CA - Ivanhoe Mines: Expansion Looks Bright But Buyer Beware

2023-04-11 08:00:00 ET

Summary

- Ivanhoe mines has slightly underperformed the market since I last wrote it last year.

- FY 2022 shows Ivanhoe in a healthy financial position.

- Kamoa-Kakula gives Ivanhoe a strong revenue base.

- Platreef and Kipushi are promising and will add earnings revenue in the future quarters.

- Risks should be understood and not understated.

Background

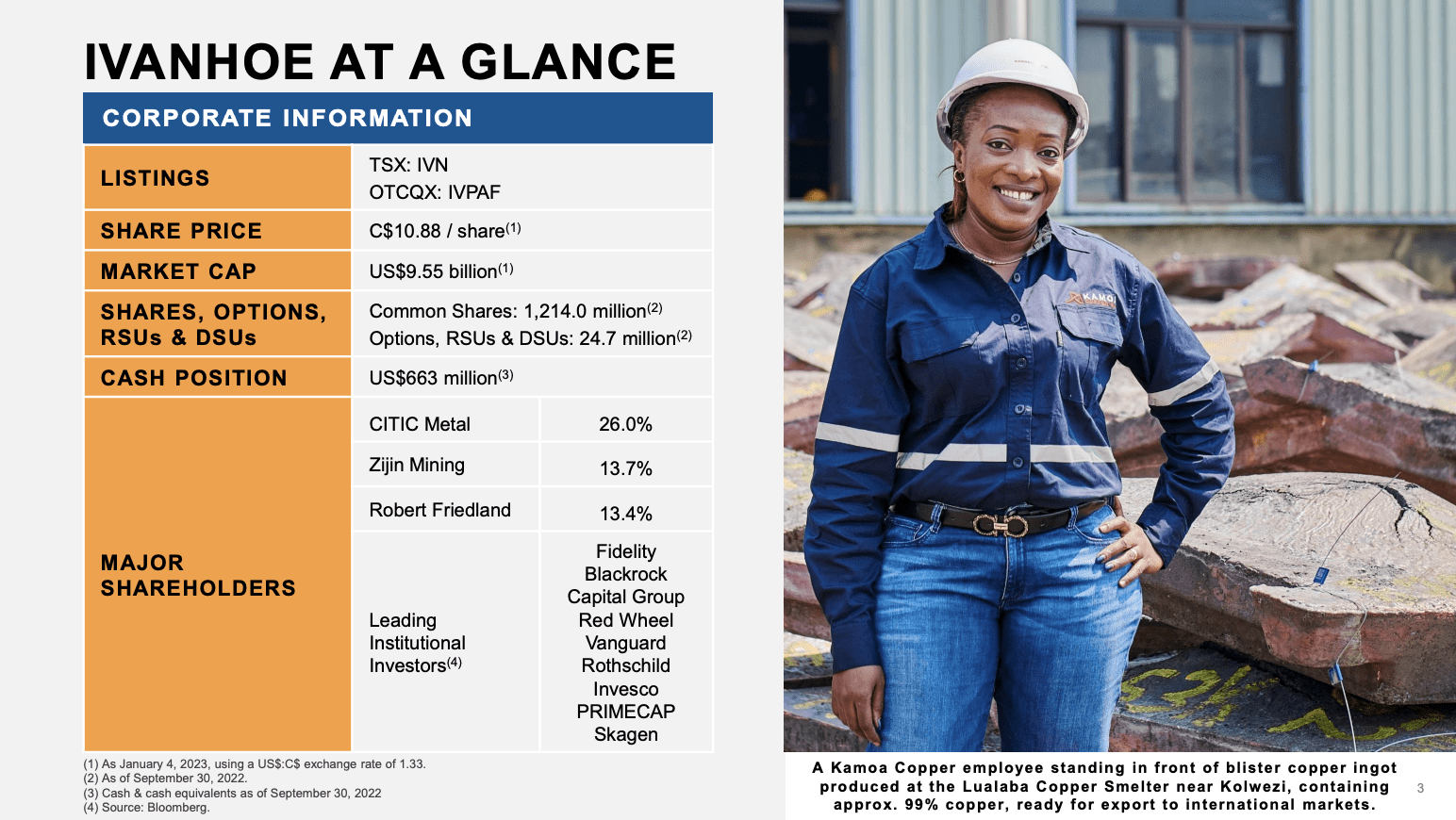

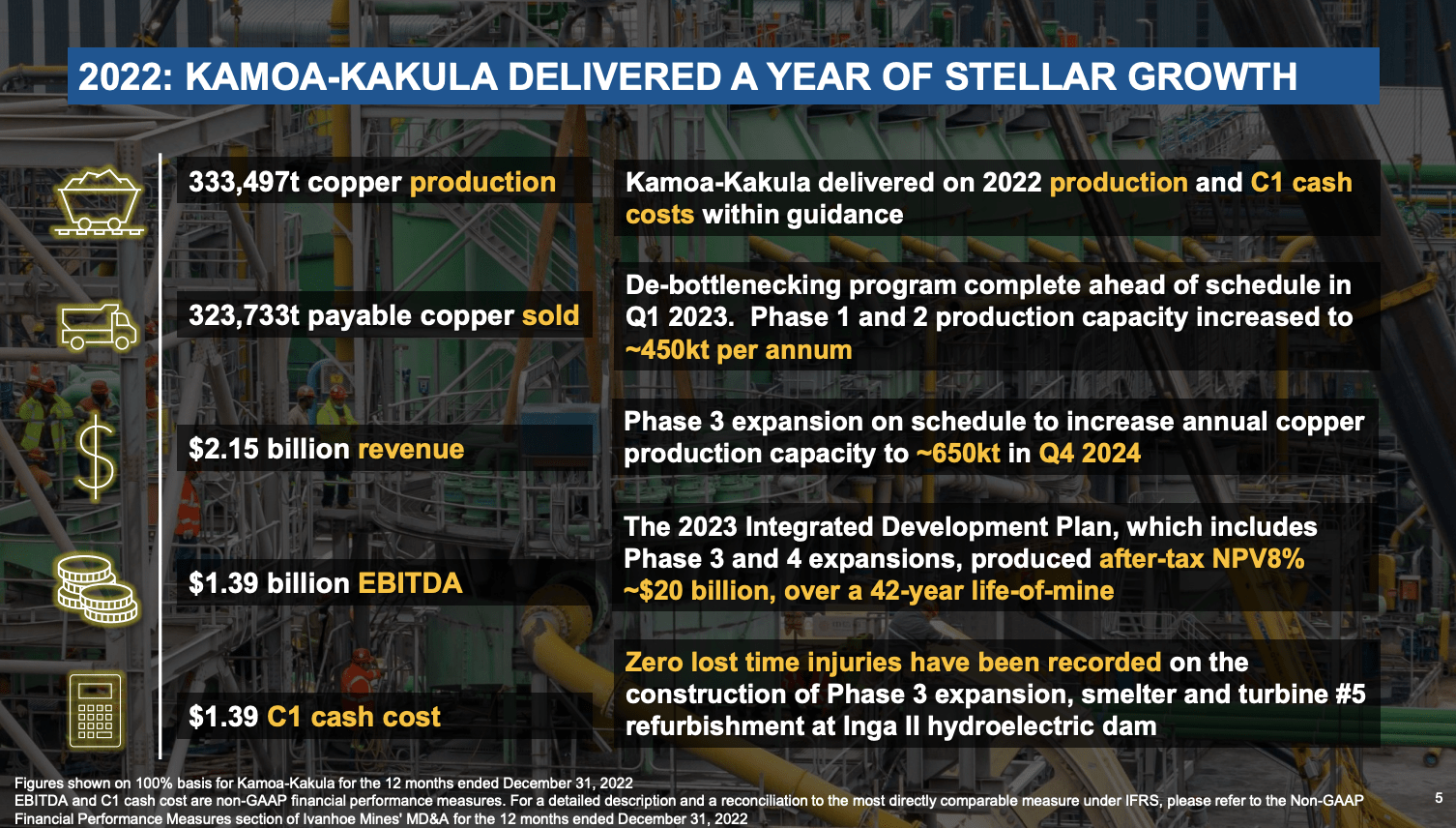

Ivanhoe Mines ( IVPAF ) is a large mining conglomerate primarily focusing on the mining and exploration of copper reserves in Africa. I previously wrote an article about Ivanhoe mines back in January 2022 . This was during a rapid rise in the price of copper and my reasoning back then was, if the price of copper continued to rise then Ivanhoe's stock price would do very well. Additionally I argued that if the high price of copper was sustained, then Ivanhoe would be able to make enough money to cover their expanding operations at the Platreef and Kipushi mines. During this period of time, Ivanhoe's premier joint venture mine, Kamoa-Kakula, raked in 1.4 billion in earnings with revenues of 2.1. billion at a realized copper price of $3.79/lb with costs at $1.39/lb. 2022 was a very profitable period for Ivanhoe but to date since the article Ivanhoe has had the exact return % of the S&P 500 index. Keep in mind, Ivanhoe had a much bigger swing than the S&P 500 index. Ivanhoe Mines fell to lows as $5.70 per share at one point. I believe the