VRM - Is Vroom A Buy? Unpacking Its Strategic Pivot

2023-09-18 07:01:19 ET

Summary

- Vroom faces financial concerns and liquidity issues, with a market capitalization well below its book value.

- In 2023, Vroom undertook strategic changes, including workforce reduction and a shift to an in-house sales model, aiming to improve customer experience and reduce costs.

- The company's revenue streams are complex, with high-margin sectors in product and finance offset by negative margins in wholesale vehicle sales.

- Vroom's strategic pivot and integration of UACC present both opportunities and challenges, but its valuation remains high-risk.

- Overall, I rate VRM a hold, but it is worth monitoring its ongoing turnaround efforts.

Vroom, Inc. ( VRM ) faces a critical mix of opportunities and challenges. Financial concerns persist despite a 2023 strategy shift for cost reduction and customer experience. The market remains skeptical, with a market cap of $178.77 million-well below its book value of $338.24 million. VRM's promising high-margin sectors in product and finance are offset by high SG&A costs and an estimated annual cash burn rate of $180 million, raising immediate liquidity concerns and the risk of NASDAQ delisting. Given these factors, VRM presents a high-risk, high-reward profile, warranting a neutral rating.

Unpacking Vroom's Revenue Streams

Vroom's business model can be mischaracterized as a straightforward venture into retail and wholesale vehicle sales. Still, a deeper analysis reveals a complex revenue mix. At its core, Vroom relies on data analytics to optimize its Average Selling Price ((ASP)) in retail vehicle sales. Several factors, including market conditions, reconditioning costs, and logistics, influence VRM's ASPs. However, this analytical prowess doesn't necessarily translate into pricing power, as evidenced by its negative margins. So, the company is often at the mercy of market prices and cannot dictate terms, making it vulnerable to external economic forces.

{kind=link}

Beyond the surface-level retail and wholesale operations, Vroom has diversified its revenue streams to include 'Product Revenue' and 'Finance Revenue' generated through its captive financing arm, UACC , and the sale of value-added products like vehicle service contracts. According to its latest 10-Q SEC filing, these segments are highly sensitive to market conditions and legal frameworks. This was evidenced by a recent incident where unfavorable conditions forced Vroom to reclassify a securitization transaction, thereby retaining finance receivables on its balance sheet. This seemingly minor accounting shift underscores a critical point: Vroom's business is increasingly becoming financialized to a degree that its liquidity and financial flexibility are contingent on its ability to offload these receivables. And all of this is contingent on its overall creditworthiness (more on this later).

Author's elaboration.

Moreover, VRM's revenue model is broken down into five key contributors: retail vehicle sales, wholesale vehicle sales, product, finance, and other miscellaneous streams. Among these, the product and finance segments are profitable, boasting impressive gross margins of 94.1% and 80.9%, respectively. In stark contrast, wholesale vehicle sales act as a profitability sinkhole with a negative gross margin of -13.0%, while retail vehicle sales barely break even at a 1.5% gross margin. This disparity in profitability across segments highlights the need for Vroom to strategically allocate resources and perhaps reconsider the weightage of each revenue stream in its overall business strategy.

Cost Structure, Outsourcing, and In-House Operations

Vroom's cost structure extends beyond mere vehicle acquisition, including inbound transportation and reconditioning expenses, often outsourced to third parties. This reliance on external services risks inflating costs, adversely affecting Vroom's ASP and undermining its data-driven sales and pricing strategies. Additionally, the company's 'Product Cost of Sales' is vulnerable to macroeconomic factors such as rising interest rates, potentially eroding margins, and negating gains from its technology-driven approach.

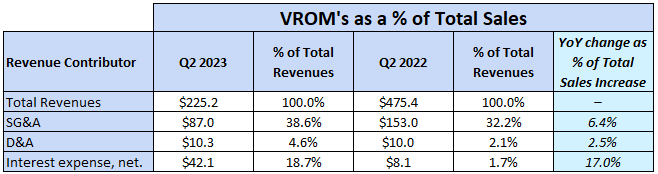

On another front, Vroom's transition to an in-house sales model is expected to escalate SG&A expenses due to increased human resource investments. However, management didn't give much detail into the specifics of this strategy when they were asked about it in their latest earnings call . And while intended as a cost-saving measure, this shift could backfire if poorly executed. Furthermore, it's worth noting that early indicators show a rise in SG&A expenses, accounting for 38.6% of total sales this quarter, compared to 32.2% in the same quarter last year.

