IONQ - IonQ Has The Potential To Become A Long-Term Compounder

2023-12-29 00:44:04 ET

Summary

- IonQ is a quantum computing pure-play and is making significant technological breakthroughs.

- They have high gross margins and are experiencing increasing demand and revenue.

- They have a low cash burn rate and are currently holding a significant amount of cash and short-term investments to continue funding operations.

- I currently rate IonQ as a Buy.

Thesis

One of the things I look for with potential investments are growing companies in growing industries. IonQ, Inc. (IONQ) caught my attention several months ago. I initiated a small position in the company and planned to add to it as they reached financial milestones. However, the share price rose well above my expectations so I happily exited for a significant profit in early August.

This is an update to the two articles I previously wrote on IonQ. The article I wrote in February detailed the extensive amount of partnerships they had formed. The article I wrote in April focused more on their financials and their path to profitability. Because of the industry they are in and their high gross margins, I still believe this company has excellent potential and may eventually become a long-term compounder. I am still watching their progress because I am planning on making future investments into it as they improve their income and cash flow. After reviewing their financials and valuation, I presently rate IonQ as a Buy.

Company Background

IonQ, Inc. was founded in 2015 and is a developer of quantum computers. In addition to constructing them, they also sell access to already built machines through various cloud platforms. Time on their machines can be accessed through Amazon Braket, Microsoft's Azure Quantum, and Google's Cloud Marketplace. They also provide consulting services for the development of quantum algorithms and the design, development, and construction of specialized quantum computing systems. They are currently headquartered in College Park, Maryland.

Long-Term Trends

I found three different projected growth rates for the global quantum computing market. One expecting it to have a CAGR of 19.6% through 2030, a second one expecting a CAGR of 38.3% through 2028, and the third projecting a CAGR of 32.1% through 2030.

Guidance

Their most recent earnings call transcript revealed that demand has outpaced their expectations. I am going to cover some of the highlights from the earnings call and recommend investors read it. IonQ more than met their goal of selling their first quantum system by the end of 2023 by selling four of them.

They are currently experiencing significant demand for their AQ 35 system and view it as a stepping stone to AQ 64. IonQ agreed to sell two network node systems to the United States Air Force Research Lab for $25.5M. This should grant them a significant revenue spike when it resolves. The sale of additional systems going forward may eventually become steady enough that it becomes a stable part of quarterly revenue.

They announced two new systems. IonQ Forte Enterprise will be a rack mounted and modular grade AQ 35 system. The also announced they will be producing an AQ 64 system, which they expect to be able to solve problems that current non-quantum supercomputers cannot. They also plan on delivering either a Forte Enterprise or Tempo system for use as QuantumBasel in Switzerland. Their barium based technology has achieved AQ 29; they consider this an important milestone to reaching AQ 64.

In September, they announced they believed they would be able to reach AQ 64 through the use of error mitigation instead of full error correction. The problem of error correction is systemic to quantum computing, so I am eager to see if the method they employ for mitigation ends up being effective enough, or if they will still find themselves searching for a practical method for error correction.

IonQ holds a significant number of patents which should help preserve the moat they are establishing within their industry:

"Our patent portfolio includes 74 US issued patents plus another 163 US pending patent applications, as well as 19 international issued patents and another 111 international pending patent applications. Note that these patent portfolio figures are as of October 31st, 2023." - Thomas Kramer

They have increased their outlook for full year revenue to fall in the range of $21.2M to $22M. They are also providing guidance that they expect for Q4 revenue to land between $5.3M and $6.1M.

Overall, reading their Q3 earnings call transcript increased my confidence in their ability to continue digging their already significant technological moat. Assuming that demand continues to grow, they appear to be on a clear path toward long-term success.

