IVT - InvenTrust Properties: Low-Risk Essential Retail Compounder

2023-12-20 08:30:00 ET

Summary

- InvenTrust Properties is a grocery-anchored shopping center REIT with a strong and low-leveraged balance sheet.

- The retail real estate sector has low new supply under construction, while retailer and food service demand remains robust.

- IVT's portfolio is well-positioned in Sunbelt states, with high occupancy rates, great locations, and a focus on essential retail, making it recession-resistant.

InvenTrust Properties (IVT) is a small, 62-property, grocery-anchored shopping center REIT concentrated overwhelmingly (95%) in fast-growing Sunbelt states. In addition to boasting one of the best positioned and most defensive portfolios in the retail real estate space, it also enjoys among the strongest and lowest leveraged balance sheets.

The retail real estate sector currently has the lowest amount of new supply under construction of anytime going back to 2005. Deliveries of new centers is near record lows, while retailer and food service demand remains robust.

While Sunbelt markets that have grown rapidly in recent years typically have slightly higher retail under construction, development pipelines are still quite low. There is no risk of an oversupply scenario showing up anytime soon.

At a price to core FFO of 15.8x, a price to AFFO of 21.6x, and a price to free cash flow of 22.9x, IVT admittedly isn't cheap. But it is also very reliable, low risk, and recession-resistant.

With former CEO of NNN REIT (NNN), another low-risk, slow-and-steady compounder, Julian Whitehurst recently ascending to the Chairman's seat on IVT's board of directors, my view of IVT as a reliable and steady compounder is affirmed.

Between IVT's 3.3% dividend yield and mid-single-digit growth, I would expect total returns of 8-9% for this retail stalwart going forward.

InvenTrust's Well-Positioned Portfolio

IVT owns and manages a lean, 62-property portfolio of mostly grocery-anchored shopping centers in the Sunbelt as well as the Washington DC metro area.

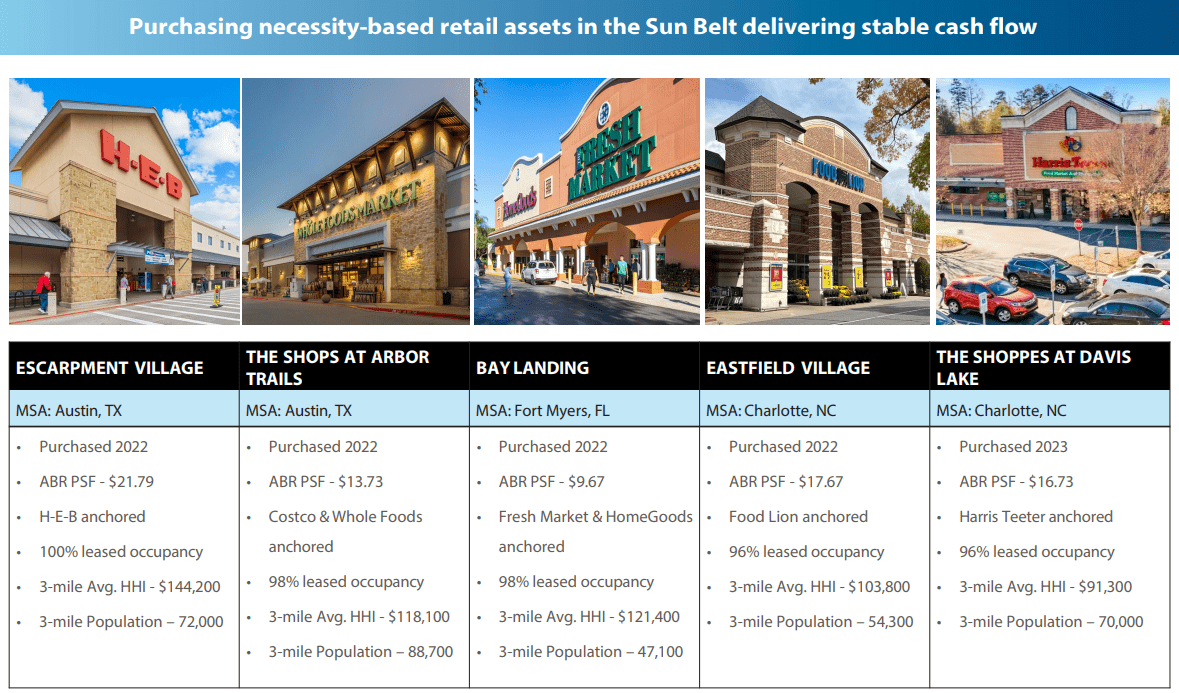

Here are some examples of recently acquired properties, which illustrate the REIT's investment criteria:

{kind=link}

The 95% concentration in the Sunbelt is a major positive, because population and job growth in these areas has been above-average and will probably continue to be so going forward due to lower taxes, lower overall cost of living, and less crime.

