CCJ - Kazatomprom: A Top Choice For Uranium Exposure

2023-03-26 09:14:07 ET

Summary

- 2022 was a record year for Kazatomprom, with revenues up around 45% on the back of rising uranium prices, and profits doubling.

- At the same time, production costs also rose, with cash cost and AISC up, respectively, 16% and 28%, as a result of inflationary pressures and logistical challenges.

- Such challenges are going to persist through 2023 and call into question the company's ability to ramp up production in the future.

- Nonetheless, Kazatomprom remains a top choice in the uranium space, thanks to its cheap valuation, a commitment to returning capital to shareholders, leverage to uranium prices, assets in the lowest quartile of the global cost curve, high margins and a disciplined approach to production.

Overview

Kazatomprom (KAP.L) is the biggest uranium miner in the world: in 2022, it was responsible for around 22% of all uranium primary supply. Compared with other uranium producers, such as Cameco (CCJ), (CCO:CA), Kazatomprom has also the competitive advantage that all its uranium production is mined using in-situ recovery ((ISR)) methods.

The difference with conventional mining methods is easy to explain. In conventional mining, uranium ore needs to be physically removed from the ground, broken up and chemically treated to remove the uranium from the rest of the mineralized rock. With ISR, the uranium ore remains in the ground; instead, a leaching solution is pumped underground, which is able to dissolve the uranium contained within the rocks. The resulting pregnant solution is then pumped back to the surface, where it can be further treated. Therefore, uranium is effectively pumped out of the ground in a similar way to oil.

ISR has the advantages that it tends to have lower capital costs, faster start-up times and lower environmental impacts. When a well is exhausted, it simply needs to be sealed or capped, and the land can revert to its previous use. Not all uranium ore deposits are suitable for ISR. Only 18% of world uranium resources are hosted in sandstone uranium deposits; however, more than 60% of total uranium production currently uses ISR techniques because of its advantages. Such advantages are even more significant as inflationary pressures and stricter environmental regulations make it more difficult to permit, develop and operate conventional mines.

As a result, Kazatomprom is the most profitable uranium miner in the world. Not only does it enjoy the best margins in the sector, but it also has the biggest uranium reserves. At the end of 2022, the company reported 313 thousand tons of uranium metal equivalent ((UME)) tonnes of proved and provable reserves. For comparison, Kazatomprom's 2022 production was around 11 thousand tonnes and global production around 50 thousand tonnes. Therefore, Kazatomprom is in the best possible position to capitalize on the current uranium bull market.

The reader is certainly familiar with the fact that uranium is currently trading below its marginal cost of production. While spot is selling for around $50 per pound, the cost to bring online new primary supply is above $70 per pound. In addition, the uranium market is in a structural deficit. Therefore, the uranium price will have to rise in order to incentivize new production when the inventory of secondary supplies is exhausted. In a scenario where the uranium price overshoots to the upside, Kazatomprom would be a major beneficiary. It could in principle ramp up production faster than any other miner and at a lower capital cost.

The picture, however, is not so simple, as there are other considerations that must be taken into account. Kazatomprom is facing a number of challenges. First of all, Kazatomprom suffers from a geopolitical discount. Kazakhstan is a relatively young country. The disorders of January 2022 have revealed that it is still politically unstable. In addition, the Russo-Ukrainian war is putting further strain on the company's operations. While Kazatomprom has not been directly affected by the sanctions, there are indirect effects. Kazatomprom relies on Rosatom, the Russian state-owned nuclear technologies company, for enrichment services. In addition, it is experiencing higher costs for exporting its products (transportation costs have doubled in 2022 compared with the previous year), a consequence of the fact that its main export route currently goes through Russia (first by train and then by sea out of the port of St. Petersburg). Finally, many of the company's suppliers are located in Russia, which is creating delays in the provisioning of new material and cost increases.

