RTX - Kaman Corporation: A High-Risk/High-Reward Turnaround Play

2023-05-25 03:14:24 ET

Summary

- Net sales remained stagnant for a few years.

- Profit margins are improving as the management is cutting expenses, improving operating efficiencies, and has acquired a manufacturer of high-value-added products.

- The company needs to deleverage the balance sheet urgently.

- The dividend is at risk as interest expenses skyrocketed in the past quarter.

- This is a high-risk/high-reward turnaround play worth the risks.

Investment thesis

Operations of Kaman Corporation ( KAMN ) have been subject to periods of high volatility over the years due to its high cyclical component, so it is important to take advantage of the economic cycles in order to buy low and sell high or, failing that, buy low and enjoy a high dividend yield on cost. After a few years of restructuring its operations through the sale of its Distribution business segment and the acquisition of two companies that manufacture highly engineered products, the company finds itself with a debt pile that needs to be addressed and stagnant sales at a time when inflationary pressures are impacting profit margins on the brink of a potential recession as a result of recent interest rate hikes. These factors, and the recent surge in interest expenses, caused a sharp decline in the share price due to the high risks that the company is facing in the short and medium term.

The first quarter of 2023 has shed some light at the end of the tunnel thanks to a strong recovery in profit margins boosted by increased volumes, aggressive cost-cutting efforts, and operations from the acquired Aircraft Wheel & Brake, but given the surge in long-term debt to fund the latest acquisitions, investors seem dissatisfied as growth has been very gradual while interest expenses are putting serious pressure to the dividend. Still, I strongly believe this represents a good opportunity to acquire shares at very reasonable prices as the P/S ratio is significantly below the average of the past 3 years and the company's improving margins should allow for relatively strong cash from operations that will be useful to slowly pay down its debt pile.

A brief overview of the company

Kaman Corporation is a manufacturer of highly engineered products for the aerospace, defense, industrial, and medical industries, and has operations in the United States, as well as manufacturing facilities located in Germany and the Czech Republic. The Company also has an investment in a joint venture located in India and enjoys strong barriers for competitors to enter the industries in which it operates. The company was founded in 1945 and its market cap currently stands at $644 million, employing over 3,000 workers. The company's main customers are the U.S. military, foreign allied militaries, Sikorsky Aircraft Corporation, The Boeing Company ( BA ), Airbus ( OTCPK:EADSF ), Lockheed Martin ( LMT ), Rolls-Royce ( OTCPK:RYCEY ), Raytheon ( RTX ) and Bell Helicopter.

Kaman Corporation logo (Kaman.com)

The company operates under three reportable segments: Engineered Products, Precision Products, and Structures. Under the Engineered Products segment, the company manufactures aircraft bearings and components, miniature ball bearings, proprietary spring energized seals, springs and contacts, wheels, brakes, and related hydraulic components for helicopters and fixed-wing and UAV aircraft. Under the Precision Products segment, the company provides precision safe and arming solutions for missile and bomb systems for the U.S. and allied militaries, subcontract helicopter work, restoration, modification, and support of the company's SH-2G Super Seasprite maritime helicopters, support of its heavy lift K-MAX manned helicopter, and development of the KARGO UAV unmanned aerial system, a purpose-built autonomous medium lift logistics vehicle. And under the Structures segment, the company provides complex metallic and composite aerostructures for commercial, military, and general aviation fixed and rotary wing aircraft, as well as medical imaging solutions.

Currently, shares trade at $22.98, which represents a 69.39% decline from all-time highs of $75.08 reached in May 2018. This decline is the result of a recent margin contraction after some years of net sales stagnation, as well as increased debt, interest expenses, and recessionary concerns. Nevertheless, the company performed two major acquisitions since 2020 after the major divestiture of the Distribution segment and both gross profit and EBITDA margins, as well as net sales, have shown strong signs of recovery during the past quarter.

Recent acquisitions and divestitures

In August 2019, the company completed the divestiture of its Distribution segment for around $700 million, excluding certain working capital adjustments, in order to focus on aerospace and engineered products with more added value.

