NVTA - Invitae's Battle To Reignite Revenue Growth And Overcome Financial Challenges

2023-03-07 08:20:43 ET

Summary

- Invitae is facing two main challenges - assembling a coherent business model from dozens of acquisitions and avoiding a cash crunch looming in 2024/2025.

- The company has taken decisive action to address its convertible debt deal, fully repaid its senior secured term loan, and reduced its ongoing cash burn to $77 million for the quarter.

- Despite progress made in reducing cash burn and executing on its realignment plan, the company may still face a liquidity crunch, and its cost structure is not yet fully adjusted.

Addressing Invitae's Two Main Challenges: Business Model Cohesion and Cash Crunch

An update on Invitae ( NVTA ) is warranted. As I've mentioned previously, this stock was once a darling during the Covid outbreak. However, the management team's penchant for serial acquisitions, combined with an unforgiving macro environment for cash-burning stocks, led to the bubble bursting.

Now, the company is swiftly pivoting its strategy to prioritize execution and stem the cash bleeding. But let me be clear, they are not out of the woods yet. In fact, even companies in a better footing may struggle in the current macro environment.

Invitae is currently facing two main challenges. Firstly, the company must assemble a coherent business model from dozens of puzzle pieces, which have been acquired in the past couple of years. Secondly, Invitae must avoid the cash crunch that is looming in 2024/2025. The company has recently released its 4 th quarter results , and we can now see how they have addressed these challenges thus far.

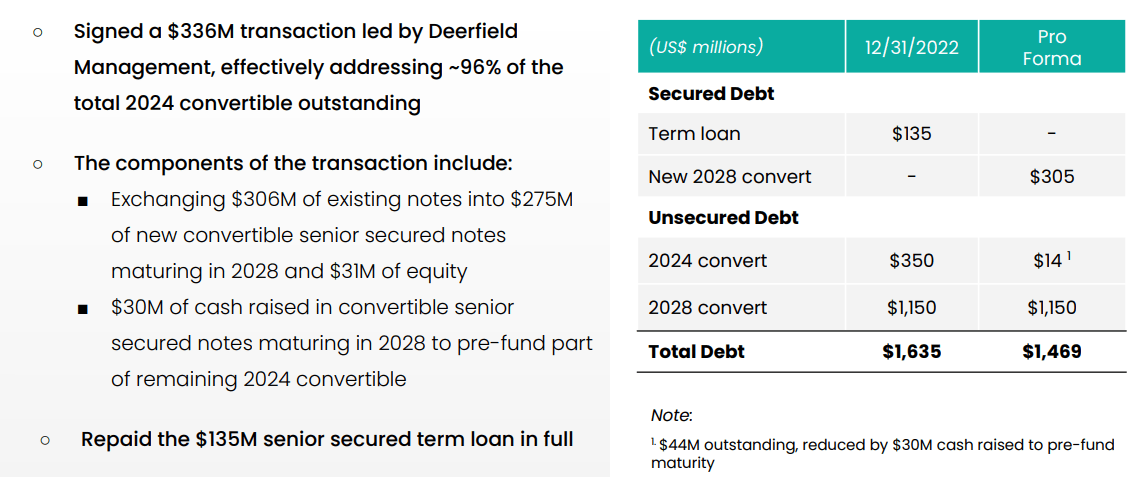

The company had convertible debt maturing in 2024, which could have been highly dilutive for shareholders. However, the company has taken decisive action to solve this first issue. The company has signed a $336 million transaction led by Deerfield Management, which effectively addresses 96% of the outstanding convertible debt deal in 2024. Investors will exchange 90% of their current 2024 notes with new senior secured notes due in 2028 and also will equitize 10% of their holdings. Additionally, the company has fully repaid the $135 million senior secured term loan, and the debt repayment is estimated to save over $15 million of interest expense.

