K - Kellanova: It's Too Early For Me To Consider The Company Attractive

2024-01-18 20:57:03 ET

Summary

- Kellogg Company has spun off its North American cereal business and will focus on snacks and plant-based protein brands.

- The company's financials show a high level of debt, but it is managing it smartly and is not at risk of insolvency.

- The company's efficiency and profitability have declined in recent years, but improvements are expected as inflation subsides and costs normalize.

Investment Thesis

With margins down badly this year and a spin-off of the North American segment and seeing that the company is about to announce its quarterly results, I wanted to see how Kellanova ( K ) performed in the past to see if, after the spin-off, it would be a good time to start a position. Revenues may see a slight acceleration as the company starts to focus on snacks, however, with margins down this year to multi-year lows, and the company’s share price being stagnant for the last decade, I am assigning a hold rating until I see substantial improvements in margins and revenue growth.

Briefly on the Company

Formerly known as Kellogg Company, recently spun off its North American cereal business and will focus primarily on snacks and plant-based protein brands, while the spun-off company is going to be called the WK Kellogg Co. under the ticker name (KLG). Kellanova is still going to distribute cereals as it retains its license for international markets. The company’s famous brands include Eggo, Pringles, Pop Tarts, Rxbar, Cheez-It, and many different cereal brands.

What to Expect from the next earnings report

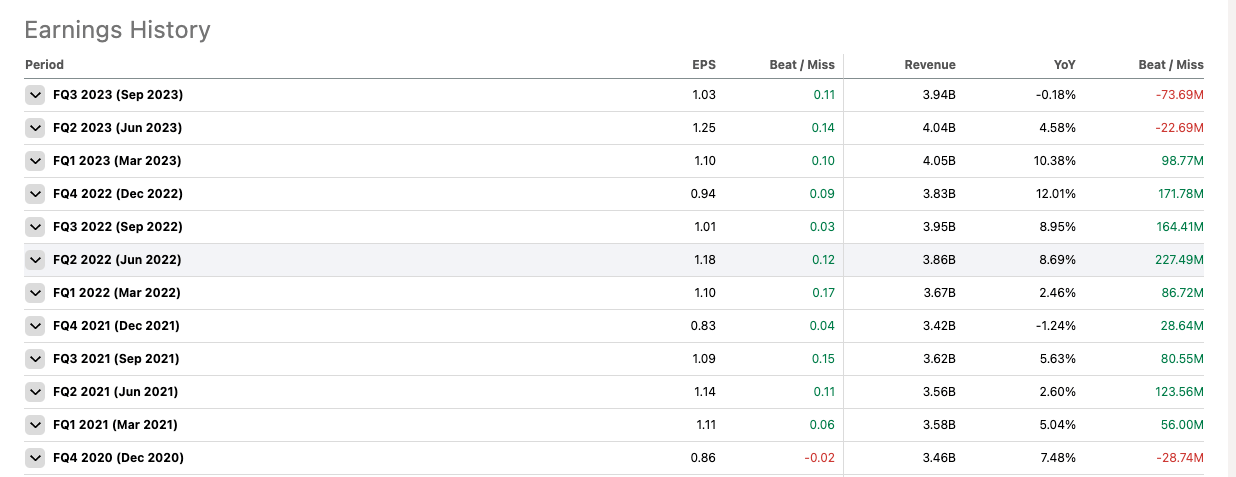

In terms of EPS, GAAP, and non-GAAP are expected to come in at around $0.74 and $.073, respectively, and around $3.1B in revenues. Over the last 12 quarters, the company missed 3 estimates, so there is a high likelihood that K will beat these estimates.

