TC - Investing In Tomorrow's Skyways: Uncovering The Value Of Eve

2023-03-22 14:31:24 ET

Summary

- The company has an impressive potential order book, outperforming competitors with around 2.8k units, approximately US$8.3 billion, and a 25% market share.

- Strong backing from Embraer allows Eve to leverage the aerospace giant's expertise and infrastructure, reducing short-term Capex and operational costs.

- The total addressable market for eVTOLs is projected to surpass US$1 trillion by 2040 for passenger demand alone and up to US$3 trillion when including cargo and military applications.

I believe that investing in Eve Holding (EVEX) is a wise decision, and I base this opinion on several key factors. Firstly, Eve's impressive potential order book, which contains approximately 2.8k units or around US$8.3 billion, outperforms its competitors and signifies a 25% market share. This prominent position in the market makes Eve an attractive investment opportunity.

Secondly, the strong backing from Embraer, which owns about 90% of Eve's stake, sets the company apart from its peers. Embraer not only provides financial support but also acts as a service provider to Eve. This relationship allows Eve to operate with lower operational costs during its initial phases, which is a significant advantage in a competitive market.

Thirdly, the total addressable market for eVTOL (electric Vertical Takeoff and Landing) vehicles is projected to surpass US$1 trillion by 2040, considering only passenger demand. When accounting for cargo and military applications, this figure could potentially reach up to US$3 trillion. This vast market opportunity demonstrates the immense growth potential for companies like Eve that are leading the way in eVTOL technology.

However, it is crucial to acknowledge the inherent uncertainties and risks associated with investing in a nascent industry such as eVTOL. The certification process and widespread adoption of eVTOL vehicles remain significant question marks, which could negatively impact our forecasts. Despite these uncertainties, I maintain a positive view of both the company and the eVTOL segment as a whole, and I am confident that my buy rating on Eve is well-founded.

Company Description

{kind=link}

Eve Air Mobility, an Embraer subsidiary holding around 89% share, was founded in October 2020 to develop electric vertical take-off and landing (eVTOL) aircraft for urban air mobility. The company is seeking certification from Brazil's ANAC, which has agreements with the FAA and EASA. Eve aims to both deliver aircraft and provide services, with its eVTOL set to debut in 2026. In 2022, Embraer successfully spun off Eve through a SPAC merger with Zanite Acquisition Corp, and the company began trading on the NYSE on May 10th, 2022. However, the stock currently has a limited daily trading volume of less than US$1 million.