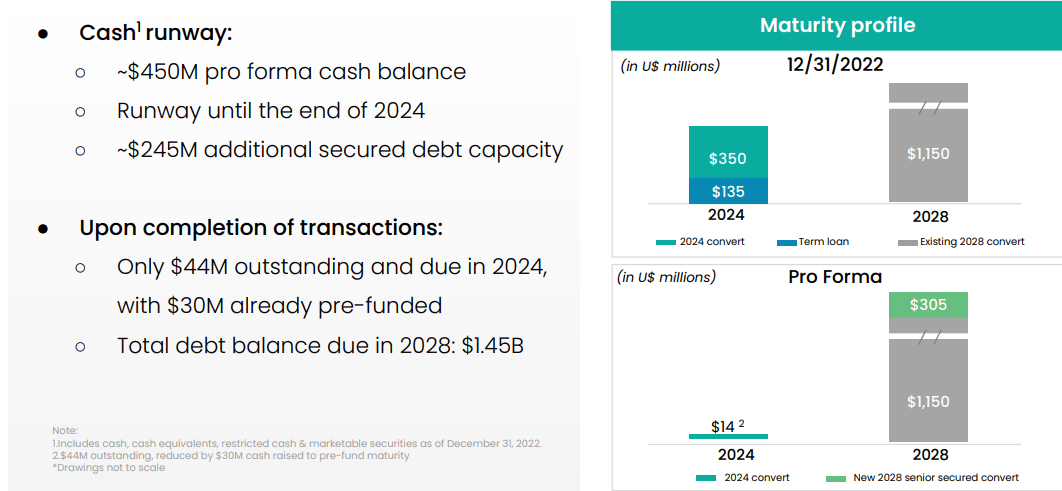

After that, the company estimates that it will have a pro forma cash balance of $450 million at the close of the debt transaction. Additionally, Invitae has approximately $245 million secured debt capacity available after the transaction, which means they have access to additional funding that they have not yet utilized. This further extends their cash runway and provides additional flexibility as they navigate their business model changes.

{kind=link}

{kind=link}

Albeit a good step, it's important to note that it merely postpones the company's financial challenges rather than solving them entirely.

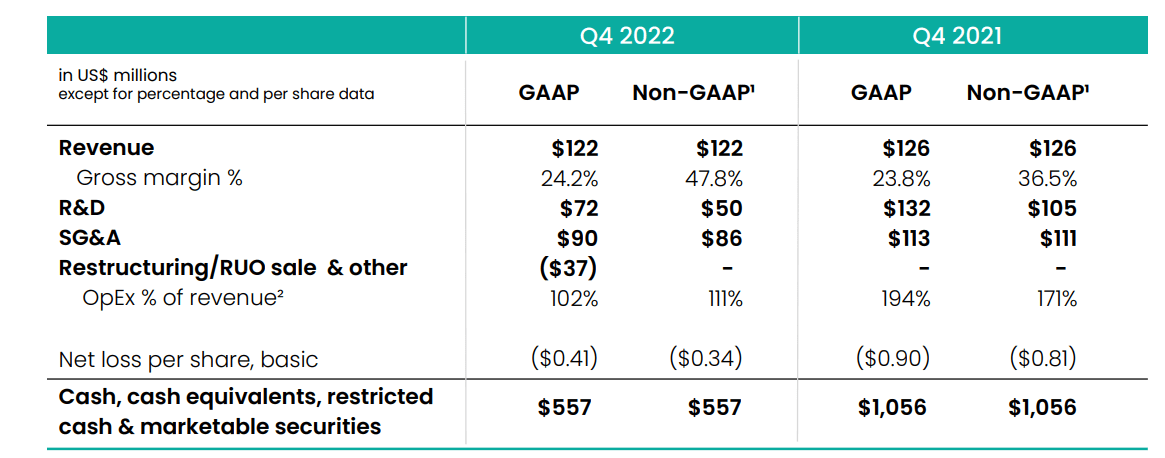

On the business side, Invitae has been taking concrete steps to reshape its cost structure. These efforts have gained momentum, with non-GAAP operating expenses reduced to roughly 111% of revenues in Q4 2022 compared to 171% in Q4 2021.