Kazatomprom is proactively taking steps to limit its exposure to Russia. It is arranging for alternative suppliers and is testing a new Trans-Caspian export route, which does not go through Russia. In addition, it is quite interesting to note the recent agreement between Kazatomprom and China General Nuclear (CGN), the main nuclear plant operator in China. Under the terms of the agreement, the parties committed to constructing a new fuel assembly plant at the Ulba Metallurgical Plant. CGN provided (together with cash considerations) a guarantee that Ulba's production will be purchased, in exchange for a 49% interest in Kazatomprom's subsidiary "Ortalyk" LLP. In December 2022, the Ulba plant carried out its first delivery of nuclear fuel (around 30 tonnes of lowly enriched uranium) to CGN. The plant plans to increase production capacity to 200 tonnes per year by 2024. Thus, Kazatomprom is simultaneously diversifying away from mining into the nuclear enrichment services sector and forging strong business relationships with China. A strategic move by the company, considering that China represents the main source of growth for nuclear energy in the coming decades.

Unfortunately, investors must accept the fact that a geopolitical discount is likely to continue to weigh on the valuation. Kazatomprom is a state-controlled company in an emerging market country, exposed to both internal uncertainties and the influence of Russia. The Russo-Ukrainian conflict has painfully revealed the importance of security of supply for several strategic commodities. With Russia dominating the nuclear enrichment sector and nearby Kazakhstan dominating the uranium mining sector, it is not impossible that Western buyers will start to place a greater emphasis on the source of origin. One could even envision a future scenario in which uranium sourced from friendly countries is trading at a significant premium. Such arguments could be used to justify the fact that, for instance, Cameco, which is clearly inferior as a company to Kazatomprom, is deserving of a higher multiple.

As already remarked, Kazatomprom enjoys a dominant position in the uranium market. That the company is greatly benefiting from the recent increase in uranium prices is clearly evidenced by its record financial performance for 2022. However, going forward, Kazatomprom will have to face the problem of rising production costs. This increase in costs is the result of two main forces: inflation and logistical challenges. The inflationary problem is felt quite acutely at the moment in Kazakhstan; however, it is mitigated by the fact that any nominal increase in costs measured in the local currency is partially counterbalanced by rising revenues due to the stronger dollar. The logistical problem is the result of the covid pandemic and, more recently, the war in Ukraine. Because of covid-related shipping constraints, the company had to delay wellfield development in 2021. Since there is an 8-10 months delay between wellfield development and uranium extraction by ISR, 2022 production fell short compared to the previous year. These delays have accumulated and are expected to continue into 2023. In addition, the war in Ukraine has put further pressure on the company's suppliers. As a result, Kazatomprom has incurred higher costs and significant delays in the procurement of critical materials, such as certain types of pumps, drilling equipment, pipes and sulfuric acid (a critical component needed for uranium leaching). While such challenges are expected to resolve in time, in the short term they are causing the company to slightly lower its production guidance for 2023 and, in general, call into question its ability to ramp up production if needed (at the moment, the company is targeting a 20% reduction of production volumes relative to Subsoil Use Agreements with the government of Kazakhstan).

Deep dive on financial results

The rest of the articles contains more detailed comments regarding the recently released 2022 financial results.

