K - Kellanova: The New Chapter Is Not As Exciting As It Might Seem

2023-11-10 12:35:36 ET

Summary

- After reporting Q3 2023 results, Kellanova's management is creating an exciting narrative around potential growth in snacking.

- The company's brand portfolio, however, is inferior to those of the leaders in the space which would be a problem.

- Margins will experience a tailwind following the spin-off, but in my view this will be short-lived.

- Even though the company is priced very conservatively, I don't see Kellanova outperforming its high quality peers.

After years of disappointing shareholder returns, the rebrand of Kellogg to Kellanova ( K ) is now a fact and shareholders are eagerly awaiting the first standalone results of the company when it reports full fiscal year results early next year.

By focusing on the highly attractive snacking category, Kellanova's management and investors alike are looking forward to a quick turnaround after the stock did underperform the broader market by a very wide margin in the past three years.

{kind=link}

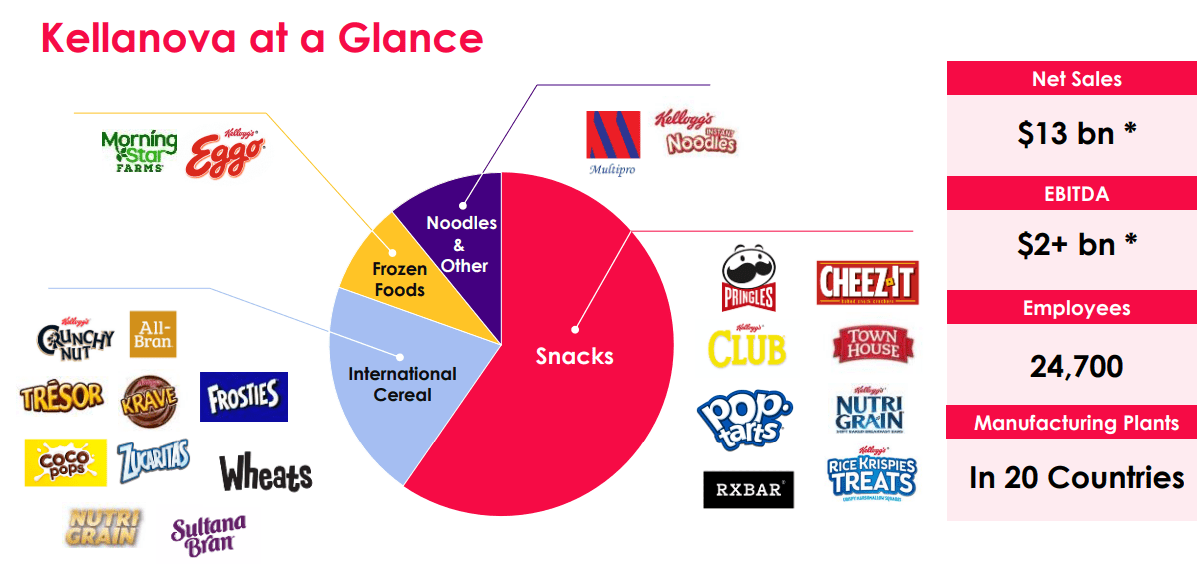

After the spin-off, Kellanova is now focusing on its Snacking business, which will likely only grow in importance within the company's sales mix.

{kind=link}

Although this makes sense, given the attractiveness of the snacking product category in terms of growth, customer loyalty and margins, Kellanova relies on a very small number of brands within this space.

Half of our net sales come from five highly differentiated brands, Pringles , Cheez-It , Pop-Tarts , Rice Krispie Treats and Eggo (...)

Source: Kellanova Q3 2023 Earnings Transcript

Apart from Pringles, Kellanova does not have any truly international brands in the snacking space and this is a major disadvantage to the current leaders in the space, such as Mondelez International, Inc. ( MDLZ ), PepsiCo, Inc. ( PEP ) and Nestlé S.A. ( OTCPK:NSRGY ).

Although the company generates roughly half of its sales outside of the United States and Canada, the overall exposure to Emerging Markets in the snacking category is also very low. I recently talked about this in a thought piece on Mondelez , where I showed why geographical exposure matters so much about shareholder returns.

