META - Interpublic Group: Deep Value Advertising Giant

2023-07-28 15:59:07 ET

Summary

- Interpublic Group stock dropped after disappointing earnings, but it is currently undervalued and presents a buying opportunity.

- IPG has a strong track record of dividend growth, with a 5-year and 10-year Dividend Growth Rate of 9.00% and 16.09% respectively. In addition, share buybacks can drive potential returns.

- Despite macroeconomic headwinds, IPG's core drivers of growth, such as media offerings and the healthcare sector, have remained strong.

- We currently hold IPG LEAPS, which we bought at the green trendline support. We believe IPG is currently a buy at the current level.

Introduction

Interpublic Group ( IPG ), one of the leading global advertising and marketing services companies, got slaughtered after its latest earnings report. The company is currently trading 23% lower than it was before earnings. Unfortunately, the earnings results were disappointing. Nonetheless, we believe Interpublic Group is a buy at the current valuation, and in this article we will go more in-depth why we believe this is the case.

Strong Dividend Growth Even In Rough Times

Interpublic Group operates in one of the sectors who had a rough time in 2023: the communication services sector. Despite the pressure, the company was trading near all-time highs recently, due to the fact that IPG has continued its exceptional execution even in this rough market for the sector as a whole.

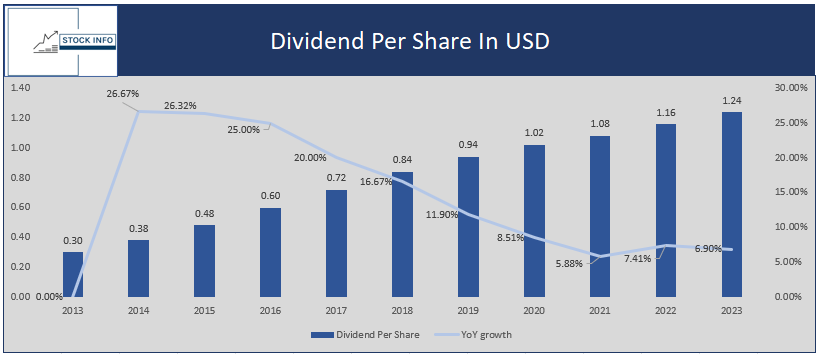

Yes, the company has suffered, but the company is currently sitting at an attractive valuation for investors playing the long game and along the way shareholders receive a nice dividend. Regarding the dividend, IPG has an excellent track record of growing its dividend with a 5Y and 10Y Dividend Growth Rate of 9.00% and 16.09% respectively, which is really impressive.

As can be seen in the table below the dividend has been consistently growing, but the YoY growth has decreased, which is normal as the dividend becomes larger over time.

{kind=link}

If IPG is able to continue this 6%-7% dividend growth in the next few years, which they should be easily capable of given their current payout ratio of 43.32%, this indicates that they have plenty of room to increase the dividend in the future. In addition, IPG remains confident that they can continue to grow their revenue this year between 1% to 2% in 2023, which is a slight revision from their earlier statement of 2% to 4%.

{kind=link}

Nonetheless, this is still impressive due to the rough macro environment the company has to operate in. Furthermore, should the macro-environment improve, the company's results could significantly improve, which could drive shares a lot higher from here.

Current Headwinds and Expectations

As stated in the paragraph above, the company has suffered from the current macroeconomic environment. The CEO of IPG, Philippe Krakowsky mentioned in the Q2 earnings call that the macro uncertainty impacted some of their specialty assets and traditional consumer agencies.

Nonetheless, strong drivers of their growth over the years remained steady in the latest quarter, namely IPG's media offerings and the healthcare sector. In addition, IPG saw strong growth in disciplines such as public relations and we believe this trend is likely to continue.

Due to the rough macro environment we saw large tech companies such as Meta ( META ), Amazon ( AMZN ), Microsoft ( MSFT ), and Alphabet (GOOG) ( GOOGL ), among many others, announce large layoffs. Unfortunately for IPG this isn't the only measure companies tend to take in times of hardship. Other than layoffs, companies also tend to aggressively cut their spending on advertising during these times.

