NLCP - It's Time To Play REIT M&A

Summary

- I don't consider M&A a catalyst for stock picking, unless, of course, there's an Activist behind the noise.

- So in this article, let's just say that I'm a suggest-ivist.

- I like the M&A game and its fun trying to speculate on the companies that could be gobbled up, like these three.

You'd think last year came up short in terms of business mergers and acquisitions (M&A).

In which case, you'd be wrong.

On December 29, The Street published " The 6 Biggest Mergers and Acquisitions of 2022 ," which noted how "active" the M&A scene was. "More than 2,000 deals" were "made, with a total value of about $2 trillion."

Higher interest rates? No problem, apparently.

Higher inflation? Whatever.

Confusing consumer spending? Bring it on!

Now, all sarcasm aside, the article did add this:

"While the M&A market is down from historic highs in 2021, its numbers are fairly even with pre-pandemic levels.

"'Uncertainty always weighs on decision making. And M&A is a big decision for deal makers,' said Andy West, global coleader of McKinsey & Company's M&A Practice, in an article on its website. 'So naturally we're seeing a bit of a slowdown.'"

Just not nearly as much as we would expect.

Real estate investment trusts ("REITs") got their piece of the pie throughout all of this, despite enduring - or perhaps because of - their own dreadful year. Industry experts and advocate Nareit released its own assessment of 2022's business wheeling and dealing just last week, writing:

"Total REIT [M&A] activity came to $83.0 billion in 2022, the second-highest annual figure since 2007, with transactions taking place across a range of property sectors. In 2021, total REIT M&A activity stood at $99.4 billion. The highest level prior to that was $97.9 billion in 2007."

And there's no doubt more to come.

The Negatives REITs Face in Making M&A Decisions

Before we go down that train of thought further, it's only fair (and accurate) to note these paragraphs from the Nareit article:

Christopher Johnston, partner and Americas REIT Leader at EY, noted that 2022 saw some large transactions. "But those deals take some time to work through, so you're right on the heels of a good recovery in the economy in 2021, leading into 2022 with some good tailwinds. They were able to pull the trigger and get those deals closed in the front half of 2022, and even into the third quarter.

Adam Emmerich, partner at Wachtell Lipton, noted that deals slowed down in the second half of 2022, with the momentum to consolidate or go private 'countered by large gaps between seller and buyer valuations and a challenging macro environment, particularly rising interest rates and difficult debt markets, volatility in REIT stock prices, and general economic and geopolitical uncertainty.'"

And, of course, we don't see much improvement in those regards for at least the first half of the year. Despite the markets trying to play chicken with the Federal Reserve (yet again), rates are likely going higher.

Don't believe me? That's okay. But maybe you should believe the institution itself.

Federal Reserve officials are trying to douse any lingering hope that the brightening inflation outlook will give them leeway to cut interest rates later this year.

In a series of recent speeches, central bankers have fallen in line behind Fed chair Jerome Powell with a consistent message: the federal funds rate - which influences the cost of mortgages, credit card debt, and business loans - will climb above [5%] and stay there for some time."

In short, this next year could be an interesting one to watch unfold.

But Even So, the Strong REITs Survive

Again, I have no doubt the current economic climate will continue to present challenges. I also will point to Nareit's " 2023 REIT Outlook ," published last month, which noted how:

Higher interest rates and debt costs are throttling commercial real estate transaction volume. The combination of high rates and weak valuations resulted in a dearth of REIT capital raising in the third quarter of 2022; it is at its lowest level since 2009."

However, here's its overall assessment:

With strong operational performance and balance sheets, REITs are well-positioned to navigate economic and market uncertainty in 2023."

As for Nareit's expectation that "institutional investors will increasingly use REITs in [their] portfolio completion strategies"… I understand why it's saying that. It makes sense considering how investors of all kinds seek safety when the markets are down.

So I also understand why anyone might expect REIT prices to climb - maybe even skyrocket - this year as a result. However, last year's price action was so unexpected in so many ways, I'm not going to predict any such thing.

As I wrote in my "REIT Roadmap 2023," published exclusively on iREIT on Alpha , here's what I am focusing on:

Although the economic outlook is more uncertain and internal growth remains challenged… we remain fixated on the overall highest-quality REITs that offer resilient pricing power, strong balance sheets, and dividend growth."