That is why, the market is still having a hard time assessing the overall impact of the recent restructuring and has punished both Kellanova and WK Kellogg Co ( KLG ) following the spin-off.

As a result, K now trades at multi-year lows and investors are getting excited by the prospects of better returns ahead given the spin-off of the slow-growth North America Cereal business. But as the headline of this article suggests, I am still skeptical of Kellanova's ability to outperform its peers and reward shareholders with superior returns.

Brands, Pricing Power and Volumes

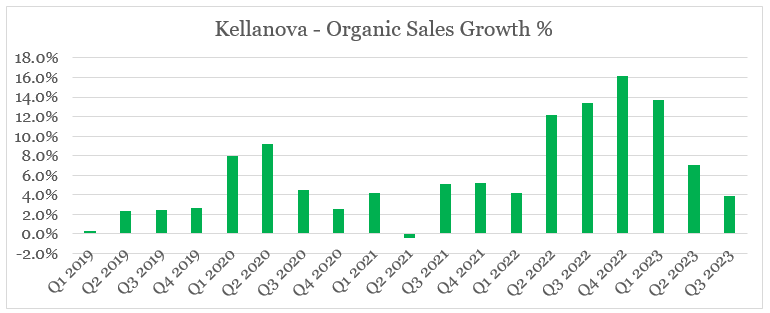

On a combined-company basis, Kellanova's third quarter results were very disappointing as organic sales growth declined to below 4%, from nearly 14% a year ago.