While advertising is vital for most companies, it is reasonable to expect a further decline in advertising costs if macro conditions would worsen. In case of a recession, IPG would definitely be under more pressure. Nonetheless, companies must continue to advertise as in the short-term cutting advertising cost might not affect your revenue and sales significantly, in the long-term sales most definitely decrease as mentioned in this article from Wolters Kluwer ( WOLTF ).

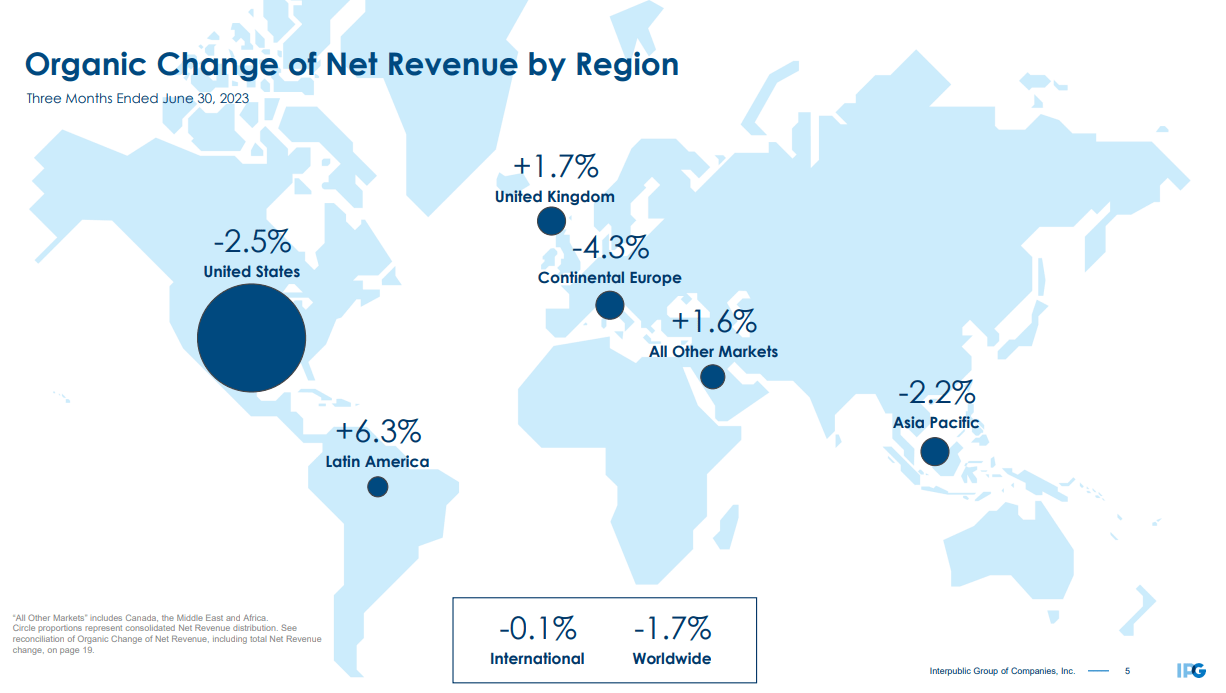

While IPG has shown to be resilient during this time of economic challenges the company took a small hit in its latest earnings, which can be seen in the visual below. It is likely that the company will struggle for a bit longer as these conditions aren't likely to improve in the short term, though we believe the company got punished a bit too hard after the latest results and now provides an attractive opportunity for the long-term investor.

{kind=link}

As shown above, the United States and Continental Europe were hit the hardest, which impacted the overall results.

Financials and Catalysts

As mentioned earlier, companies tend to cut advertising costs in times of economic hardship. On the other hand, companies need to continue advertising so they don't lose market share to their competitors. In good times, companies tend to increase their spending on marketing and advertising. With IPG being pretty resilient already, we believe if the macro outlook improves, IPG could benefit significantly from this.

As an investor, buying into cyclical companies can be difficult as it is often hard to see when the downward trend ends. We believe it is important to buy quality companies in this case and IPG definitely qualifies as one. When the market improves, earnings will more than likely skyrocket, which makes Interpublic Group an interesting buy as we believe the advertising industry might be mispriced at this moment in time. We believe IPG might be the best opportunity for value investors out there looking to buy into a stellar company within the advertising industry.

