CA - July's 5 Dividend Growth Stocks With 5.82%+ Yields

2023-07-20 21:27:34 ET

Summary

- Investing in dividend growth stocks can provide steady cash flows to investors, no matter what the market decides it's going to do for the day.

- This month, we have a few familiar names that popped up once again; however, we also have a new name to make the list this month as well.

- The names that we will be looking at for a quick update are IIPR, RMR, BNS, BCE and JHG.

Written by Nick Ackerman.

Dividend growth stocks aren't always the most exciting investments out there. They often aren't grabbing the headlines, and they aren't the stocks running up hundreds of percentages in a year. In fact, they are often some of the least exciting stocks. And that is precisely their strongest selling point. With such a vast world of dividend growth stocks available out there, it is important to screen through to see if there are any worthwhile investments to explore.

They are stocks that provide growing wealth over time to income investors. Dividend growers are often larger (not always), more financially stable companies that can pay out reliable cash flows to investors. Some are slower growers than others. Some are going to be cyclical that require a strong economy. Some are going to be secular, which doesn't generally rely on a more robust economy.

Dividend growth can promote share price appreciation. Of course, that is if these companies are growing their earnings to support such dividend growth in the first place. Trust me. There are yield traps out there - I've owned a few that I'm not particularly proud of.

I like to think of investing in dividend stocks as a perpetual loan of sorts. Essentially, every dividend is a repayment of your original capital. Eventually, holding long enough, you have the position "paid off." It is all returned back into your pocket from that point forward.

The jobs data from ADP showed that the private sector added more than double the expectations. That led to a sharp sell-off across the board in equities as it drove yields higher. The rationale is that hotter jobs almost guarantee the Fed stays aggressive and, other than just two more hikes this year, could suggest a need for more than anticipated. This economy continues to be too hot, and that is a bad thing in terms of trying to get inflation down. However, by the next day, we had the official jobs report for June which was much weaker than expected and well below what ADP had reported.

Inflation has come down significantly but still remains well above the Fed's 2% goal. At the same time, unemployment remains incredibly low.

All of this being said is important to understand my approach to dividend stocks and why screening dividend stocks can be important for income investors. These are July's five dividend growth stocks that might be worthwhile for a deeper exploration. As with any initial screening, this is just an initial dive - more due diligence would be necessary before pulling the trigger.

The Parameters For Screening

I'll be using some handy features that Seeking Alpha provides right here on their website for this screen. In particular, I will be screening utilizing their quant grades in dividend safety, dividend growth and dividend consistency.

Dividend Safety is relatively self-explanatory. These will be stocks that SA quants show reasonable safety compared to the rest of their various sectors. The grade considers many different factors, but earnings payout ratios, debt and free cash flow are among these. This category will be stocks with A+ to B- ratings.

For the dividend growth category, we have factors such as the CAGR of various periods relative to other stocks in the same sector. Additionally, the quants also look at earnings, revenue and EBITDA growth. As we will see, this doesn't mean that every stock with a higher grade has the growth we are looking for. This just factors in that the dividend has grown or earnings are growing to support dividend growth possibly. For these, the grades will also be A+ through B- grades.

Finally, for dividend consistency, we want stocks that will be paying reliable dividends for us for a very long time. In particular, hopefully, they are raising yearly, though that isn't an explicit requirement. We will also include stocks with a general uptrend in dividend payments, which means there could have been periods where they paused increases for a year or two.

After looking at those factors alone, we are left with 525 stocks at this time from the 549 listed last month. I'll link the screen here , though it is a dynamic list that constantly updates regularly. When viewing this article, there could be more or less when going to the link.

From there, I wanted to narrow down the list a lot more. I then sorted the list by forward dividend yield, from highest to lowest. Since these will be safer dividend stocks in the first place, screening for those among the higher payers shouldn't hurt.

I will share the top 25 that showed up as of 07/06/2023.

{kind=link}

As usual, we have some repeats that make the least that we regularly cover. Those names we skip over at least until the next quarter, so when we do take a fresh look, we have more worthwhile data to see what might have changed.