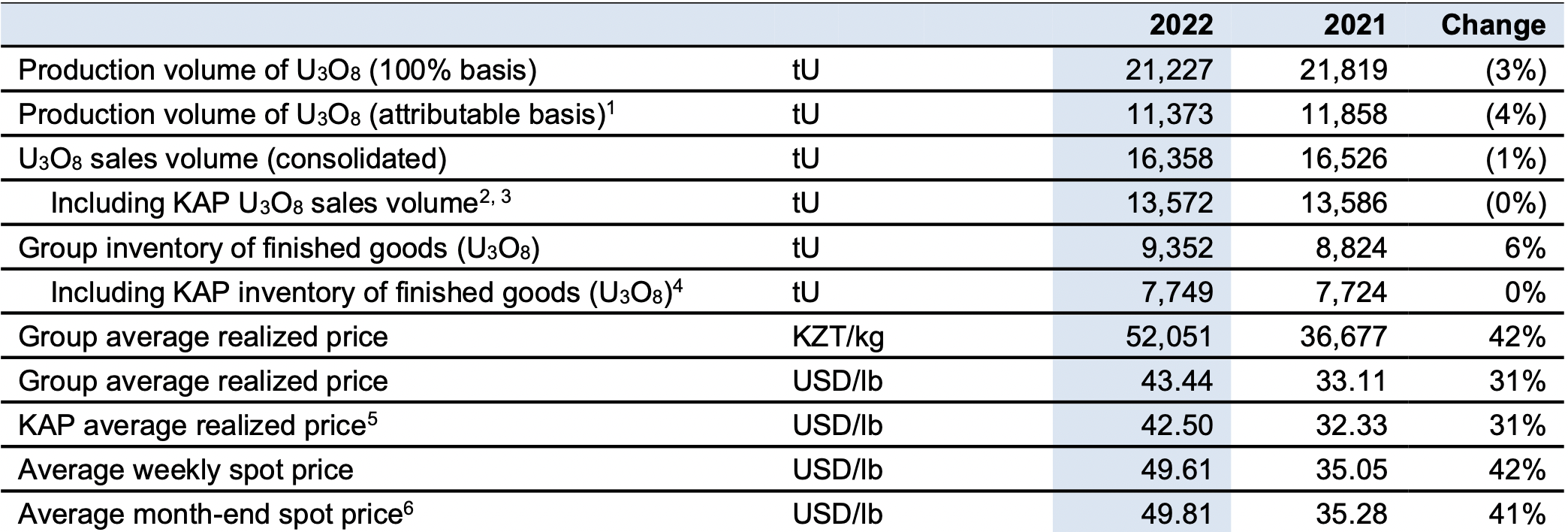

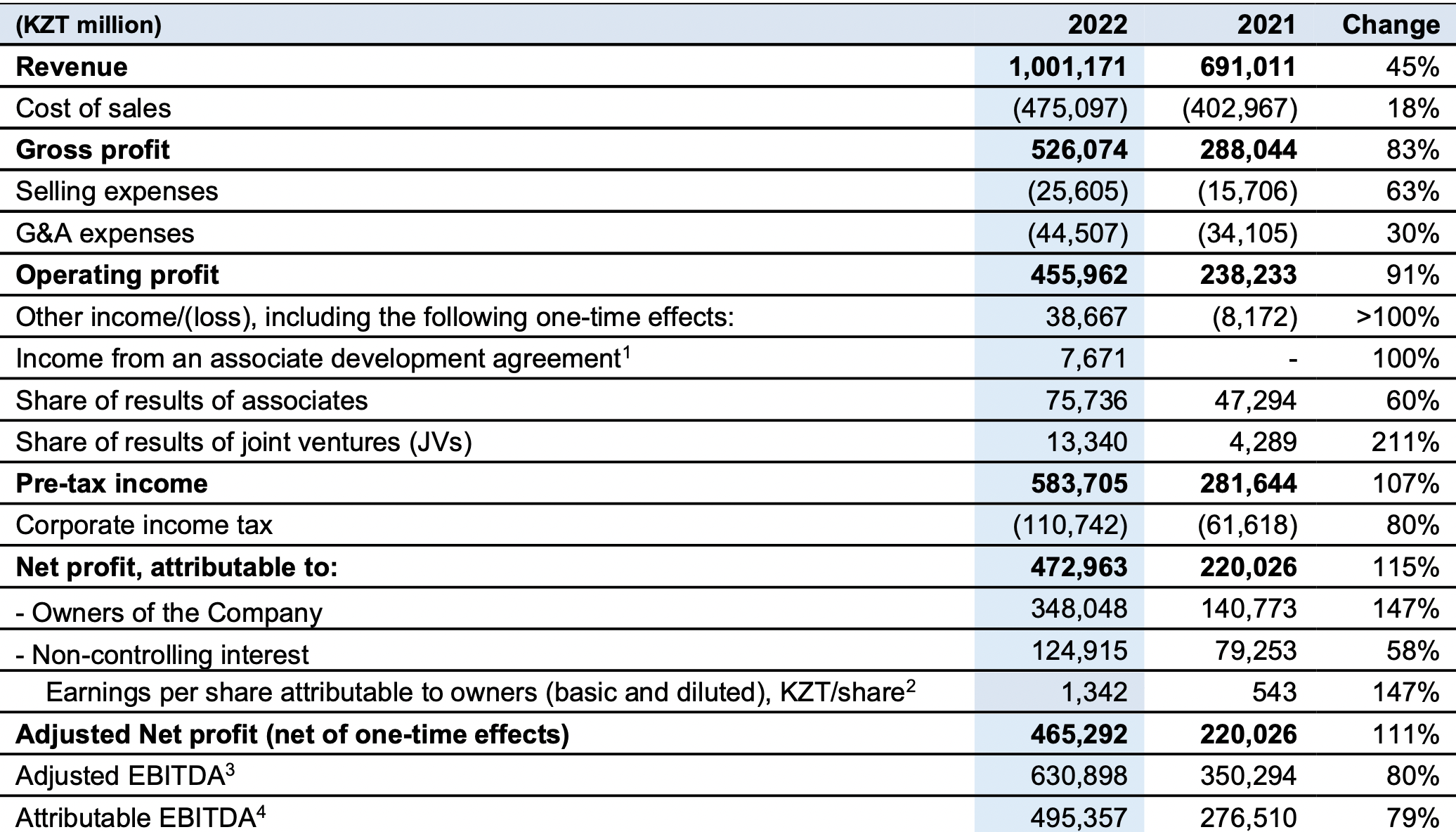

It should immediately be noted that Kazatomprom reports its financial results in the local currency, i.e. the Kazakh tenge (KZT). However, uranium prices are usually reported in US dollar terms. Most of the company’s revenues (and borrowings) are denominated in US dollars; most of the company’s expenses are denominated in tenge. The dollar has strengthened against the tenge by around 7.4% during 2022. Therefore, all the results are "inflated" by the fact that they refer to tenge amounts. For example, revenues were up by 45%, a consequence of the fact that the average realized uranium price (in tenge) increased by 42% (sale volumes were almost unchanged). However, the average realized uranium price was up only by around 31% in dollar terms.

Normally, commodity exporters benefit from a strengthening of the currency in which their exports are denominated, since on the contrary their costs are denominated in the weakening local currency. However, inflation can change significantly the overall picture. Because of inflation, costs can rise at a faster rate than that at which the local currency is weakening. This is indeed the case for Kazatomprom, and is a consequence of the fact that inflation is running hot in Kazakhstan at the moment (in December 2022, inflation stood at 21.2%). To determine the net effect on costs, it is necessary to combine the effect of both inflationary and exchange rate forces. With the inflation rate far in excess of the tenge depreciation