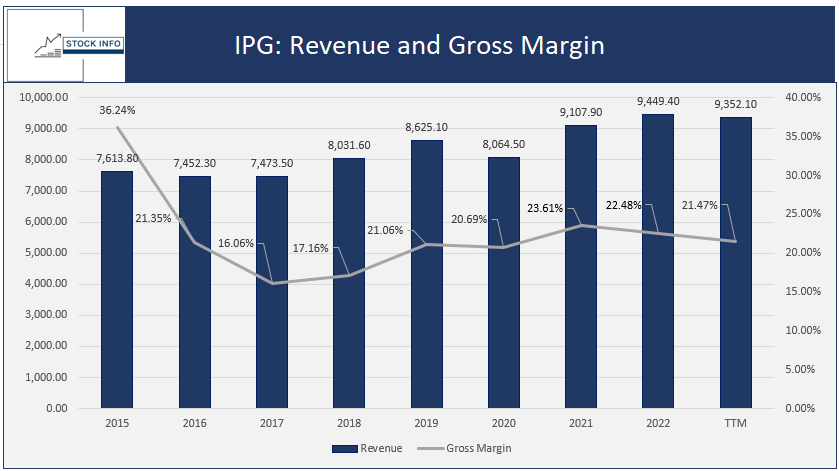

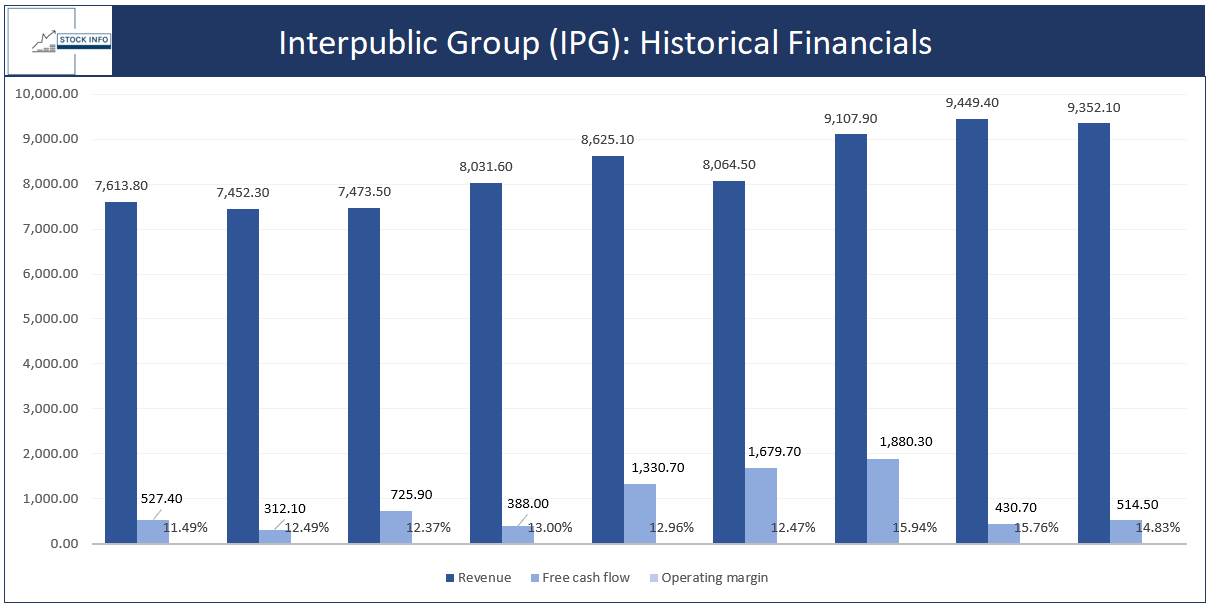

As can be seen in the chart below, IPG has seen a steady long-term growth in revenue over the years. In addition, IPG has been able to keep their gross margin steadily above 20%.

{kind=link}

In addition, the company made $9.35B in revenue over the trailing twelve-month period ((TTM)), this means that the company is trading at only 1.3559x the TTM revenue.

This seems cheap for a company like IPG, however, the company is currently trading at around 24.89x FCF, which can be seen as relatively expensive. Nonetheless, we believe the FCF will increase again if the macro-environment changes, which could bring us back to 15x FCF and below.