Milestones and Catalysts

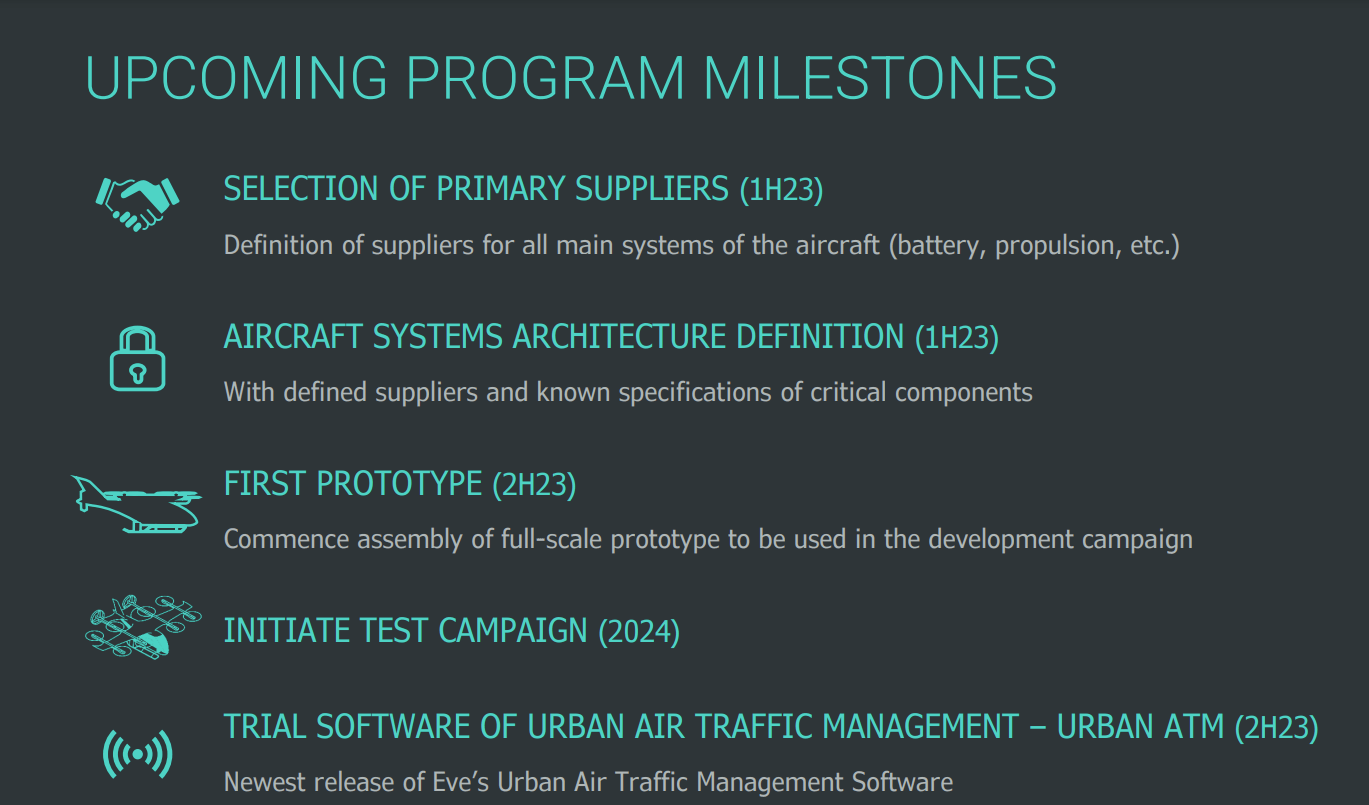

In 2022, Eve achieved several significant milestones in the development of its eVTOL aircraft . The company conducted helicopter flight tests and simulations in Rio and Chicago, demonstrating the viability of the aircraft's concept of operations. Additionally, Eve formalized the type certification application with ANAC, Brazil's FAA.

Looking ahead, Eve has several upcoming milestones that are expected to bring the company closer to commercial operations. In the first half of 2023, the company is expected to select suppliers of main systems such as batteries and propulsion and commence assembly of its first full-scale prototype in the second half of 2023. The test campaign is expected to begin in 2024, and a trial software of urban air traffic management is also planned for the second half of 2023.

Investment Thesis

{kind=link}

Source

Capitalizing on Embraer's Expertise for a Competitive Edge

I believe Eve Air Mobility is poised to be a frontrunner in the Urban Air Mobility (UAM) market, thanks to its strong support from Embraer. As a spin-off from one of the world's leading aircraft Original Equipment Manufacturers (OEMs), Eve can leverage Embraer's over 50 years of aerospace expertise and infrastructure through a service agreement. This enables Eve to rely on Embraer's plants and workforce, reducing short-term capital expenditures and operational costs compared to competitors.

I believe that investing in Eve is a cheaper way to gain exposure to Embraer ( ERJ ), even though I have a relatively optimistic outlook on ERJ. This is because Embraer currently owns almost 90% of Eve, which is worth around US$1.3 billion, representing around 55% of Embraer's current market cap of US$2.4 billion.

My analysis suggests that Embraer's valuation ex-Eve appears distorted, with a current EV/EBITDA of only 3.2x 23e, compared to its 5-year average valuation of 8.6x EV/EBITDA. This implies that Embraer's ex-Eve value is worth US$1.05 billion.