That healthy positioning should lead to business decisions that positively affect our investments for some time to come. The best management teams know how to take advantage of trying times.

That's why I wouldn't be surprised to see the following REITs get snapped up in 2023, even in the midst of all this turmoil.

3 REITs ripe for takeover

As I've said quite a few times on Seeking Alpha, I don't consider M&A a catalyst for stock picking, unless of course there's an Activist behind the noise.

So in this article, let's just say that I'm a suggest-ivist who believes there's a good chance that these three REITs will end up being taken out by a bigger and stronger entity.

I like the M&A game and it's fun trying to speculate on the companies that could be gobbled up, like these three...

Spirit Realty Capital, Inc. ( SRC )

Spirit Realty is a REIT that primarily owns single-tenant free-standing properties that are leased on a long term, triple-net basis. Spirit Realty was founded in 2003 and went public in 2012 and currently has a market cap of $5.77 billion.

As of the 3rd quarter of 2022, SRC owned 2,118 properties in 49 states with 346 tenants. Their properties are well diversified by asset type with a portfolio consisting of 70.4% retail properties, 20.7% industrial properties, 2.6% office properties, and 6.3 classified as other.

They had an occupancy rate of 99.8% with a weighted average lease term of 10.4 years. Their top 10 tenants make up 22% of their annual base rent ((ABR)) while their top 20 tenants make up 35% of their ABR.

Spirit has good credit metrics and has a BBB credit rating with a stable outlook from S&P. They have a Total Debt to Total Assets ratio of 38%, an Adjusted Debt to Annualized Adj EBITDA of 5.2x, a Fixed Charge Coverage ratio of 5.4x and have $1.3 billion in liquidity available to them. 99.9% of their debt is unsecured and 100% is fixed rate. Additionally, no maturities come due until 2025.

{kind=link}

With its strong balance sheet and the quality of its assets, Spirit Realty could be an acquisition target with a market cap of $5.77 billion. In my opinion, the most logical buyer would be Realty Income Corporation ( O ).

Realty Income is a triple-net lease REIT with a very similar business model to that of Spirit. They serve many of the same industries, have a similar mix of property types, and share many of the same tenants listed as their top 20 clients.

Both Realty Income and Spirit Realty primarily focus on retail properties, but both have a decent amount of industrial exposure as well. As of 3Q22 Spirit received 70.4% of its annual base rent from retail properties and 20.7% from industrial real estate. Realty Income received 84.6% of its ABR from retail and 13.9% from industrial properties.

{kind=link}

When comparing their list of top tenants, many of the same companies appear as top tenants for both REITs. Realty Income and Spirit Realty both list: Home Depot, Dollar General, and Walgreens to name a few. In all, the two REITs share 8 out of their top 20 tenants.

SRC/O Investor Presentation (data compiled by iREIT)

Realty Income is no stranger to M&A activity, with its recent merger with VEREIT in 2021 for approximately $11 billion, and more recently the acquisition of a portfolio of retail and industrial properties from CIM Real Estate for close to $900 million.

Spirit's property mix and tenant base would pair nicely with Realty Income and give them increased exposure to industrial properties. Currently, Spirit is trading at a slight discount to its normal P/FFO (funds from operations) multiple, and well below the sector's average normal P/FFO.

No one can predict the future, but Spirit does have high quality assets trading below the sector's average that fit very well with Realty Income's current portfolio. We rate Spirit Realty a Spec Buy.

{kind=link}

{kind=link}

NewLake Capital Partners, Inc. ( OTCQX:NLCP )

NewLake Capital is a triple-net lease REIT that acquires industrial and retail properties through sale-leaseback transactions to state licensed cannabis operators. NLCP was founded in 2019 and went public in August 2021 and is a small cap stock with a total market capitalization of just $360 million.