{kind=link}

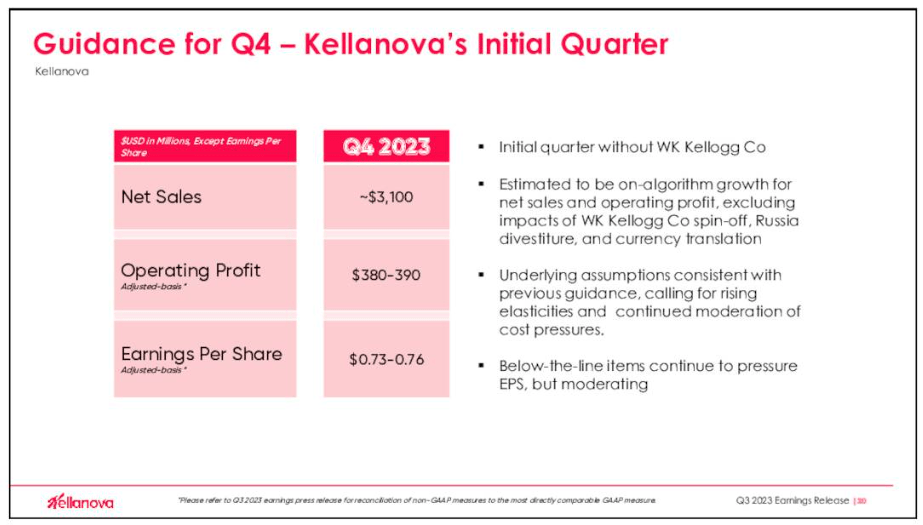

Furthermore, the next quarter will be fully spun off from WK Company (KLG) and any remaining numbers will be disclosed as discontinued operations.

The management expects to continue to see gross margin restorations and should come in at around 33%, which is slightly higher than what K managed to achieve so far, as you'll see in the financials section later. The company also expects to make around $380m to $390m in adjusted operating profits.

{kind=link}

I believe these estimates should be easy to beat. I will be looking forward to hearing how the management is going to go about streamlining the business further and improving margins across the board. Taking out the NA cereal segment will of course affect the company's top line by around $1B but if the company can continue to become more efficient, then value will follow.

Financials

As of Q3 '23, the company had around $1.1B in cash and equivalents, against $5.5B in long-term debt, which has only increased by around $200m since FY22. Many people will avoid companies with excessive debt, and I don't blame them for wanting nothing to do with the added risks leverage carries, however, if the company is managing it smartly, utilizing debt is a great way to complement the company's day-to-day operations. There are a few metrics I like to look at to determine whether the company is using leverage smartly and is not too risky.

Firstly, I look for the company's debt not to be more than the company's total assets. I like to see the debt-to-assets figure below 0.60. In the last 5 years, the company was comfortably under that threshold, so it seems that the company is not overleveraged in terms of its assets. The next ratio I like to look at is how much debt it has in terms of shareholder equity. Here, I look for a debt-to-equity ratio to be under 1.5. This metric is a little more volatile as only in the last full financial year and so far in Q3 ´23, the company managed to go under the acceptable level. The company's debt position is improving. Lastly, I like to look at the company's ability to meet its debt obligations, in terms of being able to pay down its annual interest expenses with the operating profit it earned during the period. Many analysts consider an interest coverage ratio of 2x to be a healthy ratio, however, I prefer to see at least a 5x, as this allows for much more leeway when it comes to bad years of performance, in which operating profit drops significantly. 2x is a little too close for comfort. Over the last 5 years or so, K's interest coverage ratio was anywhere from 5x to 8x, which means that it even passes my more stringent requirements, so it is safe to say the company is not at any risk of insolvency.