Quarterly Financials

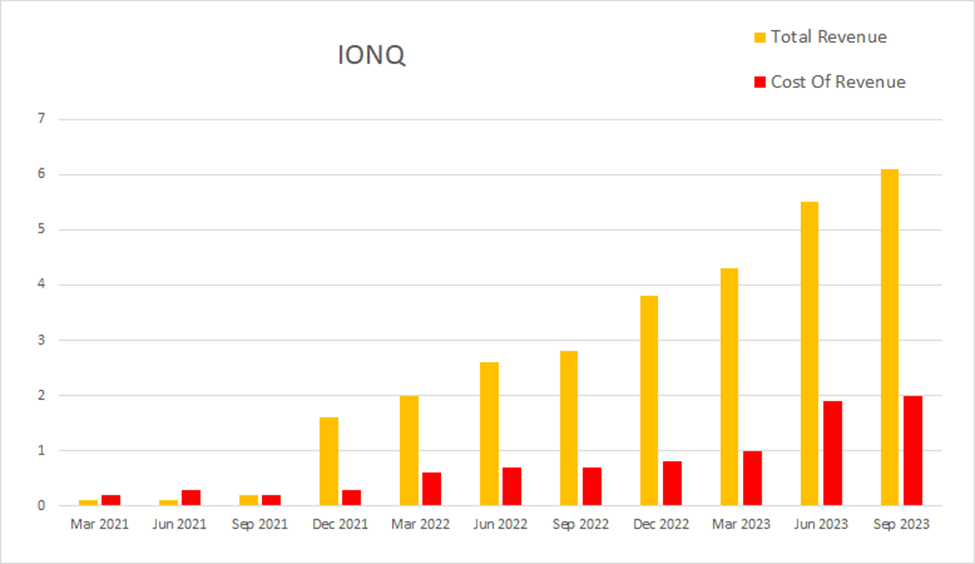

Although their revenue is still quite low, the company has achieved significant growth. Eight quarters ago IonQ had a quarterly revenue of $0.2M. Four quarters ago that had grown to $2.8M, by this most recent quarter that had further grown to $6.1M.

IONQ Quarterly Revenue (By Author)

{kind=link}

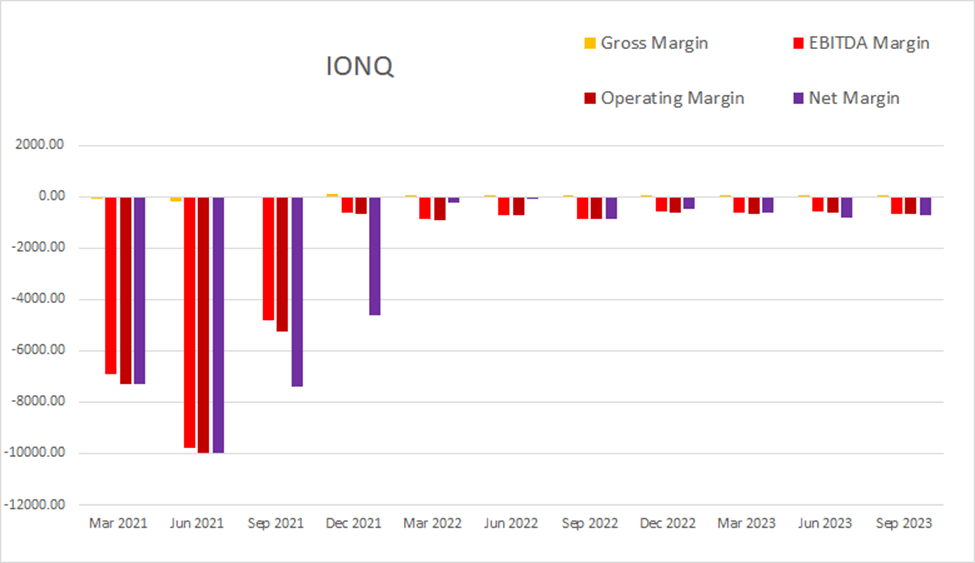

Although they have significant expenses, they also enjoy attractive gross margins. Their high gross margins are one of the primary reasons I am interested in IonQ as a potential investment. As their revenue increases, their gross profit should begin to overcome their expenses. Gross margins this strong have the potential to make them quite profitable in the future. As of the most recent quarter gross margins were 68.85%, EBITDA margins were -659%, operating margins were -691.8%, and net margins were at -734.43%.