{kind=link}

Examining VRM's revenue streams and cost structure reveals a precarious balancing act. On the one hand, the company offers a promising, data-driven retail platform with the potential to disrupt the automotive industry. On the other hand, it faces many risks, from workforce downsizing (more on this later), reliance on third-party services, and market vulnerabilities that challenge its profitability. So, given that VRM hasn't been profitable since its inception, I'd argue its business model remains largely unproven.

VRM's Strategic Pivot and UACC Integration

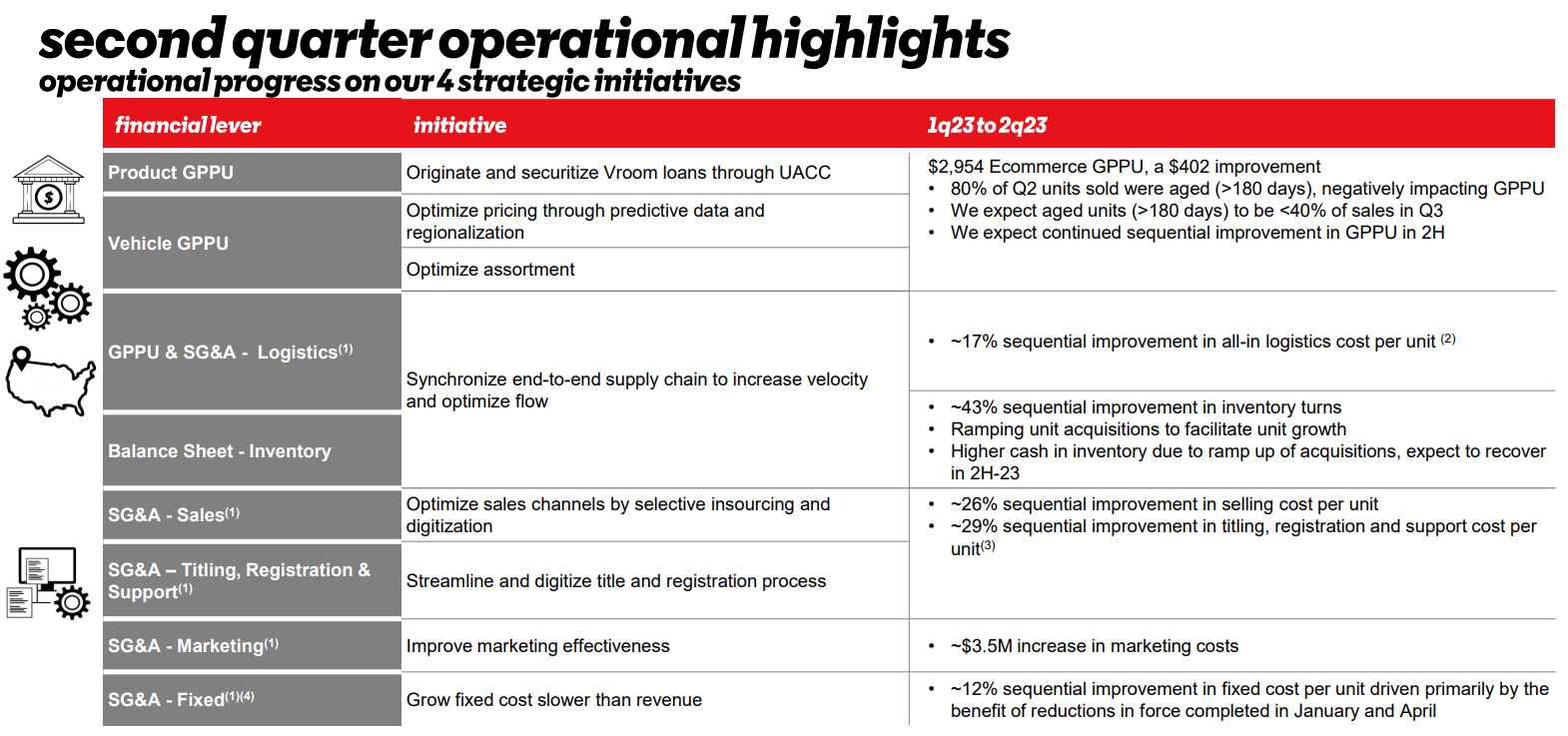

Recognizing the need for change, Vroom has undertaken aggressive financial and strategic realignments throughout 2023. However, these moves are more nuanced than they initially seem. The company slashed its workforce by approximately 55% since January 2022, targeting an annual cost savings of around $42 million. These reductions, while substantial, have incurred $6.4 million in severance costs and coincided with Vroom's investment in enhancing customer experience, including the development of an in-house sales team. This shift from third-party sales support has led to a temporary dip in sales volume, but the company anticipates fully internalizing its sales operations by Q3 2023. This represents a pivotal moment for Vroom, as its future ability to convert platform visitors into customers will increasingly hinge on its in-house capabilities.

As part of Vroom's strategic pivot, the company has repurchased $32.8 million in Convertible Senior Notes this year, effectively reducing its debt burden. However, this move also casts a spotlight on the sustainability of its long-term capital structure, especially in light of the ongoing costs associated with the UACC acquisition. While this acquisition enhances Vroom's financing capabilities, it exposes the company to the volatile subprime sector and the intricate challenges of securitizing auto finance receivables. UACC is a double-edged sword: it broadens Vroom's financing options across the credit spectrum and heightens its vulnerability to rising interest rates and potential credit losses. The UACC acquisition could be accretive to Vroom's value in the grand scheme. Still, its successful integration represents yet another complex layer in the company's already challenging pivot and cost-structure realignment.

{kind=link}

Furthermore, I interpret Vroom's strategic pivot primarily as a crisis-driven response to the NASDAQ's looming threat of delisting. Such a delisting would tighten market liquidity and activate an immediate redeemability clause for Vroom's outstanding notes, exacerbating its fragile liquidity situation. This is particularly alarming given Vroom's limited ability to set prices and its yet-to-be-proven business model. Adding to these concerns, the company's existing and future debt covenants could further restrict operational agility, intensifying a chain of negative outcomes. While Vroom regained NASDAQ compliance as of June 23, 2023, the specter of delisting continues to hang over the company.