After the divestiture, in June 2020, the company acquired Bal Seal Engineering, a global leading designer, developer, and manufacturer of highly engineered products including precision springs, seals, and contacts, for $317.5 million. And in September 2022, the company acquired the Aircraft Wheel & Brake division from Parker-Hannifin Corporation ( PH ), which provides mission-critical wheel and brake technology products and solutions, for $441.3 million.

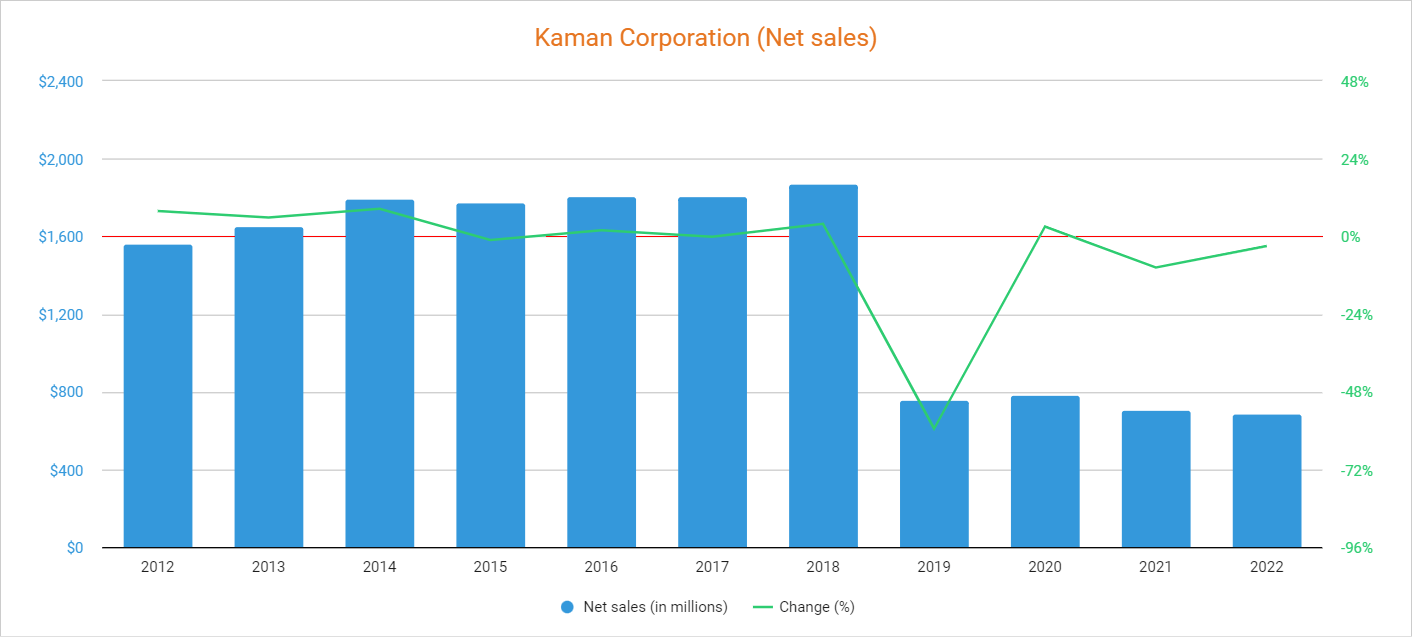

Net sales are gradually recovering

After a major decline in net sales of around 60% as a consequence of the divestiture of the company's distribution business segment in 2019, sales kept declining, which is certainly causing strong pessimism among investors. In this regard, net sales only increased by 3% in 2020, but declined by 9.62% in 2021, and by a further 2.97% in 2022.

{kind=link}

More specifically, net sales declined by 7.91% year over year during the first quarter of 2022, by 11.86% in the second quarter, and by 4.36% in the third quarter, but increased by 12.56% year over year during the fourth quarter and by 23.09% during the first quarter of 2023 (but declined by 1.32% quarter over quarter) to $194.5 million as net sales in the Engineered Products segment increased by 51.4% year over year boosted by the acquisition of Aircraft Wheel and Brake (without the acquisition, the segment's sales would have increased by 28.6%). Still, considering the two major acquisitions carried out in 2020 and 2022, it is certainly a very mild increase and I strongly believe investors expected more out of the company's M&A strategy as it significantly leveraged the balance sheet in order to perform these acquisitions. Nevertheless, net sales are expected to increase by 8.42% in 2023, and by a further 2.88% in 2024 as the current backlog of the Engineered Products segment is at record levels.