reason that Ivanhoe didn't appreciate as much as it could have is because of all the upcoming risks and costs from the Kipushi, Platreef, and Western Forelands projects. All of the aforementioned projects show promise but have yet to show real shareholder value other than their multi billion dollar NPV. While this adds assets to Ivanhoe's balance sheet it also adds an incredible amount of risk due to the nature of mining in Africa. However, due to this massive price swing in 2022 I believe that these costs have been factored into the current price. Ivanhoe Mines represents a lot of potential reward but I have to re-rate Ivanhoe Mines to neutral due to the intensive capital needed for expansion and exploration and for the political instability in the region.

Investor Presentation January 2023

{kind=link}

Ivanhoe does have many prominent and important backers. This is mainly due to Robert Friedland and his previous successes in the mining industry. Friedland built up his reputation as the head of the original Ivanhoe Mines which was a joint venture exploration company exploring the South Gobi in Mongolia. This later led to the Oyu Tolgoi mining complex which I previously wrote about here . With billions in capital behind the major money managers I doubt there will be much issue obtaining capital for fundamental reasons. However, there are inherent political risks both for ESG reasons and for political reasons in the Democratic Republic of the Congo. Nonetheless, evaluating Ivanhoe's assets from a fundamental perspective and a mineral economic perspective, it's hard to ignore the profits and fundamentals at play with Ivanhoe Mines.

Kamoa-Kakula Mine and its Risks

Ivanhoe's only operating mine is the Kamoa-Kakula mine. The joint venture is between Ivanhoe at 39.6% ownership, the Government of The Democratic Republic of The Congo at 20% equity, Zijin Mining Group at 39% ownership and Crystal River Global at .8%. This has been the way Ivanhoe has operated for some time now as high startup costs are very risky for mining companies with only a couple billion in market capitalization. This is why many joint ventures fail because the projects become too capital intensive before production starts and debt starts to pile on. This is not the case from Kamoa-Kakula as all parties have vested political and economic interests in the mine. Zijin Mining groups largest shareholder is a state owned property group. This mine is important for the Chinese government as they attempt to jump start their economy through investment, which will require copper for different industrial uses. Another government involved in the project is the home country of the Democratic Republic of The Congo. In the past there have been cases of African countries deciding to nationalize mines at the behest of government interference. This is relatively less risky in the Congo as the country is very cash strapped and needs investment from foreign countries to survive. A little more risk does occur here as Ivanhoe has concentrated most of their mines in the DRC as both their Kipushi and Western Forelands projects are both located in the south of the DRC.