YCharts

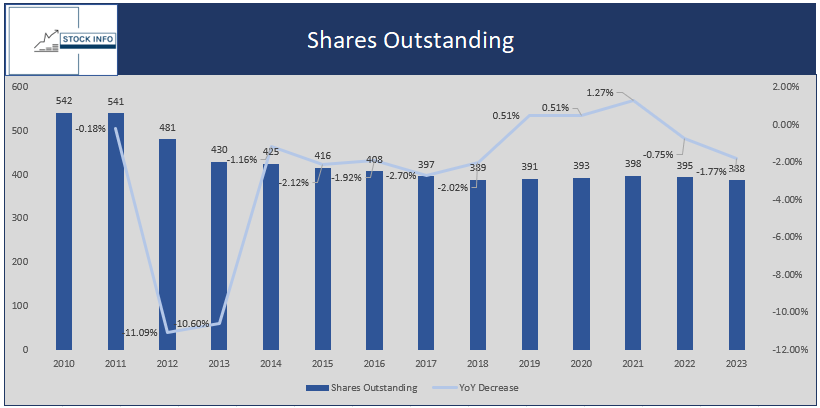

When taking a look at their shares outstanding, we can see that IPG has decreased its shares outstanding from 542 million shares to 388 million shares as of the 30th of June 2023, a decrease of 28.14% since 2010.

The company seems confident it will be able to continue this trajectory and I believe it is more than likely that they will start buying shares more aggressively if the stock continues to decline further. This makes IPG an enticing investment, as we can expect a decline in shares outstanding, as well as margin expansions and more than likely revenue - and free cash flow growth in the future if the macro conditions improve. In addition, we can expect an increasing dividend over the years, which makes IPG an enticing investment for the upcoming years.

{kind=link}

In addition, the company currently has a 5Y revenue CAGR, which is not great, but we expect this to increase once the sector is out of the woods. Furthermore, the company is currently trading at a FCF yield of 4.06%, indicating that the company could buy itself back in a little less than 25 years.

Valuation and Peers

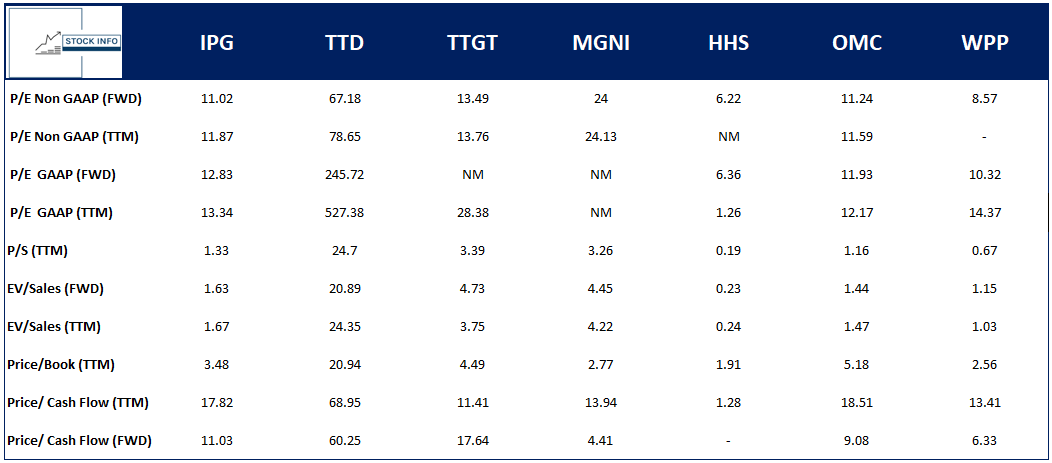

IPG is one of the largest advertising companies with stellar financials. When taking out the micro-caps and looking at the quality companies only 3 remain: Interpublic Group, The Trade Desk ( TTD ), and OMC. We pick those as in case of a recession only the best are able to retain pricing power and low debt will be crucial.

The Trade Desk is in another league and can't really be seen as an immediate competitor of IPG. We believe The Trade Desk is an amazing company, but it is currently trading at a steep valuation. However, the company definitely deserves a premium for its excellent execution and amazing growth trajectory. We will more than likely discuss TTD in another article.

When looking at IPG, we can see that they currently have a ROIC of 19.74%, which indicates that for every $100 the company invests in its business the company is able to generate an additional $19.74 in operating income.