{kind=link}

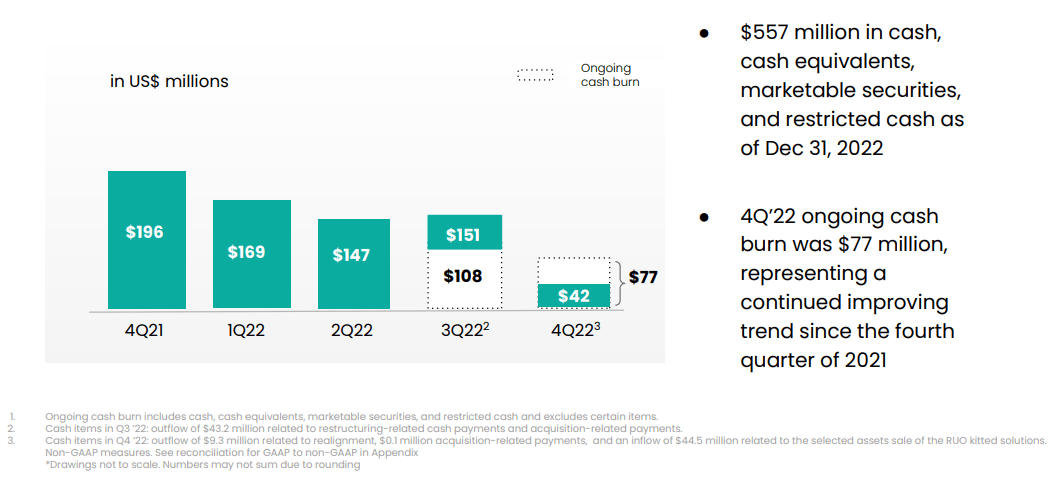

They claim to have made significant progress in its strategic realignment efforts, including the sale of certain assets related to the distributed RUO kitted solution. As a result, Invitae has been able to reduce its ongoing cash burn to $77 million for the quarter, excluding certain items. A significant reduction compared to $196 million in Q4 2021. Looking at the full-year results, we can see that Invitae has achieved 12% year-over-year growth in revenue, a non-GAAP gross margin of 42.5%, and a full-year cash burn of $510 million.