IONQ Quarterly Margins (By Author)

{kind=link}

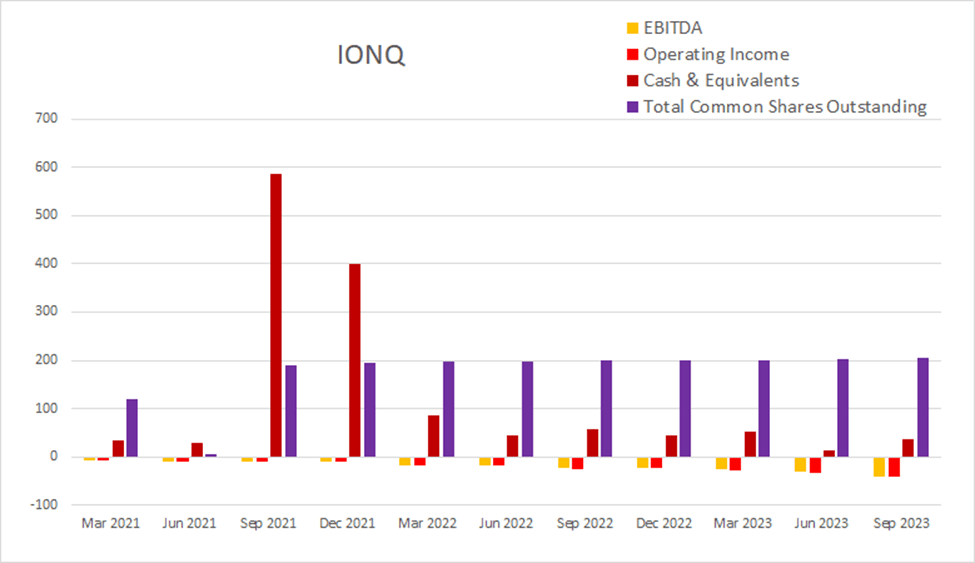

Compared to most other companies at this stage in their business life cycle, IonQ has a relatively low dilution rate. The sum of their last eight quarters of dilution comes to 7.11%; over the last four quarters this sum has dropped to 2.59%.

IONQ Quarterly Share Count vs. Cash vs. Income (By Author)

{kind=link}

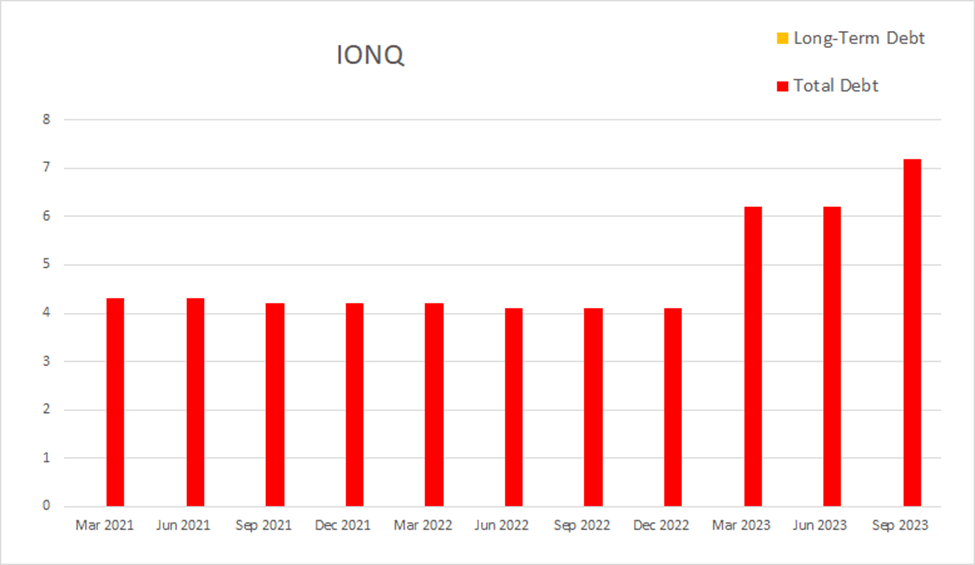

Unlike many other start-ups which are focused on growth, they do not have the burden of long-term debt. While they may have to take on debt at some point in the future, their present debt situation also helps improve their attraction as a potential long-term investment. This most recent quarter, IonQ had $5M in net interest expense and total debt was at $7.2M.