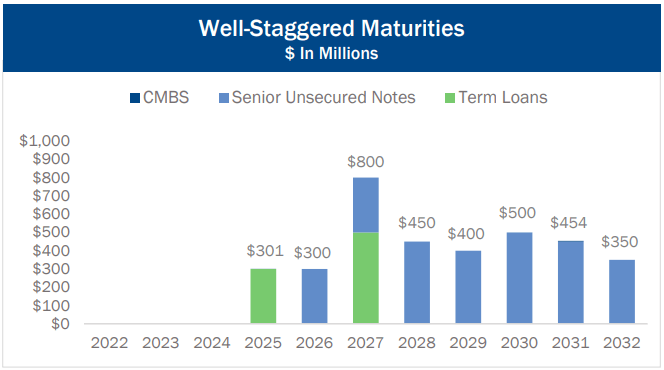

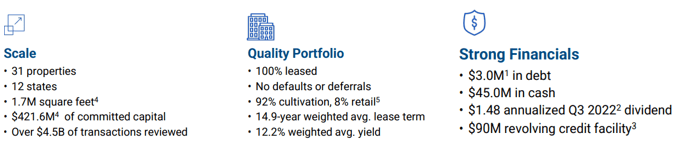

As of their November 2022 presentation, NewLake held 31 properties across 12 states for a total of 1.7 million square feet. They are 100% leased with a weighted average lease term of 14.9 years and have no defaults, rent abatements, or deferrals.

As a percentage of committed capital, their property mix consists of 92% industrial cultivation real estate and 8% retail properties.

{kind=link}

NewLake Capital has a strong cash position with $3.0 million in debt vs. $45.0 million in cash and a $90 million revolving credit facility that is almost at full capacity with only $1.0 million drawn as of September 30, 2022.