Ivanhoe Mines Full Year 2022 Results

{kind=link}

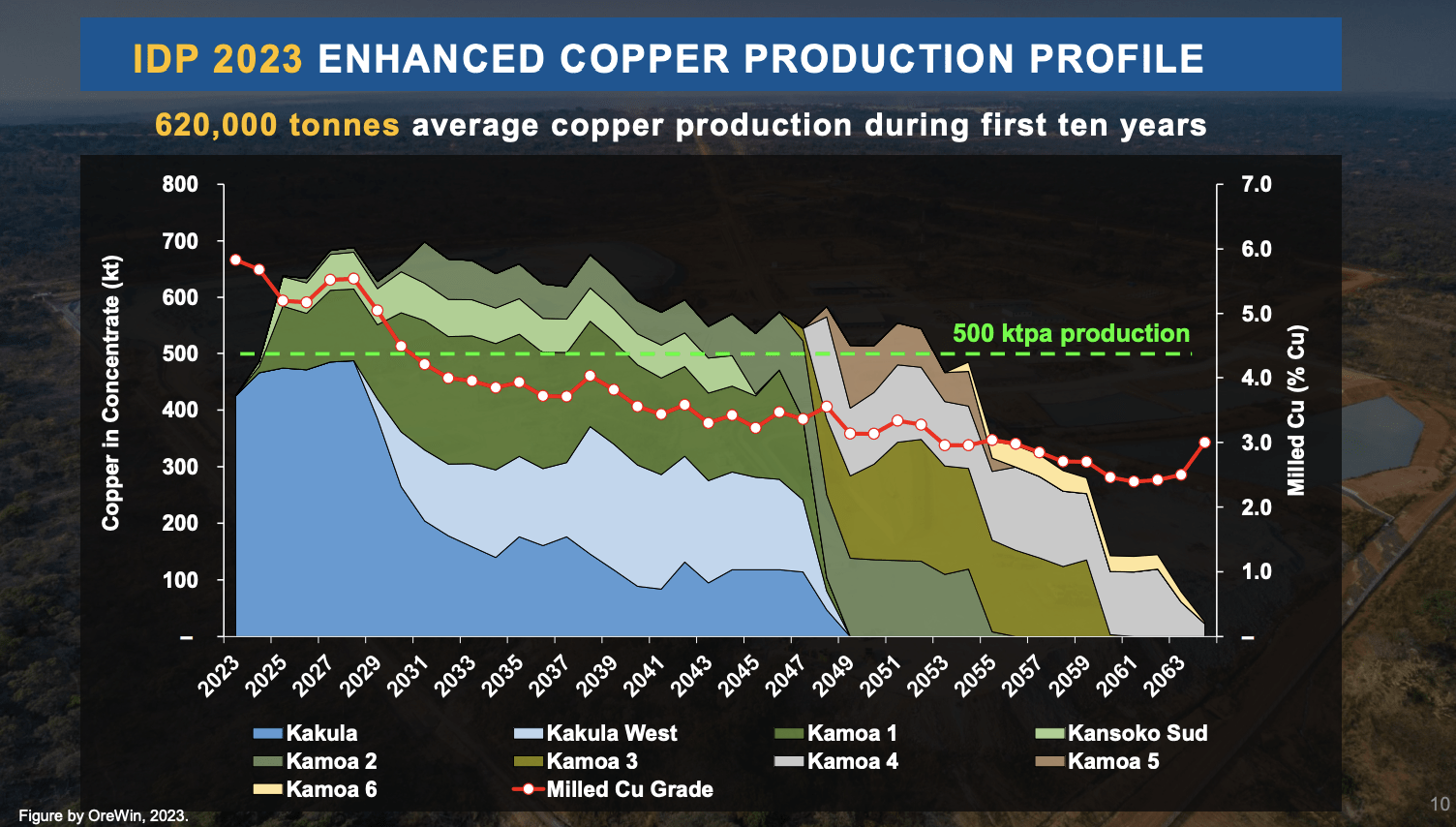

Even though Kamoa-Kakula may have excess risks due to location, it's hard to deny the mines profitability impact for Ivanhoe. The company reported 65% gross margins in 2022 which is much higher than the 28.55% gross margins for the metals & mining sector . Following their expansion predictions, this will place Kamoa-Kakula in the top 10 largest copper mines in the world at some of the lowest costs per lb. With production of 333,497 tonnes of copper and contracts to sell 323,733 tonnes of copper there is no shortage of demand for copper from Kamoa-Kakula. Production capacity is also increasing at the same time production will scale. This is not even factoring in the hike in demand that is likely coming from China's reopening. the 2024 production capacity will be close to matching the output projected by 2025 of 650,000 tonnes per annum. This should not be too much of an issue since 97% of Ivanhoe's 2022 production is under contract.