The 5 names this month that we'll take a quick look at are Innovative Industrial Properties ( IIPR ), The RMR Group ( RMR ), The Bank of Nova Scotia ( BNS ), BCE Inc ( BCE ) and Janus Henderson Group ( JHG ). IIPR, RMR, BCE and JHG have come up previously. However, BNS will be a new name we take a look at this month that hasn't come up since I started this screening article.

We recently covered OneMain Holdings ( OMF ), Hess Midstream ( HESM ), Medifast ( MED ) and Alpine Income Property Trust ( PINE ), meaning we will skip over those names until they potentially come up next time.

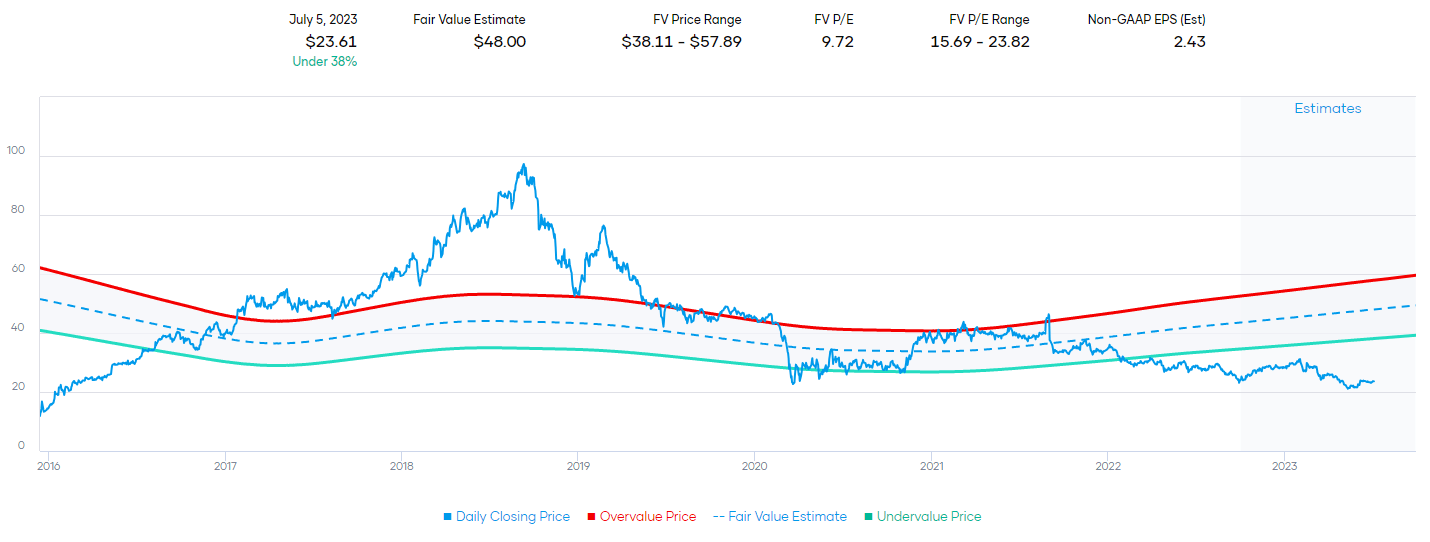

Innovative Industrial Properties 9.77% Yield

IIPR is a name I personally hold, and while at one time it was my best holding, things have certainly turned south. Fortunately, I bought it before it ascended into the clouds, buying most of my position in 2019 and 2020. I've added some through reinvesting the dividend. It has broken below my cost basis of around $92, but including those dividends the losses are reduced. It's also not a very large position for me. I'll take the small losses as a blessing compared to any investor that bought in 2021/early 2022.

Ycharts

This remains a small position even as it's dropped precipitously for me and even while it looks like steal simply because the headwinds they face are quite real. This is a speculative position that owns industrials that are leased out to regulated cannabis facilities. At one point, FFO growth and dividend growth was extraordinary, but that was when money was easy, and investors were willing to bid up everything and anything.

These days, the cannabis industry has been struggling. Several of their tenants have been defaulting, and the dividend growth due to uncertainty going forward has come to a halt. However, they are still showing strong rent collections from their tenants despite this - at least so far.

IIPR Historical Rent Collection (Innovative Industrial Properties)

{kind=link}

FFO for this year is expected to show some growth, coming in at $8.09. Next year analysts expect FFO to nudge up slightly to $8.22. So the fast pace days of growth certainly appear to be behind them.

