KAMN - Kaman's Q2 Earnings: Navigating Turbulence

2023-08-09 13:00:00 ET

Summary

- Kaman Corporation's Q2 earnings exceeded estimates, with non-GAAP EPS of $0.22 and revenue of $195.2 million.

- The company saw growth in sales, operating income, and adjusted EBITDA due to acquisitions and cost-saving efforts.

- However, Kaman has underperformed in the market, struggled with dividend consistency, and faces challenges with interest expenses and overvaluation.

Thesis

In the second quarter, Kaman Corporation's ( KAMN ) non-GAAP EPS of $0.22 beat projections by $0.14, while revenue reached $195.2 million, exceeding estimates by $10.07 million. However, despite positive indicators, this analysis reveals challenges in KAMN share price, dividend consistency, and market underperformance that warrants a cautious "hold" rating.

Company Overview

Kaman Corporation, headquartered in Bloomfield, Connecticut, operates in aerospace, defense, medical, and industrial markets, segmented into three primary divisions: Engineered Products, Precision Products, and Structures. The Engineered Products segment focuses on various aircraft components; Precision Products deals with missile systems, helicopters, and UAV systems; and the Structures division covers both aviation structures and medical imaging solutions. With a history dating back to 1945, the company's reach extends across North America, Europe, Asia, the Middle East, and Oceania.

Kaman Corporation's Q2 Earnings Highlights

In the second quarter , Kaman Corporation has drawn attention to its financial performance with some promising metrics and structural strategies.

One of the key strategies implemented by Kaman is the consolidation of its Joint Programmable Fuze ((JPF)) operations into a singular facility. According to management , they've laid the groundwork for a higher degree of operational readiness and ushered in significant program cost reductions as volumes decrease. With a clear plan in place for the facility's closure, the company has already commenced realizing the savings from these measures. The delivery on the remaining JPF backlog continues, generating around $7 million in EBITDA in the first half of this year. This specific figure, however, is not anticipated to recur in the latter half.

Sales during the quarter provide another aspect of the narrative, reaching $195.2 million - a 21.4% surge compared to the same quarter last year. A deeper examination reveals two key sources of this growth: an 8.2% organic increase, mainly within the Engineered Products segment, and a $21.2 million infusion stemming from the acquisition of Aircraft Wheel & Brake. Given the projected growth of the Aircraft Wheels and Brakes market to USD $7.48 billion by 2030 at a 7.3% CAGR, the significance of this acquisition becomes even more pronounced.

A dramatic uplift in operating income, from $1.9 million last year to $17.6 million in Q2, illustrates the company's strengthened position. In tandem with this, adjusted EBITDA has escalated, doubling from $16.1 million to $32 million, and the gross margin reached 37%, up by 480 basis points year-on-year.

The reasons behind these figures lie in the Aircraft Wheel & Brake acquisition, organic volume growth, and successful cost-saving efforts. Additionally, a strategic reduction in selling, general, and administrative expenses to 21.3% of sales further buoyed the financial standing. Such a shift was enabled by higher volume leverage, cost containment, and fewer corporate development costs.

Among the financial strategies, Kaman's significant debt refinancing and extension of maturity to 2028 are worth mentioning. The amendment to their credit facility safeguards sufficient capacity to use proceeds from the facility to settle convertible notes and meet future working capital needs. The company's intention to maximize the benefits of the lower coupon rate on the convertible notes pending a refinancing decision also merits note.

The free cash flow during Q2, standing at $17.4 million, underscores the firm's readiness to address future demands, and the GAAP net income increase to $5.3 million, up from $3.8 million, adds to the favorable picture.

Peering into 2023, Kaman foresees healthy performance in its end markets, with notable expansion in market share. The defense end market shows particularly strong momentum, with double-digit growth attributed to the core defense portfolio. Despite some softness in safe and armed devices related to the JPF program wind down, this has been more than offset.

In the medical segment, growth exceeding 10% in the first half has been recognized, propelled by a high volume on miniature bearings and other components used in medical implantables and devices.

{kind=link}

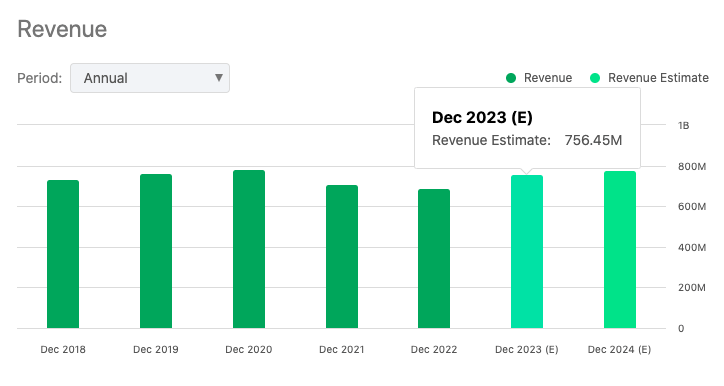

Concluding with Kaman's targets, the revenue range is pegged between $730 million to $750 million (falling short of the 756M estimate above), with expected adjusted EBITDA of $97.5 million to $107.5 million.