I believe that the value gap between Eve and Embraer is due to Eve's liquidity, with the stock trading less than US$1 million daily. Additionally, different investors have different focuses, with Embraer investors wanting to see the company reducing leverage and increasing profitability, while Eve shareholders want to invest in a fast-growing, disruptive company rather than buying Embraer and carrying a turn-around case.

Market Leader with First-Class Partners and a Robust Order Book

{kind=link}

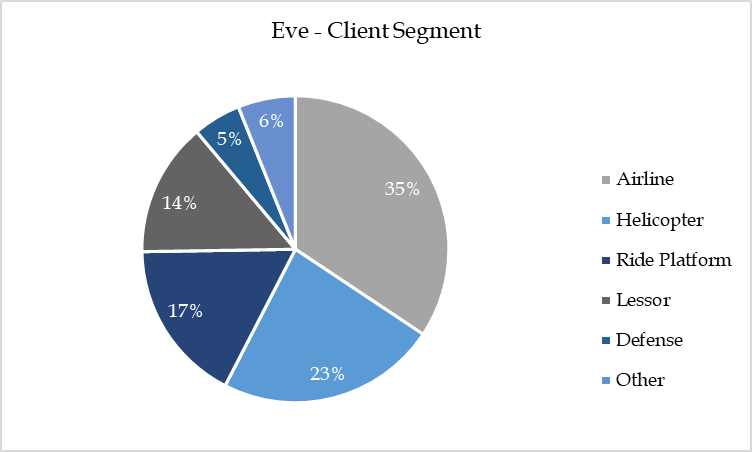

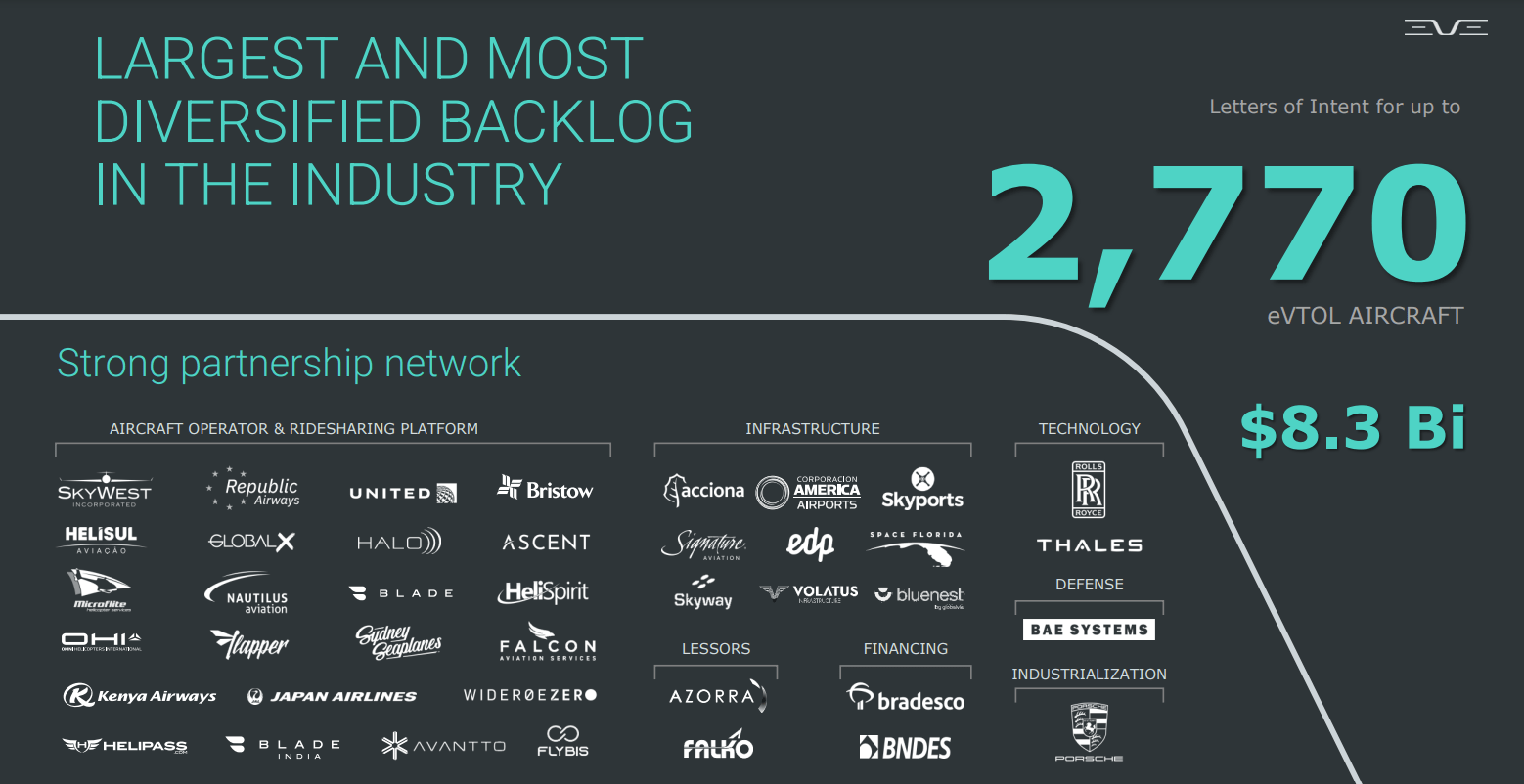

Eve stands out with the highest number of potential orders in the industry, totaling approximately 2.8k eVTOLs or around US$8.3 billion, considering an average price of US$3 million per unit. This translates to a 23% market share of total potential orders, as per SMG Consulting data . Moreover, these orders come from high-quality clients across diverse business segments, with no single client representing more than 15% of potential orders.