{kind=link}

Of course, the positive here could be that if they can hit these estimates, then the payout ratio of 90% still means they are covering their dividend. At a nearly 10% yield, even if they are able to freeze the dividend where it was and continue paying it, I would be quite happy. However, even at that yield, it reflects the very real risks in this REIT.

Due to significant headwinds from a weaker economy and weak tenants, IIPR remains speculative but worth exploring for higher-risk investors. I'll continue to reinvest at this point and see where this name takes me.

The RMR Group 6.78% Yield

This is a name we've touched on before, but only once previously, and it had not been a name I was familiar with. It's in the real estate sector, and the industry is identified as diversified real estate activities. They describe themselves as:

...leading U.S. alternative asset management company, unique for its focus on commercial real estate ("CRE") and related businesses. RMR's vertical integration is strengthened by approximately 600 real estate professionals in more than 30 office nationwide who manage over $37 billion in assets under management and leverage more than 35 years of institutional experience in buying, selling, financing and operating CRE.

The "C" word in this current market is certainly a dirty word, and it could explain why the share price has been weaker to prop up the dividend yield in the first place. Shares are down nearly 17% on a YTD basis. That said, it gets a "Buy" rating from SA Authors and Wall Street Analysts. Additionally, the quant shows a "Strong Buy" rating, suggesting at least in the short term, there could be some opportunity.

RMR Rating Summary (Seeking Alpha)

However, there is only slim coverage from SA Authors. Additionally, something worth noting is that when I did touch on RMR in last April's article, it was commented that RMR needs more research due to "not the greatest reputation." In another comment, a reader mentioned, "many [of] us would never invest in RMR vehicles, the REIT space people rightly abhor it for self-dealing against its advisees." So that is certainly something to consider A conflict of interest between management teams and other stakeholders isn't something that's new to investing, so it's always something to watch out for.

Perhaps it could still be worth considering for the right price for a flip. Based on its historical valuations, it's trading well below its fair value range. Then again, the trend of a lower share price has been quite steady for a few years now.

