GOOD - Is It Worth Chasing 9% Yielding One Liberty Properties?

2023-09-07 03:49:55 ET

Summary

- One Liberty Properties has fallen in price, making it the cheapest triple net REIT on AFFO multiple with a dividend yield of over 9%.

- The triple net REIT sector has been undervalued due to a flow of funds from income-focused investors towards bonds and Treasuries.

- OLP has a cheap valuation based on NAV and cash flows, a well-diversified property portfolio, and a healthy balance sheet with amortizing debt.

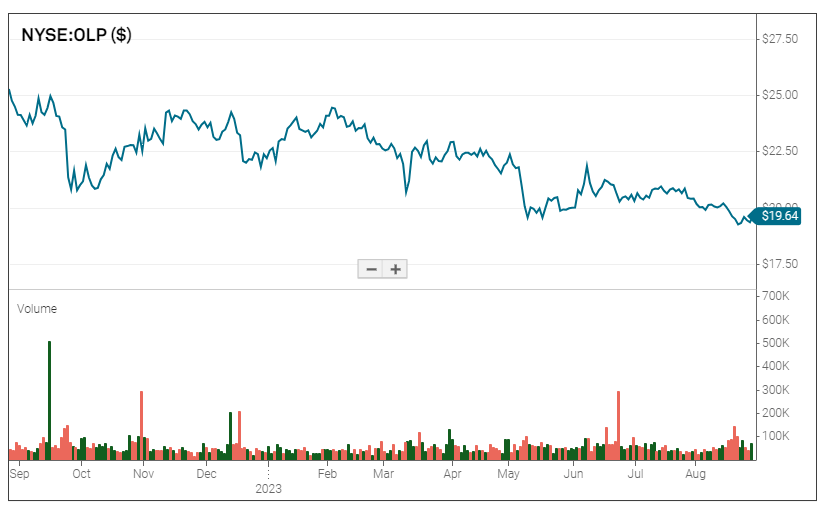

One Liberty Properties ( OLP ) has fallen from $25 to $19.64 making it the cheapest triple net REIT on AFFO multiple and also giving it a greater than 9% dividend yield.

{kind=link}

We have followed this company for many years but have not been invested in it for quite some time. However, given the improved valuation, I think it is worth another look and we have a taken a small position in the name to keep it on our radar.

Let me open with some commentary on the triple net space and follow with the OLP specific analysis.

Triple net constituency driven cheapness with fundamental strength

There are 2 main mechanisms by which valuations move:

- Estimation of forward fundamentals

- Flow of funds

So which is it that moved triple nets?

Mathematically, higher interest rates hurt all stocks due to the higher discount rate at which their future earnings should be discounted back to present value. The amount a given stock fundamentally should have dropped is related to the weighted average duration of its cash flows. The further in the future the average cash flow, the more the stock should have dropped.

This is likely why the start-up and VC space has crashed so hard. Their average cash flows are decades into the future so they really should have gotten hit the hardest by the same math that says a 30 year treasury should have dropped more than a 2 year treasury.

Triple net REITs actually have fairly short weighted average cash flow duration because their cash flows start in year 0. They are collecting rent now and paying dividends now. They will still be collecting rent and paying dividends in 20 years so they do have out year cash flows, but the year 0 cash flows make the Macaulay duration of triple nets shorter than that of the S&P and significantly shorter than that of the Nasdaq.

As such, the earnings multiples of triple net REITs fundamentally should have been punished less than the rest of the market, but an examination of the valuation of the sector reveals they have been punished more.