IONQ Quarterly Debt (By Author)

{kind=link}

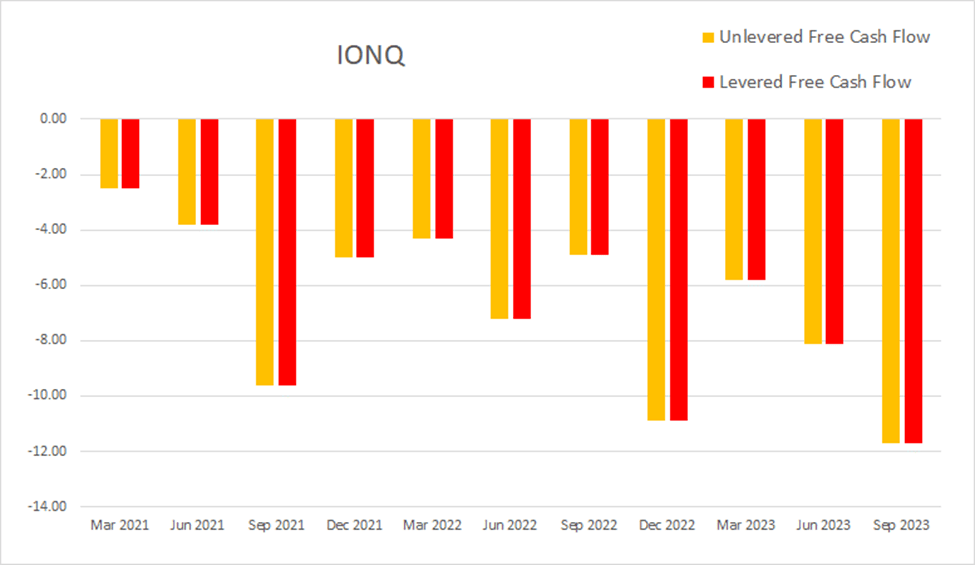

Although they have yet to achieve positive cash flow, their cash burn rate is relatively low. IonQ has a ttm levered free cash flow of -$36.5M and a reserve of total cash & short-term investments at $384M. If their cash flow trends remain stable, this would give them over ten years of runway before they need to raise more.

As of the most recent earnings report, cash and equivalents were $37M, total cash & short-term investments was at $384M, quarterly operating income was -$42M, EBITDA was -$40.2M, net income was -$44.8M, unlevered free cash flow was -$11.7M, and levered free cash flow was -$11.7M.

IONQ Quarterly Cash Flow (By Author)