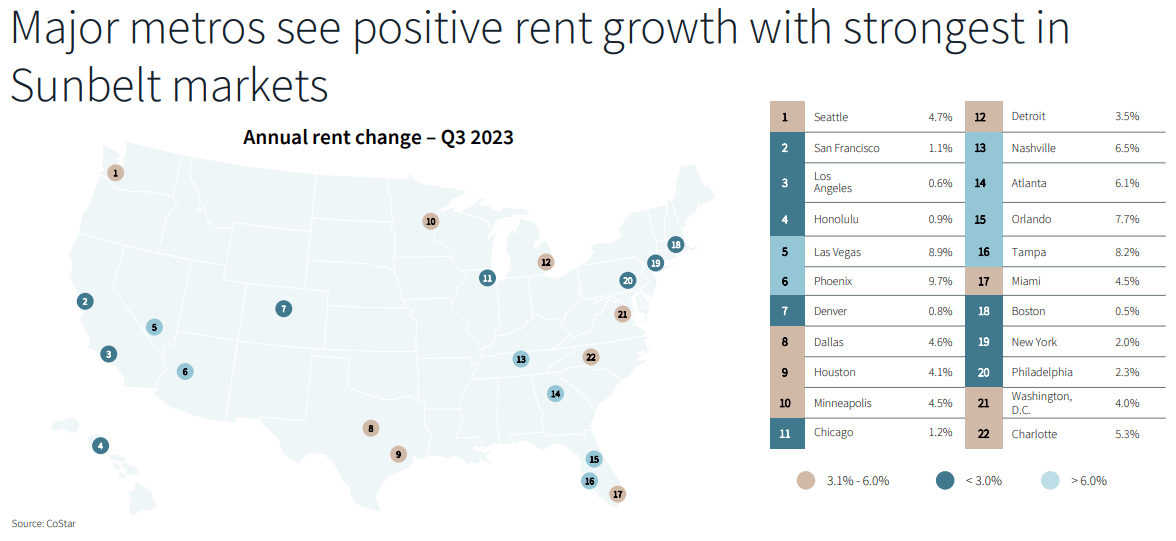

In the third quarter of 2023, the markets with the highest retail rent growth were almost uniformly located in Sunbelt states.

{kind=link}

Texas markets exhibited moderately strong growth between 4-5%, while non-Texas Sunbelt markets like Tampa, Orlando, and Atlanta all enjoyed high single-digit rent growth rates.

These are some of IVT's hand-picked markets.

