenses over a larger number of properties. In addition to this, the REIT also has some of the longest lease terms in the industry with a weighted average lease term of 15 years and essentially no lease expirations until 2029. This means that vacancy is not really a concern, unless a tenant goes out of business.

Notably, the REIT also has a very high portion of tenants with operations in multiple states (89% to be exact). This is great, because with cannabis there’s always a risk that any one state can change legislation. With operations diversified between multiple states, tenants and in turn also the landlord are better protected from this risk.

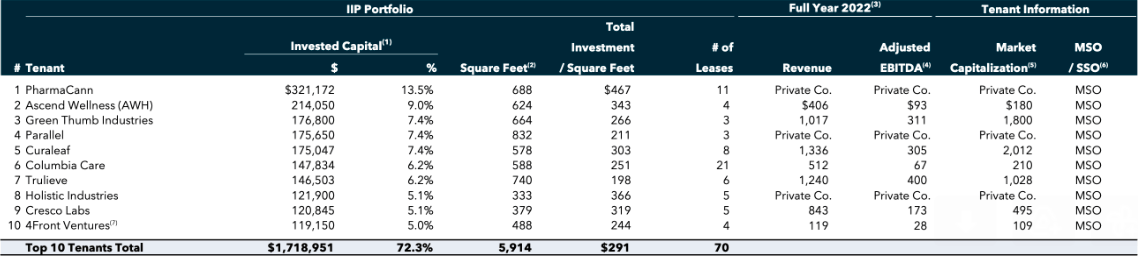

Just like NLCP, Innovative Industrial is heavily exposed towards just a few large tenants. In fact, top 10 largest tenants account for 72% of total rental income. This can be quite risky, especially in a sector where operator bankruptcies are quite normal, even expected, in tough economic conditions. It’s also hard to accurately judge solvency of some tenants, because many of them are privately held companies which don’t need to report their results the same way publicly traded companies do.

{kind=link}

Indeed, the company already had to face defaults last year as Parallel and Green Peak stopped paying rent on some of their properties. The company is actively dealing with the issue and so far it seems that things are under control as collections in Q1 2023 remained high at 98%. Going forward, I think further defaults or at the very least rent delays are to be expected, as the cannabis industry is currently going through somewhat of a downturn.

{kind=link}

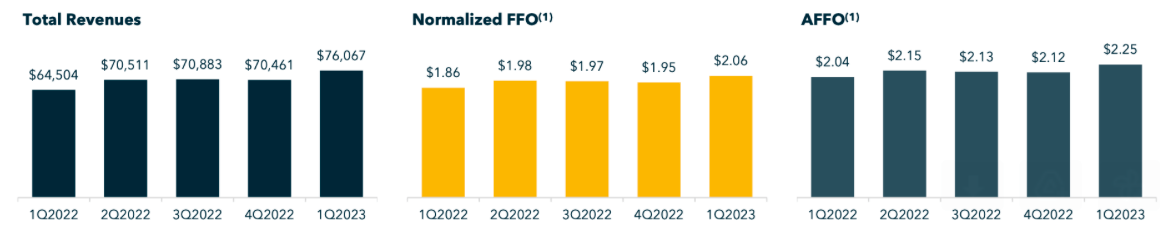

Despite the market being worried about further defaults, operational results remain strong as revenues as well as AFFO grew during the first quarter of the year. In fact, AFFO which is a key measure for a REIT, increased by over 6% YoY.

{kind=link}

With regards to their balance sheet, the company has more debt than NLCP which has no debt. Still, I consider their balance sheet solid as it only has one material debt maturity of $300 million in 2026 fixed at a 5.5% interest rate.

{kind=link}

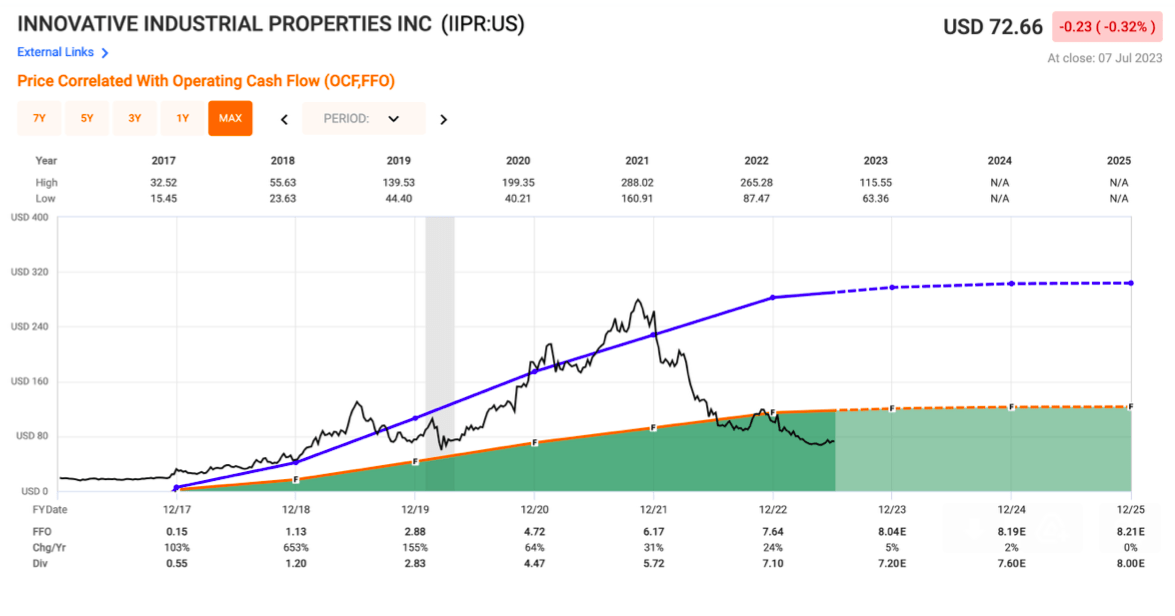

The forecast for 2023 FFO calls for a 5% annual increase which seems achievable in light of decent Q1 results. This is expected to be followed by two years of roughly flat AFFO which could reach $8.20 per share by 2025.

What attracts a lot of investors to the stock is the dividend which currently stands at $7.20 per share which translates to a yield of 10%. I personally wouldn’t buy the stock for the dividend, as the payout ratio is fairly high at 90% and if the company has to deal with further tenant defaults, I can easily see a dividend cut occurring.

IIPR has a short history, but it has a very good management team behind it, headed by Alan Gold. Currently IIPR trades at 9x FFO which is a little higher than NLCP which trades at 8x FFO. The premium, however, is justified by its size, a better multi-state operator mix and arguably a stronger management team. Relative to history, the average multiple provides little value here, because given its short history it was heavily influenced by the 2020-2021 bull run. As such, I don’t think IIPR is particularly undervalued on a risk-adjusted basis.

Sure, there is space for multiple expansion, but there is also a risk that more tenants will struggle to pay rent in which case the dividend as well as the stock will likely take a hit. All things considered, IIPR is a little too risky for my appetite and I therefore rate is as a HOLD here.

{kind=link}

For further details see:

Innovative Industrial Properties: I'm Not Falling For This 10% Dividend Yield