ZION - July Fed Meeting Preview: Are Stocks Overvalued Ahead Of A Likely Rate Hike?

2023-07-24 07:30:00 ET

Summary

- The Federal Reserve will conclude their two-day July policy meeting on Wednesday, July 26.

- A 25 basis point increase in the overnight benchmark rate to a range of 5.25% to 5.50% is widely expected.

- I expect Chairman, Jerome Powell, to highlight banking resilience and modest economic cooling in his post-meeting press conference. He may also address the "stickier" components of the CPI.

- I view another 25bps increase in September or later in the fall as likely and not yet priced into current stock valuations.

- A 10-15% pullback in the major indexes in the months ahead would be viewed as healthy for a more sustainable rally in the final months of the year.

The Federal Reserve (“Fed”) is expected to increase its overnight interest rate by 25 basis points (“bps”) to a range of 5.25%-5.50% following the conclusion of their July policy meeting this week.

Of greater interest and debate is what the Fed will do in September or later in the fall. The stakes of the post-meeting press conference from Chairman, Jerome Powell, therefore, are high.

What To Expect From Powell’s Prepared Remarks

Resiliency Of The Banking System:

Supporting a pause in June, Powell pointed to giving the economy time to adapt to their cumulative actions thus far. Banking, particularly, warranted heightened attention. “We don’t know the full extent of the consequences of the banking turmoil that we’ve seen,” said Powell. “It would be early to see those, but we don’t know what the extent is.”

Recently released results from the regional banks likely provided Fed officials confidence of banking resiliency following high-profile failures earlier in the year. The more positive results also follow the Fed’s stress tests , which showed banks enduring relatively well.

One of the primary concerns of regional bank investors ahead of earnings was deposit flight. But banks, such as KeyCorp ( KEY ), Western Alliance Bancorp ( WAL ), and Zions Bancorp ( ZION ), all reported deposit figures that were either stable or higher than in the first quarter. Some, including Citizens Financial Group ( CFG ) and M&T ( MTB ), even reported deposit growth during the period.

To be sure, deposit stability came at the cost of higher interest rates to retain depositors. This weighed on profits at many regional banks in the second quarter. For instance, YOY profits were down 17% and 14% at WAL and ZION, respectively.

Losses also continue mounting on commercial real estate exposure. MTB reported a doubling in charge-offs due in part to several office buildings in New York City and Washington, D.C. PNC Financial ( PNC ) also reported a significant jump in charge-offs due to their office exposure. And looking ahead, PNC CEO, Bill Demchak, believes that there will be further problems in their office book.

I expect Powell to highlight the positive results of the stress tests and deposit stability among the regional banks. He may also point to tightening credit conditions as evidence that their current policy efforts are having their desired effect. As an area of concern, he may cite the rapidly deteriorating office market as one notable risk facing overexposed lenders.

Modest Signs Of Economic Cooling:

Powell’s confidence of engineering a “soft economic landing” is likely high and his commentary will likely be geared accordingly. Observers should expect Powell to point to the drop in the June inflation rate to its lowest reading in more than two years as positive progress.

Other economic indicators may also be referenced to support the cooling assertion. June retail sales , for example, rose less than expected. In addition, the Conference Board Leading Economic Index (“LEI”) declined again in June for the 15 th straight month, it’s longest weak-spell since 2007-2008. This was driven in part by more pessimistic consumer expectations and weaker new orders , to name two factors.

The weakness in orders could be clearly seen in the manufacturing and industrial sectors. The June PMI Manufacturing Index , for example, remained in contraction territory. And June U.S. Industrial Production missed expectations, with a negative reading on the month. Recent results from industrial and construction supply distributor, Fastenal ( FAST ), are reflective of the sector weakness.

On the other side of the token, Powell will also likely note that the inflation rate is still too high to declare victory. Powell could point to a tight labor market as one data point to support the notion that more cooling is needed. And he could also contrast the declining manufacturing index with the services PMI , which is expanding and running hotter than expected.

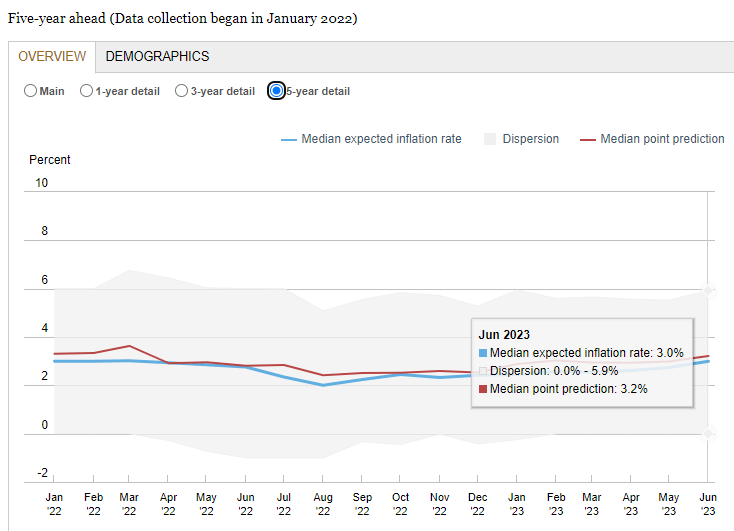

And though consumers’ near-term inflation expectations are dropping, they are not expecting inflation to reach the Fed’s target for at least five years. And even then, expectations are still elevated. This could lead Powell to convey messaging along the lines of “higher for longer.”

