ITT - ITT: Good Growth Prospects With An Attractive Valuation

2023-11-09 13:19:40 ET

Summary

- ITT Inc. has a strong backlog that is expected to contribute to revenue growth in the coming years.

- The company's Motion Technologies segment is poised to benefit from gains in the EV market, recovery in Chinese OEM production, and capacity expansion.

- Strength in the Connect & Control Technologies and Industrial Process businesses, supported by strong demand in various end markets, will further contribute to revenue growth.

Investment Thesis

ITT Inc. ( ITT ) has a strong backlog which is expected to contribute to its revenue growth over the next few years, and the company’s Motion Technologies ((MT)) segment should benefit from EV market share gains, recovery in Chinese OEM production, and capacity expansion in the coming quarters. In addition, strength in its Connect & Control Technologies ((CCT)) and Industrial Process businesses supported by strong demand in the Aerospace, Defense, General Industrial, and energy end markets should further add to the revenue growth. Beyond 2023, the company’s revenue is poised to benefit as the inventory destocking in MT’s aftermarket and CCT’s connector distribution businesses should likely end in FY24. Besides organic growth, ITT’s strong balance sheet should enable it to pursue bolt-on acquisitions driving inorganic growth. In terms of margins, price increases, productivity initiatives, and volume leverage should benefit the margin growth. The valuation also looks attractive when compared to its historical averages. An attractive valuation coupled with good growth prospects makes ITT stock a buy.

Revenue Analysis and Outlook

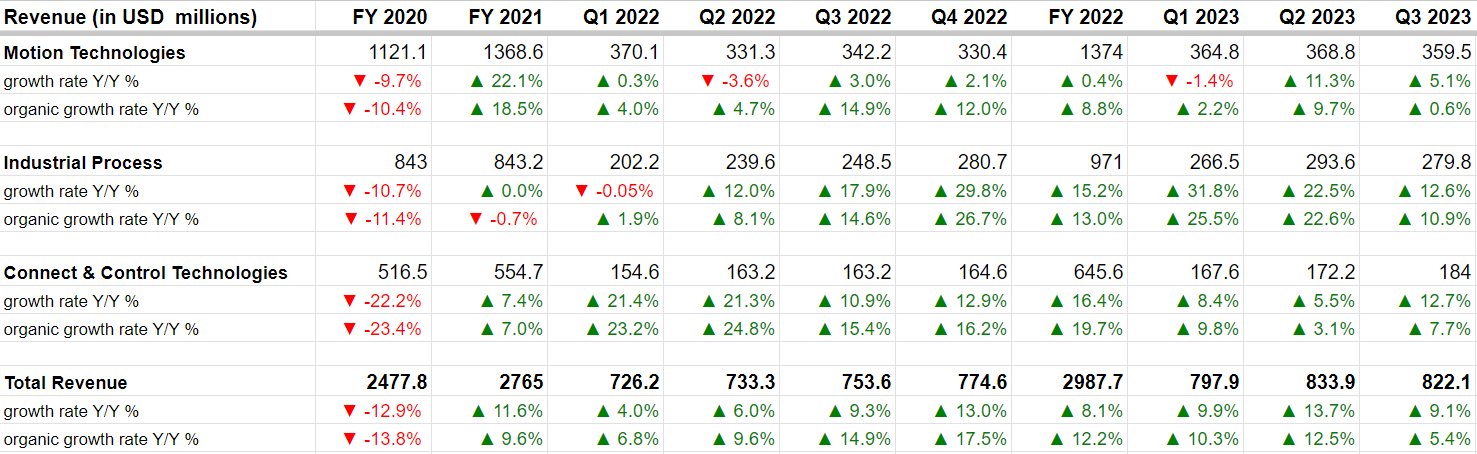

Post-pandemic, ITT has seen good growth in revenues with strength across its business segments. In the third quarter of 2023, the company recorded a 9.1% Y/Y increase in revenue to $822.1 million on a reported basis and 5.4% Y/Y organically. The increase in organic sales was driven by higher sales volume and pricing actions, particularly in the Motion Technologies Friction OE business, the Industrial Process pump project, baseline pumps and aftermarket businesses, and the Connect & Control Technologies components business. Additionally, FX translation favorably impacted the revenue by 3%. Further, the acquisition of Micro-Mode contributed 1% to the positive results.

