NVTA - Invitae: Revenue Troubles Build

2023-08-09 10:33:26 ET

Summary

- Invitae's shares have plummeted as the company slashed its growth forecast to avoid bankruptcy.

- Revenue for Q2 was slightly above estimates but down 12% YoY, and analyst revenue estimates have significantly declined.

- The company's financials remain concerning, with ongoing losses and cash burn, potentially necessitating a capital raise.

After the bell on Tuesday, we received second quarter results from genetics company Invitae ( NVTA ). Shares of the company have crashed from their late 2020 peak as management was forced to slash its growth forecast to avoid bankruptcy. While efforts to preserve cash are improving, the revenue picture is only getting worse, which could send shares below a key threshold.

My worry with the company over the years has primarily started with its revenue growth picture that has not lived up to the hype. For Q2, the company reported revenues of $120.5 million. This number was slightly above street estimates but was also down almost 12% over the prior year period due to divestitures. Excluding exited businesses, the topline would have grown by roughly 1%, which isn't exactly tremendous. Just two years ago, analysts were calling for over $231 million in total sales for this Q2 period, so topline expectations had nearly been cut in half.

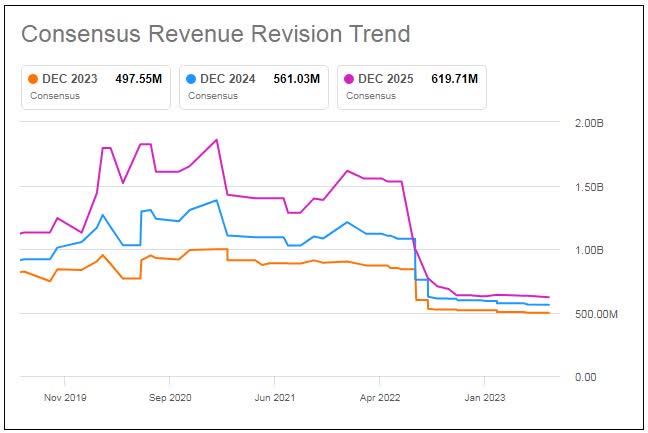

Analyst revenue estimates for the company have come down significantly in recent quarters, as seen in the graphic below. Even though the 2023 average street estimate declined by another $7 million since my previous article, management found a way to disappoint yet again. 2023 revenues are now expected to be between $480 million and $500 million, compared to previous guidance for over $500 million. Analysts were looking for over $497.5 million, so the midpoint of this new forecast is a bit below that level. The new forecast likely means pro forma revenue growth this year will be in the high single digits, percentage wise, down from low double digits previously.

{kind=link}

The second issue I've had with Invitae has been its financial picture. When the company was reporting some growth in previous years, it did so with massive ongoing losses. Management has done a good job in recent quarters of limiting expenses, but they still are deep in the red. The non-GAAP net loss for the second quarter of 2023 was $78.2 million, or $0.30 per share, compared to a non-GAAP net loss of $158.5 million, or $0.68 per share, for the second quarter of 2022. The company did beat street estimates by 7 cents here for its adjusted loss.

These large losses have led to tremendous cash burn over the year. Total cash and investments were $335.6 million as of June 30, 2023, compared to $557.1 million at the end of 2022. The good news here is that ongoing cash burn is now expected to improve to the range of $220 to $245 million in 2023 from the company's previous guidance range of $250 to $275 million. However, Invitae may want to raise more capital in the next year or so as its cash position continues to dwindle. The company also has well over $1 billion in convertible notes on the balance sheet that will need to be repaid by 2028 or refinanced at what could be a very costly rate.

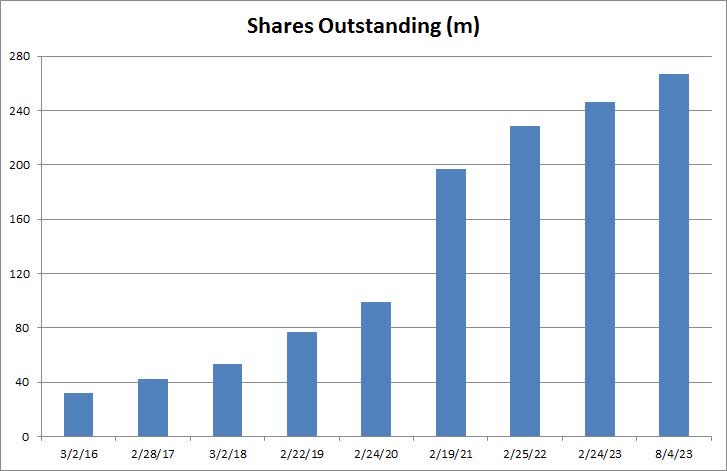

Raising more funds would only add to the significant dilution investors have faced in recent years, and is one of the key reasons why I continue to rate this stock a sell. Prior to the restructuring, Invitae had made some acquisitions to bolster its growth profile. Between those deals, needed equity raises, and the company's compensation structure, the outstanding share count has been surging. The graphic below shows that situation based on the company's annual 10-K filings and the latest 10-Q filing. As of early August , the number of shares outstanding was over 267 million. Ongoing stock-based compensation will mean that the share count will continue higher moving forward.

{kind=link}

In the after-hours session, Invitae shares were down more than 6% to $1.12. My worry here is that if the stock falls below a dollar, management may need to do a reverse split to satisfy listing requirements. We've seen a number of reverse splits in recent years in the electric vehicle space, and many of those names have dropped considerably afterward. Reverse splits usually only happen when a company is in significant financial distress, so investors worry about the increasing potential for bankruptcy.

Going into the Tuesday report, the average price target on the street was $1.95, implying a significant upside from current levels. A bit over a year ago, however, that average valuation metric was more than $17, and two-plus years ago it was well into the $50s. Since my previous article, the street has cut its average valuation by another 30 cents, and this latest revenue warning likely won't help that figure.

My continued sell rating on the stock is based off the two main themes I've covered above. The first is that revenue growth targets continue to be missed, even with dramatically reduced expectations. The second is that another capital raise will likely be needed, and this is on top of the significant dilution that's happening already. With a market cap just under $300 million now, even raising $100 million could be very painful for investors. These issues could send the stock under the key $1 level, opening up the idea of a reverse split, which is a major negative catalyst itself. For me to consider an upgrade to hold, I need to see the company start delivering some strong sustainable revenue growth along with near-zero cash burn.

In the end, the revenue problems at Invitae continued with Tuesday's Q2 report. While second quarter results were better than expected, primarily on the adjusted bottom line, management cut its yearly revenue forecast yet again. Expenses and cash burn are coming down at decent rates, but they are still large, and this balance sheet needs a lot of help moving forward. This stock could easily drop below $1 if the growth picture doesn't improve soon, at which point a reverse split could spark another leg lower.

For further details see:

Invitae: Revenue Troubles Build