Kamoa-Kakula IDP 2023 Investor Call Agenda 2023

{kind=link}

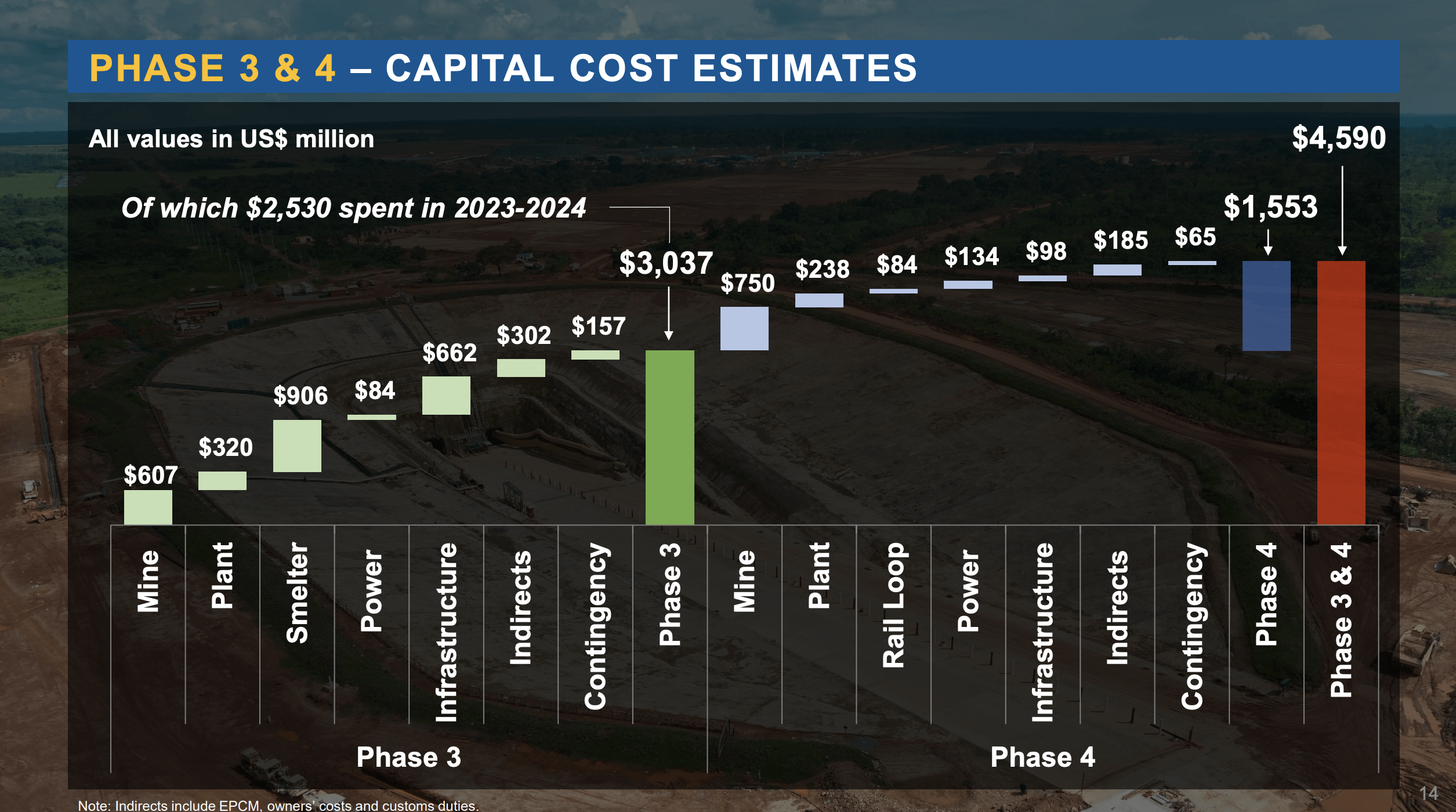

Costs are one of the biggest concerns I have for Ivanhoe Mines. Even though the net asset value of the mine is projected to be 20 billion Ivanhoe would only own 5 billion of this value with their current stake. Ivanhoe would then have a projected debt of 1.7 billion to reach that 5 billion mark. This wouldn't be as much of a concern for a 9 billion dollar mining company if there wasn't future exploration projects in the coming years. Additionally Ivanhoe owns a bigger percentage of their other projects. Ivanhoe owns 100% of Western Foreland, 64% of Platreef, and 85% of Kipushi. The startup costs of these mines will likely be in the multi billion dollar range. This requires Ivanhoe to take out debt that would represent a sizable margin of their market capitalization. Even though there are notable backers of Ivanhoe stock such as Fidelity and Blackrock, investors need to be pragmatic and understand that large Funds won't be afraid to drop Ivanhoe if they don't reach production targets. This could lead to volatile earnings calls both up and down in the future.

Kamoa-Kakula IDP 2023 Investor Call Agenda 2023

{kind=link}

When evaluating Kamoa-Kakula's production it's important to keep in mind the life of the mine and the purity of its copper. The average purity is around 4.8% for copper mines in the world, Kamoa-Kakula will average a purity of 5.5% over the next 10 years. This is important because this requires less ore to be milled for more production of copper. This puts less wear and tear on machinery which is very important when considering a long term investment in a mining asset with a long mine life.

