INST - Instructure Holdings: Driving Digital Transformation In Education Sector With Canvas LMS

2023-06-07 04:26:33 ET

Summary

- Instructure Holdings, an edtech company known for its Canvas learning management system, is well-positioned to meet the growing demand for digital education solutions as the market expands and digital integration becomes standard.

- Global spending on education technology is projected to reach $404 billion by 2025, with significant investments in infrastructure development.

- I view the stock as a buy at current levels and have an end-of-year price target of $32 on the stock.

Investment Thesis

Instructure Holdings, Inc. ( INST ) is an education technology company renowned for its Canvas learning management system [LMS], which facilitates the creation, management, and delivery of both in-person and remote instruction. With nearly 7,000 customers, Instructure holds the leading market share position in the U.S. Higher Education, and K-12 paid LMS segments. The COVID-19 pandemic drove increased demand for Instructure's services, resulting in accelerated revenue growth. INST is well-positioned to meet the demand for digital education solutions, as its online platforms and tools align with the evolving needs of educational institutions worldwide. As the market expands and digital integration becomes standard, Instructure's offerings are poised to facilitate efficient teaching and learning practices. I view the stock as a buy at current levels and have an end-of-year price target of $32 on the stock.

Q1 2023: Strong Results and Robust Pipeline

Instructure had a strong start to the year, with Q1 results surpassing expectations. The second-quarter guide was also better than expected as the company raised its full-year guidance. In higher education, Instructure maintained its market share of over 40% and observed RFP (Request for Proposal) activity in line with expectations. The K-12 segment showed promise with a healthy pipeline and increased interest. Notably, the assessment product experienced significant growth within the K-12 market. The international division remained the fastest-growing part of the business, particularly in regions like Latin America and APAC (Asia-Pacific). Structure's market position, growth prospects, early international expansion, and consistent execution in a challenging economic environment make me optimistic about the outlook of the company.

Growing TAM Includes Underpenetrated K-12 and International Markets

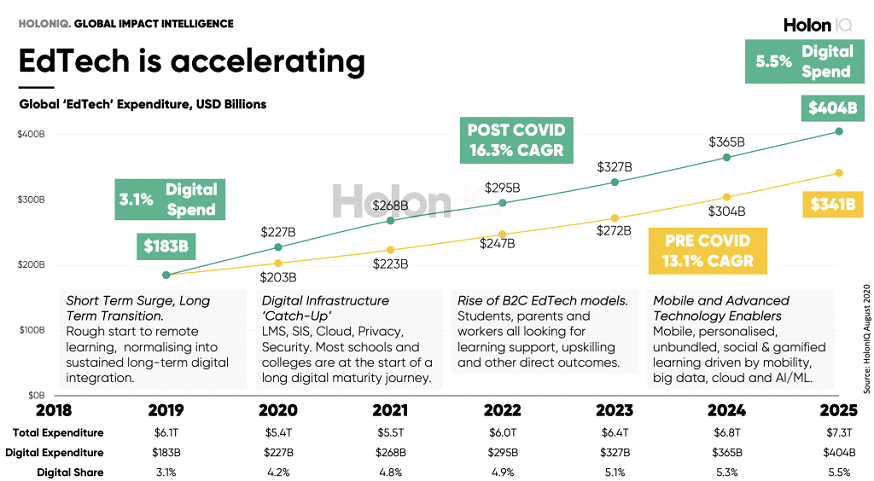

Instructure is capitalizing on a significant shift in the global education landscape, where the use of digital tools between students and teachers is becoming increasingly essential. While the COVID-19 pandemic played a role in accelerating the adoption of online education, many of these digital capabilities will remain crucial even as in-person or hybrid teaching resumes. Activities like homework submission, grading, student analytics, collaboration between parents and teachers, and scheduling are likely to continue being conducted online. In fact, online education platforms are expected to gain importance in hybrid learning environments as they enable teachers to track student performance and progress remotely. Consequently, most schools are planning to maintain their digital learning investments at post-pandemic levels.

