CA - Interfor: Worse To Come But Relative Value And Demographic Tailwinds Remain

2023-04-23 02:33:08 ET

Summary

- Interfor is a company we definitely worry about in the short term. The bottom hasn't come for their results yet especially in new home construction.

- However, we also see that housing dynamics in the US ultimately remain favourable, even though this market may take the biggest short term dive in lumber use cases.

- Some meaningful tax receivables are worth mentioning, which have accumulated over the last couple of years and represent about 50% of market cap.

- Still, best to stay away at the moment.

Interfor ( IFP:CA )( IFSPF ) is a pureplay lumber company with assets in Canada and in the US. On a first note, they're somewhat insulated from the beetle issues in the Rockies thanks to acquisitions over the last couple of years that have increased their capacity elsewhere, on the other, their imports into the US have created pretty large tax receivables from taxes held in trust. These receivables cover about 50% of market cap and make for a pretty interesting thesis. The issue is that lumber prices have already retreated to local lows, and they could keep going lower as housing starts materially drop with housing end-markets still being levitated in the mix. Lack of backlog there will be an issue, although we think the dynamics in housing also demonstrate that the shortage has not been addressed enough in this period, and will only continue to grow. We continue to watchlist these lumber plays, and now prefer Interfor over West Fraser Timber ( WFG ) whose tax receivables are much smaller.

Recent Figures

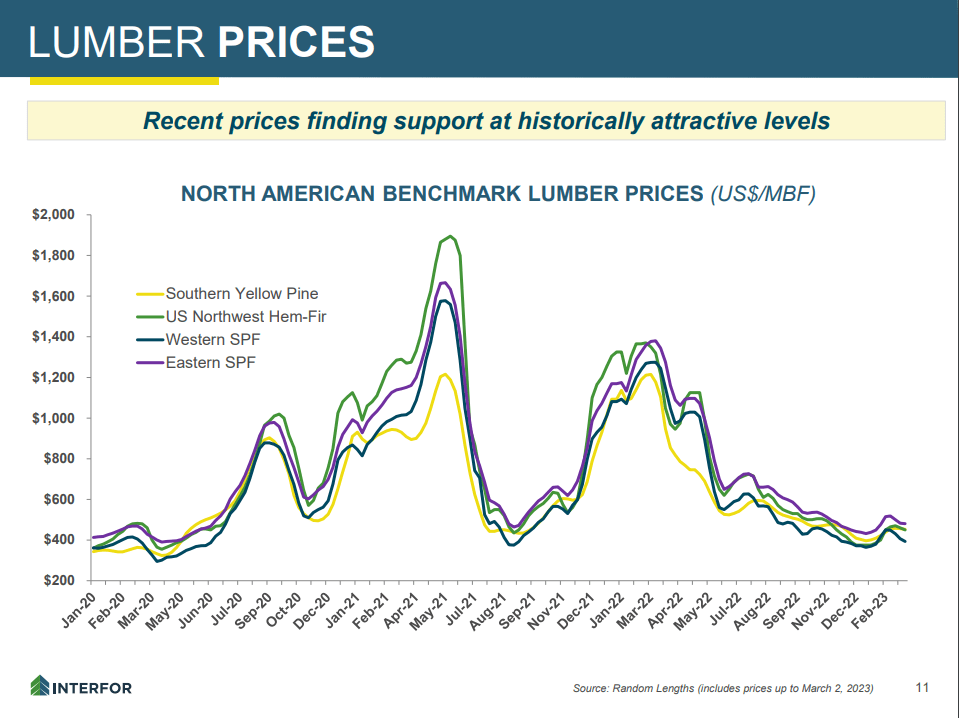

The first thing to point out is the situation with lumber. Prices have retreated to local lows over the last 3 year period.

{kind=link}

EBITDA has started to fall that way as well, being the same as the average 2021 levels, but 2021 also had some of the highest lumber prices we'd seen in years. EBITDA could easily continue to halve just considering the run-rate dynamics, and could go down further depending on what tightening credit conditions does to housing, likely to bring it down to levels substantially worse than just pre-COVID.

Lumber End-market Demand (Q4 2022 Pres)