VRM's Valuation is High-Risk, High-Reward

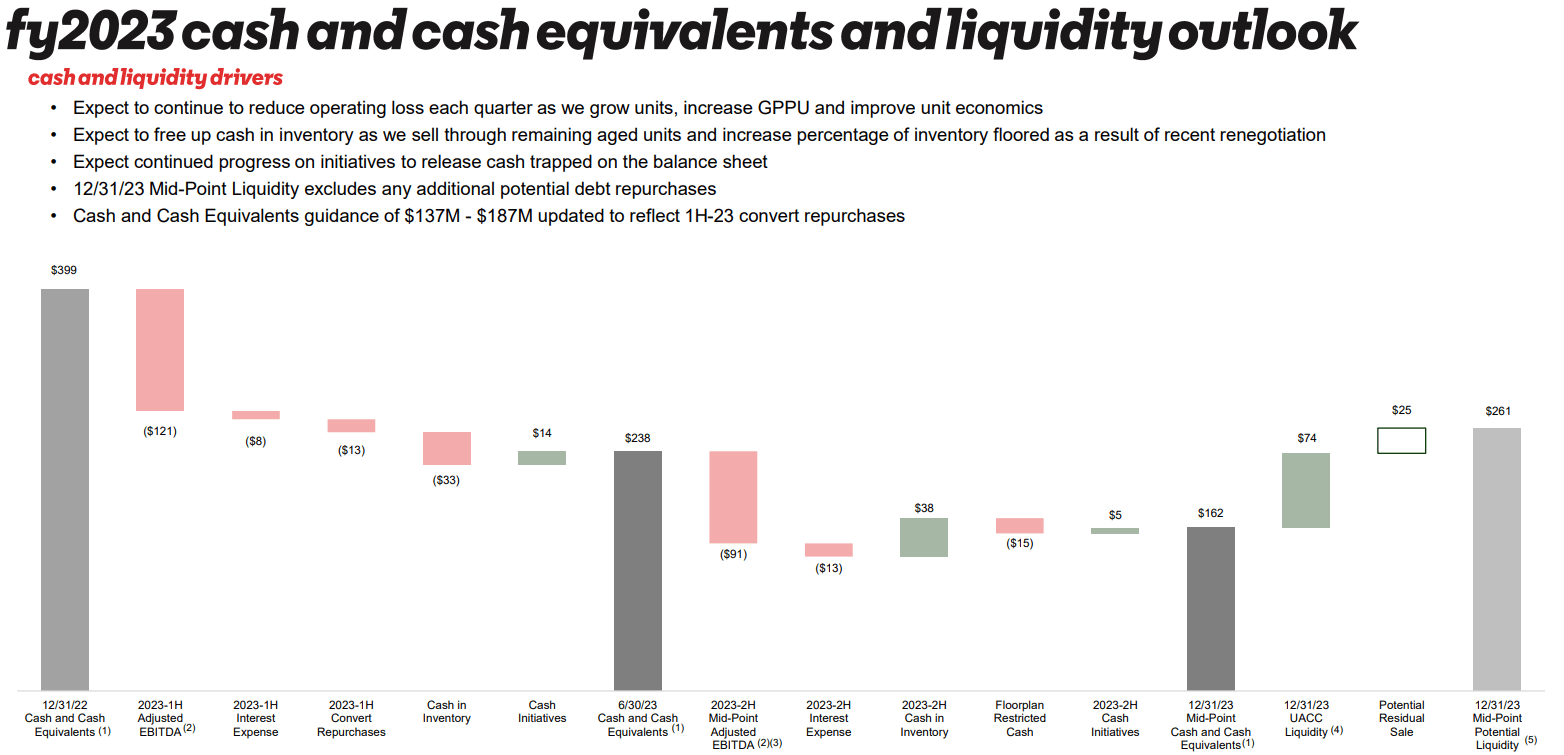

VRM's current market capitalization of $178.77 million, significantly below its book value of $338.24 million, encapsulates the market's perception of the company as structurally unprofitable and financially distressed. This is despite VRM's promising revenue streams, like product and finance, enabled by the UACC acquisition. The company's focus on data analytics for operational efficiency and its multi-pronged revenue approach could yield significant free cash flows if it successfully trims operational fat. However, the reality is stark; VRM's guidance indicates $200 to $225 million in adjusted EBITDA losses, and its cash reserves stand at a precarious $237.9 million . Moreover, VRM's SG&A expenses are nearly double its gross profits.

{kind=link}

Estimating cash burn for VRM is challenging due to the company's complex business dynamics. Nevertheless, a rough calculation can be made by subtracting net interest and SG&A expenses from gross profits. Based on this method, Vroom burned approximately $45 million last quarter. When annualized, this translates to an estimated yearly cash burn rate of around $180 million. This rate is concerning and exacerbates liquidity issues, heightening the risk of NASDAQ delisting and potentially limiting access to affordable financing.

Seeking Alpha Valuation Tab

However, Vroom's depressed valuation already accounts for its immediate challenges. If the company successfully navigates its liquidity constraints and streamlines operations, it could unlock cheaper capital sources and stabilize its stock price. Vroom's focus on enhancing gross profits in high-margin sectors and leveraging technology to cut SG&A expenses is key to this turnaround. Also, the acquisition of UACC, despite its inherent macroeconomic risks, is a strategic move to capitalize on lucrative finance revenues and could become a valuable revenue driver in the long run.

Therefore, while the market appears to price Vroom for failure, this perception creates a unique investment opportunity. A successful pivot could bolster EBIT margins, alleviate liquidity issues, solidify its NASDAQ listing, and provide sustainable access to affordable capital. For investors aligned with management's optimistic vision, this scenario could trigger a revaluation of the stock, shifting it from a distressed asset to a high-reward investment.

Final Thoughts

Vroom stands at a critical juncture, balancing high-reward potential in its focus on high-margin sectors like product and finance with significant risks, including liquidity concerns and the threat of NASDAQ delisting. The company's Q3 2023 performance will be a key indicator of its strategic success, particularly its shift to an in-house sales model and operational efficiencies. Due to these mixed indicators, I assign Vroom a 'Neutral' rating, reflecting its challenges, opportunities, and current depressed valuation. Importantly, Vroom's future largely hinges on its ability to consistently generate revenue from its high-margin sectors while effectively managing its cost structure. Therefore, any news or quarterly results indicating progress in these areas could prompt a re-evaluation of Vroom as a longer-term investment. For now, Vroom remains a company to watch closely but not necessarily one to invest in immediately.

For further details see:

Is Vroom A Buy? Unpacking Its Strategic Pivot