The sharp decline in the share price experienced in the past few years has caused a steep decline in the P/S ratio to 0.890, which means the company generates net sales of $1.12 for each dollar held in shares by investors, annually.

This ratio is 39.37% lower than the average of the past three years and represents a 57.78% decline from the 3-year peak of 2.108 reached in 2021. This shows a high degree of pessimism among investors as they are placing much less value on the company's sales not only because of low growth expectations, but also as a consequence of higher debt levels, skyrocketing interest expenses, recessionary concerns, and lower profit margins as a consequence of inflationary pressures.

Nevertheless, the company's profitability has significantly improved in the past quarter boosted by efficiency and cost-cutting programs, increasing volumes, and recent acquisitions.

Margins are starting to improve after a significant contraction

The company has enjoyed positive profit margins over the years that have enabled it to generate reliable cash flows. In this regard, gross profit margins danced around 30% over the years while EBITDA margins danced at around 8%. Still, inflationary pressures, impairment and restructuring charges, inventory and contract cost write-offs related to the K-MAX, and one-time costs from the Aircraft Wheel & Brake acquisition negatively impacted profit margins as the trailing twelve months' gross profit margin currently stands at 27.04% and the EBITDA margin at 0.10%.

Nevertheless, both gross profit and EBITDA margins dramatically improved during the first quarter of 2023 to 24.72% and 11.69%, respectively, as the company announced cost structure optimization measures in January 2023 aimed at improving profit margins in the long term by achieving annualized run-rate costs savings of around $25 million per year by 2024. These measures include headcount reduction, increased efficiencies, improved working capital management, streamlining facilities and processes, removal of non-value added activities, discontinuing K-MAX production, and right-sizing the overall cost structure.

In this sense, it will be very important that EBITDA margins remain in positive territory in order to cover current interest expenses and gradually pay down the debt contracted used for recent acquisitions, and cost reduction efforts should help in achieving it.

A debt pile that needs to be addressed

After some deleverage during the 2016-2022 period, the company borrowed around $400 million to perform the acquisition of Aircraft Wheel and Brake, and long-term debt currently stands at $609.33 million as a consequence.

On the other hand, cash and equivalents are currently very low at $53.99 million, with which the room for maneuver is relatively small. Luckily, the company currently holds $186.50 million in inventories, which could be converted into cash in order to generate positive cash from operations in the medium term and thus pay down some debt.

The problem is that interest expenses are skyrocketing as a consequence of higher debt levels and interest rates, and trailing twelve months' total interest expense currently stands at $24 million.

Furthermore, total interest expense during the first quarter of 2023 was $9.60 million, which means annual interest expenses should soon approach $40 million, which will put the dividend under serious pressure. In this regard, it will be the reduction of long-term debt that will allow this to be a successful turnaround story. Still, it is very important for investors to understand that the current dividend, despite offering a high dividend yield on cost, is at risk of being cut or canceled in the short to medium term until interest expenses are significantly reduced.

The dividend is at risk as interest expenses skyrocketed

Kaman investors enjoyed a growing dividend over the years, but the quarterly dividend has remained frozen at $0.20 per share since 2017. In addition, an increase in the foreseeable future should not be expected as margins have recently been contracted while interest expenses are very high.

Even so, the recent fall in the share price has opened up the opportunity to obtain a high dividend yield on cost compared to the past at the expense of expectations of a frozen dividend or, in the worst case, a temporarily cut (or paused) dividend as interest expenses are higher than usual and profit margins are subject to high volatility as a result of inflationary pressures. Furthermore, cash from operations could take a significant hit if a recession finally materializes as a result of the recent interest rate hikes.

