INST - Instructure Is Poised To Leverage Its Leadership Position

2023-10-26 21:47:21 ET

Summary

- Instructure is rated as a Buy due to its operations in an underpenetrated market, leadership position, international expansion and customer stickiness.

- The company has a strong track record of revenue growth, particularly during the COVID-19 pandemic, with a robust operating profile since it got relisted in 2021.

- The education market is set to grow, providing a significant opportunity for Instructure, and the company is focusing on AI capabilities to drive further growth.

Investment Thesis

We ascribe a Buy rating on Instructure driven by 1) massive and underpenetrated TAM with growing focus and adoption on digital technologies 2) its leadership position within the US 3) expansion within international markets (K-12 market in rest of the world is worth $2.5 trillion and assuming even 1% tech penetration implies a massive $25 bn opportunity) 4) focused investments in AI capabilities to drive next leg of growth 5) customer stickiness and its ability to cross-sell driving improving utilization and aiding operating margins (43% of existing users use more than 1 Instructure products with average revenue per customer growing from $47k in 2018 to $64k in 2022). We believe the company is poised to leverage its leadership capabilities across the US and globally to drive technology adoption within the education sector which remains underpenetrated. Its relatively comfortable and improving balance sheet position and strong cash generating ability with robust operating margins enables them to drive continued investments and deleverage its balance sheet.

Company Background

Instructure Holdings ( INST ) is the leader in both higher education and K-12 market within the US with a market share of 40% and 33% respectively . It has over 7,400 customers representing Higher Education institutions and schools in more than 100 countries globally. The company has transformed itself significantly since the acquisition by Thomas Bravo in 2020, selling its underperforming corporate LMS business and centralized its operations. Since then the company got re-listed on the bourses at a market value of $2.77 bn (~40% higher than the take private deal)

Historical Track Record

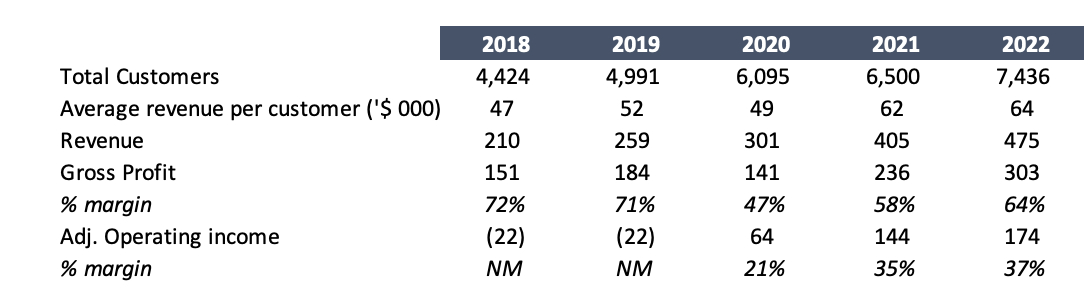

The company had reported strong growth in its revenue especially since COVID which has led to a stronger adoption of its LMS learning system as the schools and institutions looked for ways to find solutions to the unexpected shutdowns. Revenues grew at a record 22% CAGR during the 2018-2022 period leveraging its strong brand leadership within the overall LMS market. Its gross margins declined slightly as a result of the pressure within its corporate LMS business which it soon exited. However, its non-GAAP operating income margins went about 20% since the acquisition as a result of centralization of its operational costs, closing and consolidating its development facilities, restructure of sales and marketing teams by eliminating sales coverage in non-core international markets. Instructure's 43% of existing customers and 60% of new deals included customers which deployed more than one product solution from the company.

{kind=link}

Note: Gross profit are on GAAP basis. 2021 customer numbers are estimated.

Market Overview

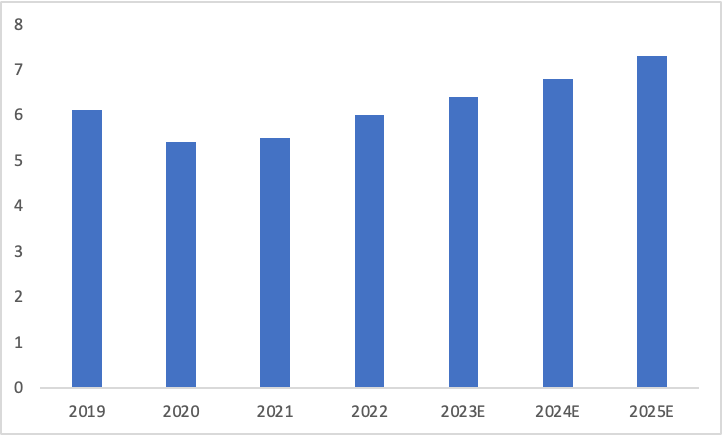

Education market is about a $6.0 trillion industry having declined slightly compared to the pre-pandemic levels but is set to grow to $7.3 trillion by 2025. This is still in line with the GDP growth compared to pre-pandemic levels (6.7% of global GDP in 2019 vs 6.6% of global GDP in 2025)