{kind=link}

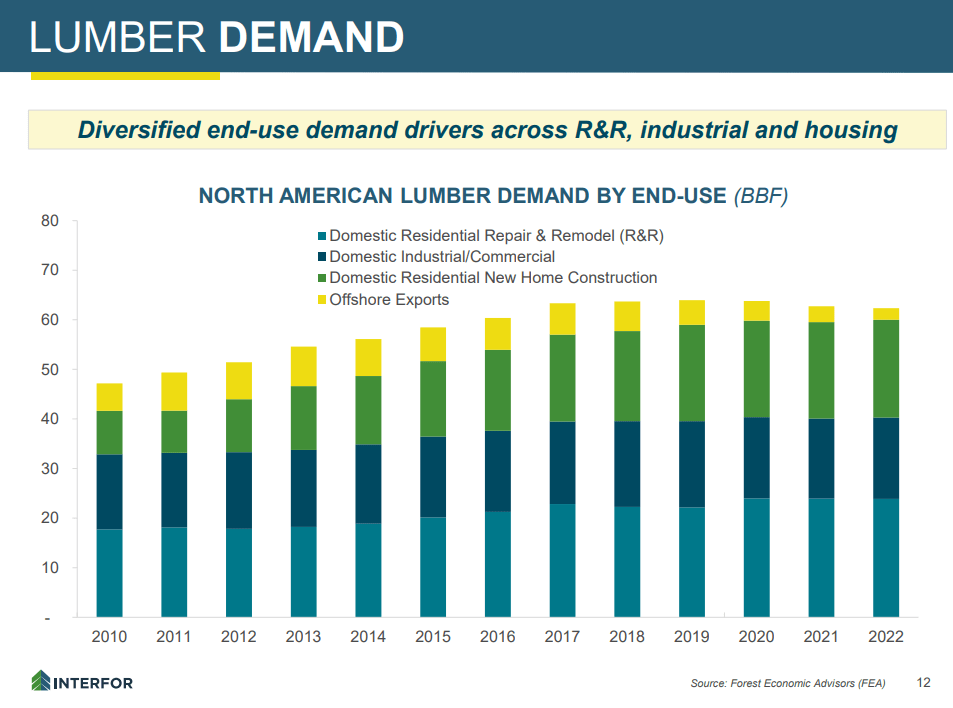

New residential home construction was still a large market for Interfor, but a serious decline in housing starts is an issue.

US Housing Starts - House Age (Q4 2022 Pres)

{kind=link}

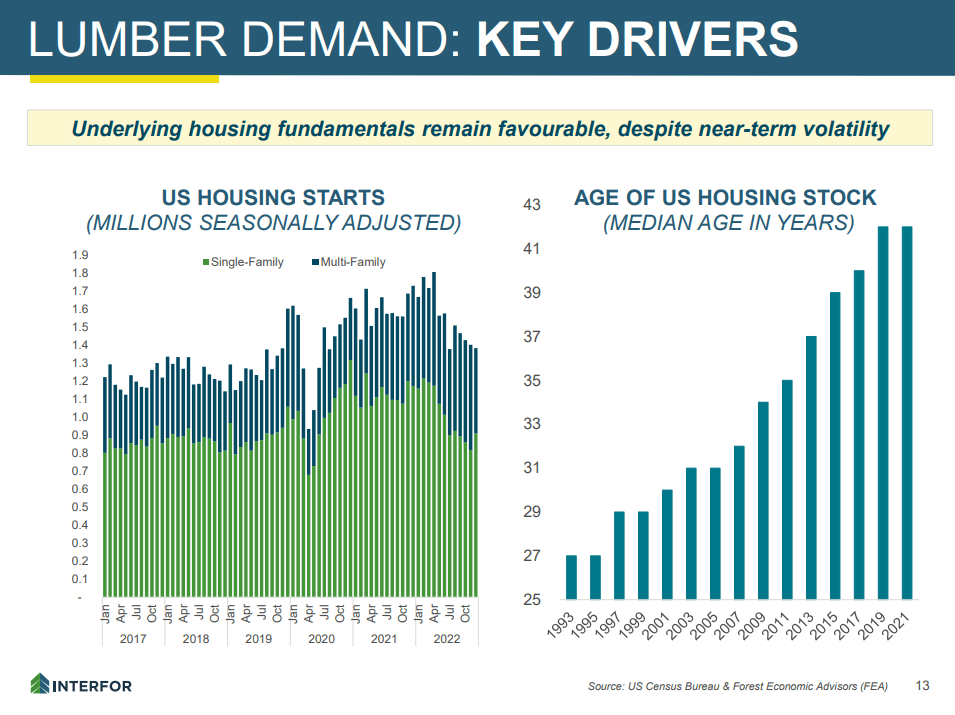

While the credit-rich period did promote quite a lot of home-building, housing age still didn't decline, and the current declines in housing starts , albeit for now only to nomalised pre-COVID levels, means that housing construction is not catching up with the demographic-based demand of millenials for housing as new families start, as well as for general US demographics which are very strong relative to other western economies in terms of population growth.

Bottom Line

There are some positives, which is a certain margin of safety created by pretty large tax assets that end up accounting for almost 50% of market cap. This comes from duties paid by Interfor that are held in trust by the US government, but with scope to be fully returned. WFG does not have as much of these tax assets.

Tax Receivables (Q4 2022 Pres)

{kind=link}

Interfor are also acquiring more lumber companies. The scope for synergies is rather high relative to current run-rate EBITDAs that these acquired companies are likely to have based on precedent transactions in the sector, and this helps Interfor hit its 2027 volume plans and diversify its supply, since environmental and biological conditions have been critical in the past.

Finally, valuation remains low, but this is on a TTM basis. We think the run-rate figures are around 5x PE at the moment. The automatically generate EV calculation will not be including the tax assets, so it is cheaper that WFG on an EV/EBITDA basis, probably by about 30% considering that WFG is slightly less commodified, although it's just as exposed to housing as Interfor, if not more so due to OSB exposures.

The direction is poor though, so we are going to keep to the sidelines. But it's worth following the story. Interfor could easily hit the forget bin if its income continue to drop, at which point picking it up at the bottom of an economic cycle could be a great way to generate some returns here.

For further details see:

Interfor: Worse To Come, But Relative Value And Demographic Tailwinds Remain