AMZN - Just Eat Takeaway: Why Grubhub Is Massively Misunderstood

Summary

- Grubhub is in a much better position than the market thinks.

- Amazon acquisition can be a significant accelerator in value realization and de-intensifying competition in Europe, Canada, and Australia.

- A narrative shift may unfold in the coming years.

Just Eat Takeaway.com N.V. ( JTKWY ) continues to be a very interesting case in the stock market. In this article, I made an attempt to understand and show qualitatively why Grubhub is in a much better competitive position than the market thinks.

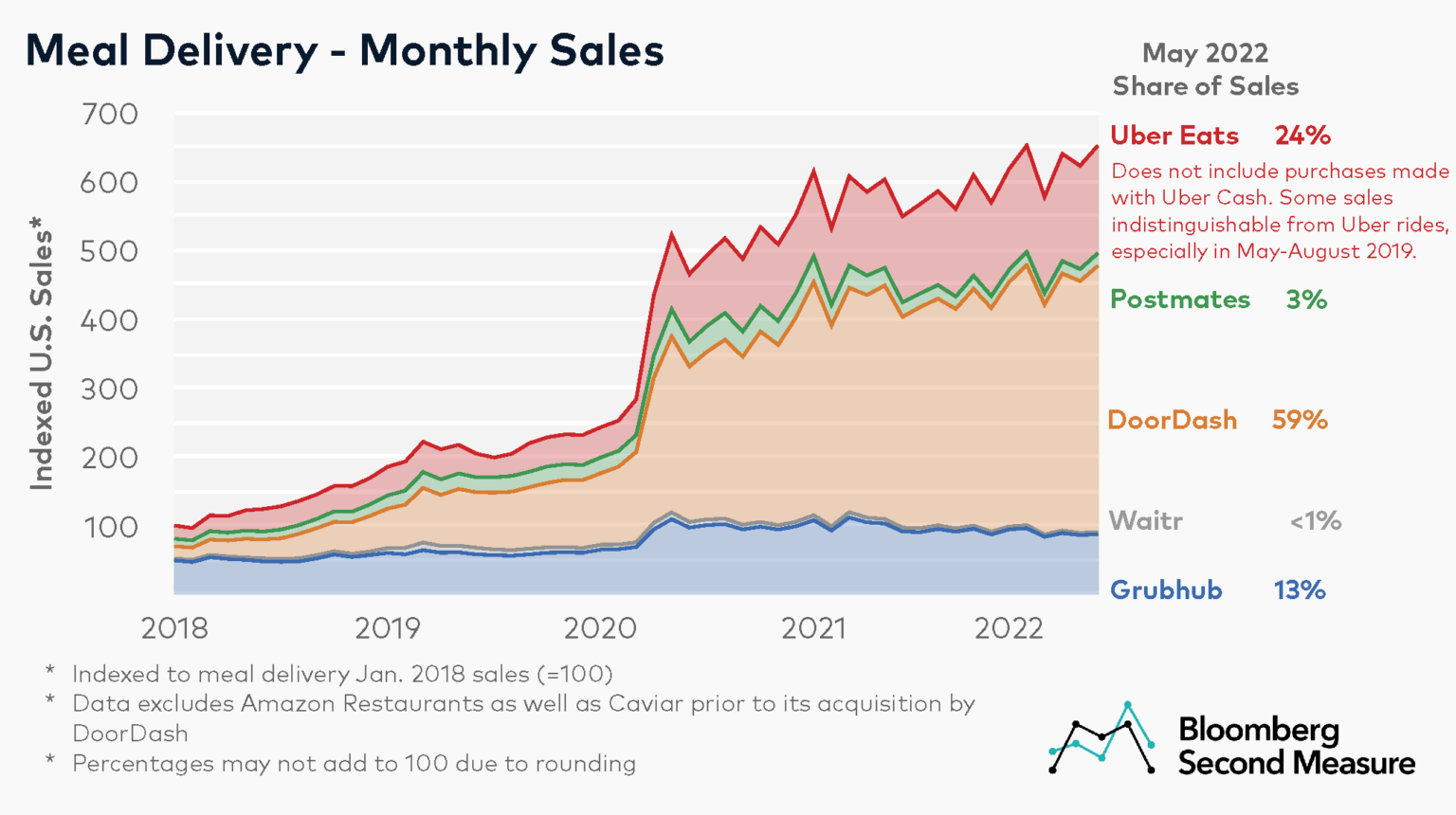

Investors are focusing too much on Grubhub's huge market share loss in the U.S. and neglecting the underlying value of Just Eat Takeaway.com. In food delivery, profitability comes from having a significantly lower marketing cost per order than competitors. This is accomplished by scale. This scale is very localized in food delivery; orders in San Francisco add very little network effects to orders in New York. The battle between food delivery companies is akin to cable companies of the previous century. By looking at the U.S. as a whole, investors believe Grubhub's small market share provides no competitive advantage to Grubhub, and so value the company at 0 in a SOTP (sum of the parts) analysis. They are wrong.