rate, it is not a surprise the Kazatomprom saw its costs rise significantly in dollar terms. Cash cost was up 16%, a result of inflationary pressures and increase in payroll for personnel. AISC was up even more, by 28%, mostly because of higher capital costs. Capital costs alone in fact rose by 61%, a result of the higher costs incurred because of logistical difficulties in provisioning materials for wellfield development.

{kind=link}

An increase in costs usually has a contractionary effect on margins. However, revenues are also increasing in dollar terms. The company is clearly benefiting from rising uranium prices. During 2022, the increase in uranium spot prices was actually modest: despite a jump in spot prices after the Russian invasion of Ukraine, the overall yearly increase was around 10% (in US dollar terms). However, realized prices are not (predominantly) based on spot prices and there is lagged effect, so that Kazatomprom is reaping now the benefits of the increase in the uranium price in 2021. In 2022, the average realized price increased by 31% (in US dollar terms).

Uranium production metrics (Company's financial results 2022)

{kind=link}

The two effects, i.e. the increase in both revenues and costs, push in different directions. Since, however, revenues are rising faster than costs, and Kazatomprom has relatively high margins, the net result is that profits are expanding. Therefore, 2022 was a record year for the company. Gross profit was up 83%, operating profit up 91%, adjusted net profit up 111%, despite costs also rising.