{kind=link}

In addition, IPG has a 5Y Revenue CAGR of 1.63%. This is quite low, but can be expected of a cyclical business which struggled over the last 2 years. As indicated earlier, we believe they will be able to grow their revenues between 5-10% on average in years to come once sentiment improves.

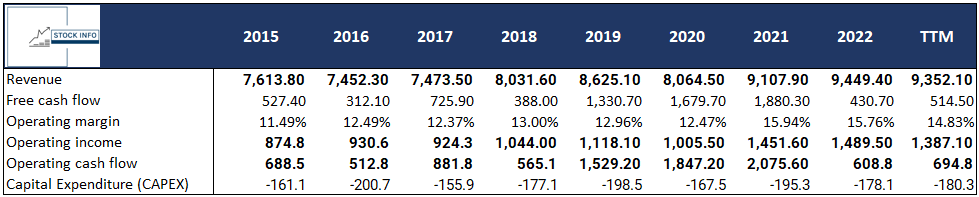

Their free cash flow currently sits around $514.50M, resulting in a 4.06% FCF Yield. In theory, this means IPG could buy itself back in a little less than 25 years. In addition, operating income declined slightly, while capital expenditure increased further, which is due to the rough macro environment the industry is going through.

The chart below shows the steady trajectory of revenue and operating margin growth.

{kind=link}

When taking a look at their peers, we can clearly see that IPG can be situated somewhere in the middle of the pack. But, taking into consideration the quality of its business and it being a leader in the industry, we believe IPG is one of the best investments in the industry.

The low multiples and an excellent P/S ratio of 1.33 and a price/book ratio of only 3.48 makes this an attractive investment.

{kind=link}

Technical Analysis

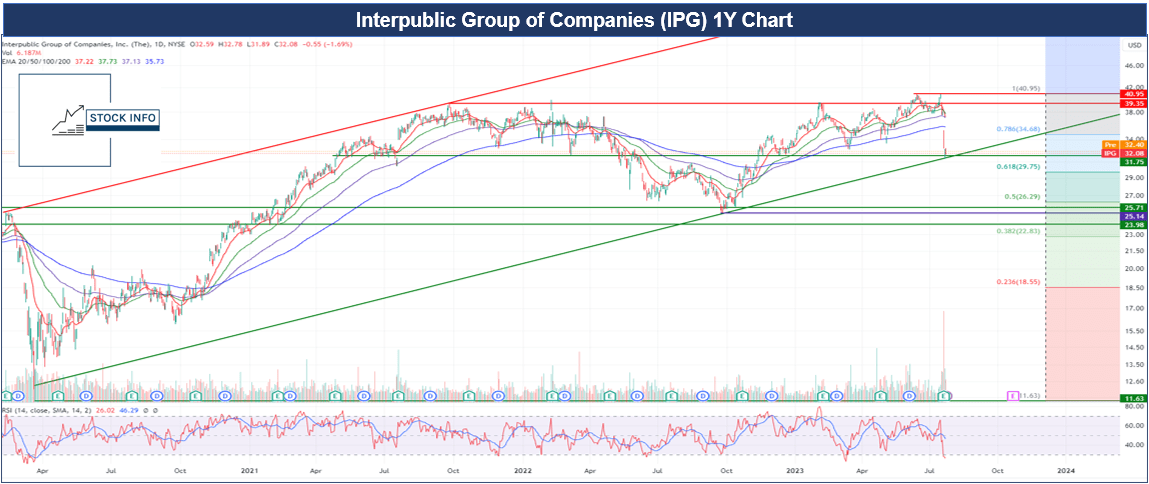

As can be seen in the chart below, IPG got slaughtered after earnings, which made the stock fall back to the rising green trend line, which has shown to be a decent support level as of now. In addition, IPG stock is currently trading below all of its EMA's on the daily chart.

It is crucial for the stock to hold this rising green trendline as breaking this level could mean the end of the uptrend and more downside can be expected if this level is breached. However, it should be noted that the stock is currently in oversold territory, which means that the stock might be due for some upside.

Immediate upside resistances would be the $34.68 FIB level and the 200 EMA (blue line). If the stock would breach the up-trending green trendline, the next stop could be as low as $25.14, which is the 2022 low. If IPG stock would lose this level it is pretty much in no man's land and one should be careful based on technical analysis.

