WBA - Is CVS Making The Same Mistake As Teladoc?

Summary

- TDOC has infamously recorded an immense asset impairment worth $9.63B over the LTM, likely attributed to the overly expensive Livongo acquisition worth $18.5B.

- With other players embarking on aggressive M&A activities into the virtual and primary healthcare market, it remains to be seen if CVS will learn from its peer mistake.

- For now, CVS has already confirmed its Signify Health acquisition at $8B, with a rumored Oak Street Health acquisition in the pipeline at $10B.

- With $50.8B of long-term debts, it is no wonder that market sentiments are mixed, likely worsened by the CEO's growing ambition in the primary care service space.

We have previously covered CVS Health Corporation ( CVS ) here and Teladoc ( TDOC ) here in August 2022. The battleground for primary care services and the virtual healthcare market has been heating up indeed, triggering aggressive M&A activities thus far. The increasingly crowded market may also trigger more margin headwinds in the intermediate term.

For this article, we will be focusing on CVS's prospects if it so chooses to double down on its primary care ambitions aggressively. While the management can boast of an excellent execution record and robust balance sheet, it remains to be seen how the company may compete sustainably without impacting its profitability. Then again, with the stock trading near 52 week lows, there is an improved margin of safety for those who choose to nibble here. Especially since market analysts seem optimistic about its top and bottom-line growth through FY2025.

The M&A Investment Thesis Is Unconvincing In The Uncertain Macroeconomic Environment

Going down the rabbit hole of primary care may be another bane for CVS, since it had previously pursued the Aetna deal at an eye-watering value of $69B in 2018. As a result, the company grew its reliance on long-term debts tremendously by 229.3%, from $21.5B pre-acquisition to $70.8B post-acquisition by FQ4'18. Market sentiments have been less than promising then, leading to a significant decline in its stock prices by -31.6% in the months after.

CVS's debt levels have somewhat improved since then, to $50.8B by FQ3'22. However, with its recent $8B Signify ( SGFY ) deal and the rumored $10B Oak Street Health (NYSE: OSH ) deal, it is no wonder Mr. Market is uncertain, triggering a notable retracement in its stock valuations over the past few weeks. While the former reported an excellent $19.98B of cash/investments in the latest quarter, the management may have to dig deep into the funding market for some help, due to the uncertain macroeconomic outlook.

Then again, CVS's execution has been excellent thus far, with reduced annual interest expenses of $2.34B (-8.9% sequentially) and normalized gross margins of 16.3% and EBIT margins of 4.4% in the latest quarter. The company also competently expanded its Free Cash Flow generation by 28.3% sequentially to $19.48B over the last twelve months [LTM]. Shareholder returns have consequently improved by 9.2% to $2.84B of dividends paid out over the LTM, with $2.34B of stocks repurchased at the same time. Notably, there is another $10B in share repurchase authorization yet to be exercised.

In addition, CVS investors would be relieved to know that only $1.71B of its long-term debts will mature by 2023, with another $2.69B due by 2024. The rest are remarkably well-laddered through 2050 as well, suggesting adequate liquidity through the management's primary care ambitions . Therefore, it is no wonder that the Seeking Alpha Quant Rating continues to rate the company's dividend safety as A-.

In fact, OSH's strategic vertical integration with Aetna's retail/ corporate insurance/ Medicare, and CVS pharmacy segments is an interesting move, since it may consequently offer value-based care in line with the current trend. The primary care service may also complement the latter's existing Health Virtual Primary Care with American Well Corporation (NYSE: AMWL ), on top of the in-person MinuteClinic and HealthHUB locations.

Notably, CVS recently announced its investment in Carbon Health , a cloud-based urgent and primary care technology platform, with the aim of launching its digital care model in its physical locations. It appears that the management is making serious efforts to consolidate its healthcare offerings, while similarly taking on the primary care market . Karen Lynch, CEO of CVS, said:

Next, we'll advance our care delivery and health service offerings to include primary care, home health, and provider enablement. This also includes optimizing our retail business, which means reducing our footprint and transforming select store formats to serve as community health centers... We're also orienting our business using digital and technology strategy centered around the consumer. And we're optimizing processes in our company that drive value and creating an agile platform to sustain efficiency and lower costs. ( Seeking Alpha )

However, we must also highlight the intensely competitive healthcare market in the US, with Walgreens Boots Alliance (NASDAQ: WBA ) similarly embarking on aggressive M&A activities thus far. The company has pledged a $1B investment in VillageMD , aiming to introduce up to 600 primary care clinics over the next four years. This is on top of its $2.34B Shields Health Solutions deal - specialty pharmacy and $722M CareCentrix deal - post-acute and home care services provider. It also recently acquired Summit Health - a health care provider for $8.9B, highlighting the massive consolidation trend witnessed in the industry.