{kind=link}

In 2023, the company is guiding for production volumes between 10,600 and 11,200 tonnes, around 4% below 2022 results and around 20% below maximum capacity based on Subsoil Use Agreements. Cash cost is expected to range between $12 and $13.5 per pound, up considerably compared to 2022 ($10.25 per pound). Similarly, AISC is also projected to rise, from $16.19 to $20-21.5 per pound. In other words, Kazatomprom does not see the current inflationary and logistical problems abating in 2023. To quote from the company's financial results statement:

Supply chain challenges are expected to continue in 2023 [...] While Kazatomprom will make every effort to meet its uranium production plan, final production volumes for 2023 may still fall short of the target level.

Therefore, unless the uranium price keeps moving upward, 2023 could see a reduction in margins. It is also worth considering that tax expenses will also be up, as the new Mineral Extraction Tax ((MET)) comes into effect from January 2023 in Kazakhstan.

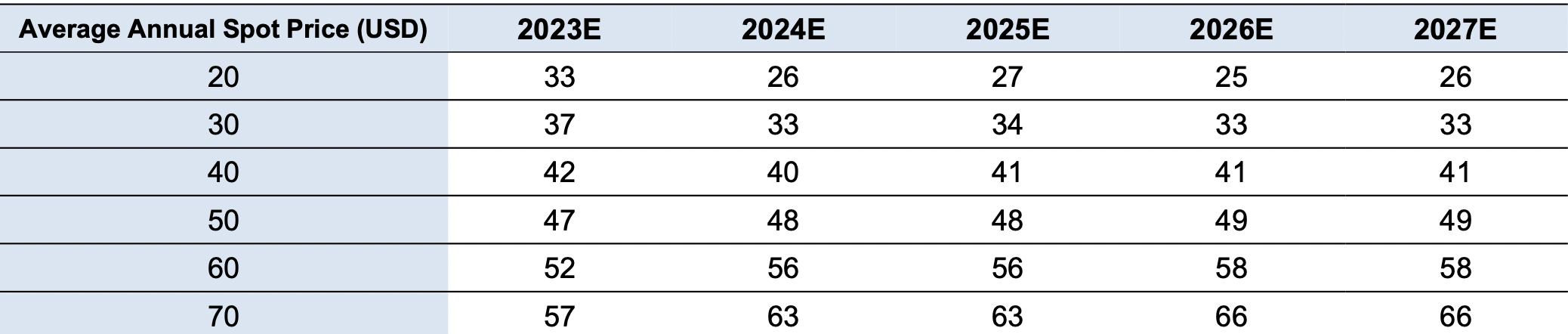

Sensitivity to rising uranium prices (Company's financial statements 2022)

{kind=link}

Conclusion

In conclusion, I consider Kazatomprom a top choice in the uranium mining sector. With a cheap valuation, a commitment to returning capital to shareholders, leverage to uranium prices, assets in the lowest quartile of the global cost curve, high margins and a disciplined approach to production, Kazatomprom is well-positioned for the current uranium bull market. At the same time, the events following the war in Ukraine have diminished its attractiveness compared to one year ago, in particular through an increased geopolitical discount and higher costs.

While I prefer Kazatomprom to Cameco from a purely value-based perspective (and I believe that political risks are exaggerated), investors in Cameco are still likely to achieve satisfactory returns despite the higher valuation. Investors in selected junior miners are also likely to enjoy high returns, simply because of the higher leverage (though rising capital costs should be taken into consideration). I would be interested in re-entering the uranium juniors space in case of a market sell-off event, as I believe the easy money has probably already been made in this sector (the best moment to buy was when it was left for dead in 2020) and that the current margin of safety is not enough for most names. Finally, given rising production costs, there remains a very strong case to invest in physical uranium itself, with the Sprott Physical Uranium Trust (SRUUF), (U.UN:CA) providing an efficient vehicle to speculate on rising prices.

For further details see:

Kazatomprom: A Top Choice For Uranium Exposure