{kind=link}

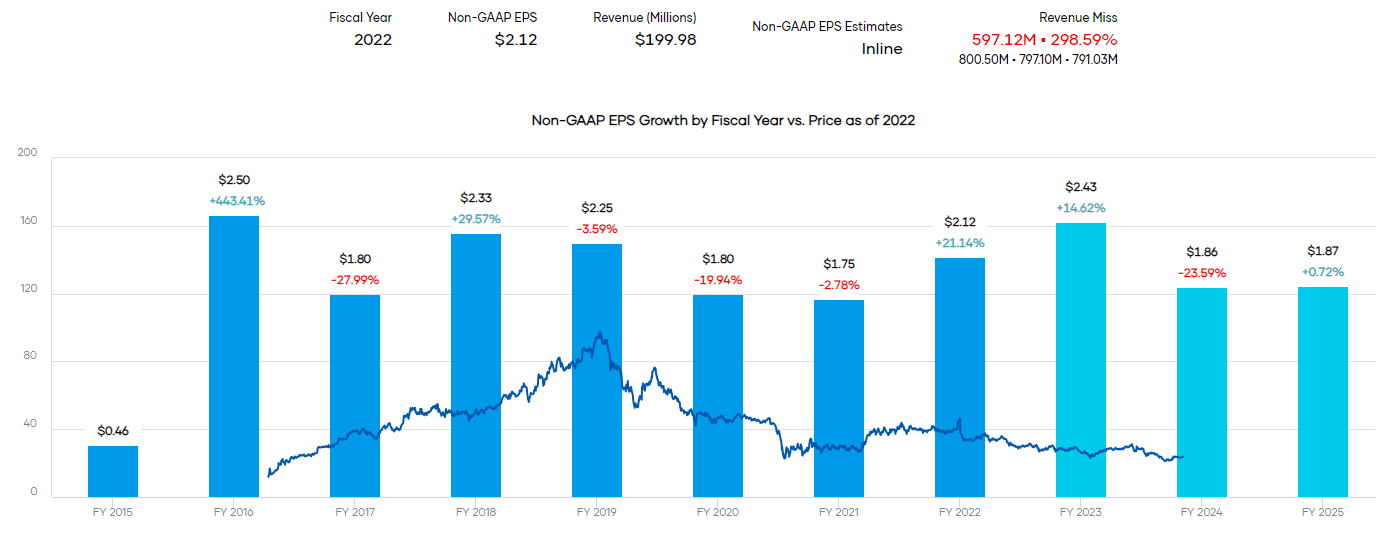

Despite the attractive valuation that is pushing it up to have an attractive dividend yield, the earnings seem to be fairly erratic. That can make it more difficult to know if they'll be covering their dividend due to that variability. Fortunately, they boast about having no debt. This can be a positive as rising interest rates won't suddenly put them in a situation where they have maturities coming due that they'll have to refinance at higher rates.

{kind=link}

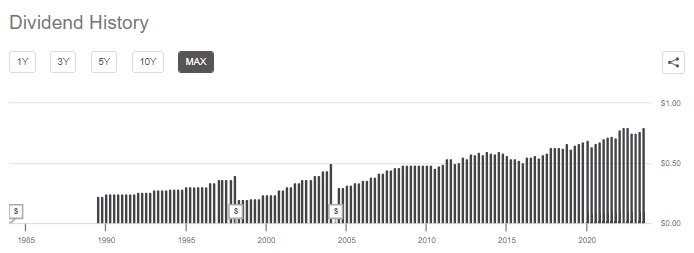

They also have a somewhat short dividend history. They've been able to raise their regular dividend, though at a bit slower pace. That isn't that unusual either due to Covid adding uncertainty through most of this period. They also paid out a large special in 2021 of $7 that isn't shown in the chart below.

{kind=link}

The Bank of Nova Scotia 6.31% Yield

BNS is a new name I've not encountered since starting this monthly screening piece. Shares are down quite significantly over the last year but are flat on a YTD basis. They "provide a broad range of banking services including personal and commercial banking, wealth management and private banking, and capital markets." So they are quite diverse with a bit of business in different categories, which makes sense as they are one of Canada's "Big Five" banks.

Perhaps it would be interesting to note that the Canadian Imperial Bank of Commerce ( CM ) also made an appearance earlier this year for our screening article. That was the first time I had looked at CM, which is another "Big Five" bank.

Similar to when we usually cover Canadian stocks, their dividend history can initially appear a bit unusual depending on where you look. When looking at Seeking Alpha, it would appear to be a variable dividend that changes every quarter.

{kind=link}

However, that isn't the case. Instead, what we are seeing is the CAD to USD conversion change every quarter. This results in what would make it appear as though they change it every quarter. A trend of a rising dividend has been in place since the global financial crisis. However, they froze their dividend at CAD 0.90 for 2020 and 2021. That was similar to U.S banks as well as the Covid pandemic was going on.

Analysts expect earnings to dip significantly this year before rebounding in the following two years. Either way, dividend coverage appears to be quite strong with this Canadian bank.

{kind=link}

BCE Inc 6.16% Yield

This month we have two Canadian names, and BCE is a name we've come across before. This appears to be a natural fit as it's a telecom company from the northern country. Similar to most other telecom industries worldwide, they tend to provide high yields.

That being said, AT&T ( T ) nor Verizon ( VZ ) have actually never made it for coverage on this screening article. Of the 525 names that screened this month, they aren't even listed because their dividend safety grades are too low. T shows a dividend safety of C, and VZ is only a touch better at C+. Of course, low grades don't guarantee a cut. Just the opposite is also true; a high safety grade doesn't guarantee a cut won't happen. We recently took a closer look at VZ and T due to the latest potential lead sheathing cable liabilities.

BCE gets a high-grade thanks to strong cash from operations, return on common equity and net income margins, which are the highest grades for this name that help indicate a low chance of a dividend cut. Just like BNS and the other Canadian names that we run across, they pay their dividends in CAD. Therefore, when looking at a dividend chart, we'll see it be 'variable' for those collecting in USD as the conversion changes quarterly.

At the same time, we see a strong history of a dividend trending higher over time. They've been raising the dividend since 2004.