{kind=link}

Invitae's Core Businesses: Hereditary Cancer and Promising Growth Areas

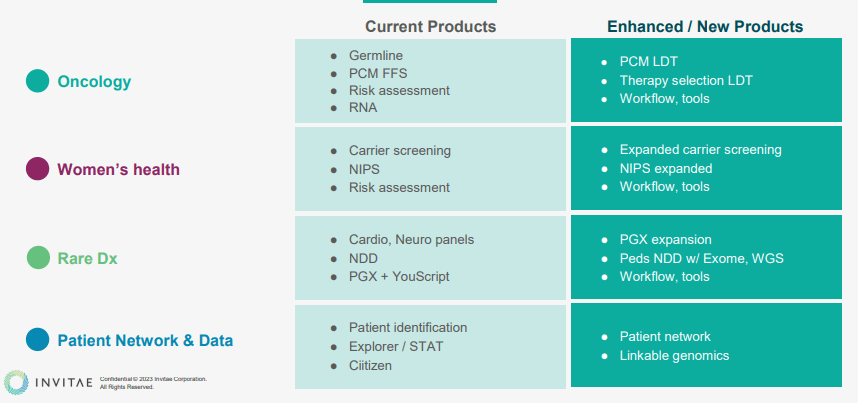

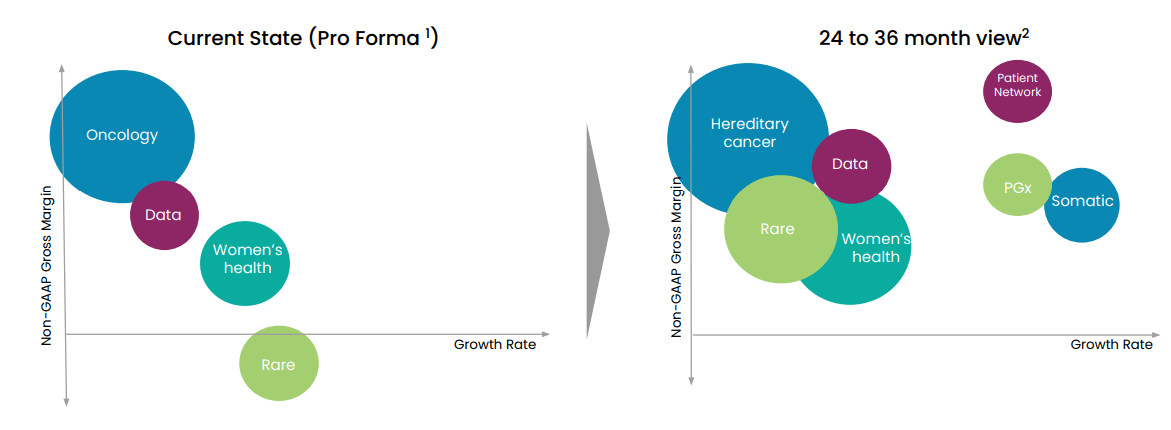

The company is betting on its core businesses, particularly hereditary cancer, to be the revenue and gross margin driver in the present. According to the CEO , the company's hereditary cancer offering is their highest revenue business, with a margin profile above their corporate average.

Looking ahead, Invitae sees growth opportunities in several areas, including somatic oncology with its minimum residual disease product, PCM, as well as in pharmacogenomics and its patient network platform. These areas represent promising opportunities for the company to reignite its revenue growth over the short to mid term.

Invitae has developed a Personalized Cancer Monitoring ((PCM)) assay that utilizes a patient's tumor to help detect minimal residual disease ((MRD)) in patients with stage I-IV cancer. By using circulating tumor DNA (ctDNA) in blood, the test provides personalized information about a patient's cancer and allows for a less invasive and more convenient way to monitor cancer progression compared to traditional methods. The company expects it to become a significant revenue driver as it moves towards positive gross margins with the benefit of reimbursement practices.

In addition, Invitae will use their pharmacogenomics offering to inform clinicians and patients of potentially dangerous drug-drug and drug-gene interactions, which can send many cancer patients to the ER unnecessarily. The company's Pharmacogenomics ((PGX)) Panel, which uses an individual's genetics to predict their response to commonly prescribed medications.

{kind=link}

{kind=link}

In my opinion, Invitae appears to be moving closer to being both a complement and a competitor to companies like Exact Sciences and Guardant Health.

Uncertain Future: Risks and Challenges for Invitae

Invitae's growth strategy was fueled by acquisitions that were financed by inflated paper stock, resulting in a lack of coherence among their offerings that could deliver synergies and reinforce growth. They tried to offer everything to everyone in the genetic testing field without real cohesion. While this could have continued and eventually sorted itself out given enough time, the new interest rate regime in 2022 changed the game.

The new management responded to the challenging environment by rolling out a realignment plan in July 2022, anticipating higher debt costs and difficulty in tapping the capital markets. The company has made some necessary decisions, including exiting certain territories and countries, resulting in the company selling products in less than a dozen countries now. As we’ve seen in the initial section, the management team has results to show.

However, the risks loom large. Despite the progress made in reducing cash-burn and executing on its realignment plan, the company may still face a liquidity crunch. Furthermore, while the refocus of its business model is underway, the continuation of revenue growth has yet to be demonstrated, and it remains to be seen if this refocus will be successful. Additionally, the company's history of serial acquisitions may continue to present challenges, and its cost structure is not yet fully adjusted. Below is a pro forma adjusted cash-burn for 2022. As you can see, the company still has a long way to go.

Author's computation based on company financials

Invitae has indicated that it expects a quarterly cash-burn of $75 million in 2023, which translates to a cash burn of $300 million for the year. Despite the balance sheet rearrangement that they have undertaken, the company can only expect a maximum of two years of cash runway. This means that they have a lot of work ahead of them to achieve a more solid financial footing.

Invitae could potentially achieve a sales multiple similar to Guardant or Exact, which could be around 5 times sales. However, considering the current state of their balance sheet and cost structure, there is also a significant risk of the company facing bankruptcy or being acquired for a low price. As a result, I believe the risk-return proposition of investing in Invitae is currently uncertain, and I am choosing to remain on the sidelines.

For further details see:

Invitae's Battle To Reignite Revenue Growth And Overcome Financial Challenges