{kind=link}

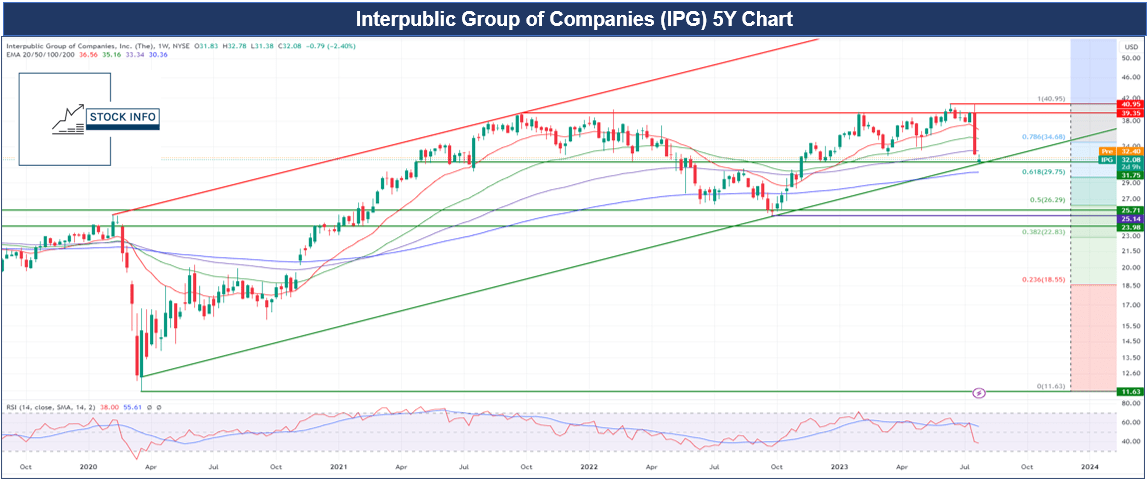

On the long-term chart, we can see the clear uptrend IPG stock has been in since the covid-19 bottom back in March of 2020. On this long-term chart, we can see that the stock has fallen below all of its EMA's except the 200 EMA. This 200 EMA can be considered a crucial support line in case we breach the green trendline and might act as final support.

On the upside, we have the $39-$40 level, which has shown to be a tough resistance zone to break over the last 2 years. If new highs are made, there is nothing holding the company back from touching the rising red trendline resistance.

All in all, we believe the technical analysis shows that IPG stock is currently at an attractive entry point if the green trendline holds and thus provides a great R/R opportunity for long-term investors or even for people who are looking for a swing trade for the next few months.

{kind=link}

Conclusion

Interpublic Group faced a significant drop in its stock price following its latest earnings report, which disappointed investors. However, despite the challenges in the communication services sector, IPG has shown exceptional execution and resilience during these rough market conditions. Moreover, the company offers a strong dividend growth history, with a 5-year and 10-year Dividend Growth Rate of 9.00% and 16.09% respectively, making it an attractive prospect for long-term investors.

Despite the current macroeconomic headwinds impacting some of IPG's specialty assets and traditional consumer agencies, the company's core drivers of growth, including media offerings and the healthcare sector, have remained robust. Looking ahead, if the macroeconomic environment improves, IPG could witness a significant uptick in earnings, as advertising spending tends to increase during more favorable economic conditions.

Financially, IPG has displayed steady long-term growth in revenue and maintained a gross margin above 20%. Additionally, the company has reduced its shares outstanding and remains confident in continuing this trajectory. A positive macro outlook could lead to further margin expansions, revenue growth, and a potential increase in dividend payouts, making IPG an enticing investment option for the future. Considering the valuation and peer comparison, IPG stands out as one of the best investments in the advertising industry.

While the stock experienced a decline after earnings, technical analysis indicates that the green trendline is a crucial support level, presenting an attractive entry point for long-term investors and swing traders.

In summary, despite the recent challenges, Interpublic Group ((IPG)) represents a compelling opportunity for investors willing to hold for the long term. The company's solid financials, attractive valuation, and potential for growth in a more favorable economic environment make it a strong contender in the advertising industry.

This, in addition to the interesting entry point from a technical perspective, makes IPG very attractive from a risk/reward perspective and as such we believe IPG is a buy at this moment in time.

For further details see:

Interpublic Group: Deep Value Advertising Giant