Tapping into a Trillion-Dollar Market Opportunity

{kind=link}

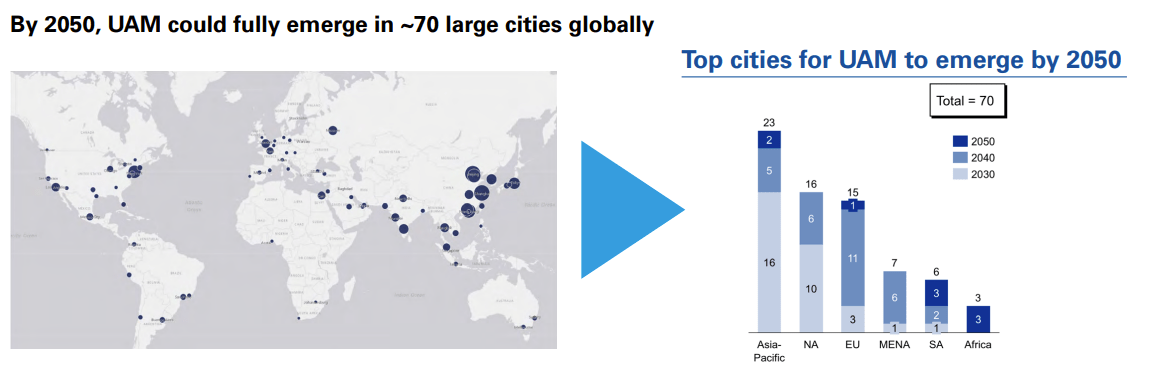

As a strong player in the growing UAM and eVTOL market, Eve is set to benefit from the numerous advantages of eVTOL aircraft, including lower noise, zero emissions, enhanced safety, and future autonomous capabilities. These benefits position eVTOLs to gain market share from helicopters, especially in congested metropolitan areas. The eVTOL market could potentially double or triple the size of the helicopter market within the next decade, reaching US$75-100 billion per year. According to KPMG and Morgan Stanley , the eVTOL passenger market could range between US$1.0 trillion over the next few decades and exceed US$1 trillion when considering medical, cargo, defense, and autonomous applications.