prepared by the author, using data from Investor Presentations

{kind=link}

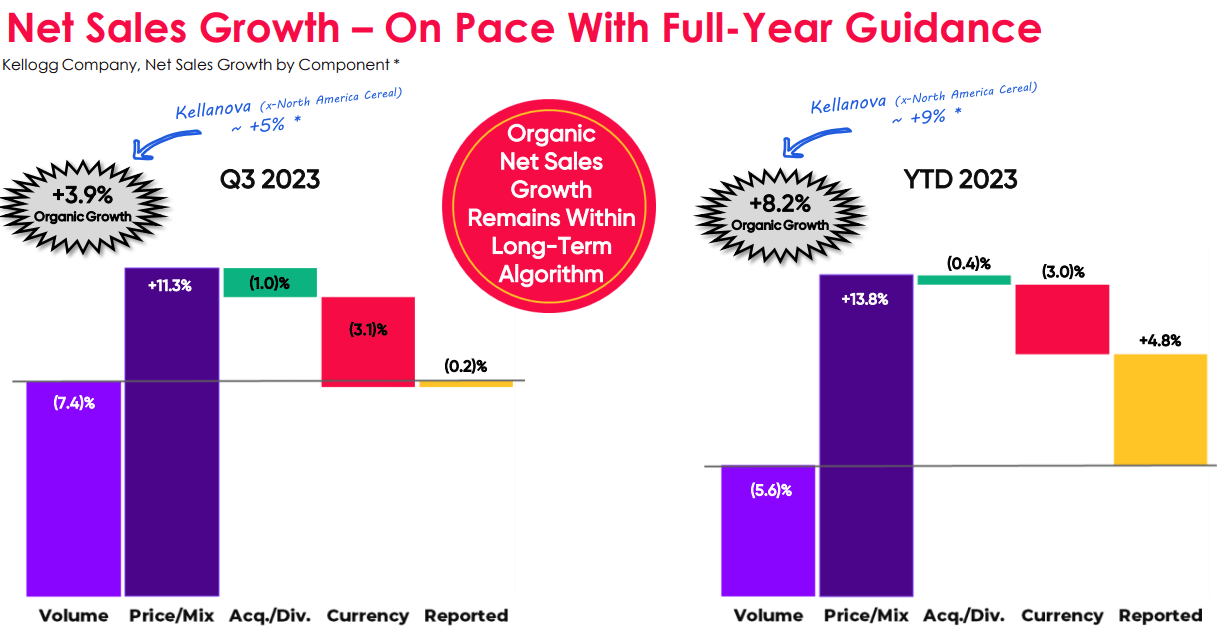

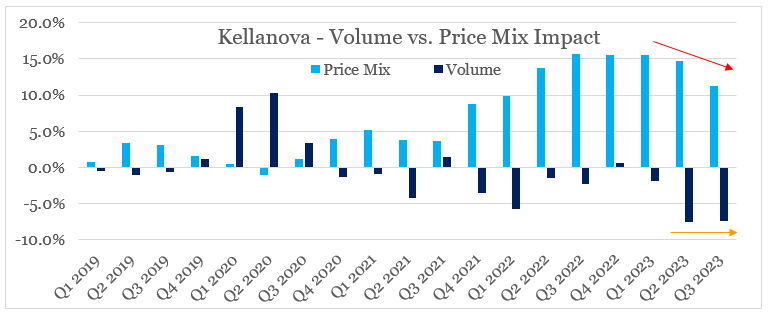

Although pricing initiatives are still having a major positive impact on revenue growth, volume declines were significant of -7.4% during the third quarter.

{kind=link}

Once we plot the quarterly impact of price/mix versus volume we could see the problem that the combined company had - significant volume declines at a time when pricing is returning to normal.

prepared by the author, using data from Investor Presentations

{kind=link}

That is why, the Q4 2023 results will be very important as they will give us some much needed context for Kellanova's business on a standalone basis.

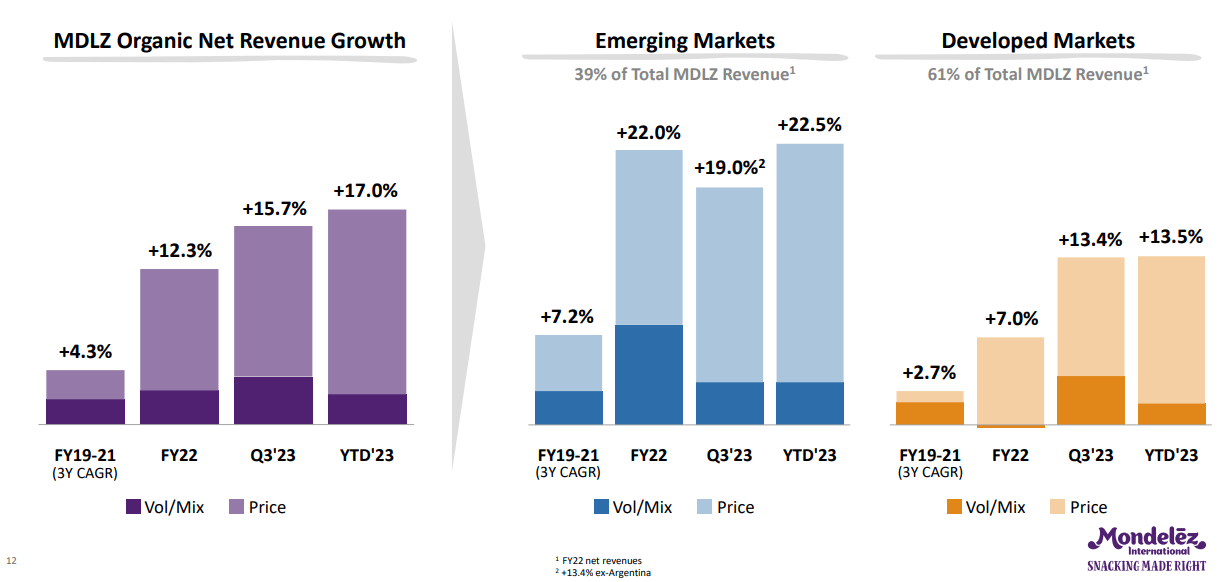

Given the strong exposure to snacking, these results would need to be evaluated against the likes of Mondelez, which delivered outstanding results in terms of significant price increases coupled with volume growth.