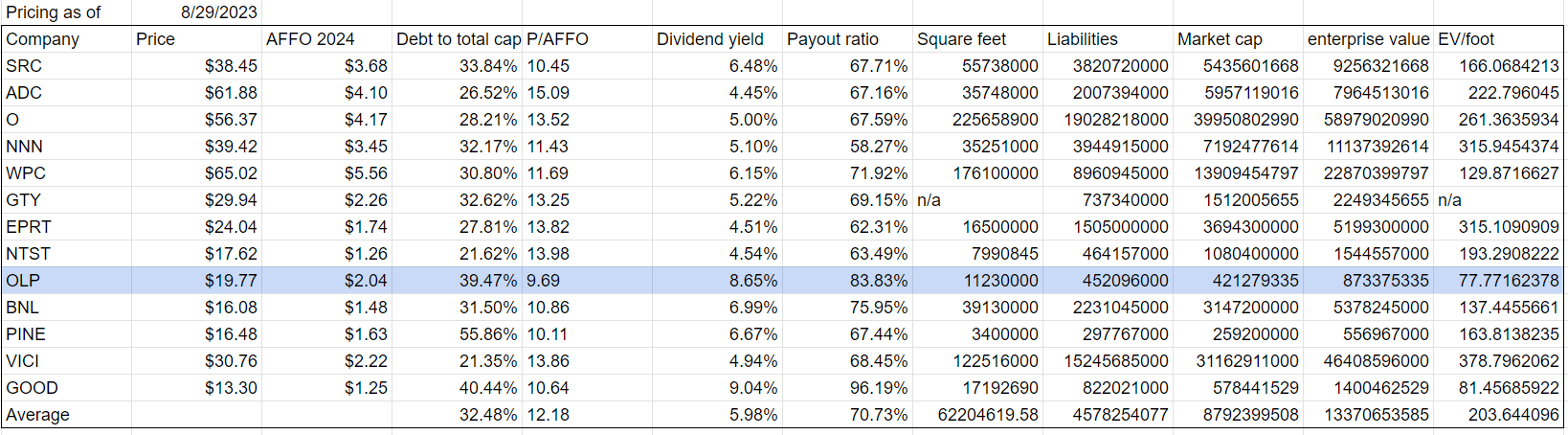

The triple net REIT sector now trades at a forward AFFO multiple of 12.18X. Even the broadly respected stocks in the space are trading around 13X-15X.

So what happened to make the sector so cheap?

Fund flows

Fund flows can drive quite a bit of price action, particularly in the short and medium term.

When someone sells a stock the impact on its market price is the same regardless of why they sold it. Someone selling because they want to buy something else has the same impact as that person selling because they dug deeper and discovered the company was damaged.

Triple nets have a distinct constituency in that they strongly appeal to income focused investors. The sector provides large and generally stable or growing dividends.

3 years ago, triple nets were just about the only game in town. Treasuries had almost negative real yields and bonds were trading at tiny yields over inflation relative to their risk.

Well, interest rates increased by nearly 500 basis points on the short end and around 300 on the long end.

Yield went from scarce to broadly available.

Triple nets still appeal to those who want a higher dividend yield and are okay with equity risk, but there is a large contingent of people who would much rather stick to Treasuries or investment grade bonds who got forced out onto the equity portion of the yield curve just to achieve a moderate yield.

Now that bonds and Treasuries are once again a decent source of yield, I suspect most of those funds have flowed back toward the fixed income instruments.

The massive selloff in triple net was not the market rendering a verdict that triple net REITs are somehow bad or dangerous. It was a simple flow of funds related to the constituency bias of the sector.

The outflows have left the sector outrageously cheap on a fundamental basis and I think it is fertile ground for investment.

{kind=link}

One Liberty Properties has fallen in price more than most of the sector leaving it as the lowest price to AFFO multiple in the group (9.69X).

OLP analysis

There are multiple aspects of OLP that we really like and a couple negatives.

The Pros:

- Valuation

- Property type/location

- Debt is well laddered

Neutral

- Stable slow growth

The Cons:

- A few troubled tenants/properties

- High stock compensation

Valuation

We like to examine valuation from multiple angles. OLP looks cheap on both NAV and cash flows.

It is currently trading at 73% of NAV but I think the consensus NAV might actually undervalue the properties. With 11.23 million square feet, OLP’s $873 million enterprise value makes it an EV/foot of just under $78.

That is by far the cheapest price per foot of any triple net REIT.

Part of that is due to the property mix with OLP being mainly industrial for its square footage. Industrial is cheaper to build than retail.

OLP

But it hard to even find a purely industrial REIT trading at that kind of a price per foot.

With more square footage per invested dollar comes more cash flow per invested dollar. Nominally, OLP is trading at 9.69X consensus AFFO. I think the multiple is slightly higher than that once we distill AFFO down to true earnings.

OLP has stock compensation cycling at around $6 million a year.

{kind=link}

As an absolute number that is not all that high compared to other companies, but because OLP is so small it hits harder.

Divided over the 21.3 million shares outstanding that is about $0.28 a share annually.

Consensus AFFO figures such as the $2.04 estimated for 2024 are meant to match the way companies calculate earnings so as to be comparable to the actual earnings that get reported.

Stock comp is of course a real expense, however, so I calculate true expected earnings at $2.04 - $0.28 or about $1.76.

Therefore, OLP is trading at 11.2X forward true earnings. Still quite cheap but not as outrageously cheap as consensus metrics suggest.