According to global intelligence platform HolonIQ, spending on education technology worldwide is projected to reach $404 billion by 2025, growing at a compound annual growth rate [CAGR] of 16.3% between fiscal years 2019 and 2025. A portion of this expenditure is attributed to the need for significant infrastructure development in managing learning, data, and administration, as most educational institutions are still in the early stages of their digital maturity journey. In light of these trends, Instructure is well-positioned to benefit from the growing demand for digital education solutions. Its focus on providing effective online platforms and tools aligns with the evolving needs of educational institutions worldwide. As the market continues to expand and digital integration becomes the norm, Instructure's offerings are likely to play a vital role in facilitating modern and efficient teaching and learning practices.

{kind=link}

Valuation

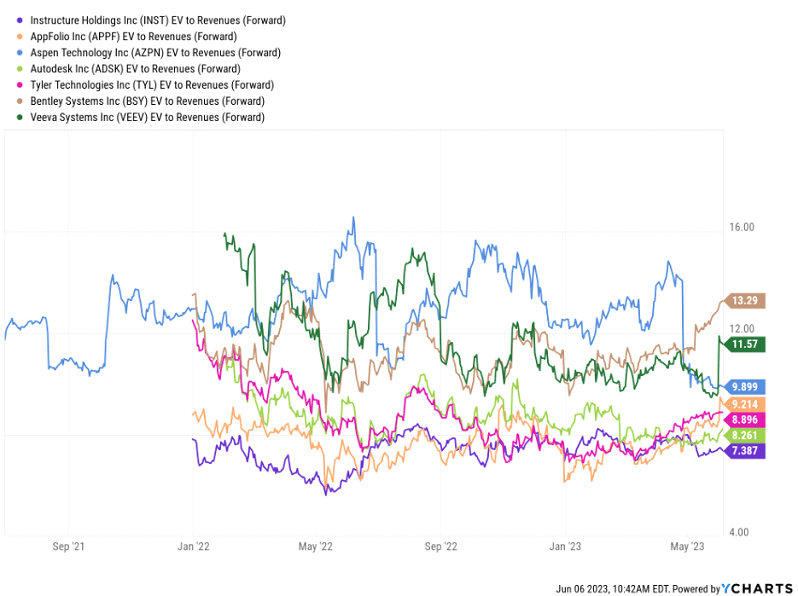

Given the high-margin and growth profile of Instructure, the vertical software names that I evaluate as comps are AppFolio (APPF), Aspen (AZPN), Autodesk (ADSK), Tyler (TYL), Bentley (BSY), and Veeva (VEEV). Each of these names trades at a premium to the implied 8x for Instructure.

If Instructure can show margin expansion, I believe that there is an opportunity to grow free cash flow faster than the average SaaS company. Instructure's discount to the broader comp group on both an EV/Sales further highlights my buy rating on the stock. My December 2023 price target of $32 is based on an 8x EV/Sales multiple applied to the FY24 revenue estimate of $575 million.

{kind=link}

Risks to Rating

The pandemic created a temporary boost in education spending as schools sought to facilitate remote and hybrid learning. However, it is challenging to determine the exact extent of growth in the medium term. I anticipate a normalization in the range of 15-20% in 2023 and 2024. If education returns fully to in-person settings, institutions might delay some digital education projects, potentially leading to slower growth compared to expectations. Moreover, there is increased competition from cheaper or even free alternatives. Additionally, certain districts rely on open-source or "free" options like Google Classroom or Moodle. However, it's important to note that implementing these solutions often incurs additional expenses, making the true cost higher than that of commercial alternatives. While these offerings may seem attractive initially, institutions should carefully consider the overall resources required before making a decision.

Conclusion

Instructure is a prominent education technology company renowned for its Canvas learning management system, which facilitates the creation, management, and delivery of both in-person and remote instruction. In the U.S. higher education and K-12 paid LMS market, Instructure holds the leading position with almost 7,000 customers. The COVID-19 pandemic led to increased demand for Instructure's services, resulting in accelerated revenue growth in recent years. The company successfully aligned its cost structure, leading to a non-GAAP operating margin of 20%. I believe that Instructure has the potential to maintain strong double-digit revenue growth and achieve impressive operating margins. Hence, I view the stock as a buy and keep a price target of $32 on the stock.

For further details see:

Instructure Holdings: Driving Digital Transformation In Education Sector With Canvas LMS