{kind=link}

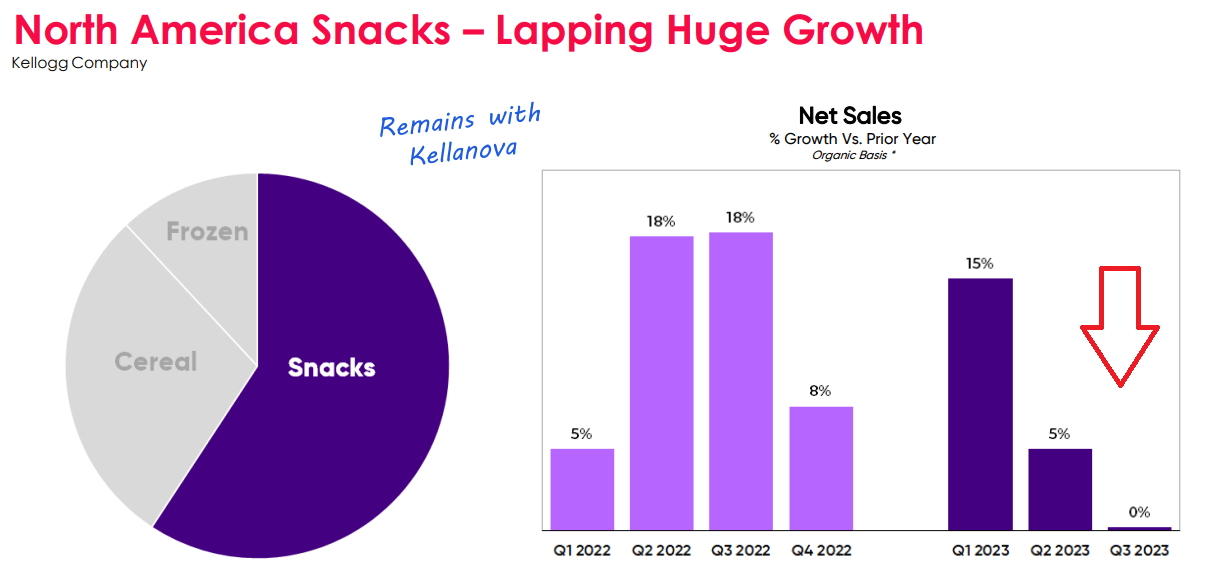

The most recent quarter, however, has already given us some indication of what we could expect. By far the most attractive segment for Kellanova - The North America Snacking business, experienced a sharp drop in organic net sales growth to almost 0%.

{kind=link}

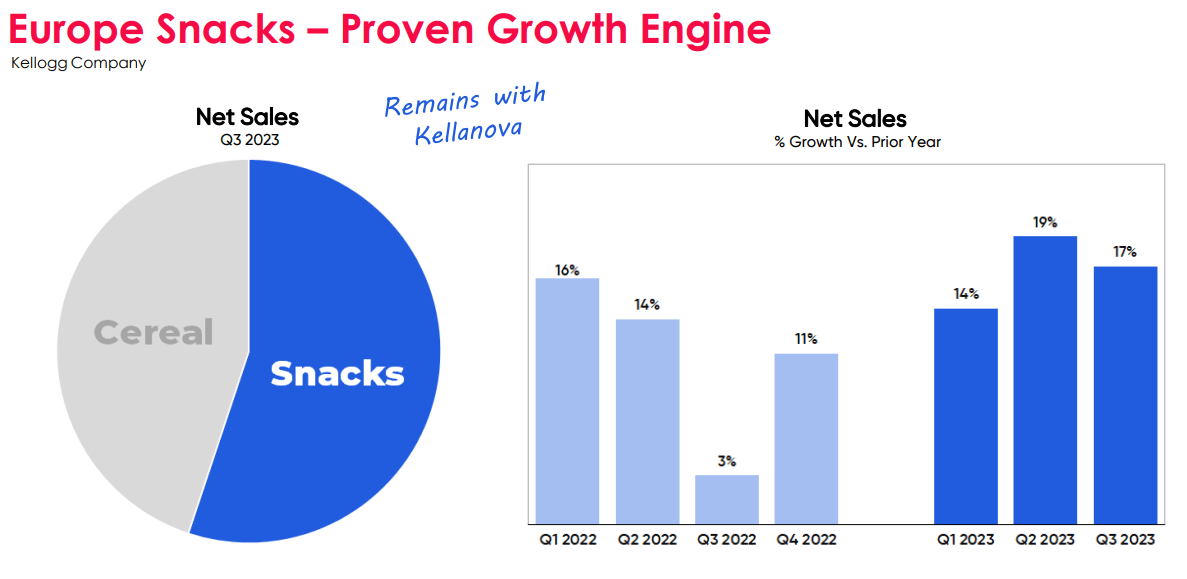

Europe Snacks remains the bright spot for Kellanova with strong revenue growth across the board - driven by double-digit growth in both salty snacks and portable wholesome snacks categories.