On the other hand, Amazon ( AMZN ) has given up on its enterprise dreams , Amazon Care, likely attributed to weak demand thus far. Interestingly, it has taken the shape of Amazon Clinic instead, focusing on retail virtual healthcare conditions such as hair loss, heartburn, acne, and seasonal allergies. Either way, the company is still proceeding with the One Medical ( ONEM ) acquisition, which has been cleared by Oregon regulators on 03 January 2023, though still pending FTC's approval.

It is uncertain if CVS will truly proceed with the OSH deal, due to the substantial 82.4% premium against its previous market cap of $5.48B prior to the tremendous 37% rally following the release of the takeover rumor. Notably, the latter has yet to achieve meaningful profitability yet, with gross margins of 4% and EBIT margins of -23% in LTM, while similarly reporting a deceleration in revenue growth at 39% compared to FY2021 levels of 62.7%. The situation is reminiscent of Livongo , which reported GAAP net losses of -$51.79M and net income margins of -16.5% in the twelve months before the deal's completion in August 2020.

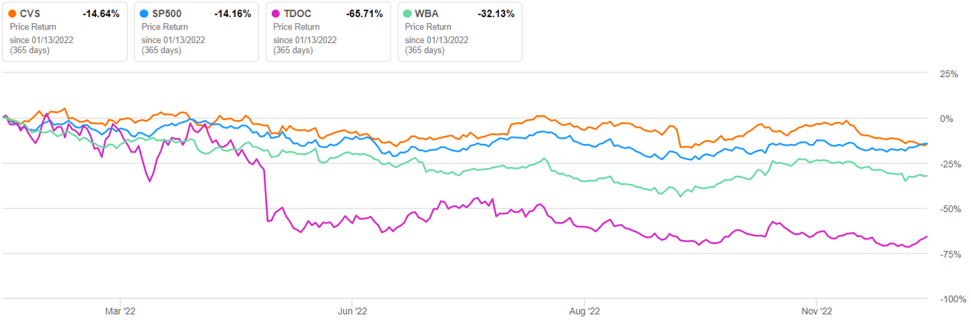

TDOC has particularly recorded immense asset impairments worth -$9.63B over the LTM, likely attributed to the overly expensive Livongo acquisition worth $18.5B . Discounting that, the company reported underperforming EBIT margins of -10% over the LTM, attributed to its elevated Stock-Based Compensation expenses of $228.7M at the same time. Its FY2022 guidance looks bleak as well, with GAAP EBITDA of up to $10M, suggesting an EBITDA margin of 0.4% and adj. EBITDA of up to $250M/10.3%. These numbers do not instill confidence indeed, despite the 57.8M paid members and 24.3M non-members in the US by the latest quarter.

There is a reason why the TDOC stock had plunged by -65.71% in the past year, with a similarly elevated short interest of 17.75% at the time of writing.

So, Is CVS Stock A Buy , Sell, or Hold?

CVS 1Y EV/Revenue and P/E Valuations

{kind=link}

CVS is currently trading at an EV/NTM Revenue of 0.53x and NTM P/E of 10.29x, lower than its 1Y mean of 0.61x and 11.68x, respectively.

CVS 1Y Stock Price

{kind=link}

Based on CVS' projected FY2025 EPS of $10.72 and current P/E valuations, we are looking at a moderate price target of $110.30. These numbers mirror the consensus estimates' target of $120.44 as well, suggesting a notable 34.18% upside potential from current levels. Then again, this is unsurprising, since the stock is trading near its 52 week lows after plunging by -19.1% since its peak in February 2022 or a -12.1% since our previous article.

Based on the CVS management's competent management thus far, we cautiously concur with the consensus estimate's decent projections through FY2025. The company is expected to record an EPS CAGR of 6.3%, suggesting a normalization to pre-pandemic levels of 6.6%. While margins may be temporarily impacted in 2023, things may improve from FY2024 onwards, nearing pre-pandemic levels as well.

Therefore, we are rerating the CVS stock as a Buy now, with the caveat that it should lower long-term investors' dollar cost average accordingly. This strategy may provide an improved margin of safety for portfolio growth, made sweeter by its forward dividends yield of 2.74%, against the 4Y average of 2.76% and sector median of 1.29%.

Inversely, new investors keen to add must be aware of the company's costly acquisitions in the short term. These may further impact market sentiments due to the uncertain macroeconomic outlook and tightened funding environment, pointing to the stock's volatility over the next few quarters.

For further details see:

Is CVS Making The Same Mistake As Teladoc?