I believe that Eve has the potential to become one of the leading companies in the Urban Air Mobility ((UAM)) market due to its strong support from Embraer. This support comes from a master services agreement that allows Eve to leverage Embraer's expertise and infrastructure, reducing its short-term capital expenditures and operational costs.

Eve was born as a spin-off from Embraer, which has over 50 years of experience in developing and certifying aircraft and has delivered over 1.7k commercial aircraft since its creation. In 2021, Embraer and Eve entered into a master services agreement that outlines the products and services Embraer provides to Eve. This agreement allows Eve to rely on Embraer's existing infrastructure, know-how, and workforce.

The master services agreement includes eVTOL Integrated Product Development, which involves up to the Type Certificate ((TC)) approval and support for aircraft approval and certification with ANAC, FAA, and EASA. It also covers UAM Business Services development, such as parts planning, technical support, MRO planning, training, and operation services. Additionally, Eve has a royalty-free license to Embraer's background intellectual property, and the agreement prohibits Eve from signing agreements with third parties for any of the services or products other than Embraer for the ones specified in the agreements.

The agreement states that Eve will pay for the use of Embraer's services on a daily or hourly basis, usually after 45 days. There is also an exclusivity clause that prohibits Eve from signing agreements with third parties for any of the services or products other than Embraer for the ones specified in the agreements.

Minimizing Certification Risks

In my view, Eve's aircraft design minimizes certification risk, which could be a significant catalyst for the company's success. As eVTOL aircraft increase the number of rotors, they become more complex to certify and operate. However, Eve's multi-rotor aircraft design includes 10 rotors in total, including 2 pushers and 8 lifters without tilting parts, which should help to facilitate its aircraft certification.

Eve's plan is to certify its eVTOL with the Brazilian Aviation Authority (ANAC), which will provide undivided attention from the regulator. This approach is different from peers such as Joby ( JOBY ) and Archer ( ACHR ), who are competing for FAA and EASA attention. Once certified by ANAC, Eve's eVTOL can be smoothly certified by FAA and EASA. Additionally, Eve will have the support of Embraer throughout its certification process. Embraer has certified over 30 aircraft models in the last 25 years, which provides Eve with additional expertise and support.

When comparing Eve's peers, Joby and Archer are developing models with 6 and 12 rotors, respectively, which are likely more straightforward to certify than more complex models like Lilium. Lilium's aircraft consists of 30 ducted vector thrust rotors that could increase vehicle aerodynamics but could also heighten certification and operational risk. This type of technology has never been certified before, which could create challenges for Lilium.

An ESG-Friendly Investment with Low Carbon Emissions

One of the key growth drivers for the eVTOL industry is its potential to significantly reduce CO2 emissions compared to traditional aircraft. As eVTOLs are fully electric, they emit zero emissions during operation and have the potential to reduce traffic congestion in large cities, further reducing emissions.

Replacing helicopters with eVTOLs is expected to speed up in the mid-term, especially in urban areas, given the low emission of eVTOLs. This is significant as helicopters have an average fuel burn rate of 20 gallons/hour (76 liters/hour), as per the linked source .

Moreover, according to McKinsey, 99% of a typical narrowbody aircraft lifecycle CO2 emissions come from fuel , including its combustion and sourcing. The remaining 1% is related to aircraft manufacturing, assembly, maintenance, or the materials used in these processes. This underscores the critical role that battery-electric propulsion used by eVTOLs can play in the aviation industry's decarbonization efforts.

Valuation

I have set my December 2023 price target for EVEX US at US$8.00, which is derived by a blended average of three valuation methods: EV/Revenues, EV/EBITDA, and market share approach, with equal weighting. This valuation uses fully diluted shares, which includes the conversion of all warrants available, leading to a total of 295mn shares versus 269mn currently.