{kind=link}

In both of these geographies, Kellanova relies heavily on the Pringles brand, which is experiencing significant momentum in Europe.

(...) with Pringles outpacing the category in markets like the UK, France, Spain, Italy and Poland

Source: Kellanova Q3 2023 Earnings Transcript

As optimistic as this sounds, the salty snacks category is extremely competitive and having only one international brand in this space is insufficient for sustainable long-term growth.

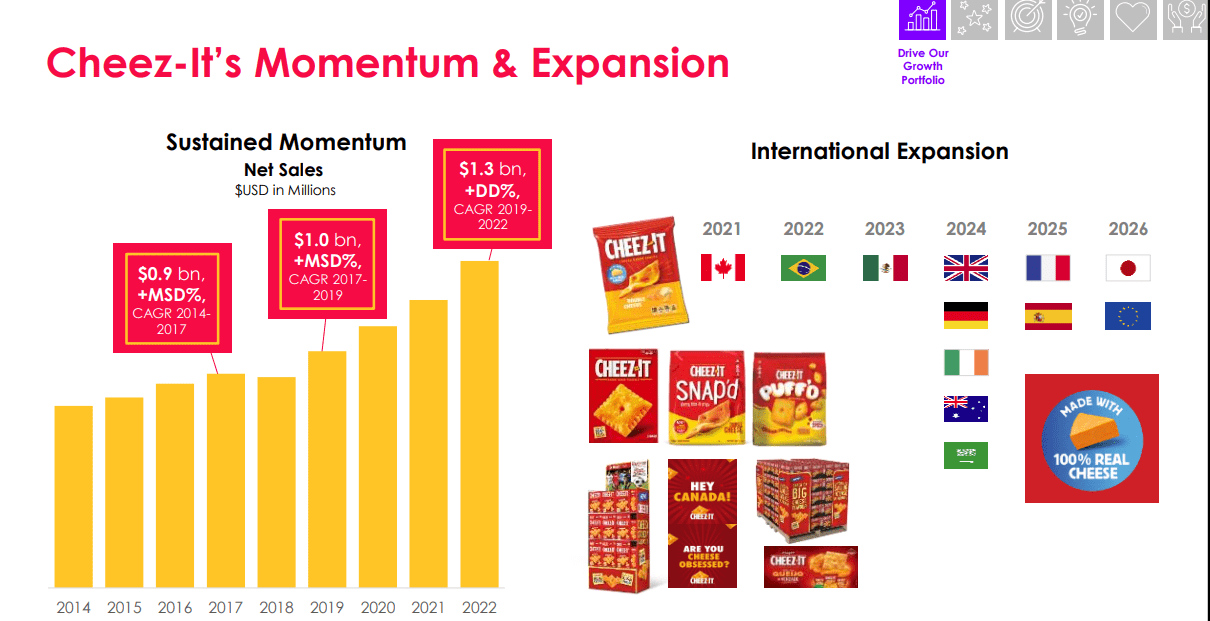

That is why, Kellanova's management is now pursuing a more aggressive expansion campaign of Cheez-it brand in Europe. Over the next few years, the company is preparing for growth in large markets, such as United Kingdom and Germany, followed by France and Spain in 2025.

{kind=link}

This would require significant investments in brand building activities in these markets, alongside logistics and other administrative expenses.

Overall, Kellanova's success in Europe is a big question mark and the company would need to significantly increase brand investment in the coming years. I also expect a more aggressive stance on large to medium-sized acquisitions going forward as management will need to expand the snacking portfolio.

Moving Up The Value Added Chain

Sustaining above peer-average topline growth will be a challenge for Kellanova going forward, but the company would also need to prove that it could sustainably improve its margins and avoid all the problems associated with being a low margin producer.

