NVTA - Invitae Needs More Meaningful Progress

2023-05-10 11:15:04 ET

Summary

- Invitae reports limited Q1 beats as expectations drop.

- Guidance maintained, but cash burn still high.

- Another capital raise may be needed for future growth.

After the bell on Tuesday, we received first quarter results from genetics company Invitae (NVTA). Shares of the company have crashed more than 97% from their late 2020 peak as management was forced to curtail growth in order to keep the company running. While Q1 results were decent, guidance was only maintained for the year, with the company needing to make more progress for investors to truly believe.

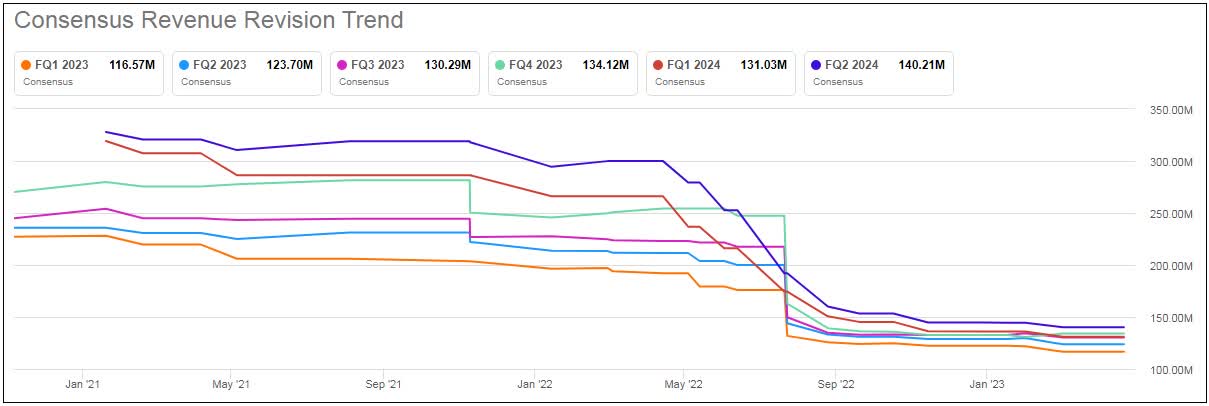

For Q1, Invitae reported revenues of more than $117.3 million, coming in a little less than a million dollars above street estimates. The reported figure was a decline of just over 5.1% from the year ago period. However, it's important to note that expectations have dropped considerably in recent years, as the major restructuring plan put a huge dent in growth plans. The graphic below shows just how much revenue estimates for this quarter and some futures periods have come down over the past two years.

Invitae Revenue Estimate Revisions (Seeking Alpha)

{kind=link}

Restructuring efforts are starting to pay off. GAAP gross margin was 24.6% in the quarter, as compared with 21.5% in the first quarter of 2022. Non-GAAP gross margin was 47.9% in the quarter, as compared with 36.6% in the first quarter of 2022. The company's operating loss narrowed to $175 million in the quarter from $213 million a year earlier, and this year's period included more than $52 million in restructuring expenses. Non-GAAP losses per share were $0.37 in the period, beating street estimates by 3 cents.

These continued large losses have led to significant cash burn over time, which has resulted in a lot of debt and equity raises for Invitae. Total cash and investments were down to about $389 million at the end of Q1, compared to $557.1 million at the end of last year. Cash burn from ongoing activities was down to roughly $51 million in the period, but the overall balance dropped mainly due to a repayment of the company's $135 million term loan. Invitae also has more than a billion dollars' worth of convertible notes here that mature by the end of 2028, so overall it is in a large net debt position.

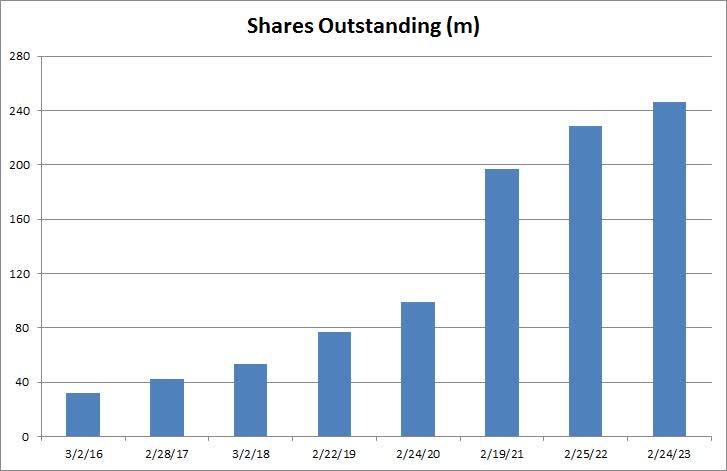

Prior to the restructuring, Invitae had made some acquisitions to bolster its growth profile. Between those deals and the equity raises, the company's outstanding share count has been surging year over year. The graphic below shows that situation based on the company's annual 10-K filings. However, the newest 10-Q filing now details that the number of shares as of May 5th is over 260 million. Ongoing stock based compensation will mean that the share count will continue higher moving forward.

Invitae Shares Outstanding (Company filings)

{kind=link}

When it comes to guidance, there weren't any major surprises. Management is expecting 2023 revenue to be over $500 million, which would represent low double digit growth compared to 2022 pro forma revenue. That forecast remains unchanged, although street estimates have come down by another $14 million to $504 million since my previous article on the name. It would have been nice to get a more concrete number for guidance or see the forecast raised, but that did not happen.

Ongoing cash burn is expected to be in a range of $250 million to $275 million for 2023. Management has talked about a cash runway lasting into and perhaps through 2024, but it wouldn't be a surprise to see an equity raise again at some point. At the moment, Invitae would be raising funds from a point of extreme weakness. Perhaps if results improve a bit more in the coming quarters and the stock jumps, funds could be raised at a higher valuation which would limit future dilution.

After the Q1 report, Invitae shares dropped more than 4% to $1.53. Going into the news, the average price target on the street was $2.26, implying significant upside from current levels. A year ago, however, that average valuation metric was more than $17, and two years ago it was well into the $50s. One key that I'll be watching is the 50-day moving average (purple line below), which shares recently bounced above. If shares hold this line and the 50-day starts rising again, it could become a support level. If shares drop back below it, however, more technical selling pressure could be seen.

{kind=link}

In the end, Invitae announced a decent set of Q1 results, but it wasn't enough for investors. The stock has recently bounced significantly (in percentage terms) from its multi-year low of $1.17. Q1 results beat heavily reduced street estimates, and management did reiterate its guidance for the year. Cash burn is certainly improving, but the balance sheet is in poor shape and investors have been facing tremendous dilution over time. This company is certainly looking better than it did in recent quarters, but results need to improve a bit more before I would consider recommending it as even a very speculative buy.

For further details see:

Invitae Needs More Meaningful Progress