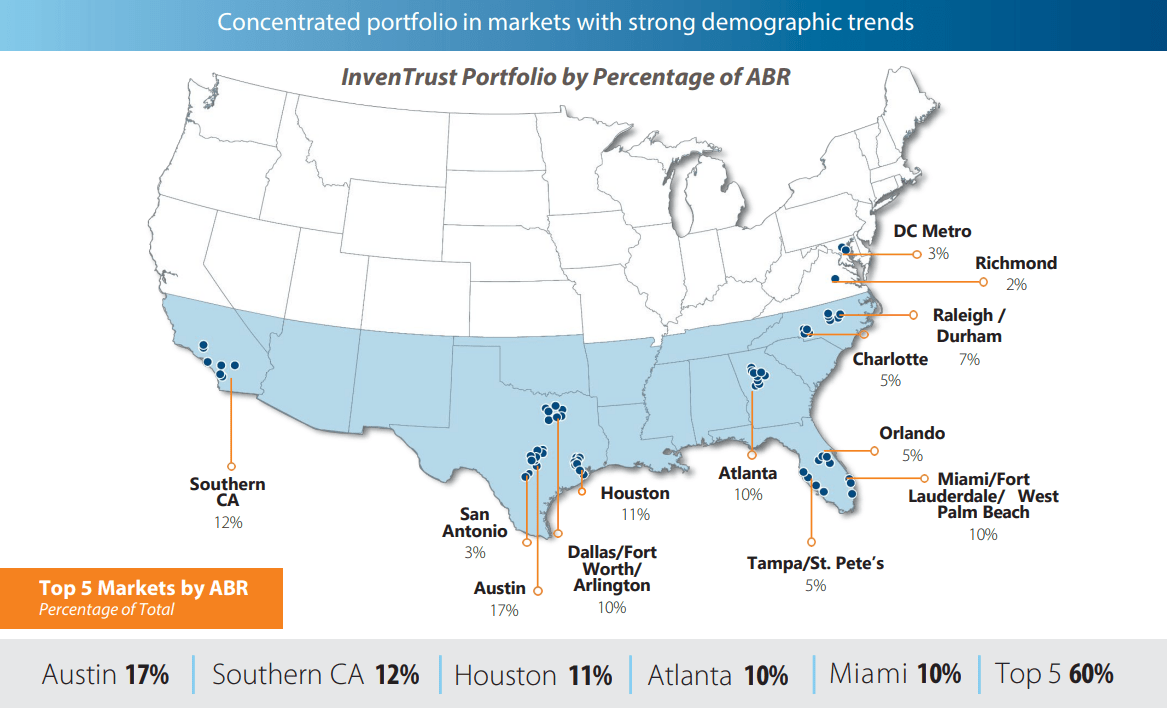

As we can see below, IVT's largest state is Texas, representing about 41% of total rent, but Southern California, South Florida, and Atlanta also account for 10% or more of rent each.

{kind=link}

IVT boasts the second most Sunbelt-concentrated portfolio of all retail REITs, behind only Whitestone REIT ( WSR ), whose portfolio is entirely concentrated in Phoenix, Dallas/Fort Worth, Houston, Austin, and San Antonio.

IVT's markets enjoy almost uniformly high occupancy rates of around 95-96%, and its occupancy rate of 95.1% is in line with that. Occupancy dropped from over 96% to that level in Q3 2023 because of the Bed Bath & Beyond bankruptcy. Once those highly coveted BB&B spaces are backfilled, IVT's occupancy should return to 96% or higher.