In the MT segment, revenue grew 5.1% Y/Y on a reported basis and 0.6% Y/Y organically driven by higher pricing in KONI, Axtone, and Wolverine, and a 7% Y/Y growth in its Friction OE business with a 25% Y/Y growth in China OE.

The IP segment’s revenue increased 12.6% Y/Y and 10.9% Y/Y on an organic basis attributed to growth in aftermarket of 14% and pump projects sales growth of 21%.

The CCT segment’s revenue rose 12.7% Y/Y and 7.7% Y/Y organically led by 25% growth in aerospace components and 9% growth in defense which more than offset the impact of continued connectors distribution destocking in Europe.

ITT’s Historical Revenue Growth (Company Data, GS Analytics Research)

{kind=link}

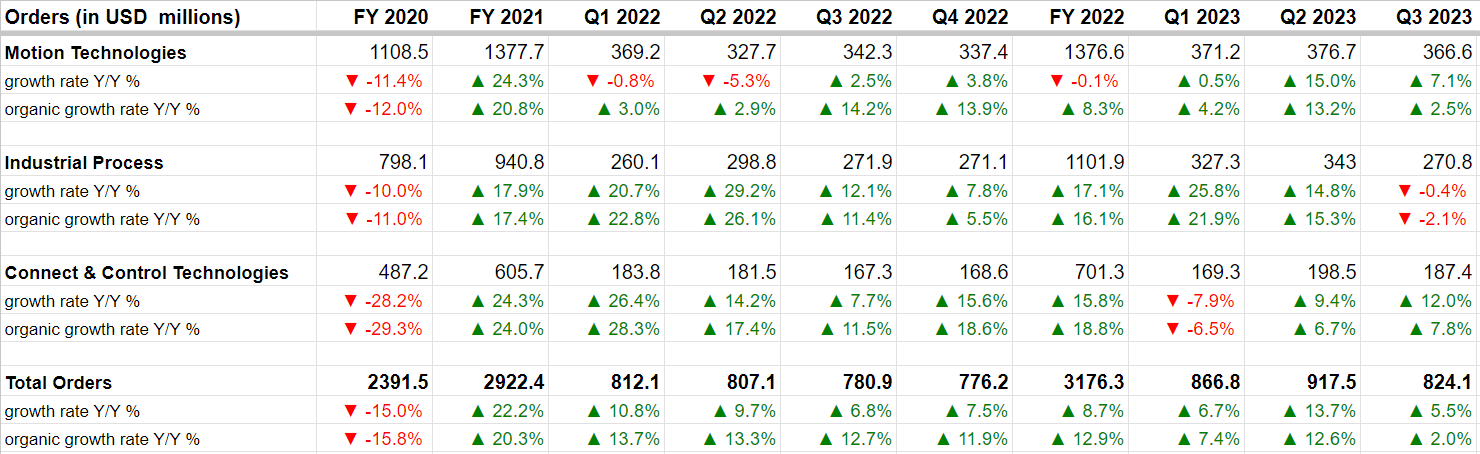

In the third quarter, the company booked orders worth $824.1 million, up 5.5% Y/Y on a reported basis and 2% Y/Y organically attributed to pump project wins and aftermarket demand in the IP segment, commercial aerospace and defense awards in the CCT segment, and Friction OE and rail share gains in the MT segment.

ITT’s Historical Orders Growth (Company Data, GS Analytics Research)

{kind=link}

Looking forward, I’m optimistic about the company's growth prospects.

The company ended Q3 with a solid backlog of ~$1.2 billion, up ~13% versus the end of last year. This strong backlog provides good visibility on the company’s future revenue growth.