{kind=link}

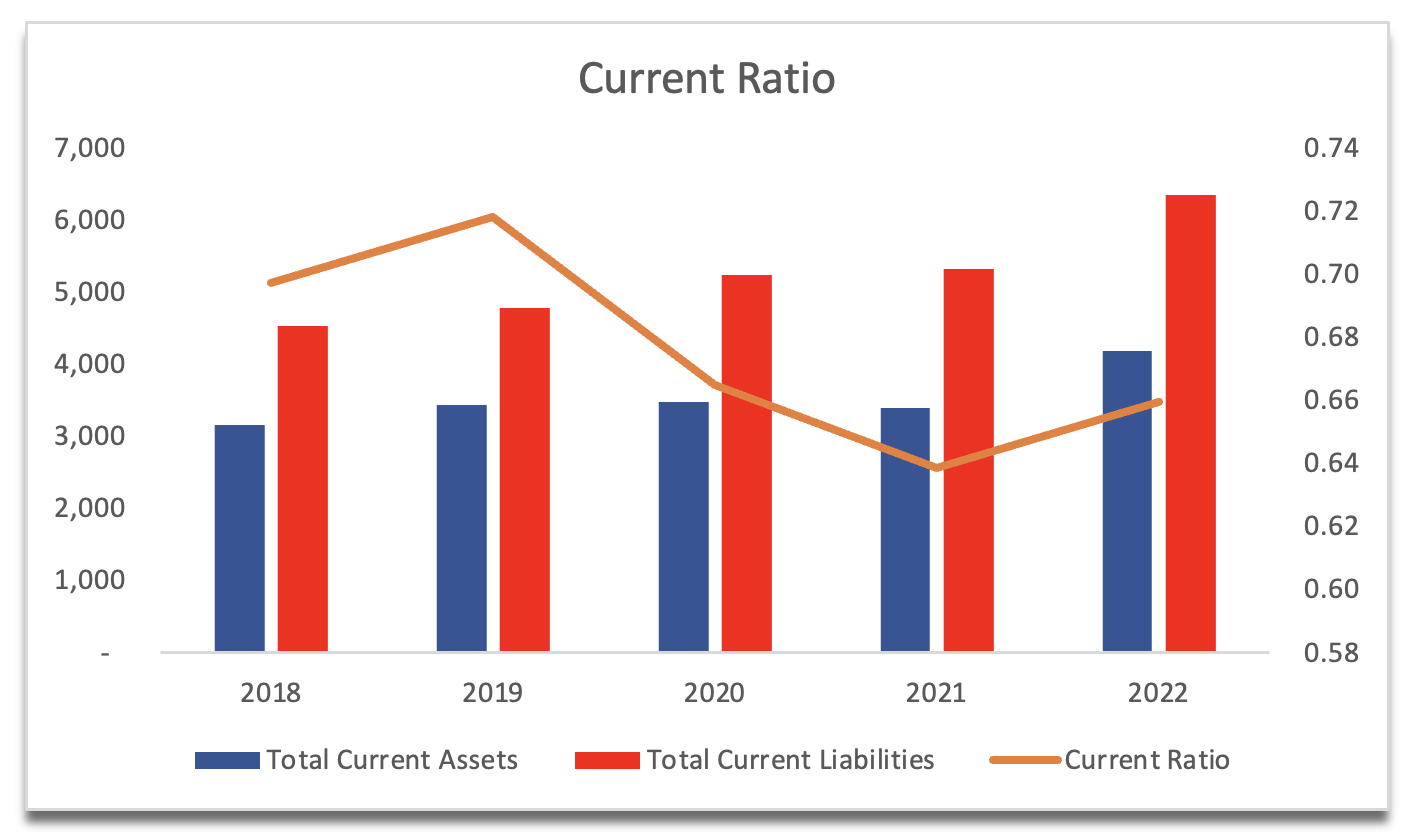

Over the last decade at least, the company’s current ratio has always been under 1, which doesn't necessarily mean the company is in financial trouble. It is very common for companies like Kellanova to consistently have a current ratio below 1, because of the industry it is operating in, which is the fast-moving consumer goods of FMCG. The company has a relatively high inventory turnover, around 60 days, which means the company converts its inventory to cash in about 2 months. This reduces the need for readily available current assets, which lowers the current ratio. So, for this reason, I am not worried about the company's current ratio. K has no liquidity issues.