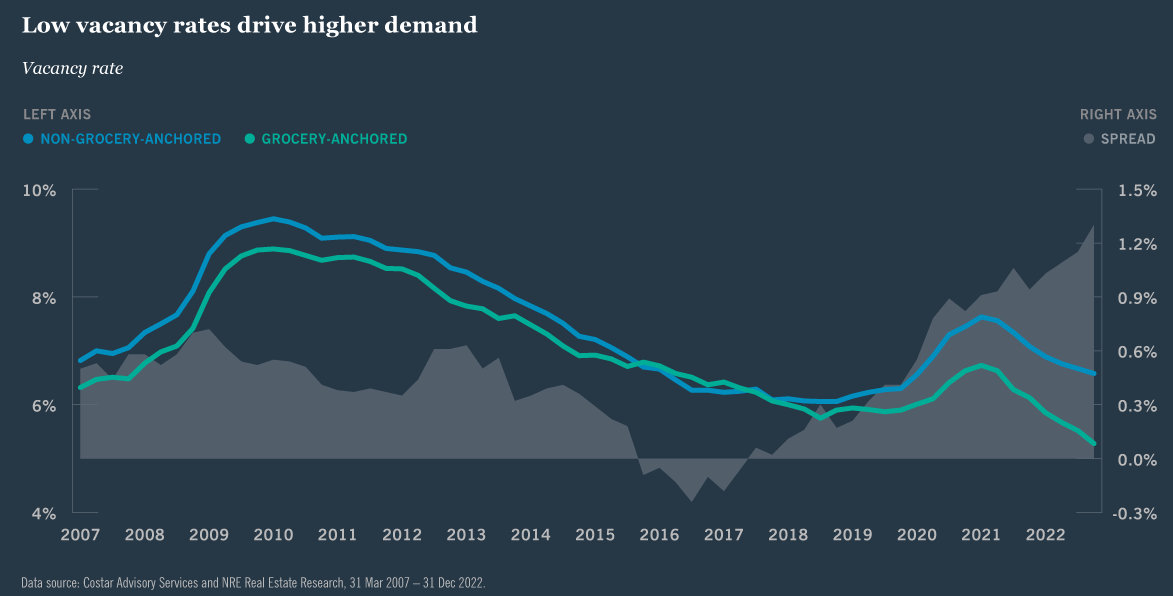

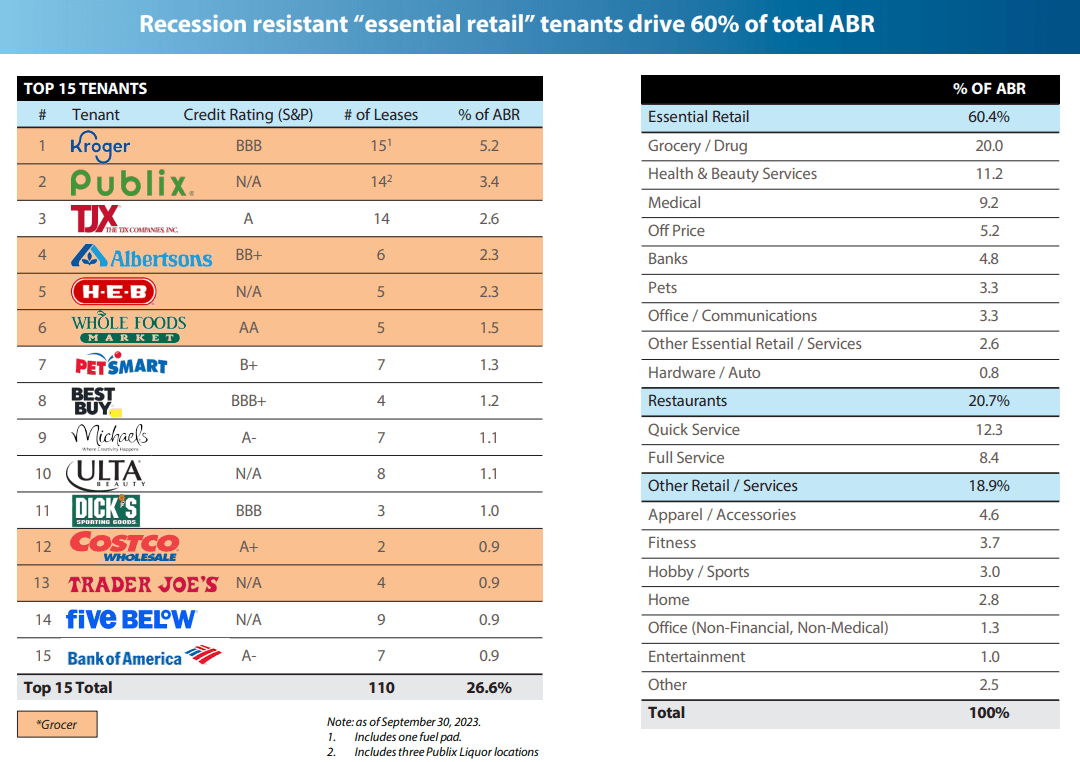

But its Sunbelt concentration is only one of IVT's spheres of strength. The other is the fact that 87% of the portfolio is grocery- or drugstore-anchored. Retailer demand for spaces in these centers has been extraordinarily high in recent years, causing grocery-anchored retail vacancy to fall significantly.

{kind=link}

These two factors go a long way in explaining why IVT will likely turn in the highest same-property NOI growth in its peer group this year.

Here's IVT's occupancy and SPNOI growth guidance for 2023 compared to essential retail peers Regency Centers ( REG ), Phillips Edison & Co. ( PECO ), and Federal Realty Trust (FRT):

| Q3 Occupancy |

| 2023 Same-Property NOI Growth |

| IVT |

| 95.1% |

| 4.25% to 5% |

| REG |

| 94.6% |

| 3% to 3.5% |

| PECO |

| 97.8% |

| 3.75% to 4.5% |

| FRT |

| 94.0% |

| 3.75% to 4.25% (author's estimate) |

If not for the BB&B bankruptcy, IVT's SPNOI growth probably would have been even higher. But the vacancy of these spaces simply sets up for a stronger SPNOI growth rate in 2024 as they are backfilled at higher lease-over-lease rent rates.

Already, IVT's top tenants list is very strong, including only a few sub-investment grade-rated tenants like Albertsons ( ACI ) and Petsmart. And if the Kroger ( KR )-Albertsons merger closes, then IVT's will have an even higher share of investment grade tenancy.

{kind=link}

IVT's portfolio is overwhelmingly geared toward essential rather than discretionary retail. But with strong locations, vacancies here and there are not terribly threatening to long-term results, as the high demand from retailers for BB&B's former spaces illustrates.

It's important to note here that IVT's portfolio is not only recession-resistant, it is also resilient against inflation. Regularly expiring leases allows the landlord to raise rents at these high-demand centers. This allows revenue growth to keep up with inflation as well as rising interest expenses on maturing debt.