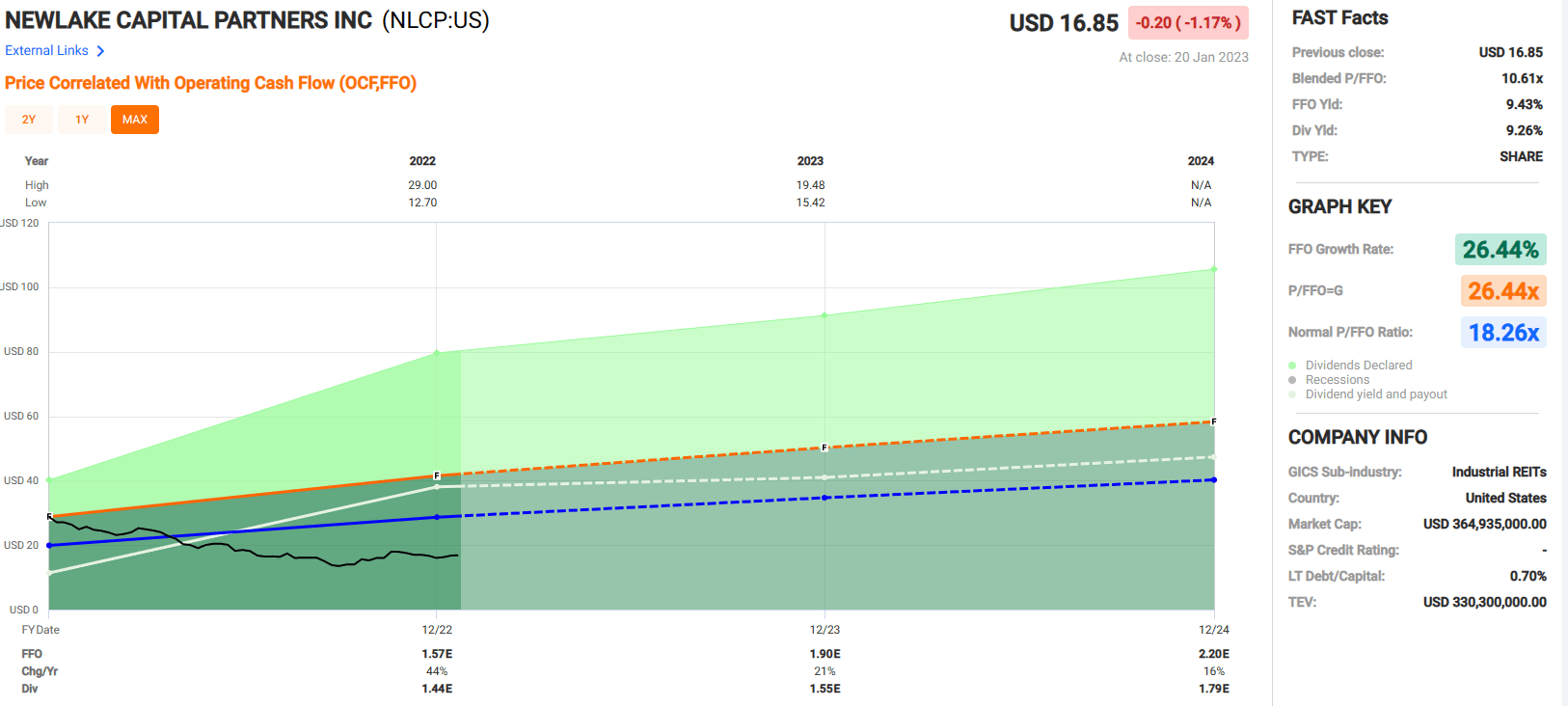

In addition to the strong cash position, 100% occupancy rates, and their weighted average lease term of almost 15 years, NewLake has shown outstanding growth in Funds from Operations since its public listing. In 2022, NLCP grew FFO by 44% and is expected to increase FFO by 21% in 2023 and 16% in 2024.

{kind=link}

NewLake Capital could be a potential acquisition target given their low levels of debt and a market cap of only $360 million, especially when considering the growth potential NLCP has shown.