Segment Wise, the demand environment continues to remain strong for Motion Technologies OE business and the company reported a ~2.5% Y/Y increase in organic orders on top of ~14.2% Y/Y increase in organic orders seen in Q3 2022. The company continues to gain market share in the EV market with 30 new platform wins in Q3 and over 130 awards Year-to-Date at a win rate that is well above its current market share. The recovery in China OEM production as the country continues to reopen is another bright spot for the company. Further, the company is expanding capacity at its Termoli plant which should be complete by the end of Q4 2024 and help the company meet the strong demand.

Overall, management expects the Automotive OEM market to be up low-single-digits Y/Y in FY24 and given the company’s track record of gaining market share, its revenue and orders from this market should grow at a higher pace.

On the aftermarket side, the Motion Technologies segment is seeing some decline due to inventory reduction at distributors. While Q4 is expected to be another slow quarter for this business, inventory reduction can't continue forever and this business is likely to return to growth in FY24.

In the company’s Connect & Control Technologies segment, recovery in the Aerospace end market is expected to help the company’s growth. Further, given the recent geopolitical development, the defense demand is also likely to see a pick up in the near to medium term. The company is also doing a good job in terms of share gains in OE and SKU expansion with distributors which should help growth. This segment has also seen inventory destocking for the last 3-4 quarters in the connector distribution business in Europe and I expect this destocking to end sometime in 2024, helping sales growth.

Finally, in the Industrial Process business, the company is seeing strong demand in general industrial and energy end markets and its backlog was up ~14% Y/Y. While orders were slightly down Y/Y in Q3, management noted that it was primarily a timing issue and orders rebounded strongly in October with large cycle projects orders up ~40% Y/Y in October. Management also noted that its project funnel is up ~16% versus the beginning of this year. This indicates continued strength in the Industrial Process segment. Further, the company’s aftermarket business remains solid given the company’s strong installed pump base and it is also increasing distribution which should help sales.

In addition to good organic growth, management has also indicated that it intends to accelerate capital deployment for M&As in the coming quarters. It recently acquired Svanehøj and I expect the company to use its strong balance sheet to drive further inorganic growth.

Overall, I am optimistic about the company’s revenue growth prospects.