Balance Sheet Strength

IVT's barely investment grade credit rating of BBB- does not fully reflect its balance sheet strength, and it would not be surprising to see an upgrade to BBB once its secured debt maturing over the next few years is refinanced with unsecured loans with longer terms.

IVT is highly liquid with $107 million in cash plus $350 million of available capacity on the credit revolver.

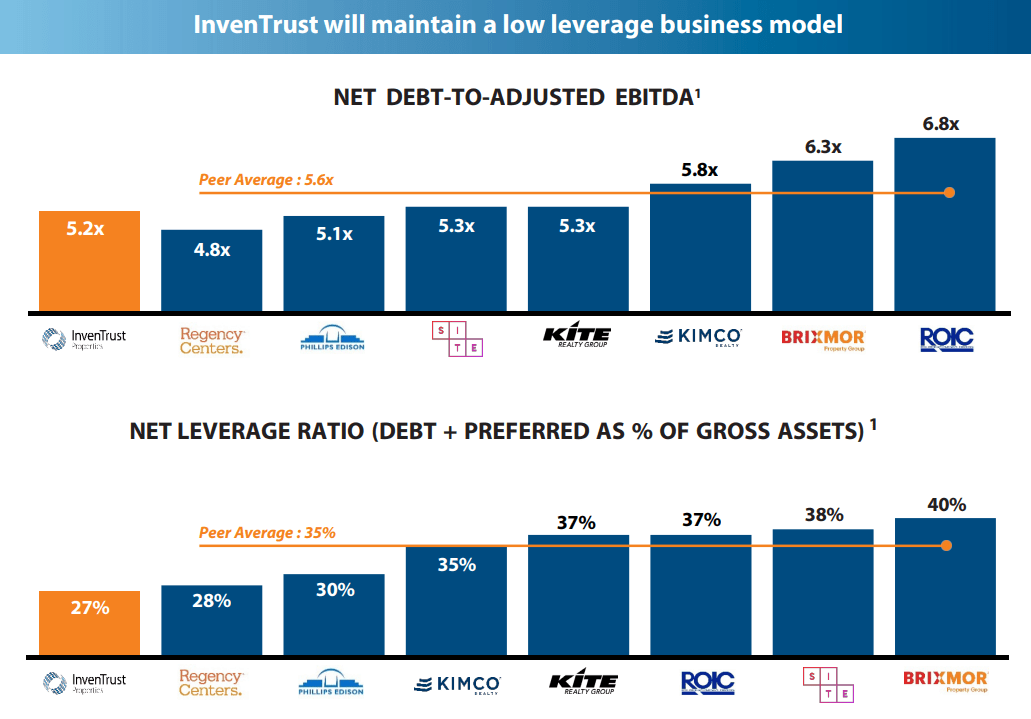

It also enjoys among the lowest leverage metrics of any retail REIT:

{kind=link}

A large contributor to IVT's net debt to EBITDA ratio falling on the low end of its peer group is its 10.4% YoY EBITDA growth in Q3 2023 and 8.9% growth YTD.

But the REIT is also simply low-leveraged, as we can see in the second chart above. Its net leverage ratio is the lowest in the retail REIT peer group.

Two-thirds of IVT's total capitalization is in the form of common equity, while 8% is secured debt tied to the properties purchased out of its former joint venture.

IVT November Presentation

When we look at IVT's debt maturity schedule below, we find that the vast majority of its debt (1) is unsecured and (2) does not mature until 2026 and after.

IVT November Presentation

In October (after the end of Q3), IVT executed a one-year extension on the $92 million secured, multi-property loan that was set to mature in 2023. In the process, that debt became floating rate.

Considering this loan extension, IVT's total floating rate debt rose from 2% of total debt to 10%, and its weighted average interest rate jumped from 3.88% to 4.33%. That is because IVT's floating rate debt currently sports an effective interest rate of around 7%.

Keep in mind that this floating rate debt will probably be eliminated next year at maturity, if not sooner. IVT has $107 million in cash that can be used to retire this debt. Plus, it is widely expected that the Fed will lower the Fed Funds Rate over the course of 2024, which will lower the effective rate on IVT's floating rate debt.