{kind=link}

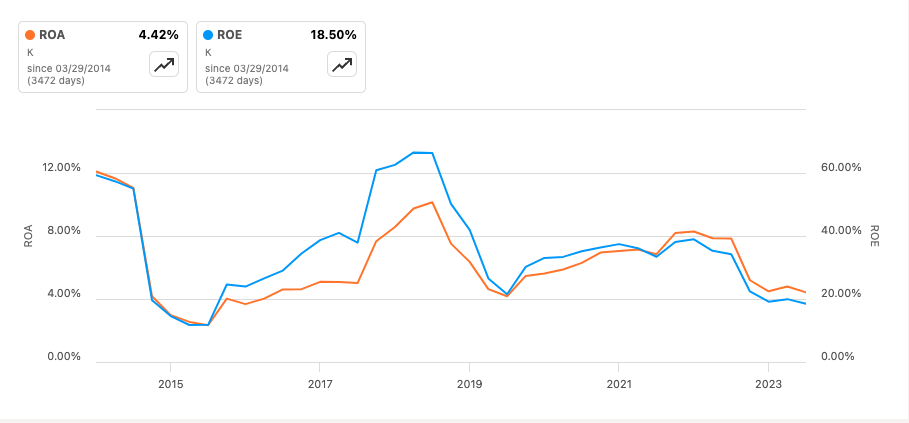

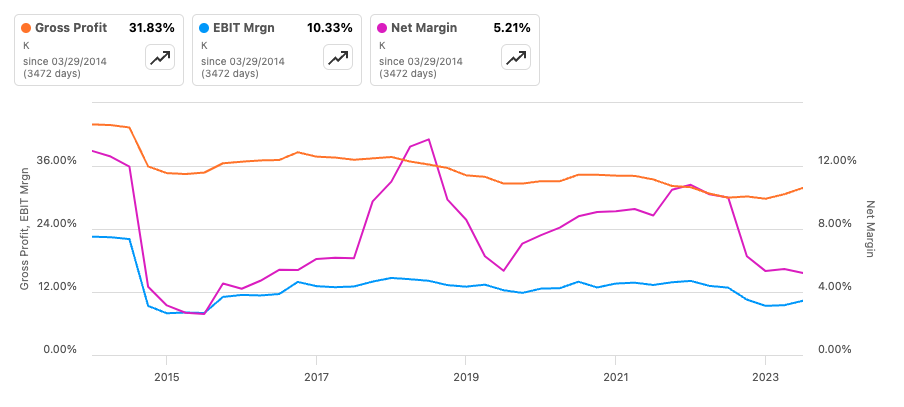

In terms of efficiency and profitability, the company's ROA and ROE have seen better days. The company's efficiency has been coming down since FY18 and quite dramatically. This decline can be explained by the lack of top-line growth, while the cost of goods sold, or COGS increased over the same period. Even though the increase in COGS every year wasn't much, it all added up to reduce efficiency and profitability. For example, in FY19, the company saw 0% growth in top-line, while COGS increased by 4%. Next year, the company saw a 1% increase in revenues, while COGS dropped by only 2%, and a year after that, revenues went up around 3%, while COGS went up 6%. Lastly, in FY22, revenues were 8% while COGS increased by 11%. So, we can see that the company did not fare well during the tougher economic times of higher inflation, which pushed its input costs, and the company was not able to pass on these costs to the consumer, leading to inefficiencies. As inflation comes down, I would expect these to improve once again, and I’m eager to see how they will develop in the near future.

{kind=link}

In terms of how efficiently the company is employing its total capital compared to its competitors, we can see that K is in the top echelon and only has been beaten by PepsiCo (PEP), which isn't even a direct competitor but does share a few products that can be substituted. So, it looks like the management is doing a decent job at allocating the capital available to profitable projects and has some sort of competitive advantage and a decent moat over most of its peers.

ROTC vs Competitors (Seeking Alpha)

{kind=link}

In terms of margins, we can see a lot of volatility in the bottom line over the last decade, and it is at the lower end in the most recent quarters. As I mentioned earlier, the company was not able to predict the increase in input prices and was unable to pass on the costs to the consumer on time, leading to lower net margins. I believe that with time this will also improve once again as inflation subsides and costs of production normalize.