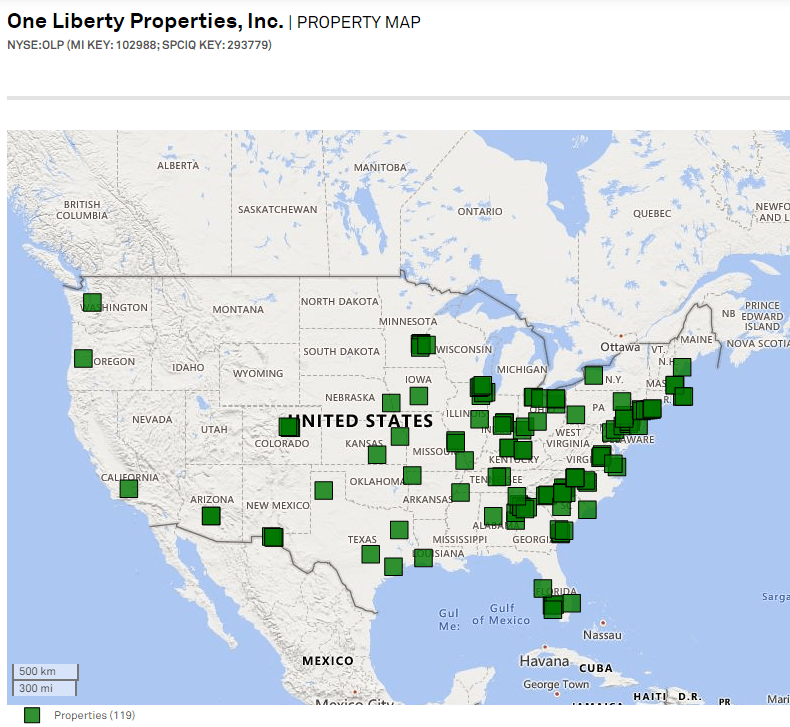

Property Portfolio

For a small company, OLP has achieved quite a bit of geographic diversification.

{kind=link}

One of the advantages of triple net is that it is relatively lower touch required once the contracts get set into motion. This allows one to spread out a bit more without it being too much of a burden on operating expense.

OLP’s annual report describes a 57/26/17 ratio of industrial/retail/other. Most of the “other” category is actually just subcategories of retail. Since that report OLP has been buying predominantly industrial so I think it would be reasonably accurate to think of their portfolio as 60/40 industrial/retail.

It is a good mix. I like the balance and along with diversification comes individual properties that outperform and underperform.

OLP’s largest tenant at 5.7% of revenue is Haverty Furniture Companies ( HVT ) which is publicly traded and quite profitable.

{kind=link}

The success of this tenant has allowed OLP to sell a few of the related properties at significant gains on sale. Its 2 nd largest tenant is FedEx, which is quite reliable.

On the other side, OLP has a few troubled properties and/or tenants.

- A Bed Bath and Beyond location that lost its rental stream due to the April bankruptcy

- An L.A. Fitness that had a competing gym built next to it. Rent has been renegotiated lower and since gym space is hard to turn into more traditional retail it may be hard to re-lease to a higher paying tenant.

- Regal Cinema rent negotiated lower.

The above mentioned tenant issues have been well described by OLP and are already in the $2.04 consensus estimate so further adjustment is not needed.

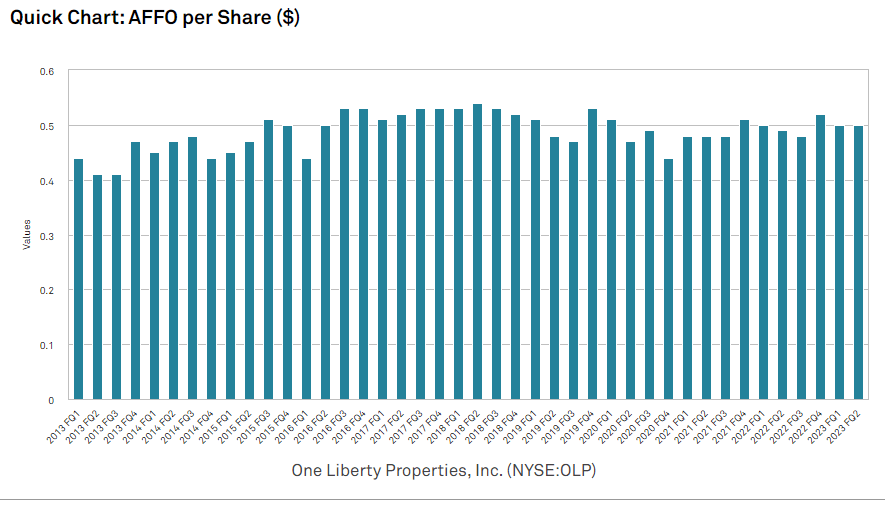

These sorts of winners and losers are more or less par for the course with a highly diversified portfolio. Some properties do great, others struggle and overall they tend to balance out. The net result for OLP has been steady but fairly slow AFFO/share growth.

