ITT - ITT: Solid Q2 Earnings Report Brings Optimism

2023-08-11 03:13:22 ET

Summary

- ITT Inc. reported strong growth in its last earnings report, with a 13.7% YoY increase in revenue and over 40% growth in net income.

- The company operates in the industrial sector and has managed to handle high material costs and wage inflation well.

- ITT aims to achieve a CAGR of 5-7% and grow EPS by an additional 10% annually, with a strong backlog and solid partnerships supporting its growth prospects.

Investment Summary

The last earnings report from ITT Inc (ITT) showcased the company is capable of growth despite a challenging macroeconomy. The top line saw a 13.7% YoY increase whilst the bottom line grew by over 40% as the management made strong progress on improving margins and the overall operational performance.

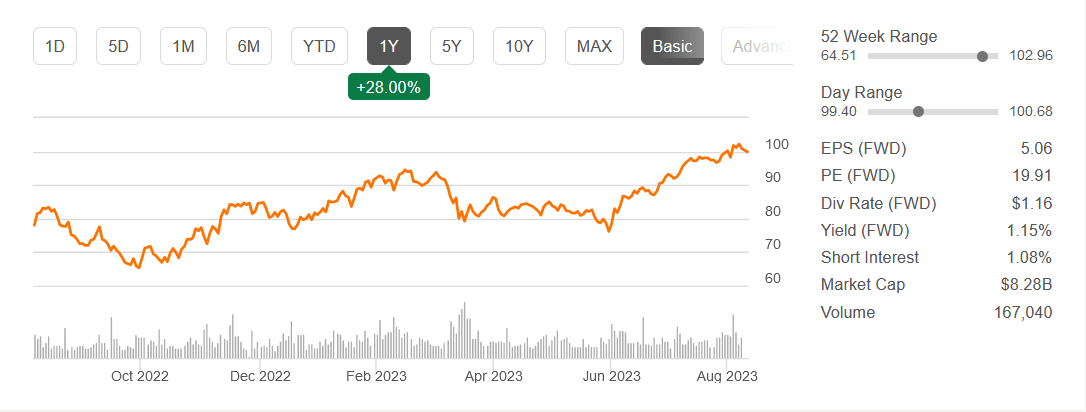

Operating in the industrial sector, there are still some concerns about how high material costs are affecting companies, but also how wage inflation is damaging earnings. It seems that ITT has managed to handle this very well and continues to chug along. The share price has run up a lot in just the last couple of months but I don't think we have reached an unreasonable valuation yet. The p/e still sits at just over 20, and paying such a premium for the growth you are getting seems fair. As a result, I am rating ITT a buy right now.