{kind=link}

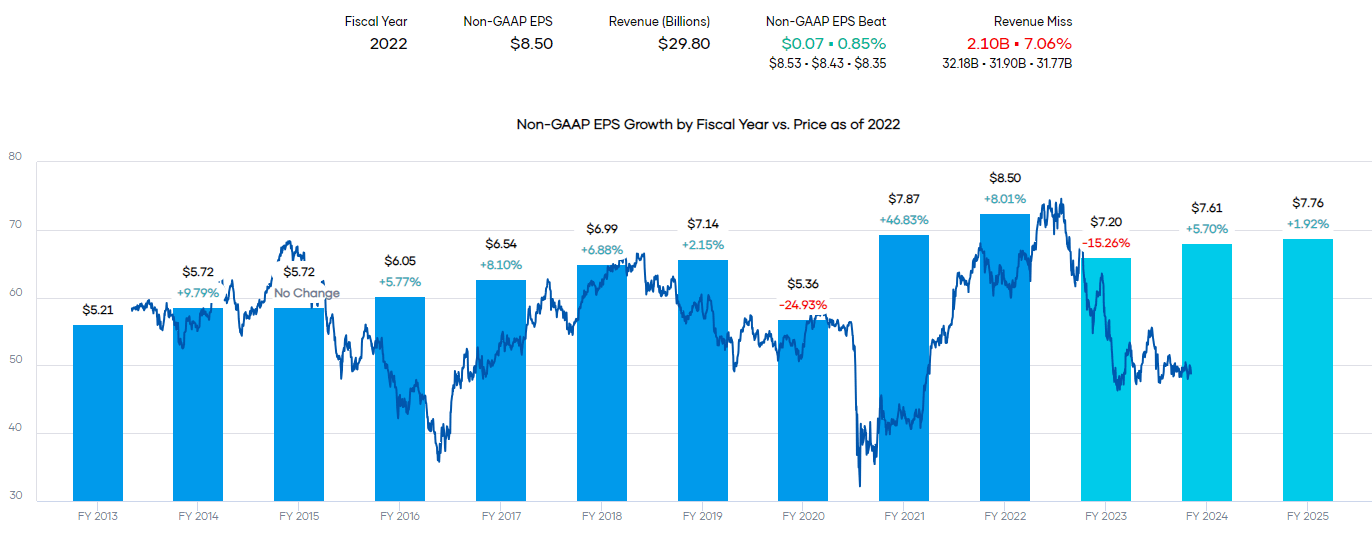

Unfortunately, dividend coverage for BCE has been weakening. The trend of growing their dividend could be halted, and they might be in a position where they could have to cut their payout. Analysts are expected earnings to decline this year before growing single digits, but even with that, coverage just isn't there.

{kind=link}

In terms of earnings coverage, it's actually looking much weaker than T and VZ. All three of these telecoms had weak Q1 FCF, but that also has to do with seasonality. So all would be relying on significant increases in FCF through the remainder of the year to cover their dividends. VZ was the closest in terms of FCF coverage.

So despite telecoms being able to provide significant cash flows, the CAPEX demands and slow growth amid intense competition continue to make this an industry that's tough to navigate. Therefore, as I already own VZ and trade T with a current long position, I wouldn't look to add more to this area. Not to mention that BCE is quite expensive compared to T and VZ, which despite their flaws, actually provide dirt-cheap valuations. BCE has simply held up better in terms of its share price relative to its U.S. peers.

Janus Henderson Group 5.82% Yield

JHG is a name we've touched on before, the latest time being in March 2023. Prior to that, it was December 2022. That said, these so far were the only times. This has primarily been the case because the stock price had slid so far after peaking in 2021. That has now driven up the yield of JHG to surface near the top of this screening article, which as a reminder, is sorted by highest to lowest dividend yield.