Margin Analysis and Outlook

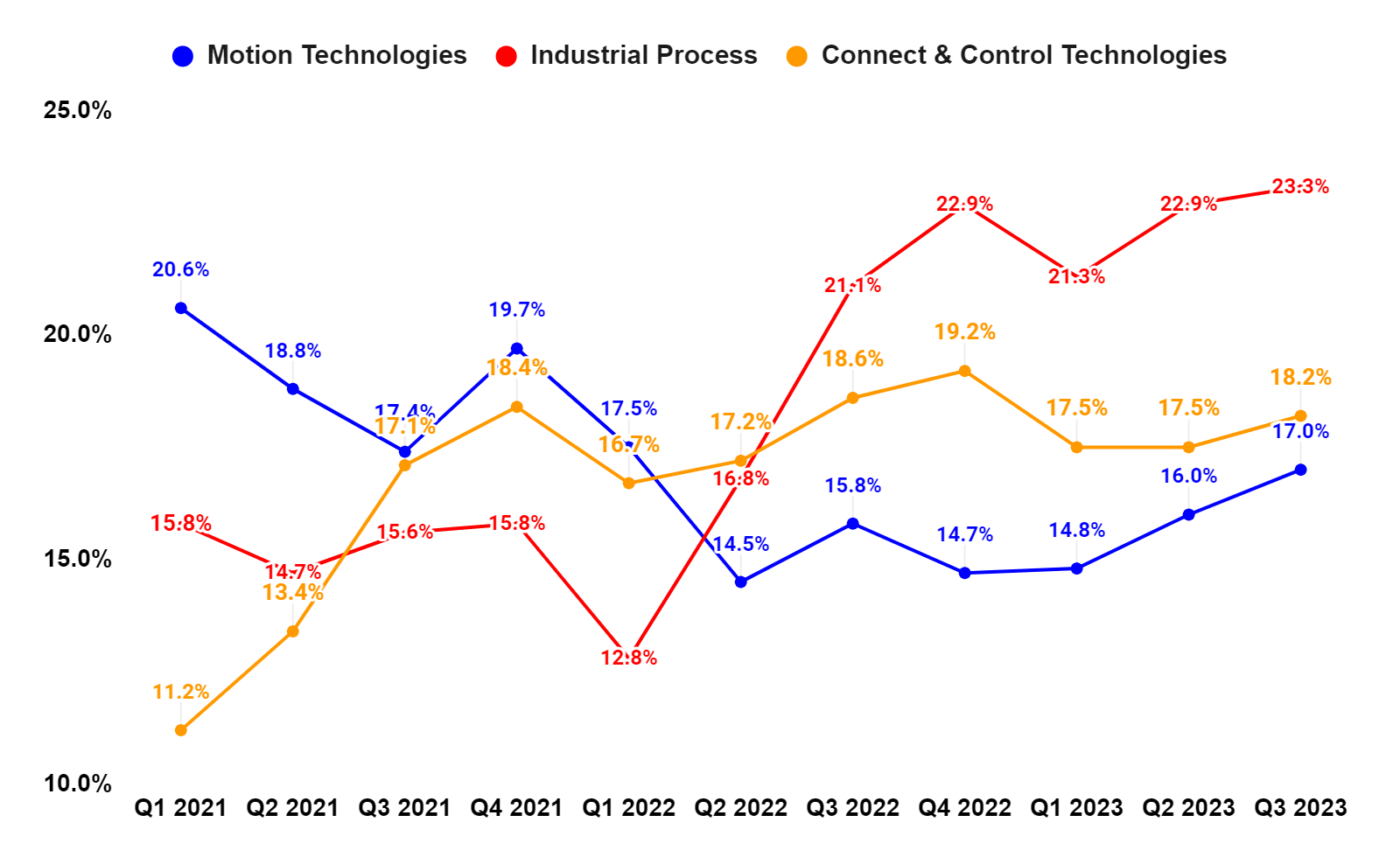

In Q3 2023, the company’s total segment adjusted operating margin expanded by 120 bps Y/Y to 19.4% driven by higher sales volume, pricing actions, and productivity savings. These positive factors were partially offset by higher labor and overhead costs due to continued supply chain challenges and cost inflation, and increased strategic growth investments.

Segment Wise, the IP segment demonstrated an impressive 220 bps Y/Y of adjusted operating margin expansion attributed to pricing benefits and shop floor productivity. The MT segment’s margin improved 120 bps Y/Y while the CCT segment’s margin contracted by 40 bps Y/Y. The strong margin performance in the IP and MT segments more than offset the margin contraction in CCT segment and contributed to the Y/Y improvement in total segment-adjusted operating margin.

ITT’s Segment Wise Adjusted Operating Margin (Company Data, GS Analytics Research)

{kind=link}

ITT’s Consolidated Segment Adjusted Operating Margin (Company Data, GS Analytics Research)

{kind=link}

Looking forward, the company should benefit from the carry forward impact of past price increases as well as upcoming price increases.

According to management, the Industrial Process backlog’s margins are currently 200 bps above what they were at the beginning of this year. While they have not talked about the backlog margin of other segments, I believe they also have seen a good increase given the way ITT has implemented price increases in the recent quarters. This bodes well for future margin growth. In addition to favorable price/cost, the company should also benefit from productivity initiatives and volume leverage from growth.

The company reported a segment operating margin of 19.4% last quarter which is close to its long-term target of 20%. Given the strong incremental margin ITT is seeing, I see a good chance for upward revision in its margin targets in the coming years. Overall, I am optimistic about the company’s margin growth prospects.

Valuation and Conclusion

ITT’s stock is trading at a 17.24x FY24 EPS estimate of $5.84 and a 15.53x FY25 EPS estimate of $6.48 which is at a discount compared to its 5-year average forward P/E of 19.39x .

The company has good near-term and long-term growth prospects driven by a strong backlog, China reopening gaining momentum, capacity expansion, favorable end market demand, inventory destocking headwind ending in FY24, inorganic growth from M&As, strong pricing, and productivity improvements. Hence, I believe the stock is a good buy at current levels given its good growth prospects and a lower-than-historical valuation.

For further details see:

ITT: Good Growth Prospects With An Attractive Valuation