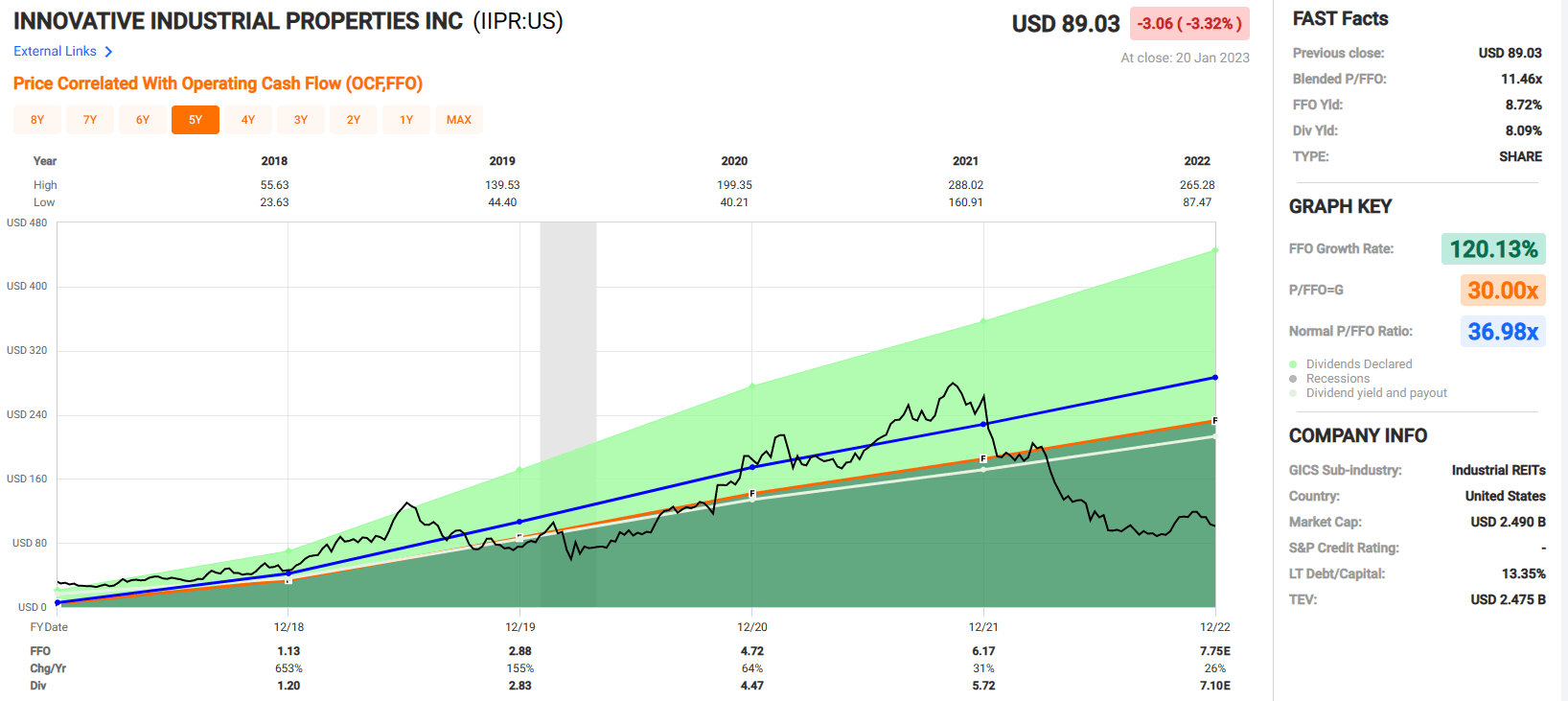

In my opinion, the perfect suitor would be Innovative Industrial Properties ( IIPR ). With a market cap of $2.49 billion, IIPR is the largest player in the equity REIT cannabis space and has shown their own impressive growth rates since their public listing in 2016.

NLCP is traded OTC (over the counter) and IIPR has a highly coveted NYSE listing.

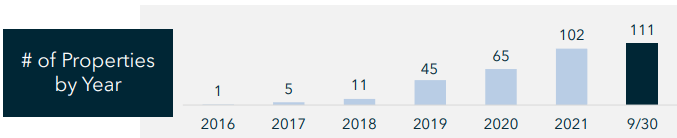

As of the 3rd quarter in 2022, IIPR had 111 properties, vs just 1 back in 2016 and over the last 5 years IIPR has had an average FFO growth rate of 120.13%. By acquiring NewLake it would add 31 properties to their existing 111 for a total property count of 142 or an increase of 27.92%.

{kind=link}

{kind=link}

NewLake Capital and Innovative Industrial share many of the same top tenants, including Curaleaf, Cresco Labs, Trulieve, Columbia Care, and PharmaCann. This could further incentivize an acquisition as IIPR is familiar with several of NLCP largest operators.

Data compiled by iREIT

Again, no can predict the future, but at NLCP's current valuation it could possibly be an acquisition target, especially if a major player like IIPR is looking to further consolidate the space. We rate NewLake a Spec Buy.

{kind=link}

Broadstone Net Lease, Inc. ( BNL )

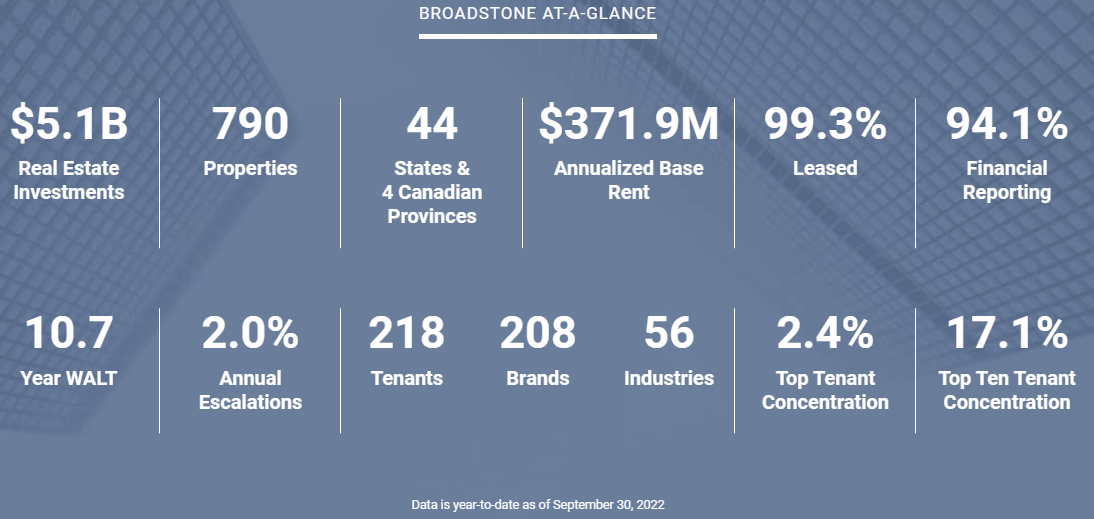

Broadstone is a net-lease REIT that owns and manages single-tenant commercial real estate across several main property types that include industrial, healthcare, restaurants, retail, and office. BNL was founded in 2007, went public in 2021 and currently has a market capitalization of $3.07 billion.

As of September 30, 2022, BNL had 790 properties located in 44 states and Canadian for a total of 36.8 million rentable square footage.