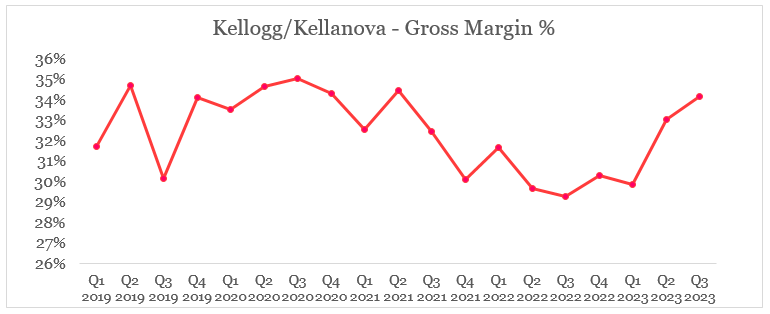

As inflationary pressures dissipated in recent quarters and the company was willing to sacrifice volumes at the expense of more aggressive pricing measures, gross margin experienced a significant tailwind over the past two quarters.

prepared by the author, using data from Investor Presentations

{kind=link}

Once again, we will need more information on a stand-alone basis during the next quarter, but given the high volume losses we saw above, the company would have to refrain from more pricing measures and would likely increase advertising and marketing spend in its efforts to regain market share.

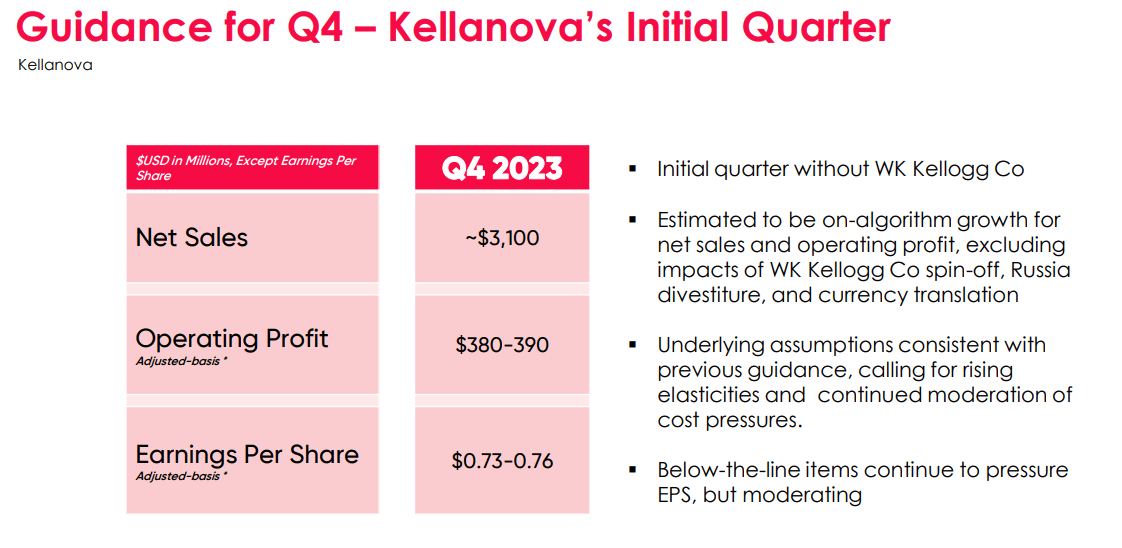

For the last quarter of this calendar year, Kellanova's management expects net sales of around $3.1bn and operating profit of roughly $385m (the midpoint of the guidance) which results in adjusted operating margin of 12.4%.

{kind=link}

Needless to say this is not materially different from the company's non-adjusted operating margin prior to the spin-off.

Seeking Alpha

This is still a long way to go before K can catch up with the leader in snacking - Mondelez, which has significant pricing power due to its strong global brand portfolio.

Seeking Alpha

Of course, Kellanova's lower margin profile is reflected within the company's conservative valuation multiples, but after everything said above I don't see a strong case for the company becoming a higher margin producer following the recent restructuring.

Seeking Alpha

Conclusion

After falling nearly 30% over the past 12-month period, Kellanova's share price is now attracting more investors looking for value in the newly rebranded and leaner organization. The snacking category is a highly attractive one within Packaged Food and the narrative around the stock is likely to gain momentum in the short term. Looking beyond that, however, I still see problems for Kellanova's topline growth and margins in FY 2024 which are the two reasons why I can't assign a buy rating yet.

For further details see:

Kellanova: The New Chapter Is Not As Exciting As It Might Seem