Copper Outlook

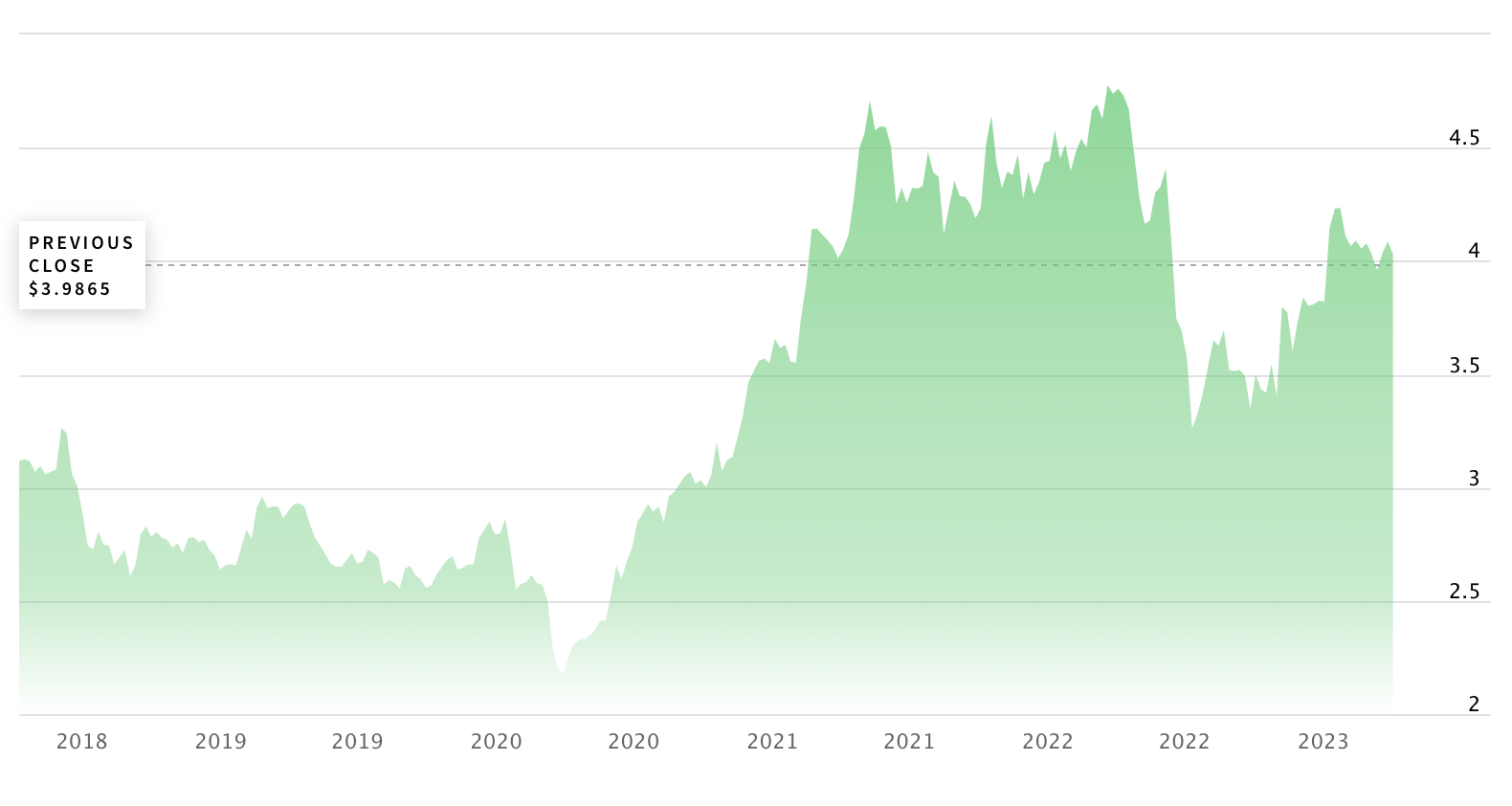

NASDAQ Copper Price Historical Data (NASDAQ Copper Price Historical Data)

{kind=link}

Copper is a needed metal that has applications across a broad range of industries. Some uses include wiring, motors, industrial machinery, pipes, and more. While this may seem like industries with stable demand for copper this is far from true. One industry that requires a lot of copper to grow is clean energy since copper has conductive properties for electricity. This is why copper is the 'go to' for the use of copper wiring in electric vehicle batteries and charging stations. These are multi billion dollar industries that are projected to have massive growth numbers in the coming years. There are also government incentives and targets to have a clean energy transition away from fossil fuels. I believe this is a mega trend in the making, due to the investment that has poured into the energy industry in the past couple of years.

In terms of copper price it's tricky to determine the fluctuations year to year. Even though the long-term picture is intact it's tough to determine how copper will perform just in 2023. I am of the opinion that copper will have a strong 2023 because of the pent up demand from China.