New York Fed Survey of Consumer Expectations - Inflation

{kind=link}

Stickiness In Certain Categories:

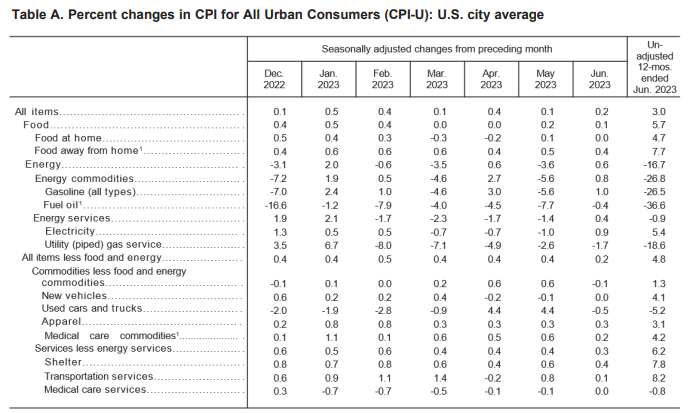

I expect Powell to provide commentary on categories that may prove more challenging to address through rate policy. Aside from the shelter component, the transportation services category has been one of the primary drivers in the monthly CPI.

{kind=link}

But it’s not airfare and rentals that are driving the gains in the category. On the contrary, these are on the mend due in part to lower fuel costs in the case of airfare.

The main driver, instead, is vehicle insurance and maintenance/repairs. These line items are more than four times higher than the overall CPI.

And I view the Fed as constrained in addressing these costs because they are mostly out of their control. Rising insurance costs, for example, are largely attributable to recent weather events.

Hurricanes, such as Ian in Florida, and major flooding in the northeastern states have taken a toll on insurers, and the costs are now being borne by policy holders. Higher interest rates are unlikely to change the trajectory of these costs, at least in the near-medium term.

Similarly, costs surrounding repairs and maintenance are up simply because miles driven have been on the increase. This has been complemented by an increase in the average age of vehicles on the road. And I believe this trend is unlikely to reverse course due to the average cost of used and new vehicles. For most, prices are still too high, even with recent declines. Fed policy perhaps can impact the market for used and new vehicles. But I believe this will take longer to play out.

Weather-related events like the recent heat waves could also affect non-core inflationary pressures in the food category. Unfavorable conditions for planting, olive trees for example, could correspond to higher prices in complementary products. Case in point, extra-virgin olive oil is up nearly 90% over the past year. And like insurance, it’s unlikely that Fed policy will be able to address the underlying issues.

There is more nuance with the shelter component due to the lag in how it’s reported on the CPI report. And I expect Powell to address this in his commentary. But for other areas, such as in transportation-related costs and those affected by recent weather events, his remarks may be less inspiring for resolution.

How Many More Times Will The Fed Increase Interest Rates?

I expect the Fed to increase their benchmark rate two more times in 2023, the first being a probable 25bps increase following their upcoming July policy meeting and one more 25bps increase in September or later in the fall. This would indicate a year-end target range of 5.50%-5.75%. I then expect a policy reversal in 2024 resulting in an expected giveback of these two increases.

My expectations for the year-end range are in-line with the projections published in the Fed’s dot plot. This showed most officials expecting the rate to end 2023 at 5.6% , indicating two more rate hikes. Some, however, such as Atlanta Fed President, Raphael Bostic, see rates best left on hold for the remainder of the year.

But others have conveyed a more hawkish stance in recent weeks. At an event in Columbia University, Dallas Fed President, Lorie Logan, cited a stronger-than-expected labor market as support for more restrictive policy. And at an event hosted by the Brookings Institution, San Francisco Fed President, Mary Daly, said that she believes more hikes will be needed by the end of the year. This belief was echoed further by Cleveland Fed President, Loretta Mester, at a separately held roundtable discussion.

How May Markets React Following The Policy Meeting?

Based on current trading sentiment, rate increases beyond July do not appear priced in. This leaves markets at heightened risk of a pullback.

The Dow ( DJIA ), for example, just closed the previous trading week with their longest win streak since 2017. Though notable, this pales in comparison to what’s occurring elsewhere. Consider the newfound optimism surrounding more speculative investments, such as Carvana ( CVNA ) and Bitcoin ( BTC-USD ), each of which are up 885% and 80%, respectively.

These gains come as retail traders are more bullish than they have been over the past two years, according to the American Association of Individual Investors. The bullishness is also accompanied with little consideration for insurance, as evidenced by the put/call ratio, which currently sits at its lowest level since early 2022. The complacency could be seen more readily in the subdued trading range of the Cboe Volatility Index (“the fear gauge”).

A potential driver of the bullish spirit is the conviction that the economy is in fact on its way to a soft landing . Former CEO of Goldman Sachs ( GS ), Lloyd Blankfein, previously stated his case in support of this viewpoint.

But in my view, those supporting a soft landing at this junction are perhaps under the notion that the rate cycle is likely to conclude following this month’s policy meeting. There would be too many unknowns to make the call otherwise. Suppose the Fed does in fact continue increasing rates. How could one be so sure of a soft landing this far out in advance?

My Prediction

A 25bps point increase this week is probable. A final 25bps increase in the fall is likely. Stocks are viewed as vulnerable, given current gains and elevated bullishness. Low readings in the fear gauge ahead of the meeting present investors with an attractive opportunity to opportunistically insure their portfolios with options. A 10%-15% pullback in the months ahead would be viewed as healthy for a more sustainable rally at the end of the year, when the Fed will likely be more inclined for a policy reversal as opposed to a policy continuation.

For further details see:

July Fed Meeting Preview: Are Stocks Overvalued Ahead Of A Likely Rate Hike?