{kind=link}

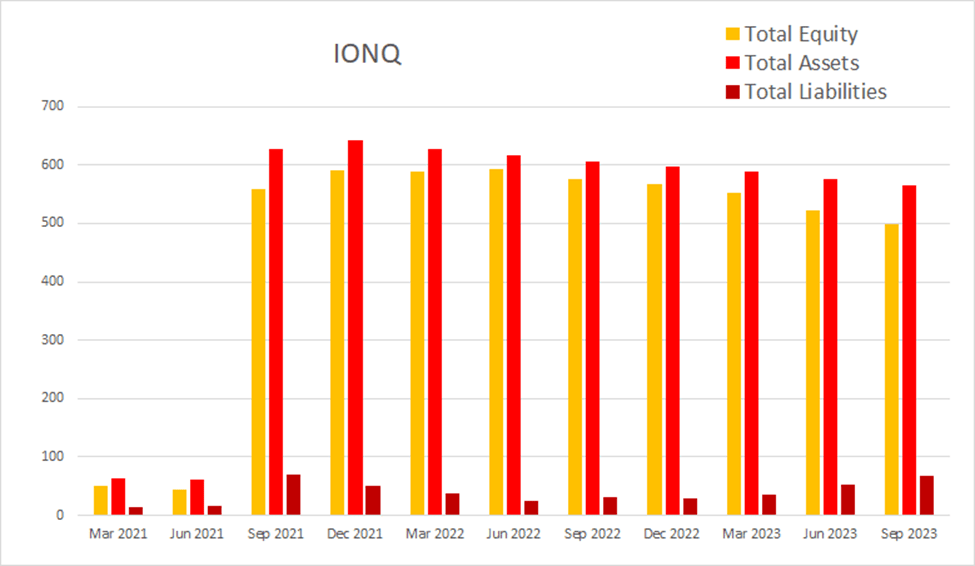

Total equity found a peak in late 2021 and has been slowly declining since then. I expect for their equity to begin rising once they improve their cash flow situation.

IONQ Quarterly Total Equity (By Author)

{kind=link}

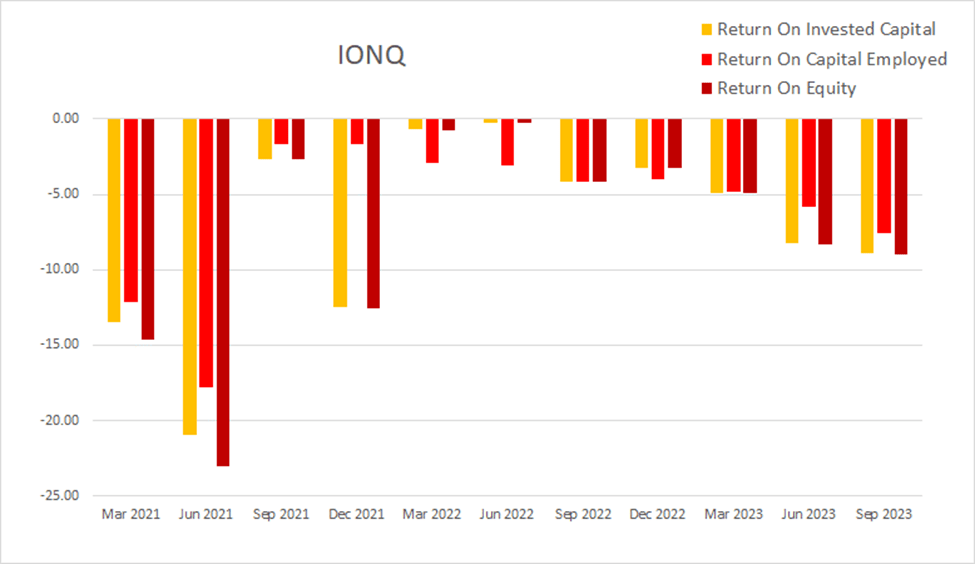

I typically search for companies with annual returns above 10% and quarterly returns above 2.5%. Because the other two are based on net income and Return On Capital Employed is based on EBIT, I wouldn't be surprised if their ROCE reaches positive values before either ROIC or ROE. As of the most recent earnings report ROIC was -8.86%, ROCE was -7.56%, and ROE was -8.99%.

IONQ Quarterly Returns (By Author)