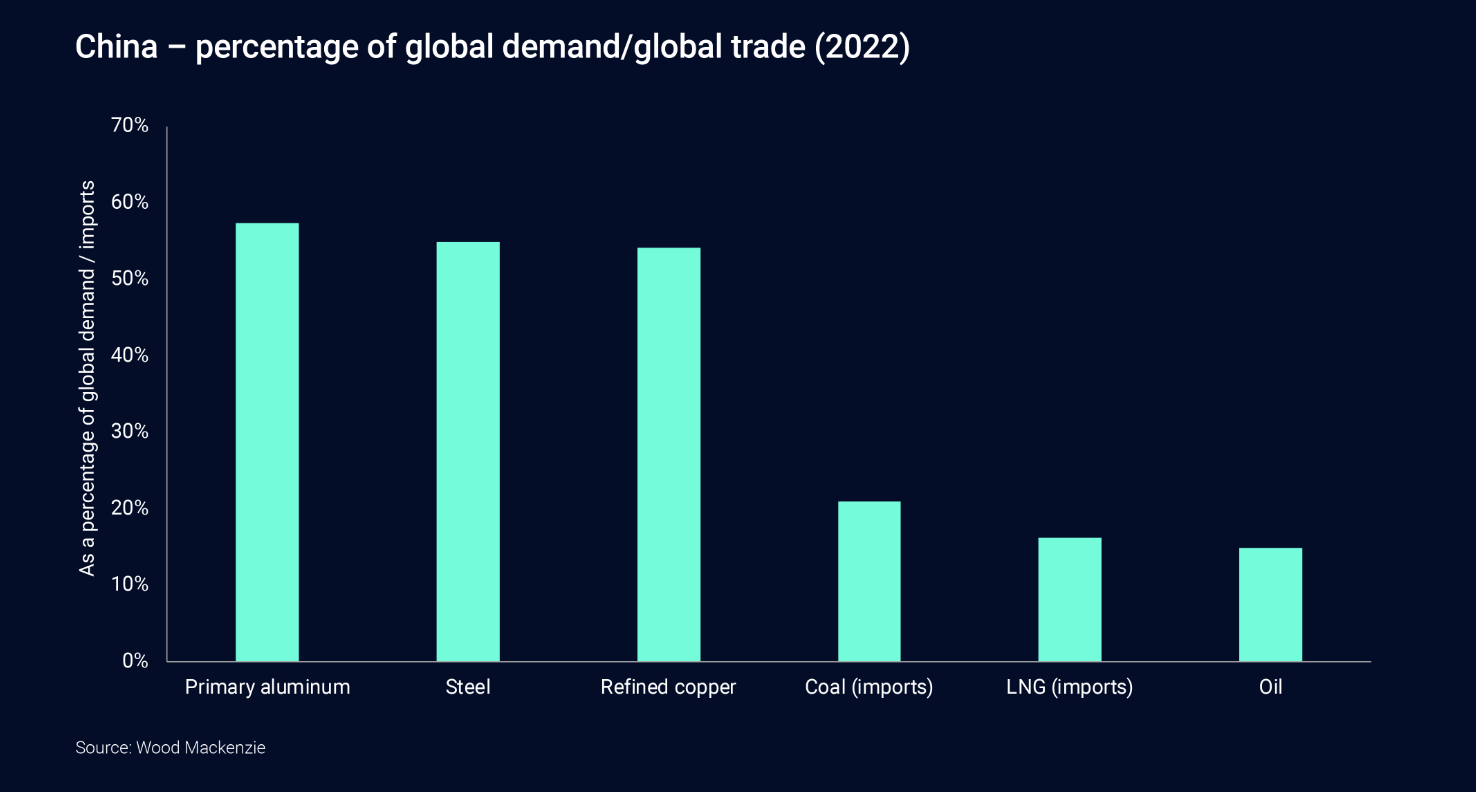

Wood Mackenzie 2023 Copper Outlook (Wood Mackenzie 2023 Copper Outlook)

{kind=link}

China is a big consumer of copper representing 55% of global demand in 2022. As the country reopens I would expect there to be further urbanization on the outskirts of the city centers which means there will be copper wiring and pipes needed in every apartment building across the country. In 2023 I will be looking primarily at Chinese demand for copper as the biggest driver of price action.

Valuation

It's hard to value Ivanhoe today because there is so much promise but so much unknown. Additionally investors have yet to see how Ivanhoe will fund each mine expansion. The only way to value Ivanhoe currently is to consider earnings from current operations. Ivanhoe is projecting 390,000 tonnes of copper on the low end of estimates. This would mean Kamoa-Kakula would generate $1.47 billion. Considering Ivanhoe's 39.5% stake this would leave Ivanhoe a profit of $541.15 million Using the industry standard 20x earnings multiple, this would mean Ivanhoe mines would be worth an estimated $10.82 billion dollars. Currently Ivanhoe is valued at $10.52 billion which represents just a 2.8% increase from today's levels.

These figures do not include all the equity Ivanhoe has in the various projects in the Democratic Republic of the Congo and South Africa. This could be looked at as a positive or a negative for some investors. On one hand, the growth potential is very large but on the other hand it will take billions in capital over many years to put the mines in production.

Conclusion

If you are looking for a Copper JV with potential, then Ivanhoe Mines should be at the top of your list. In my original article I made a big point about the need for copper in the coming years. Robert Friedland explained this more eloquently

700 million tonnes of copper had been mined in human history and a further 700 million tonnes would be needed in the next 22 years just to keep annual global growth rates of 3%.

-Source: ( Mining.com reporting on Indaba conference 2022 )

Copper will be in demand and Ivanhoe will be a top producer. With all this said, I have to stand behind my neutral rating because of valuation and political concerns. I look forward to covering Ivanhoe Mines in future quarters and seeing how exploration efforts develop.

For further details see:

Ivanhoe Mines: Expansion Looks Bright But Buyer Beware