Ycharts

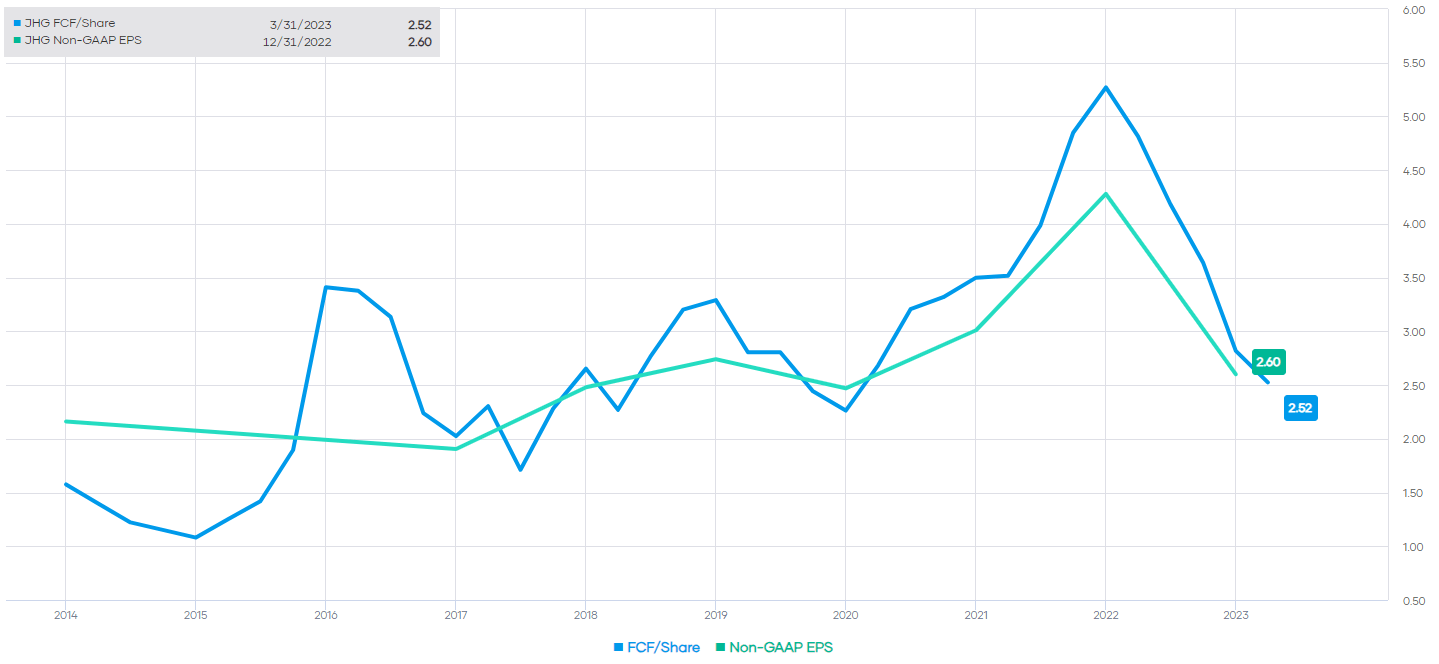

This is a fairly similar trajectory to other asset managers that benefited from the significant rise in the market during this period before collapsing back down to Earth last year. The spike in the share price followed the EPS and FCF of the company, both on the way up and on the way back down.

{kind=link}

Despite being located in the U.K. and unlike our Canadian friends discussed above, JHG has chosen to pay in USD leaving the conversion to their home investors.

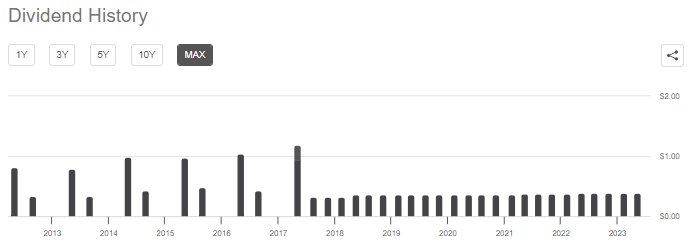

Given the change from semi-annual to quarterly dividends, the chart below can be a bit hard to tell that it has been trending higher over the last several years. That said, they did freeze the payout at $0.36 per share from Q2 of 2018 until it was increased in Q2 of 2021.

{kind=link}

Their dividend history is actually longer , but this was a newly formed company when Janus Capital Group and Henderson Group merged in 2017 .

Earnings are expected to decline to $2.20 this year. That means they could still be earning their dividend, but it won't be comfortable, and it could very likely be that investors will be frozen at this $0.39 quarterly amount. The last quarter marked the fifth quarter of that amount, which is further evidence they are content with where they are currently on the payout until potential earnings improvement.

For further details see:

July's 5 Dividend Growth Stocks With 5.82%+ Yields