{kind=link}

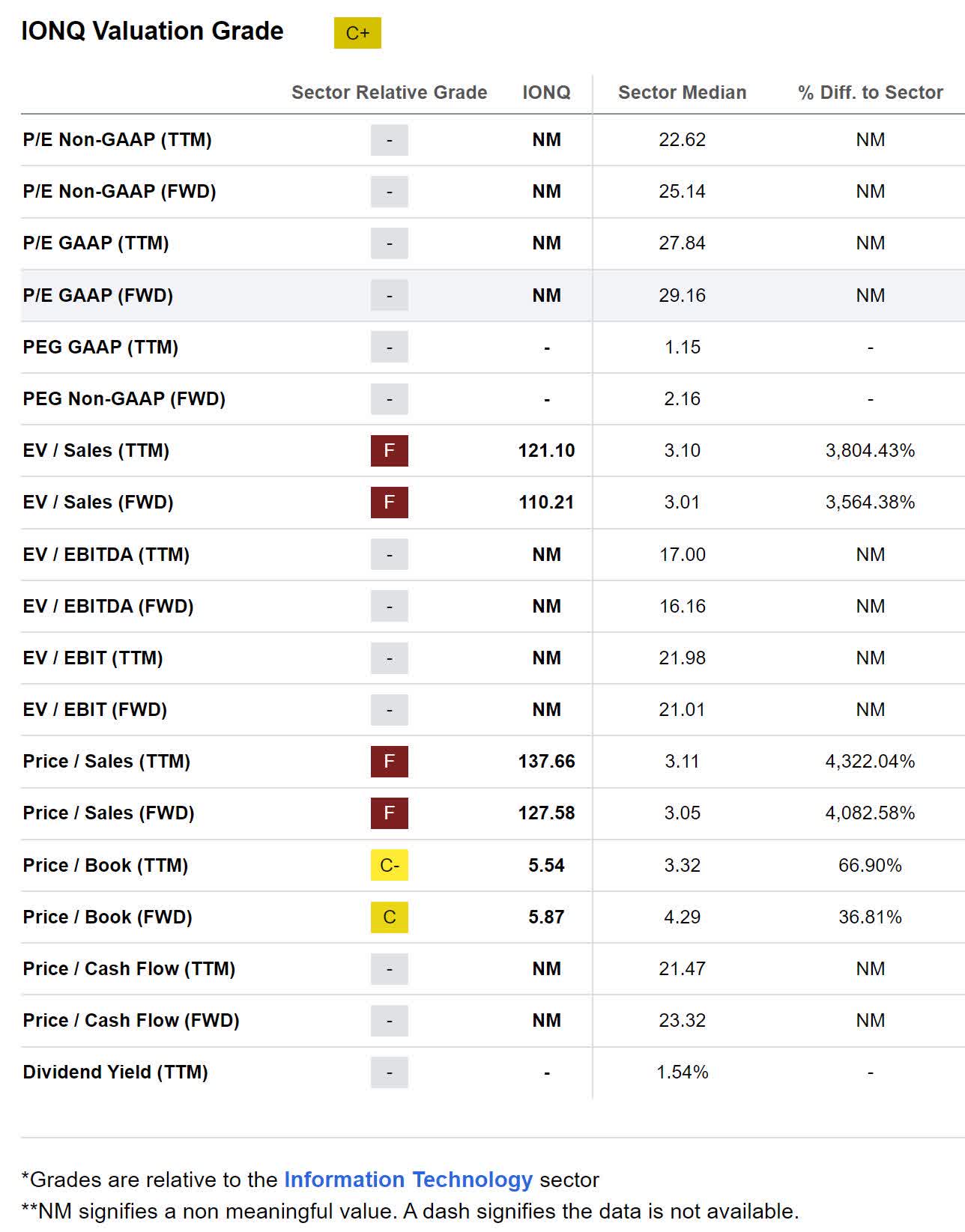

Valuation

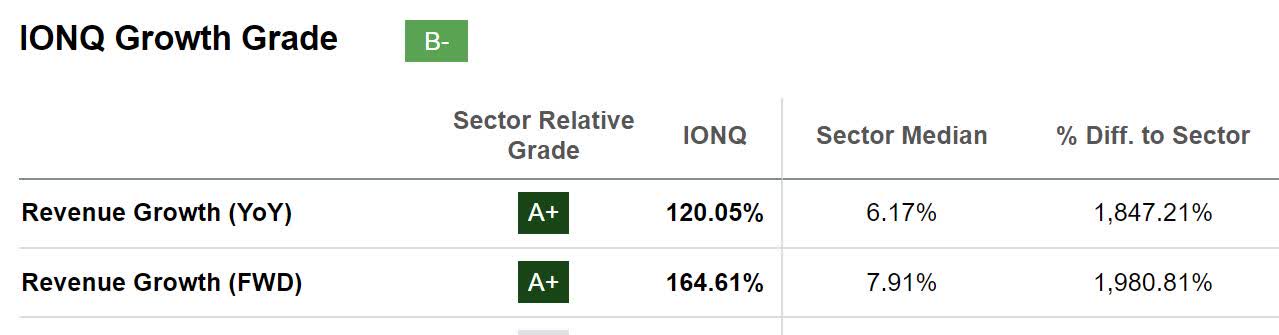

As of December 27th, 2023, IonQ had a market capitalization of $2.77B and traded for $13.21 per share. They currently have a forward EV/Sales of 110.21x, Price/Sales of 127.58x, and Price/Book of 5.87x. While I don't like using PEGY style valuation on companies which have negative net income, EBITDA, and cash flow, dividing their EV/Sales of 110.21x by their forward revenue growth of 164.61% produces a 0.6695x. Since this valuation method is using sales instead of some form of income or cash flow, I don't put much faith in it. Once they produce positive net income, EBITDA, or cash flow, I will be able to more accurately estimate their intrinsic value. However, considering their impressive gross margins and future growth potential, I view them as trading relatively close to fair value.

IONQ Growth (Seeking Alpha) IONQ Valuation (Seeking Alpha)

{kind=link}

{kind=link}

They are trading well above both their book value per share and their tangible book value per share. I view this as a statement that Mr. Market has confidence that this company is very likely to continue growing and will likely find long-term success.

IonQ Book Value Per Share (Seeking Alpha)

Using relative valuation to compare the company to peers is basically futile because this is a pure-play startup and most of the rest of their competition are massive companies with already established moats and significant cash flow. For most of these, it would not be an apples to apples comparison:

-

IBM Quantum ( IBM )

-

Rigetti Computing ( RGTI )

-

Honeywell Quantum Solutions ( HON )

-

Xanadu

-

Microsoft ( MSFT )

-

Amazon Web Services ( AMZN )

- Intel ( INTC )