For EV/Revenues, I apply a 3x multiple to Eve's year-end 2029 revenue of US$3.1bn, adjusting for the company's net debt at the time, arriving at a market cap of US$8.05bn. Discounting back at a 30% rate for five years to 2023, I arrive at a value per share of US$7.35.

For EV/EBITDA, I apply a 15x multiple to year-end 2029 EBITDA of US$462mn, adjusting for the company's net debt at the time, leading to a market cap of US$5.75bn. Discounting back at a 30% rate for five years to 2023, I arrive at a value of US$5.25 per share.

The 3x sales multiple and 15x EBITDA multiple are in line with the ones used on the valuation of similar companies in the segment, such as Lilium ( LILM ), Archer, and Joby, which are also pre-operational and reflect the risks regarding aircraft certification and infrastructure development. This methodology is similar to that used for new-to-market clean technology and clean energy providers in general, including electric vehicle companies and other cleantech providers of batteries and fuel cells.

However, it is essential to note that Eve is not expected to become profitable for some years after the projected certification, which is expected in 2026. Moreover, there is significant execution risk between now and mid-decade, and unanticipated changes to the competitive landscape could negatively impact the future-state business model.

Nonetheless, I believe that our price target of US$8.00 is reasonable given the blended average of the three valuation methods and the risks associated with the pre-operational nature of the company. I believe that as Eve progresses towards certification and begins commercial operations, my valuation could be revised upward, providing significant upside potential for investors.

Investment Risks

Navigating the Uncertainties of a Nascent Industry

Eve Air Mobility faces challenges as it operates within an infant industry with limited visibility on the total addressable market (TAM). The company's success depends not only on developing its eVTOL aircraft but also on the parallel growth of the entire eVTOL infrastructure ecosystem. This includes air traffic control, vertiports, supply chain, and certification processes. Delays or setbacks in any of these areas could slow market development or reduce the expected market size. Furthermore, security concerns and consumer adoption could impact the company's potential market reach.

Navigating the Certification Process

Eve is currently pursuing certification from ANAC, Brazil's Aviation Agency. However, there is a risk that the company may not receive approval on schedule, which could lead to potential order cancellations and delays in generating free cash flow (FCF). Additionally, validating ANAC certification with US and European agencies in a timely manner is crucial; failure to do so could result in delayed deliveries and FCF expectations.

Addressing Capital Requirements in a Developing Market

As Eve's eVTOL development and the UAM market are in their early stages, accurately forecasting the company's mid-term cash needs is challenging. This could result in the necessity for additional capital through equity or debt raises, potentially diluting shareholder value.

Currently, Eve holds a cash position of around US$250 million and a $0.00 total debt. Management is estimating its strong cash position to be sufficient for capital needs until 2025, assuming no additional debt. This means the company is totally unleveraged and will not take on any leverage for the next few years. In other words, they have no debt and do not plan on taking any more debt anytime soon because their cash position will finance everything in the coming years.

Preparing for Intense Competition

With over 15 companies, such as Joby, Archer, and Lilium, actively developing eVTOL aircraft, competition in the market may be more intense than anticipated. These companies focus on various aircraft sizes, ranges, and propulsion systems, and heightened competition could result in lower-than-expected market share or returns for Eve.

In Brief

Investing in Eve presents a promising opportunity, thanks to its remarkable potential order book, strong backing from Embraer, and the massive growth potential in the eVTOL market. With a 25% market share and lower operational costs, Eve stands out among its competitors. The total addressable market for eVTOLs is projected to reach up to US$3 trillion by 2040, indicating substantial prospects for companies leading the charge in this sector. However, it is essential to recognize the inherent risks and uncertainties in the nascent eVTOL industry, such as the certification process and widespread adoption. Despite these challenges, I maintain a positive outlook on Eve and the eVTOL segment, confident in my Dec-23 price target of $8.00 and my buy rating for Eve.

For further details see:

Investing In Tomorrow's Skyways: Uncovering The Value Of Eve