{kind=link}

Given the valuation at which OLP trades, not much growth is needed to generate a solid return.

Balance sheet

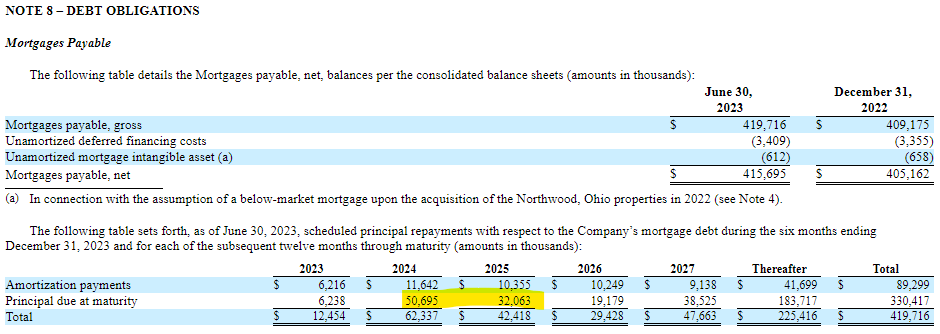

Liabilities consist primarily of property level mortgage debt. The weighted average remaining term is 6.1 years with a weighted average interest rate of 4.17%.

It is not too often that we see amortizing debt these days, but I like it. The roughly $10 million per year of amortization results in a slow reduction of leverage levels and reduces the impact of balloon payments.

{kind=link}

OLP’s largest upcoming maturity will be the $50 million in 2024. This is among their highest cost debt so replacing it should only be about 100 basis points higher in interest rate even given the environment.

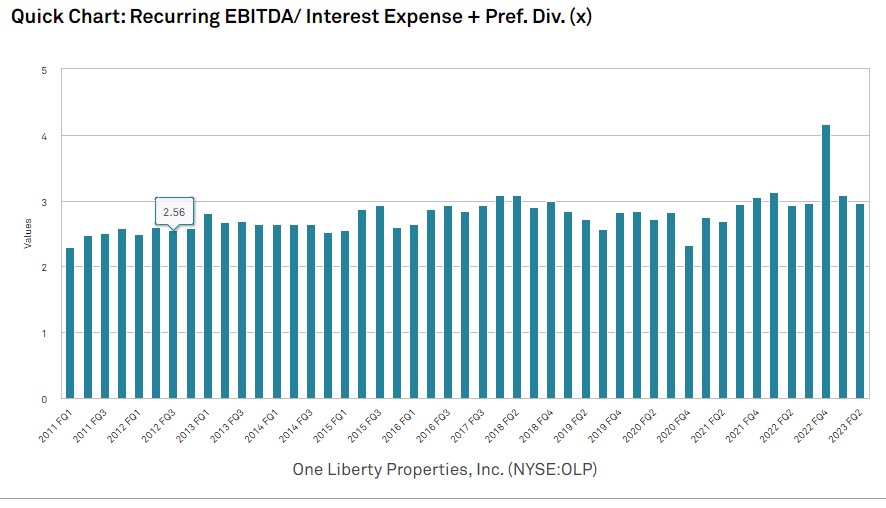

The debt paydown has resulted in EBITDA coverage levels inching up over time.

{kind=link}

Overall the balance sheet looks healthy but it is slightly above average in leverage, which should be accounted for in valuation.

We have plotted the triple net REITs below with the best fit line accounting for level of leverage. Generally speaking, those below the line are relatively undervalued.

{kind=link}

At current pricing, I find Broadstone ( BNL ), Spirit Realty ( SRC ), Gladstone Commercial ( GOOD ) and W. P. Carey ( WPC ) to be the best positioned triple net REITs.

One Liberty Properties is interesting and I think a viable way to achieve a really high dividend yield. We own a tiny bit now and will be watching it intently as the relative opportunity flexes over time.

For further details see:

Is It Worth Chasing 9% Yielding One Liberty Properties?