They serve 218 tenants across 56 industries and have a weighted average lease term of 10.7 years and an occupancy rate of 99.3%. Their top tenant only makes up 2.4% of their annual base rent, while their top 10 tenants collectively make up 17.1% of their ABR.

{kind=link}

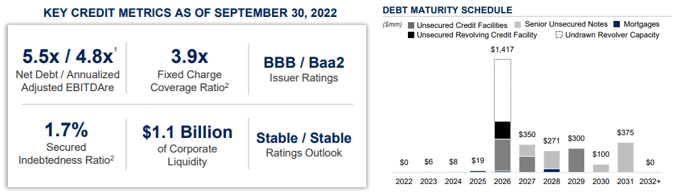

Broadstone has good credit metrics and a BBB credit rating with a stable outlook. They have a Net Debt to Annualized Adj EBITDAre of 5.5x (4.8x on a pro forma basis) and a Fixed Charge Coverage ratio of 3.9x. BNL has $1.1 billion of liquidity with no major debt maturities coming due until 2026.

{kind=link}

Broadstone, along with most other stocks, had a rough 2022 in terms of its stock price. BNL lost 21.57% over the last year, pushing its dividend yield up to 6.21% and its FFO multiple down to 12.38x.

BNL's dividend is well covered by its AFFO (Adjusted FFO) with an expected payout ratio of 77.14% in 2022 and its current FFO multiple is well below its normal P/FFO of 15.76x. At its current valuation, Broadstone could be an acquisition target, and to me the most logical buyer would be W. P. Carey ( WPC ).

{kind=link}

W. P. Carey is a much larger net-lease REIT with a market cap of $17.47 billion and is active in M&A activities to fuel external growth. In August 2022 they announced the completion of their merger with Corporate Property Associates 18 for $2.7 billion.

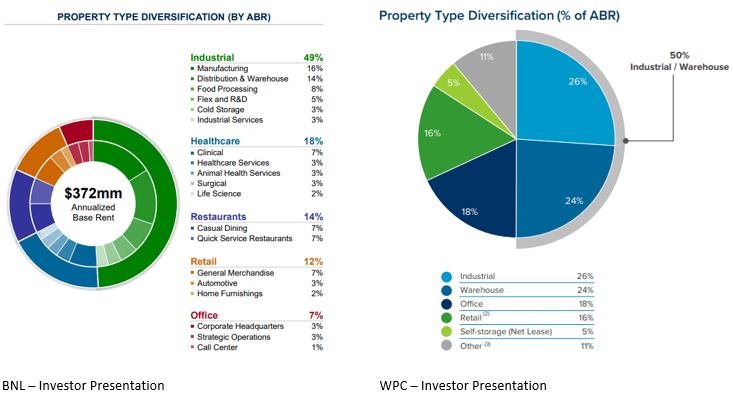

W. P. Carey and Broadstone have a similar mix of property types. Both REITs receive about 50% of their annual base rent from industrial / warehouse properties. Broadstone receives approximately 26% of ABR from Retail / Restaurants while W. P. Carey list 16% of ABR coming from retail properties. They both have a reasonable number of office properties as well.

{kind=link}

The market cap destruction we've seen over the past year has created opportunities for individuals to buy into companies at discounted valuations we haven't seen in some time. These opportunities also exist for real estate companies with strong balance sheets looking to expand their property holdings.

At its current valuation, Broadstone trades for a P/FFO multiple of 12.38x vs. their normal multiple of 15.76x and trades below their Net Asset Value ("NAV") with a P/NAV of 0.87. BNL's property mix along with its current valuation could make Broadstone an attractive candidate for acquisition in the year ahead. We rate Broadstone Net Lease a Spec Buy.

{kind=link}

Closing Thoughts...

As I explained, iREIT has Buy ratings on all three REITs, and while M&A is a possibility (for all of them), we own them because we believe that the fundamentals support future dividend growth prospects.

They all remain cheap, and this means that they offer attractive total return prospects. However, at some point, we believe they could belong in the same club as the other REITs that we once followed:

- QTS Realty

- CyrusOne

- CoreSite Realty

- Excel Realty Trust

- Preferred Apartment Communities

- VEREIT

- Weingarten Realty

- Taubman Centers

- Healthcare Trust of America

- Duke Realty

- Gramercy

- MGM Growth Properties.

As always, thank you for reading and commenting!

For further details see:

It's Time To Play REIT M&A