In order to calculate the sustainability of the dividend over the years, in the following table I have calculated the cash payout ratio in recent years by calculating what percentage of cash from operations the company has used each year to cover dividends paid and interest expenses. In this way, we can assess the company's ability to cover both expenses through actual operations. After this, I will take a look at the current state of the dividend.

| Year |

| 2014 |

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Cash from operations (in millions) |

| $106.19 |

| $109.58 |

| $107.71 |

| $79.89 |

| $162.37 |

| -$7.80 |

| $16.47 |

| $48.70 |

| $20.97 |

| Dividends paid (in millions) |

| $17.29 |

| $19.03 |

| $19.51 |

| $21.46 |

| $22.35 |

| $22.34 |

| $22.21 |

| $22.24 |

| $22.36 |

| Interest expense (in millions) |

| $13.38 |

| $13.14 |

| $15.75 |

| $20.58 |

| $20.05 |

| $17.20 |

| $19.27 |

| $16.29 |

| 16.87 |

| Cash payout ratio |

| 28.88% |

| 29.36% |

| 32.73% |

| 52.63% |

| 26.11% |

| - |

| 251.87% |

| 79.12% |

| 187.12% |

As one can see in the table above, the company has historically made a fairly conservative use of cash as the cash payout ratio remained relatively low over the years, but the cash payout ratio reached a whopping 251.87% in 2020 due to coronavirus-related headwinds, and although cash from operations improved in 2021 as the world's economy reopened, the company again reported a cash payout ratio of 187.12% in 2022 due to inflationary pressures. In this regard, cash from operations for the full 2022 was $21.0 and inventories declined by $16.6 million compared to 2021, and although accounts receivable increased by $14.9 million, accounts payable also increased by $6.2 million. In this regard, the company's operations were unsustainable in 2022, and this was the reason for the management to adopt a strategy to reduce costs and improve the efficiency of operations.

As for the first quarter of 2023, the company reported cash from operations of -$5.5 million, but inventories increased by $10 million and accounts receivable by $13.7 million while accounts payable declined by $1.1 million, which reflects the recent improvement in the company's profit margins. In this regard, the company's operations are improving significantly and the ongoing cost-cutting efforts have yet to be noticed, so although the dividend is currently at risk, the company should be able to slowly pay down its high level of debt and, with it, reduce interest expenses to give more space to a more sustainable dividend.

Risks worth mentioning

As you might expect, a ~70% drop in the share price is accompanied by significant risks, and next, I would like to highlight those that I consider most important.

- Profit margins could fall again if inflationary pressures continue to be part of the current macroeconomic landscape, which would have a direct impact on cash from operations.

- Volumes could decline if a recession finally materializes as a consequence of recent interest rate hikes to alleviate high inflation rates. In this regard, declining volumes would have a direct impact not only on net sales but also on profit margins as a consequence of unabsorbed labor.

- The dividend is at risk as interest expenses have increased significantly in recent quarters, and management could decide to cut it or temporarily cancel it in order to cover interest expenses more comfortably and be able to gradually pay off the debt.

- If the company does not generate enough cash from operations, it could be forced to continue borrowing cash to cover interest expenses, which would entail very high risks for the sustainability of operations as interest expenses could keep increasing as a consequence of higher debt.

- Orders by The Boeing Company accounted for over 10% of total net sales in 2022, so a significant reduction in orders coming from the company could have a significant impact on the overall net sales of Kaman.

Conclusion

The situation in Kaman is very difficult, and this is reflected in the recent fall in the share price. Profit margins have recently been hit by inflationary pressures and sales have increased only slightly despite the recent increase in debt due to acquisitions. Also, interest expenses have increased significantly in the last quarter, which is putting the current dividend at risk. Furthermore, there are growing concerns about a potential recession due to recent interest rate hikes.

But despite all these headwinds, things started to improve during the first quarter of 2023 thanks to profitability improvements driven by increased volumes and recent acquisitions, and margins are expected to continue improving slightly thanks to ongoing cost-cutting efforts, and for this reason, I believe that the management is going through the right direction to turn around the ship and gradually pay off the company's high levels of debt, which will gradually improve long-term prospects, allowing high capital gains for shareholders or a high dividend yield on cost in the long run. Still, it is important to understand that this is a high-risk, high-reward turnaround play.

For further details see:

Kaman Corporation: A High-Risk/High-Reward Turnaround Play