{kind=link}

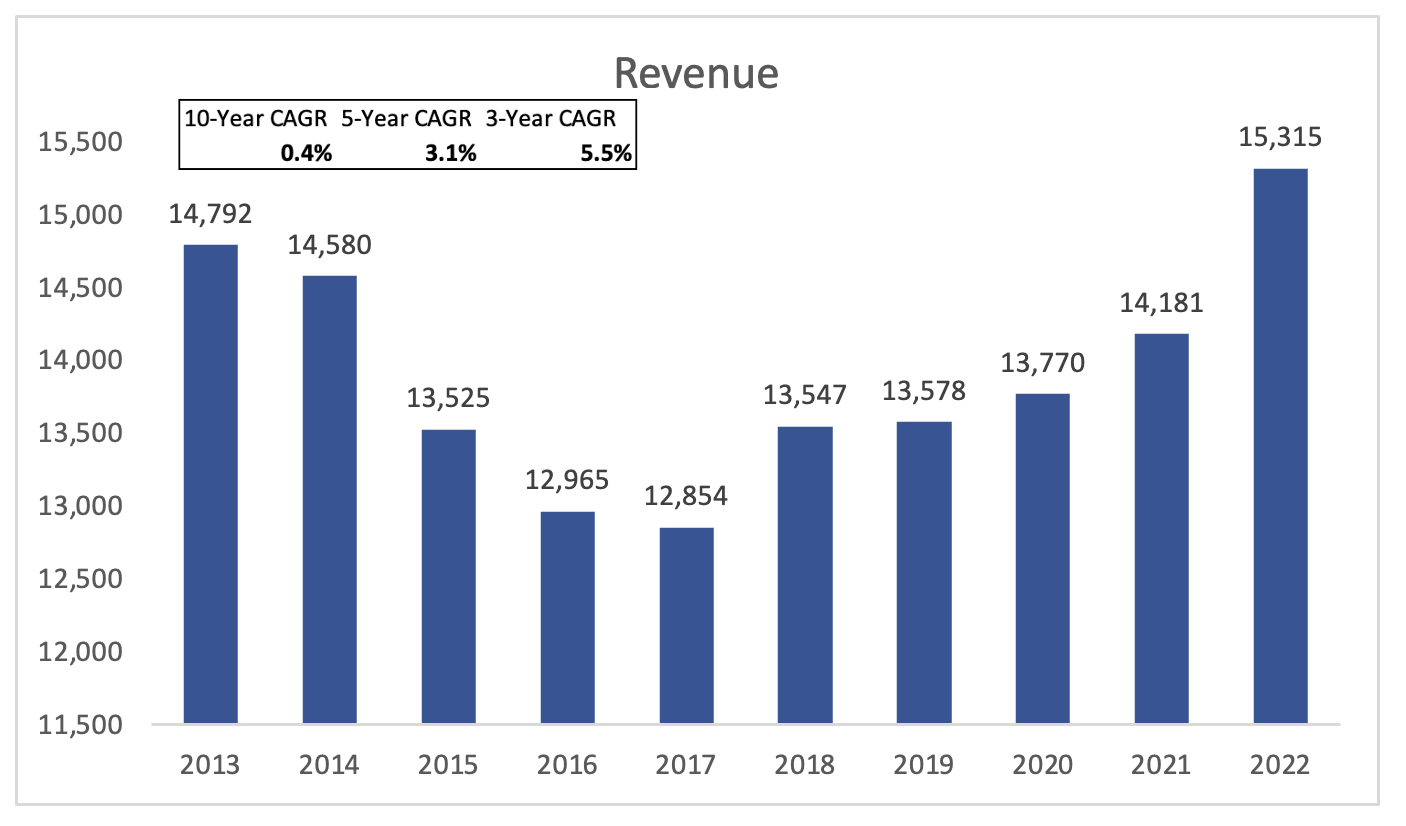

The company’s revenue growth has been poor over the last decade. It went nowhere from FY13 to FY22 in terms of 10-year CAGR. Over the last 5 years and 3 years, we saw a slight acceleration mostly because FY17 was a tough year for the company and only recently it reached the revenues it saw back in FY13. Analysts are estimating around a 1% decrease in sales for FY23, while also estimating around a 12.4% decrease for the next year, which is understandable because the company spun off its North American cereal operations. After these two years, I will take the estimates with a grain of salt as it is virtually impossible to predict what is going to happen to the economy and how the company is going to perform.

{kind=link}

Overall, it seems that the company is on the lower end of its historical performance and may bounce back in the upcoming couple of quarters once we see more improvements in the economy, which should bring down costs. Furthermore, the company incurred some extra costs due to the preparation of the separation, so I would expect margins to improve just by that in the next few quarters. The company has a lot of debt, which may deter a lot of investors, so I would like to see the management taking some initiative to lower its outstanding debt.

Valuation

It is not easy to estimate what the company's revenue growth for the next decade will be, so I like to approach these situations with a conservative mindset. Once the NA cereal business is not included in K's financials, it will see quite a drop in total revenue as the segment accounted for around 34% of total sales as of the 9 months ended September ´23. It won’t see a 33% drop in revenues because it will still sell cereal internationally, however, it will be a substantial drop, nonetheless. The cereal segment grew at around 4% in the last 9 months, while the snacks segment grew almost double that, so the growth is not coming from the cereal side of things, which is good for the company.

