INST - Instructure: New Logo Wins And Parchment Should Drive LT Growth

2023-11-15 04:16:15 ET

Summary

- Instructure showed robust growth in Q3, driven by strong new logo win rates and the acquisition of Parchment.

- I expect revenue to continue growing at >10+% through FY26 with sustained operating margins.

- INST's new logo win rate remains strong, indicating market leadership in the LMS segment, and the acquisition of Parchment should provide long-term value.

Summary

Readers may find my previous coverage via this link . My previous rating was a buy, as I believed Instructure ( INST ) previous quarter’s results were robust and showed strong growth. It has also shown that its products have a high retention rate. I am reiterating my buy rating as it continues to show robust growth in the third quarter driven by strong new logo win rates. I believe the acquisition of Parchment will serve as a robust growth driver.

Valuation

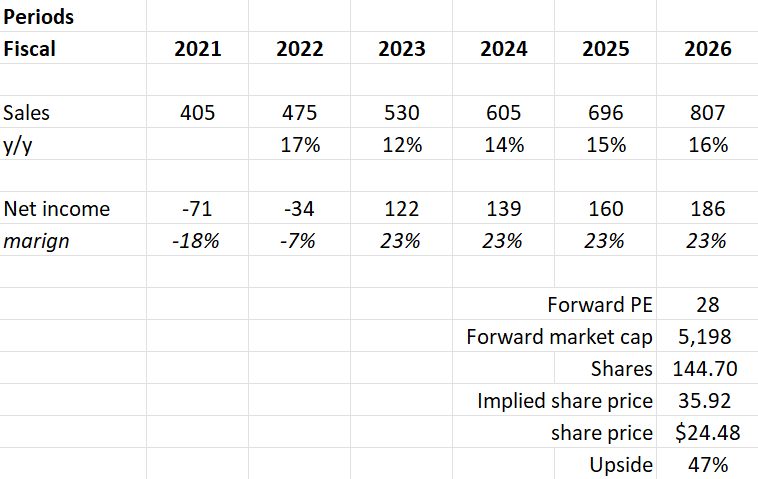

Based on my view of INST, I anticipate a 12% growth in its revenue for FY23, which will expand to 16% in FY26. This projection is influenced by a number of factors. Firstly, its revenue grew 10.2% in the third quarter, with operating margins turning positive when compared to the previous year. This reinforced my belief that it will be able to grow at double-digit growth rates. Secondly, management guidance for the full year 2023 expects revenue to be between $528 and $530 million, which translates to about 12% growth. Management also expects the net income margin to improve. With a strong new logo win rate, which is one of the best in the LMS segment, and the acquisition of the high-quality company Parchment, which will be discussed further later on, INST is well positioned for future growth and achieving net profitability.

{kind=link}

Based on author's own math

Peers overview:

FactSet

INST now trades at about 28x forward price/earnings, which is lower than the median of 41.39x. The reason INST is trading lower is mainly due to its 2-year growth outlook. In 2024, INST is expected to grow at 14% while competition is at 23%, almost twice that of INST. In terms of net income margins, INST is at negative 6.55%, while competition is lower at negative 19.75%. This trend can be attributed to competition reinvesting aggressively to boost its growth. With margins expected to turn positive in FY23, I would expect INST’s multiple to move towards the competition’s level. At its current multiple, the upside is about 47%. Therefore, I am reiterating my buy rating for the company.

Comments

INST has delivered another quarter of revenue growth. Revenue grew 10.2% year over year to $134.9 million , and operating income was $4.6 million, which represents a margin of 3.4%. This is an improvement when compared to the 2022 third quarter, where it reported a loss of $2.4 million. Overall, INST has shown robustness in both revenue and margins, which supports my positive view of the company.

I would like to touch on INST’s new logo win rate. It is a metric that measures INSTI’s success rate of new client acquisition on a base of total potential new clients. It is the percentage of potential new clients that results in an actual sale. INST’s new logo win rate remains robust, as evidenced by its continuous market share growth. Based on Edutechnica's 11 th annual LMS update, INST is the only Learning Management System [LMS] that continues to gain market share. CANVAS LMS is leading its competitor by more than double. Based on these statistics, it shows INST has a dominating market leadership and position in the LMS segment, and I believe this strength will drive INST to higher ground in the near future.

“Our strong competitive position and industry-leading platform give us confidence in the long-term durable growth of our business” Source: 3Q23 earnings

During the quarter, INST announced the acquisition of Parchment. In my view, I believe this acquisition will create value for INST immediately and in the long run. Parchment is the top credentialing program that also provides enrolment solutions. Therefore, this acquisition will allow INST to reach a larger audience base and increase its market share, boosting its future growth. INST provides learning courses for students, while Parchment is a credential solution platform. Therefore, they complement each other in a well-rounded way and provide their customers with the full life cycle of their learning journey, starting from learning all the way until getting employed.

Based on INST’s research on Parchment before announcing the acquisition, INST noted that Parchment is a high-quality business, as 95% of its revenues are recurring, which indicates a strong retention rate. This is backed by its more than 90% gross retention rate. INST is a company that focuses on M&A, and it is an important part of its growth strategy. Given its strong M&A track record, the acquisition of Parchment is set to provide long-term value for them.

“We have a strong track record of successfully integrating acquired companies, completing six integrations in the last four years. We have confidence we'll execute similarly with Parchment.” Source: 3Q23 earnings

Risk & conclusion

Updated risk relates to the acquisition of Parchment. While INST has a good track record, each acquisition is different, and it carries its own challenges such as integration issues or not producing the result as intended. This is especially more prominent when trying to integrate software systems into one big ecosystem, which is a daunting task as it takes a lot of resources and expertise to do so.

Overall, INST managed to deliver on its third quarter results. The continuous robust growth in new logo win rate is promising, and its Canvas LMS is leading the competition by big margins. This strong customer acquisition is going to add more strength to its leading market position in the LMS segment. The announcement of the acquisition of Parchment is also expected to create synergies between the two companies and build long-term, robust growth for INST. Overall, I am reiterating my buy rating for the company.

For further details see:

Instructure: New Logo Wins And Parchment Should Drive LT Growth