Dividend Growth & Coverage

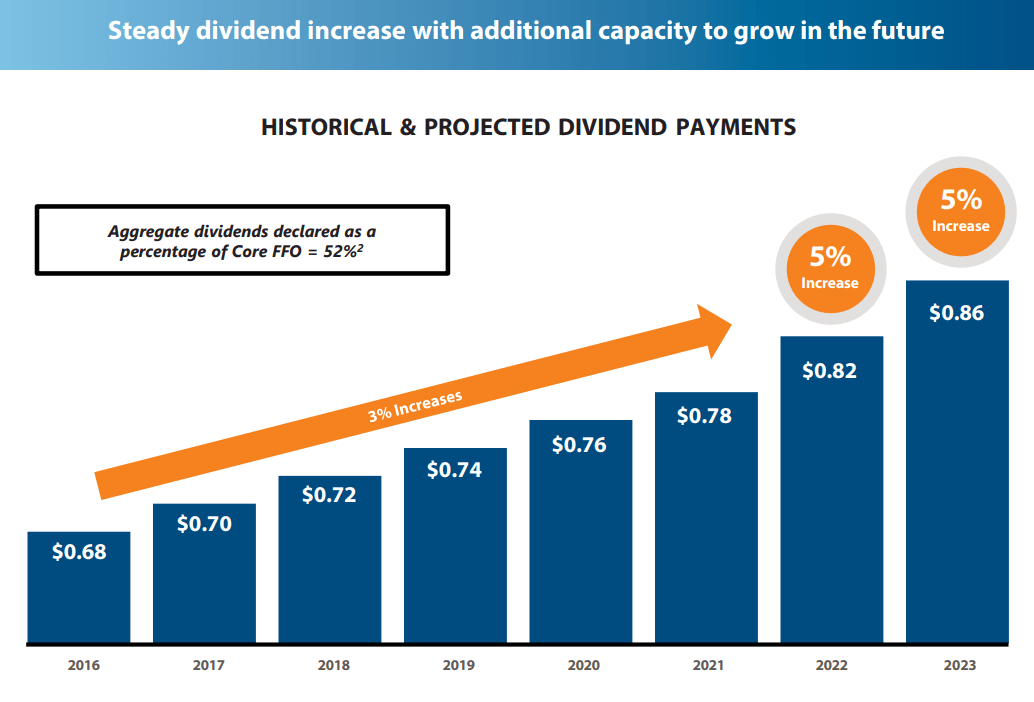

IVT has an impressively steady record of regular dividend growth, including through the COVID-19 pandemic. This is saying something, since many other retail REITs had to cut their dividends during the pandemic. The lack of pandemic-era dividend cut signifies the overwhelming essentiality of IVT's tenant industries, as only "essential retail" were allowed to remain open for a period of the COVID lockdowns.

{kind=link}

However, measuring the payout ratio by core FFO is a bit misleading. While core FFO adjusts for straight-line rent, it does not include maintenance or investment capital expenditures.

By my calculations, IVT's AFFO per share (core FFO minus maintenance capex) for Q3 2023 came in at $0.28. That brings the cash payout ratio to 77% for the third quarter.

Likewise, YTD AFFO per share of $0.90 brings the YTD cash payout ratio to 72%.

Last year, IVT generated $0.29 in AFFO per share in Q3 and $0.96 in the first three quarters of 2022, which means AFFO per share has dropped slightly this year, both in Q3 and YTD. Note, however, that IVT was a net seller of real estate for much of 2022. This entirely explains the earnings decline.

As for free cash flow (core FFO minus maintenance and investment capex), IVT generated $0.27 per share in Q3 and $0.85 YTD, which gives it a free cash payout ratio of 80% in Q3 and 76% YTD.

Last year, IVT generated $0.25 in FCF per share in Q3 (82% free cash payout ratio) and $0.82 YTD (75% free cash payout ratio). So FCF per share grew 8% in Q3 2023 and 3.7% in the first three quarters of 2023.

Rather than core FFO, which does not account for maintenance and leasing costs, I believe IVT's dividend will grow more or less in line with its FCF going forward.

Bottom Line

Adding up all the puts and takes, it looks like IVT will be able to consistently generate at least mid-single-digit growth going forward. Most of that growth will come organically from its portfolio, supplemented by opportunistic property acquisitions.

While I am by no means backing up the truck, I am willing to pay up for quality. And I view IVT as the highest quality option in the retail REIT space. Its portfolio is well-located and highly desirable, its balance sheet is strong and low-leveraged, and it has the right management team in place to execute on its conservative growth strategy.

If you want high upside or fast growth, IVT probably isn't the REIT for you. But if you want ultra sleep-well-at-night stability and steady dividend growth, consider IVT.

For further details see:

InvenTrust Properties: Low-Risk, Essential Retail Compounder