Optimistic Outlook

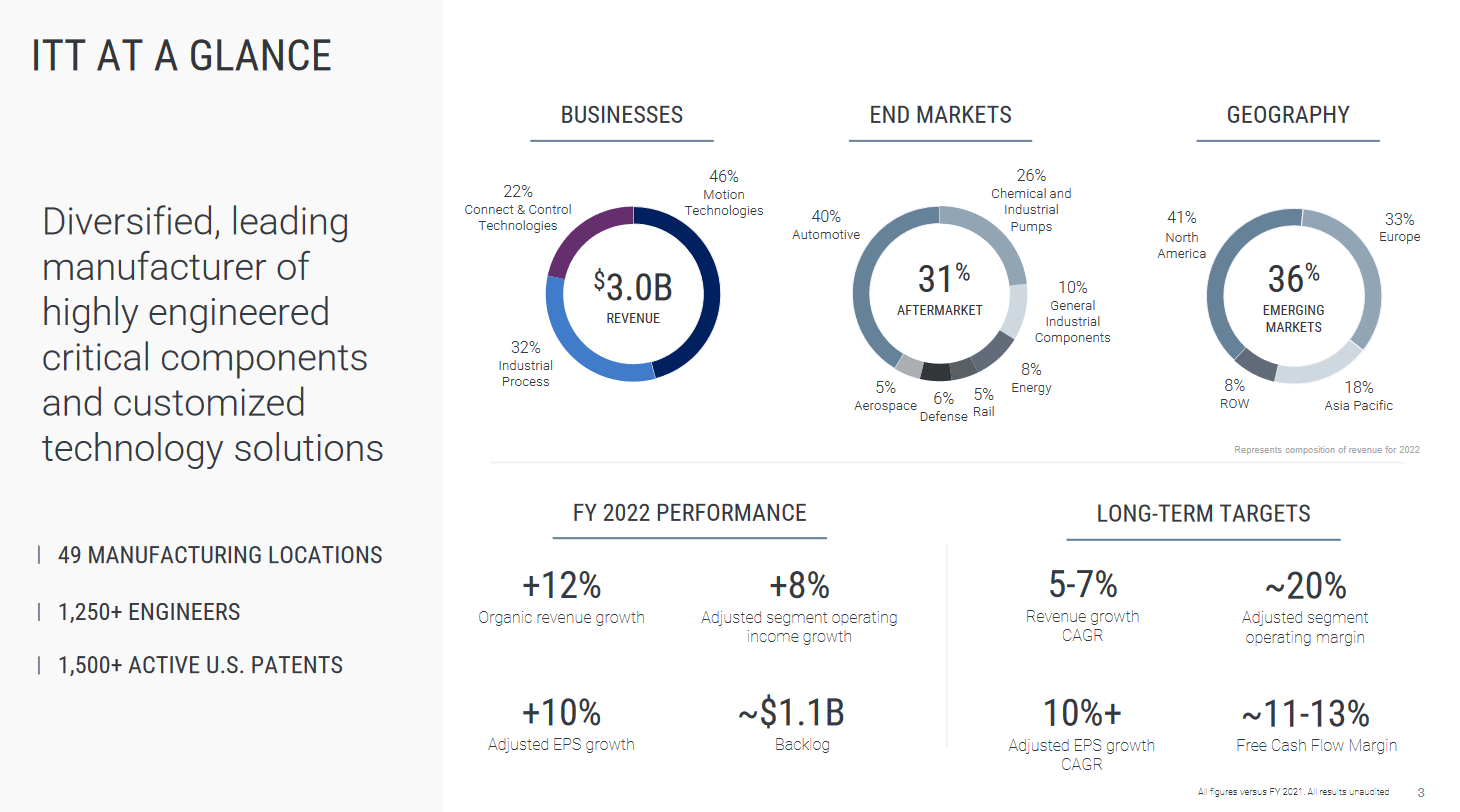

As mentioned earlier on in the article, ITT operates in the industrials sector where it has specialized in both manufacturing and selling critical engineered components and customized technologies for several end markets like transportation, industrial, and the energy market.

Within the business of ITT, three various segments make up the operations, these are Motion Technologies, Industrial Processes, and finally Connect & Control Technologies.

{kind=link}

The end markets for ITT are quite diverse with the largest one being automotive. In the recent earnings report that the company provided it was clear they have experienced a lot of demand from this market as luxury and sporting vehicles have risen demand for ITT, helping strengthen the bottom line of the business as the market is rather profitable to engage with.

Taking note of what the long-term targets of the company are achieving a CAGR of 5 - 7% is one, and one that seems reasonable if the company can keep up the same momentum they have had and capture further demand.

Where I am optimistic about the performance of an investment in the company comes from the fact they aim to further grow the EPS by an additional 10% annually. Right now the net margins sit at 13.4%. Historically, the company has just had 9.5% here but with the strong improvements it seems that ITT is heading higher and this optimism has led to the share price moving upwards as much as it has done.

Company Overview (Investor Presentation)

As for the steps the company is taking in efforts to raise revenues and also margins is securing solid partnerships and building up a strong backlog too. Going into 2022 the backlog sat at $1.1 billion, which is just above 30% of the total revenues they generated in 2022. That underscores to me the fact that ITT has a supporting base on which it can grow further. It seems they are also able to pass down some costs to customers as they grew margins much faster than the revenues.

{kind=link}

From the last report we got from the company, we can see that there are some headwinds that they have admitted. One of them is the inflation of material costs and labor costs. These seem like quite sticky issues and seeing a decrease in either of them I don't think will happen in the near term. But a significant growth driver for the business has been the favorable pricing environment and pricing actions they have taken to dilute some of these otherwise higher operating expenses.

Risks

In the immediate horizon, ITT stands at a crossroads, grappling with potential supply chain disruptions and the lurking specter of persistent inflation in raw material costs. While ITT's adeptness in navigating these challenges has been solid so far, the specter of these uncertainties looms in the near-term horizon, necessitating a prudent approach.

{kind=link}

The narrative of ITT's resilience extends to its ability to manage these critical risks, yet the undercurrent of these challenges remains a significant aspect of the business's landscape in the foreseeable future. It is this small line to walk between ongoing operational demands and the unpredictability of external factors that we need to watch the current trajectory of ITT. It seems like these issues are rather short-lived and the management of ITT is still very optimistic about the outlook for the year 2023.

ITT's balance sheet boasts a strong position, reinforced by the strategic cash position for further acquisitions. Yet, the potential for execution hurdles looms, casting a shadow on the company's expansion initiatives. While it's undeniable that the management's track record in identifying and integrating growth-accelerating acquisitions has been solid, the complex climate of execution risks and the possibility of overpayment shouldn't be overlooked. We are still in a pretty high-interest environment and taking on too much debt to fuel growth might come back to bite them as interest expenses would be rising quickly.

Financials

Taking a step into the financials of the company I mentioned just above here the fact I think they are in a solid position right now.

Assets (Balance Sheet)

The asset base for the company is a highlight as they have around $460 million in cash buy also nearly $700 in receivables as the company can drive strong growth from higher-order levels.

Liabilities (Earnings Report)

Looking at the liabilities of the company I this the lack of debt puts ITT in a fantastic position to continue and grow and deliver strong results. Future acquisitions seem like a reason possibility and I am excited to see what they do in the coming years as demand builds up.

Valuation & Wrap Up

For investors that want exposure to a fanatically run company in the industrial sector which is far from overleveraged and boast a solid balance sheet then ITT should be up there. The company has experienced strong demand from several end markets and this helped raise the orders by 10% YoY in the last quarter.

{kind=link}

The price of the company has grown quite quickly and right now sits at an FWD p/e of 20. This is not above where I would be comfortable buying the current price. I think with a company aiming to be growing the EPS by 10% annually in the long term paying such a premium is fair. Rating ITT a buy.

For further details see:

ITT: Solid Q2 Earnings Report Brings Optimism