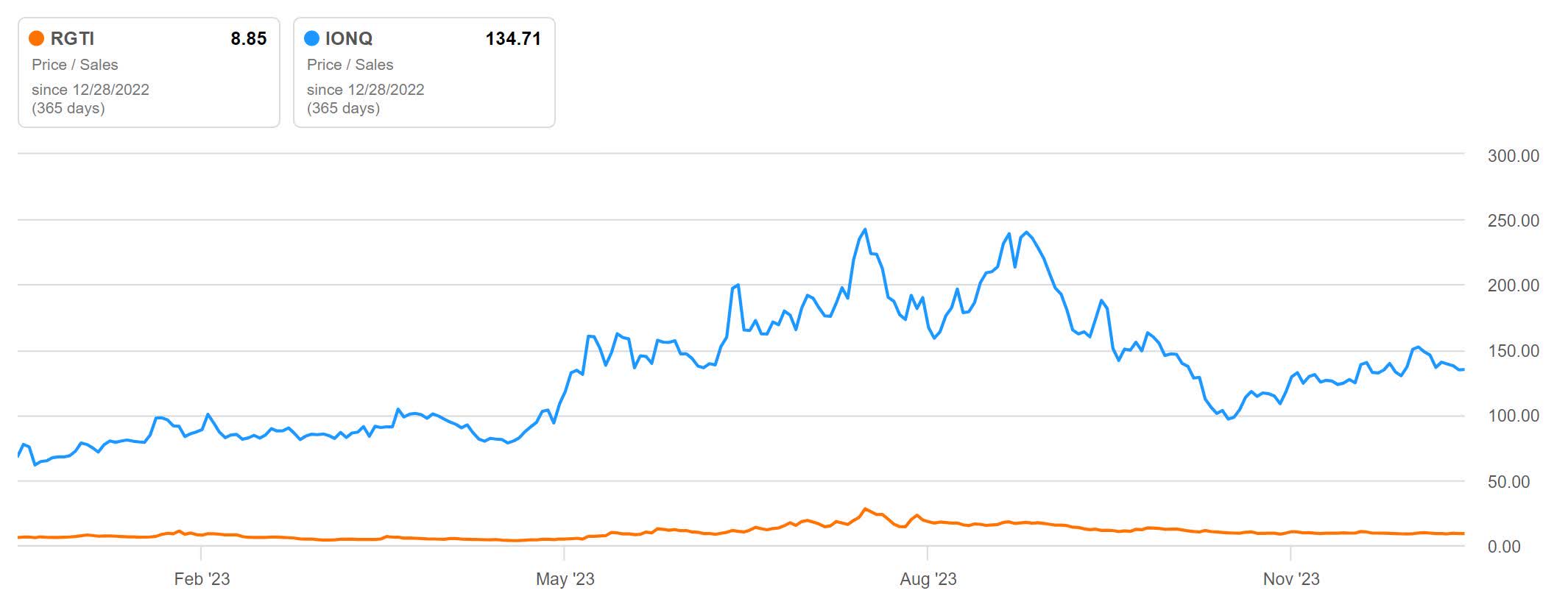

Even Rigetti Computing, the other pure-play quantum computing startup on the list above, is not a good comparison because they only have $21.7M in cash and short-term investments , and their most recent quarter had them posting a levered free cash flow of -$6.3M . They are very likely to have to raise additional capital within the next year so Mr. Market is only valuing them at a trailing P/S ratio of 8.85x.

IONQ vs. RGTI Price/Sales (Seeking Alpha)

{kind=link}

Stock Based Compensation

Instead of trying to cover this double edged sword as a part of risks or catalysts, I decided to move it to its own separate section. This company maintains a significant number of highly educated and experienced employees. As a way of both paying them what they deserve and aligning their interests with the long-term success of the company, IonQ hands out a significant amount of stock based compensation. Their ttm SBC comes to $47.4M, and this most recent quarter, it was $17M worth of shares.

While this does mean the company is steadily diluting shareholders, this also helps extend the lifespan of their available cash and short-term investments. Without it, their cash flow situation would be significantly worse. The additional time this gives them before they need to find profits or raise money through market offerings is a positive.

Risks

IonQ has a ttm levered free cash flow of -$36.5M and a reserve of total cash & short-term investments at $384M. Assuming their cash flow situation does not deteriorate, they have significant capital available to them to continue funding operations for years to come. If their revenue growth fails to meet expectations, their gross margins contract, or their expenses rise, IonQ's available capital will run out more quickly than expected.

The quantum computing industry faces the prospect of a quantum winter arriving before the technology reaches full maturity. Presently, hype and hope for their industry are both elevated. Demand for both research partnerships and time on their hardware is growing. This enthusiasm might diminish before many practical applications are achieved. If this were to happens before the company achieves positive net income, it is likely that their valuation will plummet.

Catalysts

They have very impressive gross margins and revenue growth. If both are maintained, the company has the potential to not only become net income positive, but may one day become an attractive long-term compounder. Considering the industry they are in, I believe this is possible.

With enthusiasm for quantum computing currently elevated, our forward looking markets may grant IonQ further valuation improvements off of positive guidance.

Conclusions

IonQ is an attractive pure-play in an attractive industry. Although their revenue is presently quite small, it is growing rapidly. They have plenty of cash on hand to fund operations for years to come and are likely to be able to reach positive cash flow and net income well before being forced to raise additional capital either through debt or market offerings.

I sold the small starter position I was building to move to other investments. While I was happy to take profits when they were available, I underestimated the amount of time I would have before they would be able to achieve their more recent technological milestones. However, I do plan to re-establish a position if a significant downturns presents us with an attractive buying opportunity or if they manage to achieve positive Adjusted EBITDA or EBITDA. My desire to buy back in will elevate if they are able to maintain their impressive gross margins as revenue grows.

For further details see:

IonQ Has The Potential To Become A Long-Term Compounder