{kind=link}

Grubhub continues to book strong market share numbers in the North Eastern cities like New York. Cities with a very strong B2B presence. It is very important to understand that B2B is oftentimes not taken into account for market share numbers (corporate food orders, this is probably 10% of all orders, are a huge focus in metro areas), yet this B2B business drives huge order numbers in New York and Boston metro areas.

DoorDash, Inc.'s ( DASH ) market share gain comes mainly from the suburbs. While this is a fantastic feat, I think Grubhub's position is massively misunderstood. Grubhub continues to book market shares in New York of 34%, with a huge focus on the metro areas (Manhattan is >50% market share), not the suburbs of NYC, which are often also used in market share data.

Just Eat Takeaway Capital Markets Day

In 2018, Grubhub's gross food sales made up a total of $5.1 billion. In that year, the EBITDA was $171 million, and Adjusted EBITDA was $233 million. In 2020 Gross food sales were $8.7 billion. In 2021, GTV growth was 19% YoY. In 2022, Grubhub can easily generate a GTV in excess of $10 billion. Since 2018 the size of logistics grew massively.

Something misunderstood is that both logistics and marketplace orders have the same EBITDA contribution. Without marketing spend, the EBITDA margin per order is bigger than 90%. All the decline in EBITDA is due to competition irrationally spending marketing money, and Grubhub having to increase marketing spend, too. At the end of 2021, Grubhub had over 300 million restaurants on the platforms, the majority non-QSR. Grubhub+ subscriptions had a 25% order share, with growth not slowing down. The traction Grubhub showed until that point in growing subscribers and restaurants is magnificent - especially considering there is little discussion to be had about the fact that the market puts little value to Grubhub in the Just Eat Takeaway.com N.V. stock price.

Just Eat Takeaway Capital Markets Day (Just Eat Takeaway Capital markets day)

Now, DoorDash is firing employees, Wolt is losing money with EBITDA margins growing larger in negative terms, and the stock price has declined massively. Uber Technologies, Inc. ( UBER ) has a huge debt load and operates in many competitive food delivery markets. Both competitors have to rationalize. This will put Grubhub in a position to return marketing spending to a rational level and start increasing profitability.

Compiled with DoorDash IR Data

{kind=link}

Every day news comes out that makes it more certain fee caps are set to be removed in NYC. Legislation has been proposed in the NYC council to remove the NYC fee cap, and rumors are that a significant number of council members are supportive. I think Grubhub can generate in excess of $500 million in hard EBITDA sustainably at this size after NYC fee cap removal. The company's gross food sales more than doubled since 2018, considering the 90+% EBITDA margin ex marketing costs that seem easily accomplishable. At a 10 times EBITDA multiple, Grubhub is worth more than Just Eat Takeaway.

Amazon.com ( AMZN ) has partnered with Grubhub and has a stake in the company. Will Amazon partner with Grubhub if it has a poor offering? I believe Amazon is set to acquire Grubhub, probably as the biggest acquisition by the company since Whole Foods, and this can be a significant accelerator to value realization at Grubhub for JET shareholders. I think the partnership's goal is mainly to understand the impact of the synergy between Grubhub and Amazon on Amazon Prime retention data. If this is good - and I believe it will be - Amazon could be willing to acquire Grubhub at a serious price. Amazon also acquires huge last-mile optionality and strong underlying EBITDA.

People are consistently underplaying the seriousness of this partnership. Amazon doesn't just partner with a company and adds its subscription to Amazon Prime if it doesn't have a longer-term plan!

I often see people looking at market share, and last month's Grubhub has been losing market share again. Just Eat Takeaway.com N.V. is scaling down Grubhub in unprofitable markets and investing for growth in strongholds. While Grubhub may decline in size this year, the share of "moated" orders increases of total orders.

Takeaway

What will Uber shareholders think of Uber's voucher-driven operations in Europe with low market shares and illegal employment models when Amazon enters food delivery in the U.S., while Just Eat Takeaway.com N.V. acquires a huge cash pile? Where will Uber and DoorDash shareholders want the focus of the company to be? This scenario will not only provide the company with capital close to its market cap; it will put pressure on American counterparts to reconsider their loss-making illegally operated European operations.

In the coming years, I think Just Eat Takeaway.com N.V. will undergo a total narrative shift-set that will reward shareholders.

For further details see:

Just Eat Takeaway: Why Grubhub Is Massively Misunderstood