Global Education Market (in trillions)

{kind=link}

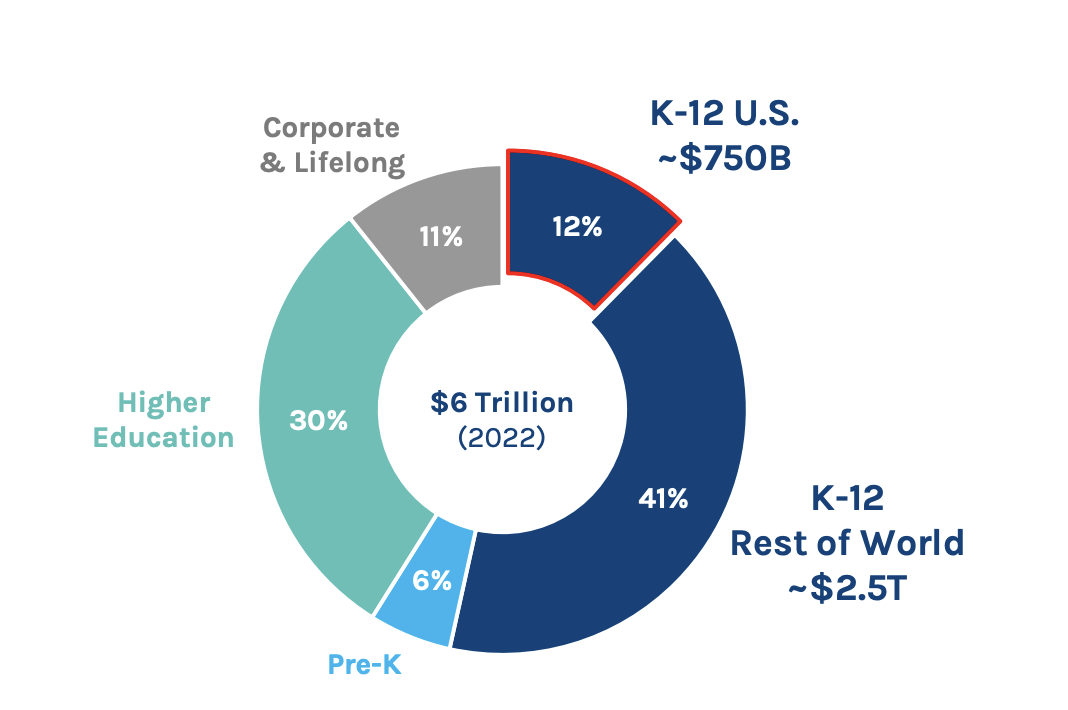

K-12 forms the bulk of the $6 trillion education market globally with higher education contributing about 30%. This provides a significant opportunity to the massive TAM that the company targets.

PowerSchool Investor Day Pres, Morgan Stanley Research

{kind=link}

In addition, technology penetration has still remained significantly lower which has improved from 3% in 2019 to 5% in 2022 and is further expected to be around 5.5% by 2025 which presents a massive opportunity to drive growth.

The Industry also has favorable tailwinds with about $90 bn of ESSER funds still left to spend by next year. While the bulk of funding could go to upgradation of infrastructure facilities as well as teachers' salaries, we believe a portion of the budget is likely to find its way within technology spending as well.

Competitive landscape includes several open source solutions such as Google Classroom and Moodle which do not provide the robust capabilities that K-12 schools and institutions pursue. Other competitors include Edmentum, Imagine Learning (both are private in nature with limited disclosure) and PowerSchool Holdings ( PWSC ).

| Company |

| # Schools |

| Revenue Growth (3Y CAGR) |

| Avg. Revenue per customer ($'000) |

| EBITDA Margin |

| Instructure |

| 1.6x |

| PowerSchool |

| 1.7x |

| Sprinklr ( CXM ) |

| 1.5x |

| EngageSmart ( ESMT ) |

| 3.0x |

| Blackbaud ( BLKB ) |

| 0.8x |

| Vertex ( VERX ) |

| 5.3x |

| Box ( BOX ) |

| 0.8x |

Source: Seeking Alpha, Author

Risks to Rating

Risks to rating include:

1) Return to in-person schooling can drive investments away from technology spends

2) Declining enrollment trends within the overall higher education market due to affordability challenges, macroeconomic scenario or competition from alternative education market

3) Consolidation within the industry could pose competitive challenges

4) Company is majority owned (85%) by Thomas Bravo, a PE firm, which can look to sell down a substantial stake at any time and affect shareholder policy changes which can pose an overhang for the stock

Final Thoughts

We believe Instructure is perfectly poised to grow within a growing education market amidst rising technology spends leveraging its significant brand leadership. In addition, the company's focus on deepening its next generation AI capabilities could be a significant growth driver amidst a rapidly shifting technological landscape. We initiate at a Buy given the brand leadership, customer stickiness, cross selling capabilities, expansion within international markets and its strong cash generation ability.

For further details see:

Instructure Is Poised To Leverage Its Leadership Position