I decided to take the analysts' estimates for FY23 and FY24 as they make sense to me, however, after that, I decided to grow at a moderate pace for the remainder of the model, which ended up being 4% CAGR over the 10 years. To cover my basis, I also included calculations for the optimistic and the conservative outcomes. Below are those estimates.

{kind=link}

In terms of margin EPS, I went more conservatively to give myself some more margin of safety. EPS will grow around 20% for FY23, decline by 13% in FY24, and then grow at around 10% average over the remainder of the model period. Gross margins will see an improvement of around 500bps over the period, which will lead to improved margins overall. Below are those estimates.

Margins and EPS assumptions (Author)

{kind=link}

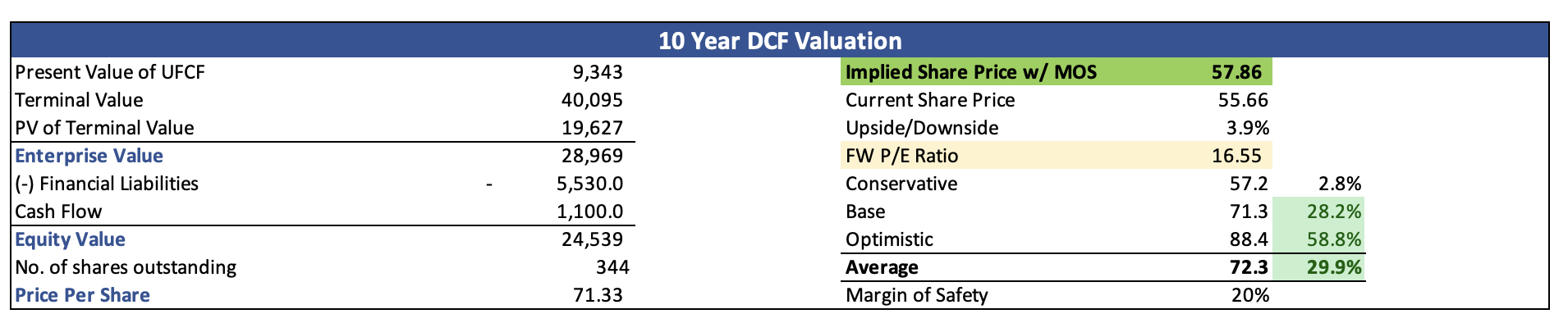

For the DCF analysis, I went with the company's WACC of 7.4% as my discount rate and a 2.5% terminal growth rate. Furthermore, I decided to add another 20% margin of safety to the final intrinsic value calculation, to give myself even more room for error. With that said, Kellanova’s intrinsic value is around $58 a share, which means the company is trading slightly below its conservative fair value.

{kind=link}

Risks to Consider and Comments on the Outlook

The downturn in the economy might last much longer than anticipated with high inflation, which may continue to affect the input costs. This will translate into lower margins for longer and we may not see a bounce for another year or more if that happens. Inflation isn't as bad as it was a while back, however, it is still lingering higher than where the FED likes it to be, so we will see higher interest rates for longer. Volatility in the stock market is not behind us yet, and I would expect further fluctuations in the share price of K because of it.

In general, a spin-off is a great opportunity to streamline all the separate businesses and make the two companies more efficient. This comes with a lot of costs, which lower margins, as we saw in the recent quarters. This may continue a little while longer, and the company’s margins may suffer not just from high input costs but also from the aforementioned separation costs. This may keep the margins lower for longer, which may bring down its share price further.

As mentioned before, the cereal segment didn't see much growth this year, however, the snack segment saw around 8.5% growth, which means that the company should see much better growth numbers going forward unless the products are not great and the company loses market share to its competitors, of which there are many in this industry.

I would like to see the company taking action in paying down its debt, as that may attract many debt-averse investors in the future.

Closing Comments

So, it looks like the company is not a bad buy at these price levels. I wouldn't be surprised if the share price keeps coming down because of low margins and the overall macroeconomic environment. I believe the spin-off should work well in the future and the growth in the top line should be more apparent now that the NA cereal brand is off the financials. It is up to you to do further due diligence and see if you would like to invest in the company. The company's share price went nowhere for the last decade and the spin-off may or may not change that. I am going to hold off for now until I see how this more streamlined company is going to perform over the next year and whether the company will manage to grow at a better pace than in the past.

For further details see:

Kellanova: It's Too Early For Me To Consider The Company Attractive