Performance

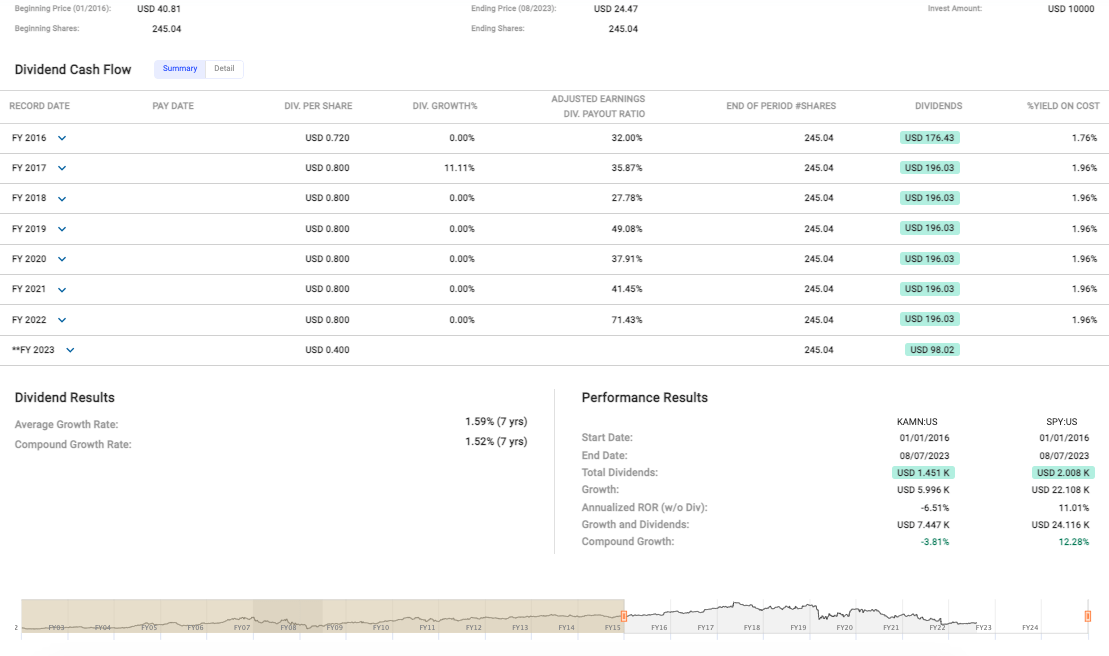

Looking at KAMN's significant drop within the medium-term (see data below), from a share price of USD $40.81 to USD $24.47 over the nearly 8-year period - a decrease of nearly 40% in share price - is a stark indication of underperformance.

{kind=link}

Also, the fluctuating dividend payout ratio over these years, reaching as high as 71.43% in 2022, tells me that Kaman's management has been struggling to balance profits with shareholder expectations with the consistency in the percentage yield on cost, hovering around 1.96% until 2023, may seem somewhat comforting on the surface, but the lack of growth in this area doesn't bode well for those seeking long-term income.

Lastly, when comparing KAMN's performance with the broader market (represented by the S&P 500 Index ) it's clear that the company has been trailing with an annualized rate of return of -6.51% without dividends, compared to the S&P's 11.01%, is a stinging indictment of Kaman's failure to capture market opportunities and grow shareholder value. The compound growth of -3.81% compared to the S&P's 12.28% only reinforces the notion that this company has been caught in a downward spiral.

Valuation

The Blended P/E ratio of 32.19x (see chart below) notably exceeds the KAMN Normal P/E Ratio of 22.83x, leading me to believe that the stock might currently be overvalued.

{kind=link}

Add to that the Adjusted (Operating) Earnings Growth Rate standing at a negative 8.46%, it's seldom a sign investors look favorably upon, as it can suggest issues with profitability, efficiency, or revenue generation. A negative growth rate, juxtaposed against a high P/E, throws up red flags and implies that the market's optimism (YTD KAMN is up 10% at the time of this analysis) might be misplaced.

Risks & Headwinds

Lower volumes in the Joint Programmable Fuze program have served to dampen some of the quarter's gains. The picture becomes more nuanced when interest expenses are considered. They escalated, as some investors might conclude - dramatically, to $10.3 million from a mere $2 million in the prior year. In my view, it's a considerable shift, largely ascribed to elevated interest rates and the incremental debt burden following the acquisition of Aircraft Wheel & Brake. This said, and to its credit, the company's strategic debt refinancing and extension of maturity to 2028 might be construed as a shield, affording Kaman the leeway and visibility to manage its deleveraging roadmap.

Also, the adjusted net income for the period declined to $6.2 million or $0.22 per diluted share, down from $8.5 million or $0.30 per diluted share in the previous year. Here again, the culprit seems to be the higher interest expenses, compounded by decreased pension income. It's a trend that persists even in the face of stronger year-to-date operating results.

The future projection adds a further dimension to this assessment. There is an apparent moderation in expectations for net earnings, ranging between $3.7 million and $11.3 million, with diluted EPS falling between $0.13 and $0.40 per share. The upward thrust from anticipated gains in the Engineered Products segment appears to be counterbalanced by the swelling interest expenses, creating a dicey equilibrium.

But maybe the most telling part of the guidance for 2023 lies in the exclusions, which might be regarded as latent sources of variation or uncertainty. These encompass "unawarded" or unsure JPF Direct Commercial Sales ((DCS)) orders and the sale of the two remaining K-MAX aircraft in inventory. Despite the roughly $800,000 of EBITDA earned from their Structures segment year-to-date, Kaman continues to assume no margin contribution from this division. They maintain optimism for success in these areas, but notably, these elements are not ingrained in the guidance for 2023.

Final Takeaway

Given the data, I rate Kaman Corporation's stock as a "hold." While the Q2 earnings highlight promising metrics, such as the consolidation of JPF operations and strong growth in sales and operating income, the long-term underperformance, higher interest expenses, and the stock's overvaluation with a negative growth rate raise concerns. Yes, the company shows potential with acquisitions and growth strategies, but the mixed signals make it difficult to commit firmly to buying, leading me to take a cautiously optimistic stance with a "hold" rating.

For further details see:

Kaman's Q2 Earnings: Navigating Turbulence